Brand Management Prognostications

Topics

The use of brands has been central to marketing for more than a century. The dominant logic has been “Build a brand, and the world will beat a path to its door.” Long-standing brands such as Marlboro, Coca-Cola, Xerox, IBM, and Intel are considered to be among the world’s most valuable assets. This precedent spurs diverse firms to base their strategies almost entirely on building brands. Car manufacturers, insurance companies, banks, and even industrial chemical producers are structuring themselves along brand and product lines, making brand managers responsible for the success of single brands or categories of products.1

Recently, many have questioned the wisdom of the brand management approach and the value of brands.2 In this article, we address the following issues:

- What is the point of marketing without brands?

- If brand managers are no longer responsible for brands, who is responsible?

- Is the brand-manager concept dead or merely ailing?

- Will brand management rise again, phoenix-like, in modified form?

We begin with the simple question: “What does a brand do?” That is, which functions do brands perform for the participants in a marketing relationship? We then identify the pressures that are influencing the evolution of brands and brand management and are leading to reappraisal of the brand-manager system. Finally, we identify three possible scenarios for brand management and their implications for firms that adopt them. We argue that only by focusing on the customer-oriented functions that brands fulfill3 can we gain some insight into the changes that may affect the evolution of both brands and brand management. Although we offer no definitive master plan for confronting the challenges posed by the demise of the brand manager, we find that common uncertainties must be alleviated, irrespective of the evolving organizational models.

Functions of a Brand

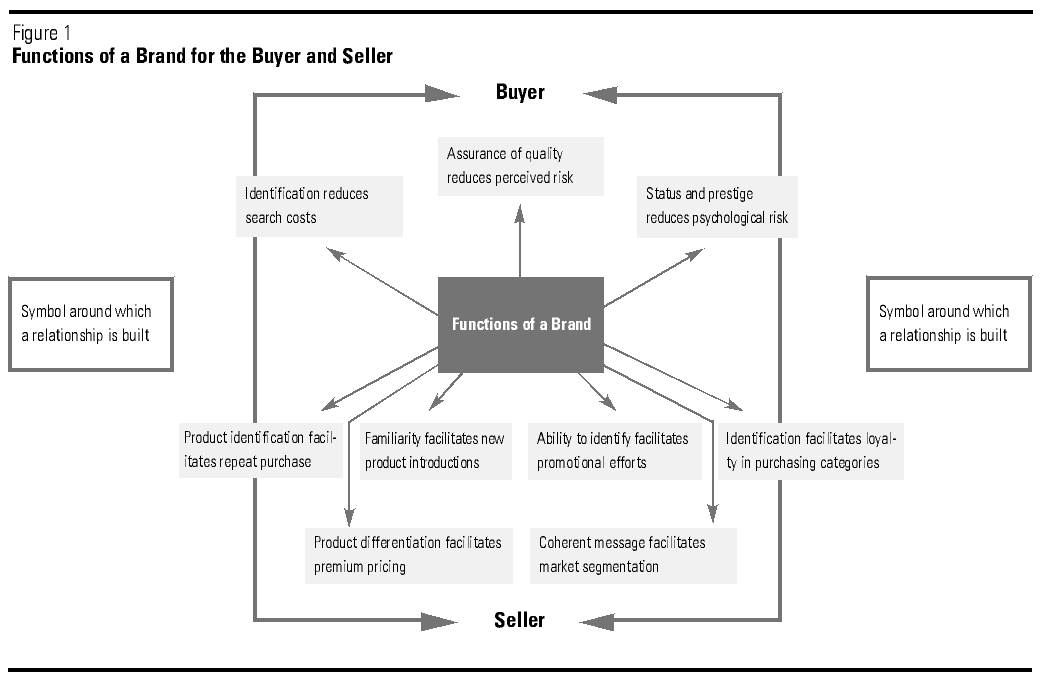

The quintessential function of branding is to create a distinction among entities that may satisfy a customer’s need. This primary distinction is the origin of a series of benefits for both the buyer and the seller4 (see Figure 1).

{kind=link}

For buyers, brands effectively perform the function of reduction: brands help buyers identify specific products, thereby reducing search costs and assuring a buyer of a level of quality that subsequently may extend to new products. This reduces the buyer’s perceived risk of purchasing the product.

References

1. Product and brand management issues remain high on the research priority list of the Marketing Science Institute, although they rank below marketing organization and processes.

Marketing Science Institute, Review (Cambridge, Massachusetts: Marketing Science Institute, Fall 1996).

2. “Death of the Brand Manager,” The Economist, 9 April 1994, pp. 67–68.

3. Throughout the paper, we use the term “customer” inclusively to subsume both the consumer and the trade customer. When discussing one or the other of these specifically, we identify them.

4. See, for comparison:

D. Aaker, Managing Brand Equity: Capitalizing on the Value of the Brand Name (New York: Free Press, 1996); and

P. Doyle, “Building Successful Brands: The Strategic Options,” Journal of Consumer Marketing, volume 7, number 2, 1993, pp. 5–20.

5. K.L. Keller, “Conceptualizing, Measuring and Managing Customer-Based Brand Equity” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 91–123, 1991); and

P.R. Berthon, N. Capon, and J.M. Hulbert, “Everything You Wanted to Know About Branding But Were Afraid to Ask” (University of Wales: Cardiff Business School, working paper, February 1998).

6. For a more detailed exposition on the functions of brands, see:

T. Ambler, “The Case for Branding” (London: London Business School, working paper, Stage 1 Report for CIM, October 1996).

7. G.S. Low and R.A. Fullerton, “Brands, Brand Management, and the Brand Management System: A Critical Historical Evaluation,” Journal of Marketing Research, volume 31, May 1994, pp. 173–190.

8. Harvard Business School, “Procter & Gamble Europe: Vizir Launch (1983)” (Boston: Harvard Business School, Publishing Division, Case 9-384-139, 1983).

9. A. Richards, “What Is Holding Back Today’s Brand Manager?” Marketing, 3 February 1994, pp. 16–17.

10. P. Weisz, “Major Marketers Reorganize Teams,” Adweek, 17 January 1994, p. 14; and

J. Lawrence, “Thinning Ranks at P&G,” Advertising Age, 13 September 1993, p. 2.

11. The Economist (1994).

12. B. Morris, “The Brand’s the Thing,” Fortune, 4 March 1996, pp. 28–38.

13. A.D. Shocker, R.K. Srivastava, and R.W. Ruekert, “Challenges and Opportunities Facing Brand Management: An Introduction to the Special Issue,” Journal of Marketing Research, volume 31, May 1994, pp. 149–158.

14. B. Saporito, “Procter & Gamble’s Comeback Plan,” Fortune, 4 February 1985, p. 30.

15. J. Liesse, “Slotting Bites New Products,” Advertising Age, 5 November 1990, p. 16.

16. R.C. Blattberg and J. Deighton, “Managing Marketing by the Customer Equity Test,” Harvard Business Review, volume 74, July–August 1996, pp. 136–144.

17. See, for comparison:

P.R. Berthon, L.F. Pitt, and R.T. Watson, “The World Wide Web as an Advertising Medium: Towards an Understanding of Conversion Efficiency,” Journal of Advertising Research, volume 36, January–February 1996, pp. 43–53.

18. P. Milgrom and J. Roberts, Economics, Organization and Management (Englewood Cliffs, New Jersey: Prentice-Hall, 1992), pp. 76–77.

19. T. Levitt, “Marketing Success Through Differentiation of Anything,” Harvard Business Review, volume 58, January–February 1980, pp. 83–91.

20. J. Deighton and K. Grayson, “Marketing and Seduction: Building Exchange Relationships by Managing Social Consensus,” Journal of Consumer Research, volume 21, March 1995, pp. 660–676.

21. V. Houlder, “Fingers That Shop Around,” Financial Times, 24 September 1996, p. 14.

22. “Software’s Holy Grail: No-Fuss Clicking Is What Consumers Need Most,” Business Week, 24 June 1996, pp. 50–53.

23. Houlder (1996).

24. We wish to acknowledge the contribution of an anonymous reviewer who pointed out this important shift.

25. L.L. Berry, E.F. Lefkowith, and T. Clark, “In Services, What’s in a Name?” Harvard Business Review, volume 66, number 5, September–October 1988, pp. 28–30; and

Morris (1996).

26. P. Sellers, “Brands: It’s Thrive or Die,” Fortune, 23 August 1993, pp. 32–36;

E. DeNitto, “Economy Puts Focus on ‘Value,’ Heinz Chairman O’Reilly Says, and That’s Bad for Food Brands,” Advertising Age, volume 1, number 4, 26 July 1993, p. 1.

G. Burns, “Restaurants: Bye-bye to Fat Times,” Business Week, 9 January 1995, p. 89;

A. Taylor, “Higher Rewards in Lowered Goals,” Fortune, 8 March 1993, pp. 75–78; and

A.J. Slomski, “Here They Come: Price-Conscious Patients,” Medical Economics, volume 83, April 1996, pp. 40–46.

27. D. Chanil, “A Year of Change,” Discount Merchandiser, January 1996, pp. 10–12.

28. P.R. Dickson, “Toward a General Theory of Competitive Rationality,” Journal of Marketing, volume 56, January 1992, pp. 69–83.

29. E. Tauber, “Brand Leveraging: Strategies for Growth in a Cost-Control World,” Journal of Advertising Research, volume 28, August–September 1988, pp. 26–30.

30. “Make It Simple. That’s P&G’s New Marketing Mantra — and It’s Spreading,” Business Week, 9 September 1996, pp. 56–61.

31. For details about this change in the United States, see:

W.M. Weilbacher, Brand Marketing (Lincolnwood, Illinois: NTC Business Books, 1995).

32. P.W. Dhar, and S.J. Hoch, “Why Store Brand Penetration Varies By Retailer,” Marketing Science, volume 16, number 3, 1997, pp. 208–227.

For example, in the United States, despite a significant increase in retailer concentration, the historical evidence suggests that brand manufacturers were holding their own in power terms, at least until the early 1990s. See:

P.R. Messinger and C. Narasimhan, “Has Power Shifted in the Grocery Channel?” Marketing Science, volume 14, number 2, 1995, pp. 189–223.

Most of the changes we are discussing have occurred since then, although in many cases the trends that spurred the changes were already in place.

33. A. Mitchell, “Managing by Our Shelves,” Marketing Week, 15 July 1994, pp. 30–33.

34. Aaker (1996).

Also see, for example:

L. Leuthesser, “Defining, Measuring and Managing Brand Equity” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 88-104, 1988);

K.L. Keller, “Conceptualizing, Measuring and Managing Customer-Based Brand Equity” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 91-123, 1991); and

R.K. Srivastava and A.D. Shocker, “Brand Equity: A Perspective on Its Meaning and Measurement” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 91-119, 1991).

35. For example:

M. Hammer and J. Champy, Reengineering the Corporation: A Manifesto for Business Revolution (New York: Nicholas Brealy, 1993); and

J.M. Hulbert and L.F. Pitt, “Exit Left Center Stage? The Future of Functional Marketing,” European Management Journal, volume 14, number 1, 1996, pp. 47–60.

36. Hulbert and Pitt (1996).

37. Aaker (1996).

38. Berry et al. (1988).

39. Economic profit is typically defined as operating profit minus a charge for capital used, computed on the basis of the company’s cost of capital.

Assuming an accurate cost accounting system (often a big assumption), economic profit contributes to increase shareholder value.

40. J.N. Sheth and R.J. Sisodia, “Feeling the Heat,” Marketing Management, volume 4, number 2, 1995, pp. 8–23.

41. Harvard Business School, Command Performance: The Art of Delivering Quality Service (Boston, Massachusetts: Harvard Business School Publishing, 1994), pp. 230–249.

42. J.R. Bettman, An Information Processing Theory of Consumer Choice (Reading, Massachusetts: Addison Wesley, 1979).

43. R.C. Blattberg and J. Deighton, “Interactive Marketing: Exploiting the Age of Addressability, Sloan Management Review, volume 33, number 1, Fall 1991, pp. 5–14;

D. Peppers and M. Rogers, The One-to-One Future: Building Relationships One Customer at a Time (New York: Century Doubleday, 1993).

44. D. Schultz, “A Better Way to Organize,” Marketing News, volume 12, 27 March 1995, p. 15.

45. Harvard Business School, “Grupo IUSACELL (A)” (Boston, Massachusetts: Harvard Business School, Case N9-395-028).

46. If a firm were to sell only a limited range of products or brands, this statement would not hold true. The importance of the distinction rises dramatically, however, as the range of products and/or brands increases. Given the size of large companies today and the worldwide trend to consolidate, this shift would have tremendous impact on most large multinationals.

47. At IBM and some other large business-to-business marketers, this shift has already occurred. For details, see:

N. Capon, “Organizing for Global Account Management” (New York: Columbia University Graduate School of Business, working paper, 1998).

48. Our thinking in this regard has been influenced by the terminology of

Peppers and Rogers (1993);

and, to a considerable extent, by Blattberg and Deighton (1996).

49. N. Capon, “Wachovia Bank and Trust Company,” The Marketing of Financial Services: A Book of Cases (Englewood Cliffs, New Jersey: Prentice Hall, 1992), pp. 24–39.

50. For comparison, see:

T. Peters, Thriving on Chaos (New York: Bantam Books, 1987).

51. Peppers and Rogers (1993).

52. Compare: J. Johanson and I. Nonaka, “Market Research the Japanese Way,” Harvard Business Review, volume 65, number 3, May–June 1987, pp. 29–32.

53. L.P. Carbone and S.H. Haeckel, “Engineering Customer Experiences,” Marketing Management, volume 3, number 3, 1994, pp. 8–19;

G.A. Churchill, R.H. Collins, and W.A. Strang, “Should Retail Salespersons Be Similar to Their Customers? Journal of Retailing, volume 51, Fall 1975, pp. 29–42; and

A.G. Woodside and W.J. Davenport, “The Effect of Salesman Similarity and Expertise on Consumer Purchasing Behavior,” Journal of Marketing Research, volume 11, May 1974, pp. 198–202.

54. The New York Times reported on Morgan Stanley’s reorganization, recounting that the firm “is trying to simplify the way it deals with major corporate clients” by grouping together its debt, equity, and investment banking departments into one “client-driven and not product-driven” structure. “Shadowing Industry Trends, Morgan Stanley Creates 2 Big Divisions,” The New York Times, 17 January 1997, p. D1.

55. S.F. Slater and J.C Narver, “Becoming More Market Oriented: An Exploratory Study of the Programmatic and Market-Back Approaches” (Cambridge, Massachusetts: Marketing Science Institute Report No. 91-128, 1991).

56. F. Gouillart and F. Sturdivant, “Spend a Day in the Life of Your Customers,” Harvard Business Review, volume, 72, number 1, January–February 1994, pp. 116–125.

57. Hulbert and Pitt (1996).

58. See, for example:

General Electric Company, “1990 Annual Report of the General Electric Company” (New York: General Electric Company, 1990); and

Procter & Gamble, “1995 Annual Report of Procter & Gamble” (Cincinnati: Procter & Gamble, 1995).

59. “Technology: Quiet Revolution,” Financial Times, 26 March 1996, p. 10.

60. K. Simmonds, “Marketing as Innovation: The Eighth Paradigm,” Journal of Management Studies, volume 23, September 1986, pp. 479–500.