Corporate Responsibility Audits: Doing Well by Doing Good

Topics

Many companies spend significant time and effort developing a mission statement — complete with vision, values, goals, and strategies. Ask managers whether their firm’s mission statement lives in the company day-to-day or whether it lies neglected in someone’s desk drawer. In too many instances, the truthful answer is: “The vision is more rhetoric than real.”

This is not because the company’s managers are neglectful or “bad people.” Indeed, most managers would say they are doing their best to exemplify the values in these documents and achieve the vision. However, in-depth investigations of company practices, even in the best of firms, frequently reveal large gaps between stated values and daily practices.

We propose that auditing a company’s core operating practices by using a responsibility audit may help to bridge this rhetoric-reality gap. Such an audit assesses a company’s overall performance against its core values, ethics policy, internal operating practices, management systems, and, most importantly, the expectations of key stakeholders — owners, employees, suppliers, customers, and local communities. Such audits alert companies to responsible business practices that will help them simultaneously “do well (financially) and do good (socially).”

Vision versus Practice

As part of a recent beta test of a responsibility audit process, eight companies assessed those operating practices that related to implementing their stated vision, values, and mission. All eight had award-winning environmental, health, and safety (EHS); human resources; or corporate giving practices. However, they all discovered significant gaps in four operating areas: employee relations, quality systems, community relations, and environmental practices. When comparing their corporate core values with employees’ core values, they uncovered organizational cultures that inadvertently contributed to the rhetoric-reality disconnect.

The eight audits consistently revealed that when a company adopted proactive, responsible practices, it reaped measurable improvements in efficiency and productivity, lowered legal exposure and risks to the company reputation, and reduced direct and overhead costs.

Responsibility auditing, also called social auditing, can help corporations uncover these gaps and proactively improve their management practices. Consider the following:

- A leading regional insurer had a higher-than-industry-average employee turnover in competitively paid, highly demanding, and stressful customer service positions. An assessment and cost-benefit analysis of employee policies, practices, and the quality management system estimated that recovering just half of the turnover costs of employee overtime, temporary help, and outsourcing due to turnover would increase the insurer’s annual profit by 7 percent. As recommended by the audit, the company increased professional development and career opportunities for customer service employees and became a “feeder pool” for local companies that needed experienced, well-trained customer service representatives. By investing in the employability of these workers, the company improved job satisfaction, reduced turnover, and generated a new — albeit small —income stream from local firms.

- A Fortune 500 firm, undergoing an intense management change, conducted a social audit of its operations. Facing the probability of future layoffs, the audit helped the company identify ways to assist adversely affected employees, reduce “decision under fire” inefficiencies, and avoid potential legal action and employee violence. By improving access to health-care benefits for the remaining employees, medical costs were reduced by $450,000 and absenteeism by 10 percent. Recommended improvements in the quality management system will shorten production-cycle time, thus reducing operating costs and increasing production capacity. These will increase output per employee and manufacturing capacity an estimated 200 to 300 percent within 3 to 5 years.

- A leading multinational manufacturing company that had won numerous environmental awards analyzed its EHS policies, as well as the EHS practices of one of its safest plants. The audit pointed out that the manufacturer could reduce the plant’s high regulatory-compliance costs by adopting waste elimination practices. Furthermore, in addition to obviating the need for some EHS training for employees, this change in practices inherently improved communication and coordination among the production, research and development, and sales departments. The strategy saved the plant an estimated $200,000 annually, increased production capacity by 25 percent, and reduced disposal costs and water use by 50 percent.

The responsibility audit process used in these cases helps companies operationalize their mission statements in ways that simultaneously increase profitability (doing well) and reduce risk with its associated damage (doing good). These audits highlight where implementing better operating practices, beyond mere regulatory compliance, can improve both the bottom line and relationships with stakeholders.1 Both types of improvement can better align vision, values, and reality.

Responsibility audits, however, evoke two radically different attitudes. Managers may view them with distaste — seeing them as necessary evils that highlight problems needing correction. Or they view them constructively, as part of continual company improvements that lead to acting more responsibly and improving overall corporate performance. This latter “both/and” logic suggests that social responsibility and corporate financial performance go hand in hand, rather than being trade-offs.2 Although there may be costs associated with socially responsible practices, even the relatively few audits conducted to date indicate that benefits outweigh costs. Current research on the social-financial performance linkage, as well as the relationship between corporate reputation and the quality of stakeholder relations, indicates that the link between financial and social performance is indeed a positive one. At worst, there seem to be few negative consequences of behaving responsibly.3

Despite the potential benefits of responsible practices, business persists as usual in many companies. The current business climate is characterized by restructuring and layoffs, which have negative consequences for local communities, employee morale, productivity, and customer relationships. Although companies have dramatically increased the rhetoric about valuing employees, international investigative bodies, activists, and journalists continue to uncover human rights abuses in both industrialized and newly industrializing nations. In addition, severe environmental degradation remains a concern along with other problems identified by critics of corporations.4

The ongoing gap between the rhetoric of well-meaning vision statements and the reality of their implementation suggests that the link between well-treated stakeholders and significant corporate profits is not well established. Most managers continue to view profitability and responsibility as a trade-off, which hinders them in shifting from the tyranny of “either/or” to the logic of “both/and.”5 However, demonstrating the positive bottom-line impacts will convince managers to move toward more socially responsible business practices.

Acting Socially Responsible

Companies intent on aligning their mission statement with reality can use a process to determine ways to add value by acting responsibly and then implement the resultant strategies over time. It is an ongoing process of continual improvement for the entire organization6 — not a one-shot, add-on program —because vision/practice alignment is not a “once then done” program. Well-treated, satisfied stakeholders lead to better performance and more likely achievement of strategic goals.

However, don’t confuse doing good with corporate philanthropy, because responsible management practices have broader and more powerful impacts. When a company undertakes daily activities expediently with little regard for consequences, those who suffer are the “extended corporation” — that is, the employees, customers, and suppliers who interact with the corporation regularly. Such actions adversely affect communities that supply the enterprise’s infrastructure and sometimes the natural environment, too. Eventually, the business owners suffer, perhaps by paying fines for abuses, by adhering to stricter regulations to curb excesses, or through loss of productivity and customers due to negligent practices. Responsible management practices in these areas are thus far more important than philanthropic contributions.

Although being responsible is good management, examples of the gap between rhetoric and reality are numerous despite obvious alternatives. Companies develop hurtful employee policies (such as developing a reputation for layoffs or discrimination) that make recruitment difficult or turnover high instead of choosing policies that retain highly skilled and knowledgeable workers. They carelessly design products, which results in great waste, though careful design consumes less resources and produces fewer byproducts. They develop shoddy products that lead to customer returns, lawsuits, complaints, and potential safety and liability problems, rather than focusing on quality and adding value, satisfying customers, and gaining repeat business. Companies treat their local communities and the environment as temporary stopping (or, perhaps more accurately, stomping) grounds, grabbing tax breaks and other benefits, when the synergy of good corporate-community relationships and becoming a “neighbor of choice” instills goodwill and strengthens positive long-term community relations.7

We measure corporate social performance by examining the way companies regularly treat stakeholders (essential for the firm’s existence), governmental entities (that provide the necessary infrastructure), and the society at large. Corporate responsibility can thus be subject to external or internal audits. Many executives appear to focus on the apparent cost of audits or the difficulty of making corporate changes instead of focusing on the hidden costs of socially irresponsible practices. These costs include waste, retention problems, recruitment costs, lost customers, acquiring new customers, lost productivity, poor quality, and more expensive transactions. Unless these costs are specifically identified through a responsibility audit, they remain hidden, and firms either do not consider them or believe them to be just “part of doing business.” Thus, the questions are: How can we evaluate corporate behavior with respect to stakeholders and society? How can we make these hidden costs more apparent? And how do we encourage socially responsible practices?

Measuring Socially Responsible Performance

Measures of socially responsible performance exist. For example, investors in socially responsible organizations have long presumed there is value in such companies, or, at a minimum, there is social value in avoiding products or services — or even entire companies or industries — that operate irresponsibly or take risks deemed objectionable or “incalculable.”

Incalculable societal risks include producing socially or individually harmful products (such as cigarettes, nuclear equipment, or military arms) or promoting socially questionable activities (such as gambling or operations conducted in countries suspected of human rights violations).8 To meet the needs of socially oriented investors, some investment houses and pension management companies — such as Trillium (formerly Franklin Research and Development), Calvert Funds, and TIAA-CREF — have developed “social screens” to identify corporate activities that socially responsible investors want to avoid.

For example, Kinder, Lydenberg, Domini (KLD) has developed a set of externally derived screens that covers ten categories, including some that can be considered “stakeholder categories,” such as employee relations, community relations, environment, diversity, and products. In addition, KLD staff members research certain areas associated with the incalculable risks noted earlier. Being externally derived, KLD data is advantageous because it is somewhat more “objective” than internally derived measures, it is consistent year-to-year, and it covers a wide range of companies (e.g., all of Standard & Poor’s 500 largest firms).

The Council on Economic Priorities (which is oriented toward consumer products) and social investment firms and associations (which are sometimes faith-based) also employ researchers who investigate relevant corporate social performance, focusing on specific investor issues. Researching employee relations involves documents supplied by companies (such as annual, environmental, community relations, or social reports) as well as public sources (media reports, U.S. Security and Exchange Commission filings, legislative and legal actions, and so on).

Social auditing began in the 1940s with external audits.9 The result of a social audit is typically a company rating that covers such items as employee policies, union relationships, community relations practices, philanthropy, volunteer programs, and other community-based activities. Similarly, an environmental rating might assess recycling, reuse, and reduction policies (such as 3M’s Pollution Prevention Pays Program), as well as Superfund designation10 or environmental fines incurred.

External assessments cover most large publicly traded firms these days, but company-specific and internal responsibility audits are less common.11 Internal audits fell into relative disuse from the 1980s until the mid-1990s. Today’s social audits, also called responsibility audits, encompass both the external perspective (for stakeholder perceptions of firm performance) and the internal perspective of traditional financial audits.12 Some companies that undertake these audits also release social reports on their findings. Recent examples are Ben & Jerry’s Ice Cream and The Body Shop.13 Ben & Jerry’s 1998 Social Performance Report, for example, compared the company’s progress toward achieving management’s 1998 goals as well as progress in key improvement areas cited in the 1997 social performance assessment. One such workplace goal was “to recruit and retain people of color.” The company lost four such managers in 1997, yet retained a 3 percent proportion of people of color on staff in 1998, which is slightly above the percentage of minorities living in the firm’s home state of Vermont.

The premise behind social responsibility audits is that responsibility pays off handsomely in profitability and productivity. This premise can, in fact, be calculated in monetary terms by incorporating costs buried in overhead, turnover rates, insurance costs, regulatory costs, and in other non-value-added expenses. Here are some examples. Companies that do not pollute are not fined and do not pay the associated legal fees; that is a cost savings. Companies that treat their employees with respect have employees who work harder, are more productive, and stay with the company longer; they avoid the costs of absenteeism, turnover, and other forms of lost productivity. Companies that provide quality and value in their goods and services have customers who continue to buy those products and services. Companies that treat local communities well reap many returns, including better schools, fewer local restrictions, and a better infrastructure to support the firm. In the long term, these decrease corporate operating costs.

Audit Methodology

Companies such as Ben & Jerry’s have received considerable attention, not all of it positive, following their much publicized social audits. In part, the notoriety may have resulted from “weak methodology and lack of rigor.”14 To overcome these charges, new methodologies are beginning to appear. The New Economics Foundation (NEF; based in the United Kingdom, where there is a much greater focus on social accountability than in the United States) and SmithOBrien, in Cambridge, Massachusetts, have developed such methodologies. NEF audits perceptions of key stakeholders about a firm’s practices, products, and impacts. SmithOBrien’s audit quantifies strategic and financial effects of corporate operating practices by assessing those practices and interviewing stakeholders. Fombrun, in his work on corporate reputation at New York University, also uses a stakeholder-based perceptual methodology.15

In the United States, audits generally focus on discovering how a company’s bottom-line performance improves through more responsible social practice. Typically, they are undertaken with the help of social auditing consultants. Basically, responsibility auditing involves systemically identifying the real and full costs of various policies and practices, and later benchmarking those practices against the best practices of other organizations and the expectations of key stakeholder groups. Generally, people think of costs as being product-driven or compliance-driven, while missing those that are stakeholder-driven.

Developing a Responsibility Audit

A holistic responsibility audit focuses on four areas: quality management systems, environmental practices and energy conservation, human resources and human rights, and community relations.

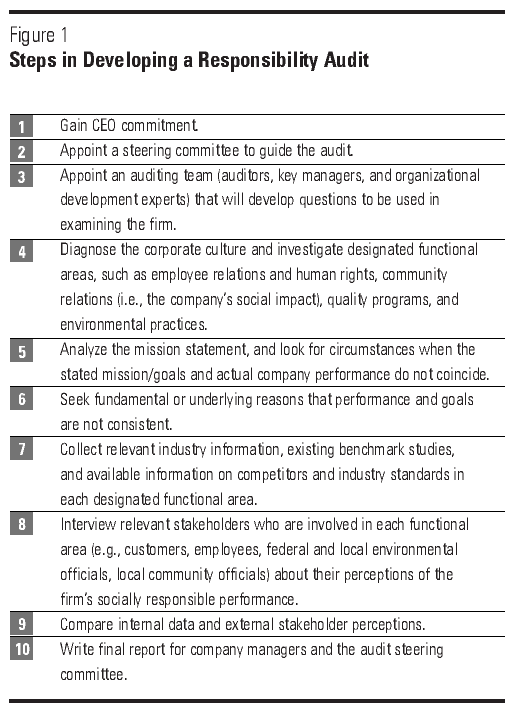

In developing a responsibility audit, the CEO’s commitment and involvement is key. (See Figure 1 for steps in developing a social audit.) Next is the appointment of an audit committee comprising internal managers which either serves as a steering committee or performs the audit. The audit team needs to assess the corporate culture and analyze the extent to which the organization’s vision and mission statements are being realized. The diagnosis process dissects the mission statement into stakeholder elements; existing policies, practices, and cultures are then assessed in light of the mission statement. A typical holistic audit covers, at the least, customers, employees, product or service quality, local communities, and the environment. Other stakeholders can be added, depending on the company’s circumstances and its industry’s concerns.

{kind=link}

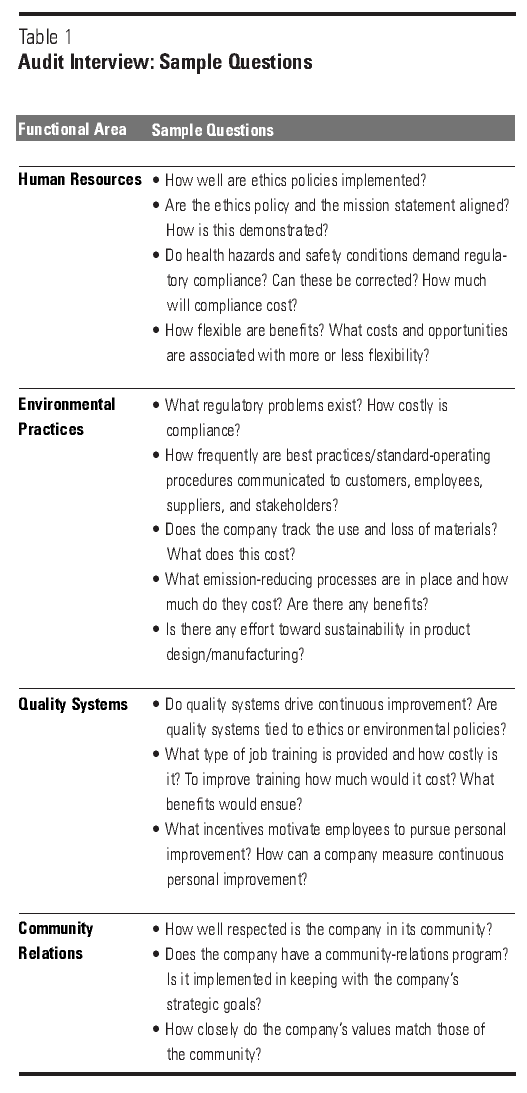

Interviews with key individuals in different functions uncover vital information about practices. An internal audit team comprises auditors, experts in the functions being audited, and organizational specialists. These multiple perspectives encourage brainstorming, which can uncover overlooked effects. The team should design a consistent set of questions for the interviews so that the data can be compared across units (see Table 1). Concurrently, the audit team collects relevant industry, regulatory, and client data in a benchmarking form to determine how the company compares with others.

{kind=link}

In the quality management area, the audit team asks questions about the company’s performance measures and management systems, customer responses, supply-chain management practices, and level of senior management and employee involvement in quality management. Other questions might cover product labeling (ingredients), extent of independent testing and certification, product/service liabilities, sustainable development, and statistical process controls.

In the area of human resources, audit questions address many topics, including the organization’s capacity to “live” its core values. Topics include: recruitment practices and costs; diversity practices; health and safety records (including violations and fines); employee turnover; policies and procedures relating to promotions, wages, and benefits; decision making; grievances; response to violence; downsizing; human rights; and contractor outsourcing. Detailed information about suppliers, large stockholders, stock analysts, peers, community leaders, media contacts, and regulators are also useful.

When problems are uncovered (pertaining to quality, wasteful environmental practices, retention and recruitment, or customer interactions), the audit team must think about the underlying hidden costs. Replacing a disgruntled employee, for example, leads to costs in reviewing résumés, interviewing, advertising, and decision making; the real costs of turnover and low morale may be unknown. Likewise, the company might save money by recycling paper or even reduce paper usage through more electronic communication. Use of activity-based costing helps an audit team understand the costs associated with problem areas, as well as the possible bottom-line benefits of changing practices. Although using activity-based costing alone will not make a company more socially responsible, it may help managers identify unused capacity and reduce the waste of materials and labor, thereby lowering overhead costs.

The audit team then submits a progress report to the CEO and steering committee, stating key findings and suggesting changes of greatest value to the company. The team highlights “low hanging fruit,” that is, instances where simple changes toward more-responsible practices would dramatically improve the bottom line. Combining internal and external views provides a reasonably holistic picture of a firm’s day-today impact on its customers, suppliers, environment, employees, and community. Adding the financial benefits of operating more responsibly illustrates how owners benefit as well.

Responsibility Auditing in Practice

A simple example illustrates how a responsibility audit adds value to a company. A small plant of a Fortune 500 multinational manufacturer — which had won numerous EHS awards — had revenues of $3 million from producing some 300 formulated products. Despite the plant’s environmentally sound reputation, the audit team identified a potential savings of $197,000 and the feasibility of a 25 percent increase in plant capacity.

The audit team included an EHS expert who specialized in pollution prevention, a quality management systems consultant, and an accountant with expertise in activity-based costing. The team interviewed key plant employees, including the general manager, health and safety specialists, and a production manager. They combined the results of their interviews with a review of environment and safety records, production schedules, and expense reports.

The audit team learned that frequent EHS compliance training required for all plant employees resulted in production shutdowns. These disruptions not only decreased output, but also required that equipment be shut down and then restarted. Meanwhile, the salesforce was under pressure to double company sales by the year 2000, so some salespeople were overselling and promising rush orders. Customers returned oversold products, and the firm could not fill some rush orders, partly because of the shutdowns. These production disruptions also caused human resource problems. To stay within the annual operating budget, plant employees worked longer hours to fulfill orders. But, on the subsequent mornings, the plant was shorthanded because these employees were allowed to come to work late.

Finally, the audit team identified communication breakdowns among the R&D, production, and EHS departments. For example, R&D would send new or improved product specifications to the plant for prompt manufacture without regard for financial, operational, or environmental consequences. This resulted in production scheduling problems.

The audit team also recommended waste elimination practices, which obviated some EHS regulatory training and decreased production disruptions. It also recommended including plant and sales managers in annual strategic planning initiatives that would reduce customer returns and hence lower disposal costs. The team also urged R&D, production, and sales to work closely together at the start of new product development to avoid later problems. Finally, the team recommended an operational improvement — adding a double-lined piping system so that delivery trucks could pump raw materials from the truck directly to the plant which would eliminate demurrage charges for deliveries of raw materials and prevent spillage.

Broader Perspective on Activities

As the example above illustrates, operating responsibly is not highly complex. In general, it is possible to improve day-to-day operating practices simply by taking a broader perspective on activities and allocating indirect or hidden costs to each area, as follows:

- In human resources, eliminate hazardous health and safety conditions that could attract regulatory-agency attention. Assess whether employee rights are respected, whether flexible benefits exist, and whether the company has appropriate grievance procedures.

- In the environmental arena, identify, reduce and/or entirely eliminate the root causes of EHS regulatory compliance. Improve the monitoring of suppliers, waste handlers, and contractors. Track the use and loss of materials, reduce emissions, and eliminate waste.

- Make similar efforts in the quality and community relations arenas.

Although human resources practices are typically consistent across company units, it is best to examine environmental and production practices at the business-unit or plant level. This is where specific costs and potential benefits are embedded, and where firms must implement recommendations for improvement. Including key decision makers on the steering committee and asking them to participate in the audit can be critical to gaining their buy-in during implementation.

Implementing the Vision

The comparative data in the 1995 Collins and Porras study of “built to last” companies16 suggests that most companies have neither the vision needed for success nor a link between their stated vision and the reality of their operating practices. The visionary companies that Collins and Porras studied are long-lived, and it appears that these companies implemented their visionary practices early and adhered to them over many years.

Other companies begin less auspiciously, realizing later the importance of aligning a clear shared vision and mission statement with socially responsible operating practices. As companies change, alignment of practices with the current core purpose and mission is necessary. Redirecting corporate practices seems akin to turning around an oil tanker; it requires planning, timing, attention to implementation, and great foresight. Responsibility audits can be of help in highlighting ways to align vision, rhetoric, and practice on a day-to-day basis.

Managers are traditionally reluctant to implement responsibility performance measures, fearing that good social performance may negatively affect financial performance. Yet example after example demonstrates that operating responsibly saves money and, in some cases, even creates profitable new opportunities. The payback to the audited companies that we studied was between six and twenty times the audit cost over periods of 6 months to 3 years. The companies consistently found that interacting responsibly with their primary stakeholders caused them to operate more responsibly and more profitably.

Responsibility audits are a management tool for demonstrating the potential qualitative and financial benefits of mirroring core values and ethics in practice. They direct managers’ attention to socially responsible practices that meet the expectations of primary stakeholders. Achieving the benefits rests on creating an adaptive and proactive corporate culture from the top down. Such proactive management helps avoid normally hidden costs and liabilities that come from reacting to problems as they occur. Moreover, operating responsibly is — or can be — a core business strategy, one in which core operating functions are considered strategic, and stakeholder relationships and financial performance are allowed to grow.

References

1. R. Edward Freeman popularized the stakeholder concept in his 1984 book. See:

R.E. Freeman, Strategic Management: A Stakeholder Approach (New York: Basic Books, 1984).

2. Collins and Porras highlight this theme of “both/and” versus an “either/or” orientation in their book. See:

J.C. Collins and J.I. Porras, Built to Last: Successful Habits of Visionary Companies (New York: HarperCollins, 1997).

3. For some current research, see:

J.B. Guerard Jr., “Is There a Cost to Being Socially Responsible in Investing?” Journal of Investing, volume 6, Summer 1997, pp. 11–18;

J.B. Guerard Jr., “Additional Evidence on the Cost of Being Socially Responsible in Investing,” Journal of Investing, volume 6, Winter 1997, pp. 31–36;

J.J. Angel and P. Rivoli, “Does Ethical Investing Impose a Cost upon the Firm? A Theoretical Examination?” Journal of Investing, volume 6, Winter 1997, pp. 57–61;

S.A. Waddock and S.B. Graves, “The Corporate Social Performance-Financial Performance Link,” Strategic Management Journal, volume 18, number 4, 1997a, pp. 303–319;

S.A. Waddock and S.B. Graves, “Quality of Management and Quality of Stakeholder Relations: Are They Synonymous?” Business and Society, volume 36, September 1997, pp. 250–279; and

L. Kurtz, “No Effect, or No Net Effect? Studies on Socially Responsible Investing,” Journal of Investing, volume 6, Winter 1997, pp. 37–49.

For summaries of research, see:

M.L. Pava and J. Krausz, “The Association Between Corporate Social-Responsibility and Financial Performance: The Paradox of Social Cost,” Journal of Business Ethics, volume 15, 1996, pp. 321–357; and

D.J. Wood and R.E. Jones, “Stakeholder Mismatching: A Theoretical Problem in Empirical Research on Corporate Social Performance,” International Journal of Organizational Analysis, volume 3, July 1995, pp. 229–267; and

J. Frooman, “Socially Irresponsible and Illegal Behavior and Shareholder Wealth: A Meta-Analysis of Event Studies,” Business and Society, volume 3, 1997, pp. 221–249.

4. For some interesting critiques of the modern corporation, see:

C. Derber, Corporation Nation (New York: St. Martin’s Press, 1998);

W. Greider, One World, Ready or Not: The Manic Logic of Global Capitalism (New York: Touchstone Books, 1998); and

David Korten, When Corporations Rule the World (San Francisco: Berrett-Koehler Publishers, 1995).

5. For extensive discussion about the concept of mental models or stereotypes, see:

P. Senge, The Fifth Discipline: The Art and Practice of the Learning Organization (New York: Doubleday, 1991). Also, see:

Collins and Porras (1997).

6. Fisher and Torbert discussed how continuous and continual improvement differ in: D. Fisher and W.R. Torbert, Personal and Organizational Transformations: The True Challenge of Continual Quality Improvement (London: McGraw Hill, 1995).

7. The term used for such positive and proactive community relations is “neighbor of choice.” See: E.M. Burke, Corporate Community Relations: The Principle of the Neighbor of Choice (Westport, Connecticut: Praeger, 1999).

8. Lydenberg and Paul argue that such risks are perceived to be “incalculable” by certain investors, and hence they will avoid investing in companies producing such risks. See:

S. Lydenberg and K. Paul, “Stakeholder Theory and Socially Responsible Investing: Toward a Convergence of Theory and Practice,” in 1997 Proceedings of the International Association for Business and Society, J. Weber and K. Rehbein, eds. (Destin, Florida: International Association of Business and Society, 1997), pp. 208–213.

9. For the history of social auditing, see:

K. Davenport, “Social Auditing: The Quest for Corporate Social Responsibility,” in J. Weber and K. Rehbein, eds., 1997 Proceedings of the International Association of Business and Society (Destin, Florida: International Association of Business and Society, 1997), pp. 197–207; and

T.J. Kreps, Measurement of the Social Performance of Business. Monograph No. 7: An Investigation of the Concentration of Economic Power for the Temporary National Economic Committee (Washington, D.C.: U.S. Government Printing Office, 1940).

10. In the past, people were less aware of how dumping chemical wastes might affect public health and the environment. On thousands of properties where such practices were intensive or continuous, the result was uncontrolled or abandoned hazardous waste sites, such as abandoned warehouses and landfills. Citizen concern about this problem led the U.S. Congress to establish the U.S. Environmental Protection Agency Superfund Program in 1980 to locate, investigate, and clean up the worst sites nationwide.

11. For example, CEP’s database covers 320 companies that produce consumer goods, some large and some small. KLD’s database covers all 500 Standard & Poor’s companies, plus another 150 or so that are included in the Domini Social Fund, which has passed KLD screening.

12. Cited in Davenport (1997), see:

H.R. Bowen, Social Responsibilities of the Businessman (New York: Harper, 1953).

13. Companies whose strategies depend on social responsibility are at significant risk of notoriety if their performance is questioned, as investigative reporter Jon Entine’s continuing commentary on Ben & Jerry’s and The Body Shop highlights. He has critiqued The Body Shop for ethical and environmental practices that appeared to contradict the company’s stated policy and image. More recently, Entine has criticized Ben & Jerry’s in a series of articles about the company’s marketing claim that Rain Forest Crunch and other products benefit indigenous peoples. See:

J. Entine, “The Body Shop: Truth or Consequences,” Drug & Cosmetic Industry, volume 156, February 1995, pp. 54–59.

The New Economics Foundation conducted The Body Shop’s social audit. For an overiew of the audits that NEF conducts, see: www.neweconomics.org/main/tools/social.htm

14. Davenport (1997), p. 199.

15. For current information on reputation management, see:

www.reputations.org/

See also:

C. Fombrun, Reputation: Realizing Value from the Corporate Image (Boston: Harvard Business School Press, 1996).

16. Collins and Porras (1997).