Managing Foreign Exchange for Competitive Advantage

GENERALS PLANNING military action and CEOs plotting corporate strategy often start from the same point: they identify the key strengths and weaknesses of their position vis-à-vis their rivals and develop a strategy to exploit the strengths and protect the weaknesses. In the corporate world many factors come into play, including quality of product, service, and availability, but two factors stand out because of their direct effect on the bottom line: pricing and cost of production. Senior managers across a wide spectrum of industries devote considerable thought to optimizing these two factors, but often ignore or underestimate a powerful force that influences them: the relative value of the currencies in which revenues and costs are denominated.

In the Bretton Woods world of stable exchange rates, currency values were less significant.1 At that time, pricing and volume determined revenues and relative labor and material costs determined production decisions. Today the world is different. Many U.S. corporations with large international businesses have seen their stock prices drop because investors have feared that a strong dollar would reduce the contribution of overseas operations to sales and earnings growth. Exporters in the United States are worried that a stronger dollar will cut into their profit margins.

Despite these developments, corporate management has been slow to grasp the full importance of foreign exchange movements. While most multinational firms are quite active in the foreign exchange market, they expend most of their effort protecting their near-term reported results, and they allow relatively low-level managers to make decisions about their foreign exchange activities. This is unlikely to continue. The increasingly global structure of the world economy and the increased volatility of exchange rates will make it imperative that firms use foreign exchange as a strategic tool in the battle for worldwide market share and profits.

The Evolving Global Market

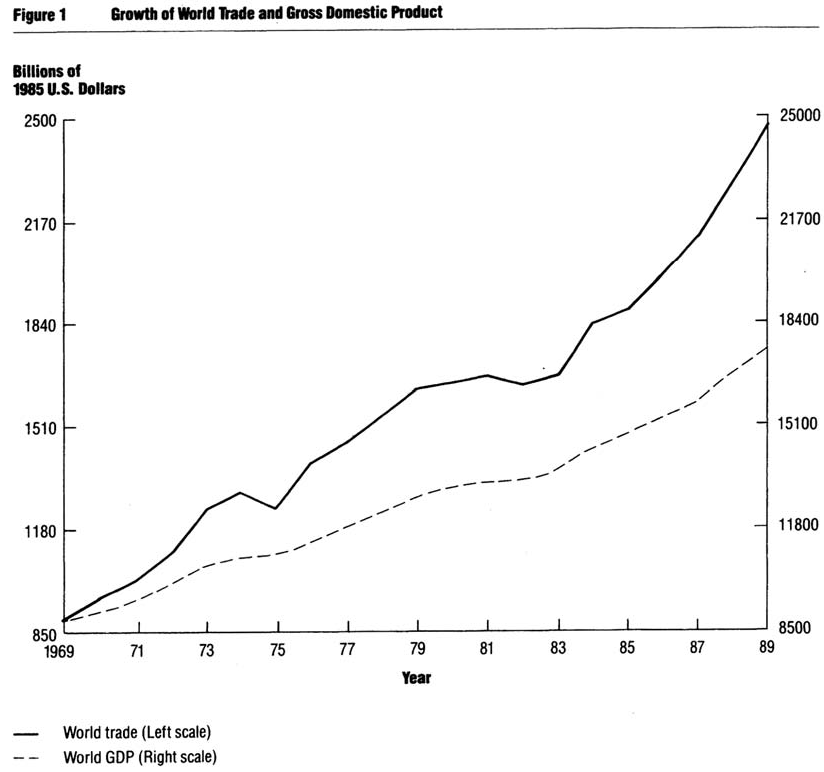

Although globalization means different things to different businesses, there is no debate that it is happening. Figure 1 compares the growth of world trade with that of world gross domestic product (GDP) over the last twenty years, assuming parity in 1968. Worldwide reductions in trade barriers, the effects of the General Agreement on Tariffs and Trade (GATT), and increasingly specialized manufacturing have increased the value of goods travelling across borders faster than the actual production of those goods has increased. In 1988 alone, world trade grew by over 8 percent, while world GDP is estimated to have grown by 4.5 to 5 percent. Geographic boundaries no longer represent market barriers to the same extent they once did. In cases such as the United States-Canada Free Trade Agreement and the 1992 changes in the European Economic Community, the walls are coming down.

{kind=link}

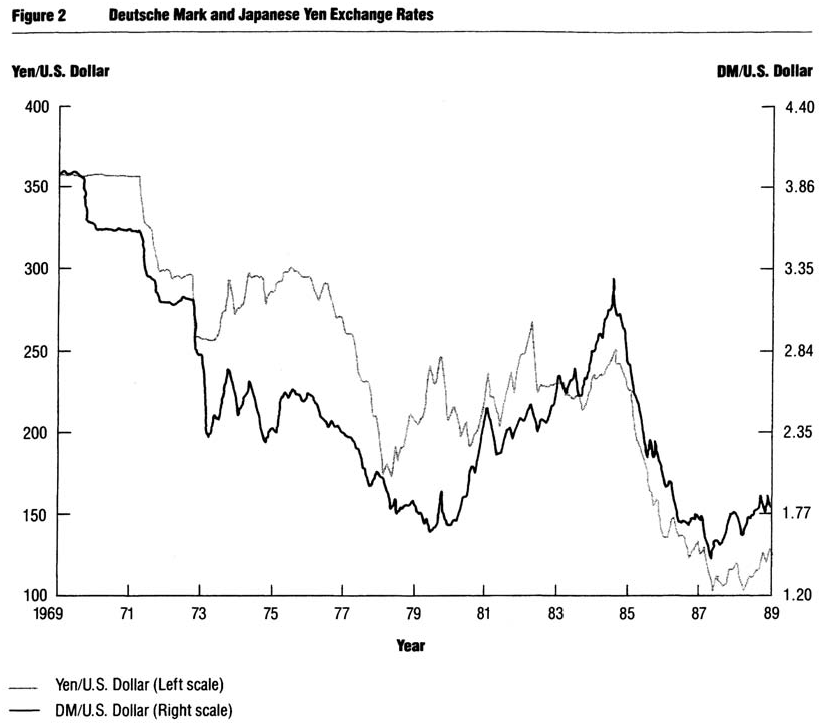

At the same time, currency values, which are the price denominators of goods crossing borders, have become increasingly volatile. One way of looking at this is to consider the range of values of a currency in a given year. The range of the dollar value of the deutsche mark, for example, in each of the seven years prior to 1971, and under the influence of the Bretton Woods agreement, averaged only 3.5 percent of the value at the start of their respective years. Through the rest of the 1970s, with floating exchange rates, the same range averaged over 13 percent, while the 1980s have seen it rise again to over 20 percent.

The same trend can be seen by mapping the Japanese yen and deutsche mark exchange rates with the dollar over the same period (see Figure 2). No longer are currency movements minor blips on a generally straight line. Instead they represent dramatic changes in prices and costs that can be prime determinants of profitability in internationally competitive markets.

{kind=link}

Stock analysts began to notice this in 1989. They paid increased attention to the effect of exchange rates on the dollar value of profits earned overseas in other currencies. For example, a U.S. company earning 50 percent of its profits in Europe would suffer a 5 percent reduction in its net income if the European currencies declined by 10 percent during the year, simply on the translation of overseas profits. Although this kind of analysis only scratches the surface of the effects of foreign exchange on profits, it is clearly a harbinger of the greater attention that will be paid in the 1990s to the influence of exchange rates on the profits, cash flow, and share price of corporations.

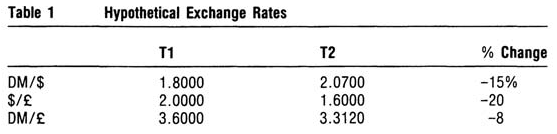

A simple illustration will show how changes in foreign exchange rates affect a corporation’s strategic competitive position. Let us assume that three companies, from the United States, Germany, and the United Kingdom, are competing for the German market for telephone switches. Each company manufactures in its home country and has a sales organization in Germany. What will happen to the profit margin and net income of each if the mark declines by 15 percent against the dollar and the pound declines by 20 percent?

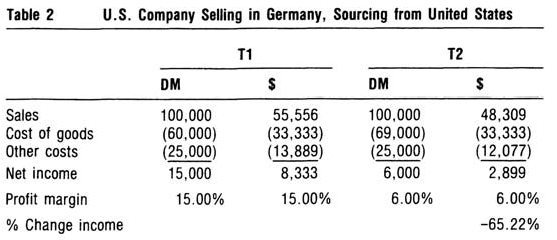

Table 1 shows the exchange rates at time T1 and T2. Tables 2 through 4 show the income statements of each of the companies before and after the exchange rate changes. We have assumed no changes in pricing or local costs, so the sole variable is currency. Note first that the U.S. company in Table 2 has seen its cost of goods sold rise from DM 60 million to DM 69 million, reducing its margin from 15 percent to 6 percent and decreasing its net income by a whopping 65 percent, from only a 15 percent change in the currency.

{kind=link}

{kind=link}

{kind=link}

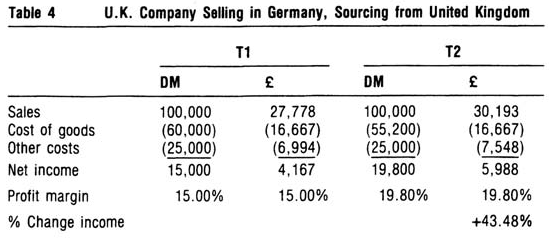

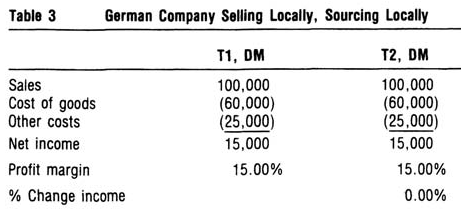

The German company in Table 3 seems unaffected, since both its revenues and costs are denominated in marks. This would also illustrate the position of a U.S. multinational with a production site in Germany whose costs were also denominated in marks. Table 4, however, shows that complacency on the part of the German company would be a mistake; the British company’s profit margin has increased to almost 20 percent and its net income is up over 43 percent, giving it the financial power to strengthen its position in the marketplace through advertising, promotions, capital spending, or price cutting.

{kind=link}

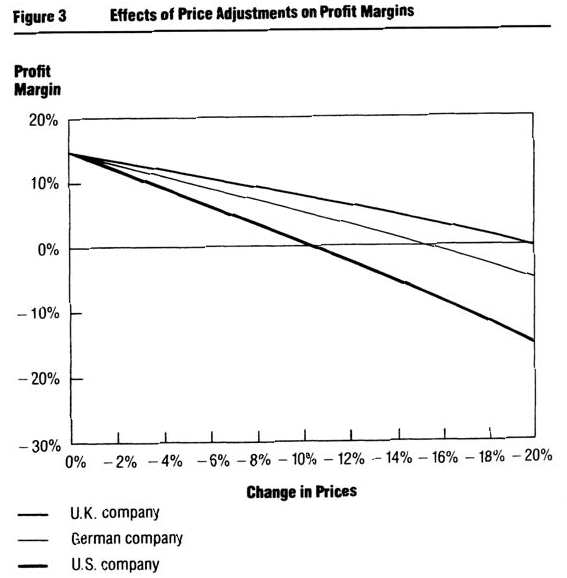

Taking this example a step further, Figure 3 shows the effects on each firm’s margins if, for every 1 percent change in the pound’s value, the British company cuts prices by 1 percent and the Americans and Germans are forced to follow or lose market share. The U.S. company, with the double whammy of adverse currency and price movements, begins to lose money when the pound declines by 10.4 percent or to a rate of ¥1.79 in our example. Many other actions and reactions are possible in this scenario and, obviously, several variables may be at work to mitigate or exacerbate the results. The conclusion, however, is clear: currency levels have a major effect on the competitive position of firms in the global marketplace.

{kind=link}

But what industries are significantly affected by foreign exchange? One measure is foreign sales as a percent of total sales in a given industry, including both sales from overseas operations and exports. Table 5 shows that such diverse industries as tobacco, cosmetics, and computer systems make over 50 percent of their sales outside the United States, while a very large portion of U.S. industry does over 20 percent of its turnover overseas.

{kind=link}

We already have examples from a number of industries that have been negatively affected by exchange rates. The battle in heavy equipment manufacturing between Caterpillar and Komatsu during the 1980s is a classic case. Although Caterpillar had manufacturing facilities around the world, it still depended heavily on U.S. production. Komatsu sourced mainly from Japan. In 1979 Caterpillar was the low-cost producer in the industry, but by 1985 most of its product lines were priced over 40 percent above Komatsu’s, mainly because the dollar had increased by 50 percent over the yen and most key European currencies. It is no coincidence that Komatsu was able to penetrate many of Caterpillar’s traditional markets, especially in the United States. The resulting decline in market share and profit margins weakened Caterpillar’s financial situation and caused its credit rating to be reduced three times. Finally, a weak dollar in 1986 gave the price relief and improvement in competitive position that led to a credit upgrade in 1987.

The U.S. automobile industry, especially Chrysler, felt the effects during the first half of the 1980s. Despite the “voluntary” agreement by the Japanese to limit automobile exports, U.S. companies saw their share of the domestic car market tumble from 88 percent in 1979 to 69 percent in 1987, partly because the strong dollar allowed Japanese manufacturers to price their cars lower.

During the same period, foreign film manufacturers, especially Fuji Photo Film, made significant inroads into several markets. Eastman Kodak estimates that the strong dollar cost it $3.5 billion between 1980 and 1985 in terms of lost market share, inability to penetrate new markets, and lower profit margin. 2

Granted, some businesses, such as utilities and life insurance, feel minimal effects, but a lack of international sales may mask a significant exposure. Table 1 shows that the steel industry has few overseas sales, but that industry is well aware, from bitter experience, of the major role foreign exchange played in increasing foreign producers’ market share in the United States. A strong dollar made U.S. producers less competitive; it affected their ability to penetrate new markets, their market share, and their margins and profits. Foreign exchange was not the sole cause, nor the sole solution, to the steelmakers’ woes, but it played a significant part.

Even a business with no foreign exchange flows in its operations can be affected by the movement of currency values. The fact is that virtually every company exposed in some way to the international marketplace will find its competitive standing altered by major foreign exchange movements.

This type of exposure fits within the standard definition of economic exposure, which is the degree to which the present value of a firm’s future cash flows can be influenced by exchange rate fluctuation.3 Our discussion goes, however, beyond the usual consideration of dealing with known or expected future cash flows denominated in foreign currency. The strategic exposure to foreign exchange is directly linked to a business’s competitive position in a market and how currency movements affect the various competitors differently. In some businesses, such as parts of the pharmaceutical industry, governments may control pricing or patents. When there is no real competition in the marketplace, foreign exchange has much less of an impact. In most businesses, however, relative exposure, how a company’s exposure differs from that of its major competitor, is a real concern. Traditional definitions of exposure concentrate solely on foreign currency flows that relate to the company’s own operations. The company develops hedges to protect against exchange losses that can be identified upon conversion. This internal focus totally ignores the fact that an unfavorable currency movement may not be just unfavorable; it could also be favorable to the competition.

A strategy that recognizes the effects of exchange rates on competitive position is a key offensive tool in a global marketplace in which currency movements may affect the various players differently. Such a strategy helps ensure cost and price competitiveness in each market and protects and improves margins and market share. Corporations that fail to use this tool in a timely and effective fashion run a substantial risk of loss of competitive position.

The Impact of Foreign Exchange

Consolidation of companies through international acquisitions, mergers, and alliances has effectively reduced the number of competitors in most markets for many industries. Consequently, the same major players are squaring off against each other in practically every country. Increased global competition in both domestic and foreign markets has led corporate planners to think in terms of a global strategy, especially when a firm’s competitive position in one country will eventually affect its position in other countries. Since currency movements affect each competitor differently, foreign exchange has now taken on strategic importance.

When companies strive for competitive advantage, they usually think of improving product quality and value, providing better service, and achieving lower cost position. Where the market does not perceive product superiority, margins are sustainable only through lower cost. However, where product superiority or differentiation exists, companies can improve margins by commanding superior prices and lowering costs. Since foreign exchange is often the denominator of both revenues and costs in overseas business, longer-term corporate profitability and shareholder value are clearly affected by exchange rate movements.

There are four basic cost categories: research and development (R&D), production, marketing and sales, and capital-financing. In at least three of the categories, foreign exchange can have a significant impact. Research and development is often centralized, and hence, costs mostly originate in a single currency. But in economic terms, these costs are distributed throughout the firm regardless of its locations. When the currency denomination of R&D is different for the competition, exchange rate movements have a built-in structural impact on comparative costs.

Where foreign sourcing is involved in production, the local currency value of raw materials and components affects the cost of the finished product. Many companies attempt to eliminate such foreign exchange impact by negotiating sourcing contracts in local currency, thereby passing on the exchange risk to the supplier. This practice is often fruitless; suppliers constantly attempt to pass back their perceived exchange risk or actual hedging cost to the buyer.

Even where sourcing is done locally, currency movements can give a comparative cost advantage to the competition if its sourcing is denominated in a weak foreign currency. Whether or not a firm can remain a lower-cost producer in a given country is greatly determined by the extent to which production costs originate in different currencies for both the firm and its competition. Although exports from countries with lower labor and other production costs can be more competitive, especially if they originate from weak currency countries, local producers usually have a built-in advantage by their proximity to the ultimate customer.

Costs associated with marketing, sales, distribution, administration, and overhead are mostly denominated in local currency; exchange rate movements play a far lesser role with them. However, exchange rates do affect the base currency value of such costs, and hence, the consolidated earnings of the company.

Capital-financing cost is complex when firms based in different countries are compared. The cost of capital is not only a function of interest costs but also exchange rate movements, especially since a multinational company today can tap the global capital market for its financing needs. Local and consolidated cash flow, earnings, and debt-equity ratios are all affected by the currency of financing. Consequently, how the capital structure of foreign subsidiaries is financed will affect shareholder value.

For example, the British subsidiary of a U.S. firm may borrow sterling locally to finance a new plant, or have the parent borrow dollars at a lower interest rate and provide an intercompany sterling loan. From the subsidiary’s point of view, the only difference is the lender, since it receives sterling in either case. From the corporate viewpoint, the net liability is in dollars in the latter case, instead of sterling, to finance the same sterling fixed asset. The subject is further complicated because the accounting profession allows U.S. companies to insulate their profit and loss statements (P&L) from the currency impact that could arise from borrowing dollars to finance a sterling asset by taking exchange gains and losses directly to the equity account, bypassing the P&L, thereby equating two different financing actions from the perspective of the reported income statement.

Companies that pursue a market share strategy must be prepared to expand capacity locally or source from elsewhere. However, sustaining margins depends on maintaining high capacity utilization. External sourcing, intracompany or third party, is preferred in certain cases until market share is well entrenched. If sourcing originates from a foreign country, foreign exchange becomes an important strategic consideration.

As for revenue, the currency denomination of pricing can be an important factor in building sustainable competitive advantage. A company that insists on pricing in its own base currency instead of the local currency of the customer, as in the case of the aircraft industry, which mostly bids in dollars, could find itself at a competitive disadvantage even when all other players price in the same currency if their respective base currencies are different. Companies selling products that force customers to pay in the seller’s currency, rather than the currency of the market, may also lose market share to more aggressive competitors who are prepared to price in a foreign currency and manage the resulting risk.

The Corporate Response

Despite general agreement among corporate foreign exchange managers and academicians that foreign exchange has these pervasive effects, relatively few corporations have set out, in a thorough and disciplined manner, to quantify and manage them. Considering the magnitude of the problem, the obvious question is, “Why are so few paying attention?”

Some U.S. corporations would say that they have taken steps to reduce their exposure to currency movements for years by diversifying their manufacturing base around the world. These steps have usually involved building a plant for export in an Asian or Latin American country with low production costs, or building a plant in Germany to serve the German market. These corporations usually made the low-cost decision, however, without ensuring that currency movements would not take away the cost advantage. While they decided to manufacture in Germany at least partially to match the currency of costs and revenues, they often ignored the competition’s activities. In both cases, they did not make detailed analyses of the currency flows or take actions to ensure that present advantages would extend into the future.

One important reason that U.S. managers pay little attention to foreign exchange as a strategic issue is their lack of education and understanding of the subject. A recent survey shows that corporate directors in the United States see international experience as increasingly crucial to success in the 1990s.4 But U.S. senior managers have far less international experience than their European and Japanese counterparts. Consequently, they rarely include foreign exchange as part of their strategic vision.

Perhaps the most important reason that foreign exchange is not fully utilized is the smokescreen provided by the accounting profession’s treatment of the subject. Statement of Financial Accounting Standards (SFAS) 52, with its emphasis on known cash flows and balance sheet items, has forced corporations to focus on transaction exposures and, occasionally, translation exposure. Transaction exposures are generally defined as assets, liabilities, revenues, and costs originating in currencies other than the functional currency of the entity, which could generate exchange gains and losses from currency movements, thereby affecting the local and consolidated P&L statements. Translation exposure is generally defined as the local currency value of equity in each entity, which could generate exchange gains and losses from currency movements upon translation into dollars, affecting the special equity section of the consolidated equity. In general, CEOs expect their treasury groups to manage the “foreign exchange gains/losses” line on the quarterly P&L statement to avoid losses or large swings that would have to be explained to shareholders and analysts. Unfortunately, confining the accounting impact of foreign exchange to one line of the P&L lulls executives into believing that their currency exposure is neatly contained, rather than permeating almost all the lines on the P&L, as it does for international companies and many domestic ones as well.

But SFAS 52 deflects the foreign exchange issue even further. For those corporations that grasp the importance of foreign exchange to the long-term profitability of their businesses, the accounting profession makes it extremely difficult to take financial actions to deal with strategic exposure. The problem is that it is often hard to connect these exposures to known future cash flows. Without that connection, hedging activities designed to mitigate real economic risks require regular marking to market. Revaluing hedges at current market rates on balance sheet dates is likely to cause wide swings in quarterly earnings, as the transactions designed to protect a company’s competitive position over a period of years is telescoped onto the P&L each quarter. One could debate whether it is SFAS 52 or the emphasis on quarterly earnings that is the real culprit, but the result is the same: corporations wanting to take strategic currency actions are confronted with a set of obstacles that many cannot overcome.

Many corporations discovered in 1989 and 1990 that they had a new kind of foreign exchange exposure which we call “CEO exposure” CEO exposure relates to a chief executive’s need to provide various constituencies, including the board, stock analysts, credit rating agencies, and others, with some parameters about projected growth in sales and profits in the next few years. The more international a company’s business, through overseas sales or foreign competition, the more these projections (and hence the CEO’s credibility) will hinge on exchange rates. Companies with high price earning multiples and large international operations, such as drug and high-tech companies, were particularly hurt by this in 1989. With their stock prices dependent on strong growth in revenues and earnings, and international nondollar flows representing a large portion of that growth, these companies watched their market valuations plummet as analysts correctly perceived that a rising dollar would reduce the value of overseas sales and profits when translated back to dollars.

A striking example occurred in September 1989 when John Akers of IBM announced that earnings would fall short of analysts’ estimates and cited three reasons, one of which was the strengthening dollar. The price of IBM’s stock declined by $6 per share on the day of the announcement and another $2.50 the following day in an otherwise rising market. The net result was a reduction in IBM’s market capitalization of over $5 billion. Similarly, in late May 1990 a Wall Street analyst cut his earnings estimates on four major drug companies, all of which earned well over 50 percent of their profits overseas. The sole reason was the appreciating dollar. He removed two of the four stocks from his “buy” list for the same reason, and the group as a whole lost over $1.6 billion in market capitalization in one trading day, purely on the expectation of negative currency translation effects on overseas earnings.

Consequently, a number of corporations began to hedge future foreign net income, and in some cases revenues, with currency options, in order to lock in their translated dollar values at budgeted rates.5 Since these hedges often cover the entire year’s projected income, accounting results for each quarter could have considerable earnings fluctuations if all the hedges are marked to market at quarter-ending exchange rates. These companies sought the less precise language of SFAS 80 on accounting for futures contracts, instead of SFAS 52 on translation of foreign currency transactions, in order to allow their accountants to treat these options as hedges, and defer their unrealized interim gains and losses for reporting purposes. However, in August 1989, the Securities and Exchange Commission (SEC) issued its interpretation on the subject, effectively disallowing the deferred accounting treatment when it involved hedging in the functional currency of the overseas operation, which the vast majority of the cases did.

Setting aside the controversy surrounding the accounting treatment, we would argue that hedging the translated dollar value of future earnings is not equivalent to managing a company’s strategic currency exposures. The focus on translation of foreign currency income into dollars ignores the longer-term effect of exchange rate movements on a company’s ability to improve sales and margins in a competitive environment. The important point, however, is that the absence of an accounting result that isolates the strategic impact of currency movements on earnings is probably the single most important reason that U.S. corporations have failed to use foreign exchange as a competitive tool.

The difficulty of quantifying foreign exchange considerations has also limited attention to it. Unlike transaction and translation exposure, which are precisely defined in relation to known cash flows and asset values, strategic exposure must be defined in terms of many variables, most of which are dynamic and impossible to measure with absolute precision. Consequently, it has been acceptable for senior management to blame poor results on “the effects of changes in exchange rates” without having to answer the seemingly obvious question, “Why didn’t you do something about it ahead of time?” The quantifying problem also gives the guardians of financial reporting the basic principle of conservatism on which to base their defense of the status quo: if you can’t measure it, it doesn’t exist in accounting terms, so you can’t hedge it. The fact is that a company’s strategic foreign exchange position can be measured to a large extent, but very few companies have seriously tried. Companies that make this effort, however, have found that their analysis yields new methods for achieving deferred accounting treatment for their foreign exchange strategies.

Managing Foreign Exchange in the 1990s

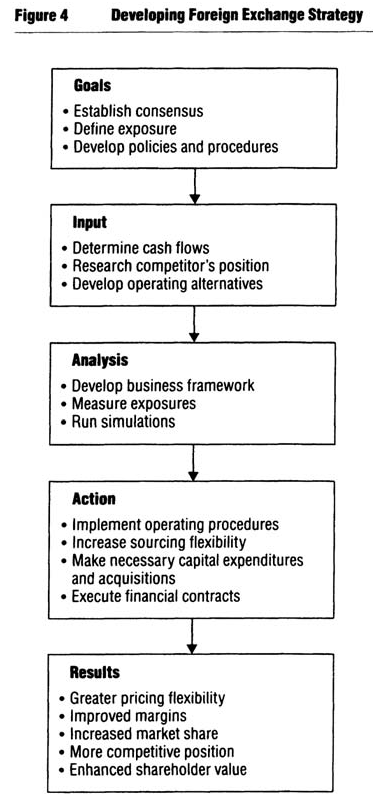

In order to succeed in the coming decade, corporations will need to utilize any competitive advantage their foreign exchange positions may give them and guard against currency movements with negative impacts. The following steps, summarized in Figure 4, represent the basic course of action required to accomplish this, with examples of companies that have taken this approach:

{kind=link}

Define corporate foreign exchange objectives and policy.

Talking to managers in major corporations, we are consistently surprised by the lack of a common perception among senior management, operating divisions, and treasury staff of the corporate objectives in managing foreign exchange. Most corporations have not established foreign exchange objectives beyond the management of known transaction exposures. They have usually not identified or attempted to manage the crucial effects of currency movements on profit margins over a longer period of time. Also, companies often ignore other lesser but still important factors, such as the distinction between optimizing dollar cash flow and earnings per share.

The first step in developing strategy is to establish a consensus within the organization of what needs to be done and who is responsible for each part. How will exposure be defined and what methods can be used to deal with it? The company must distinguish between strategic currency exposures affecting the company’s ability to sell profitably in each market and the after-sale impact of currency movements on translated revenues and costs. Both types of exposure need to be managed, and policy and procedures must be established for gathering the required information on an ongoing basis so that decisions can be made with accuracy and dispatch. As a result of this process, a greater understanding will develop among all concerned of the impact foreign exchange will have on the corporation’s business.

One of the first U.S. companies that recognized the need for a strategic approach in foreign exchange was Eastman Kodak. Following the difficult strong dollar years in the early 1980s, Kodak’s senior management embarked on an evaluation of its existing foreign exchange management policy, bringing in new staff and an outside consultant. Out of the process came an entirely fresh approach to currency management that, for the first time, made the key distinction between strategic and tactical exposures. The board finance committee approved the policy document and management expended considerable effort into communicating it to line managers in all of Kodak’s diverse businesses.

Measure strategic foreign exchange positions and evaluate divisions and individuals on their performance.

Strategic foreign exchange positions differ from traditional accounting exposures in that they are an integral part of a business’s operations and require the combined efforts of operating and financial experts to determine risks and opportunities. Companies need to analyze their position in specific product markets. They must collect information on sourcing alternatives, production capacity, market pricing, demand sensitivity, and all the other items that create or avoid a foreign exchange impact on the business. The same basic intelligence should be gathered on the competition, since it is the comparative advantage relative to one’s competitors that drives market share and margins.

The Stanley Works, a Connecticut-based multinational manufacturer of tools and hardware, has seen an increasing share of its sales and profits generated overseas, as well as increased competition from Europe and the Far East. Corporate treasury took the initiative and worked with the most internationally involved division to integrate the foreign exchange management program with the division’s longer-term strategic plan to protect its leading market position and enhance its margins. The number of products and markets and the diverse competition complicated the analysis, but ultimately a computerized model was constructed that could perform sensitivity analysis under differing exchange rate, operating, and financial scenarios. As the final step, Stanley developed a strategy to protect its competitive position and long-term earnings.

A simple illustration of the measurement process may be helpful at this point. Consider the Canadian business of a U.S. automotive parts company, which we will call XYZ International, with a manufacturing facility in Canada and a finishing plant in the United States. XYZ serves the Canadian market mainly with its manufacturing facility in Canada, and only 20 percent of its cost of goods sold originates in U.S. dollars. XYZ’s major competitor is a U.S. corporation that sources from the United States nearly 70 percent of its cost of goods sold in Canada. A stronger Canadian dollar will give advantage to the competitor, as it has more U.S. dollar sourcing. From a strategic viewpoint, the relative exposure between the two companies may be quantified as 50 percent of the cost of goods sold in Canada.

Once the company collects and analyzes the data, it can construct solutions, both financial and operating, to maintain and possibly enhance its competitive position. In the case of XYZ, two attractive solutions presented themselves, one a financial strategy that took advantage of the significant forward discounts on the Canadian dollar, and one a shift in some manufacturing activity to a U.S. plant with excess capacity. The company eventually decided that the change in manufacturing site was the best long-term strategy.

It is critically important when implementing long-term foreign exchange strategies to create a performance evaluation system within the company that measures the performance of divisions and individuals on factors over which they have decision-making power. The corporate treasury group may have full responsibility for handling accounting exposures, but operating units need to see the costs and benefits of strategic actions.

Link foreign exchange to business planning and develop a proactive approach.

To be fully exploited as a strategic tool, foreign exchange must be considered a part of long-term business decisions such as marketing and capital expenditure plans. It must be viewed as a major element in a firm’s competitive position, rather than simply a risk to be hedged away. The processes described above need to become a regular part of the firm’s strategic thinking in addressing the dynamics and uncertainties of the business.

Companies must consider strategic foreign exchange issues at the same time they make other strategic decisions, not after the fact. In the planning process they need to identify the strategic currency exposures for each product line in each country. This process will lead to an understanding of the corporation’s aggregate exposure to exchange movements. Companies must develop a currency management program that best supports their corporate goals and that is consistent with the marketing objective and the trade-off between market share and margins in each situation. When they can identify the worst case scenario, companies can plan with the knowledge that the only unplanned results of currency movements will be favorable ones.

Like Kodak and Stanley, which have successfully integrated strategic foreign exchange management with their operating plans, General Electric Company has been encouraging its more-or-less autonomous business units to do the same. At GE Plastics, a $5 billion company, foreign exchange is always considered, along with manufacturing, marketing, and distribution, when capital spending or new product plans are developed. Top management participates actively in the process.

Conclusion

In order to be a global winner, it will be necessary to use all the weapons available. Foreign exchange must be considered one of these weapons. CEOs need to understand and get involved in strategic foreign exchange management for two primary reasons. First, because foreign exchange rates have a major effect on margins, market share, cash flow, and investor’s perceptions, the effective management of foreign exchange will play an important role in maximizing shareholder value. Second, the effective execution of strategic foreign exchange policy cuts across functional lines and requires the combined efforts of different parts of the organization, including financial and operating units. Such action is most likely to require top management leadership and a clear mandate for the corporate treasury.

Some aggressive companies will take the importance of foreign exchange to the extreme and attempt to exploit foreign exchange trading as a business of its own, hoping to make speculative profits in the process. Such activity has little to do with strategic management of foreign exchange. By the same token, corporations should not shrink from aggressively using the currency markets as they fine tune their analyses of the risk-reward trade-offs between being hedged and unhedged and the multitude of positions in between.

It is clearly impossible to predict currency movements with a high degree of reliability. Companies do and should consider the future value of the Japanese yen and other relevant currency, and should be prepared to take them into account as they develop foreign exchange strategies. But it is crucial to first understand their own foreign exchange positions and how a range of currency movements will affect the ultimate value of their businesses. Only then can they develop hedges to minimize the risk from possible adverse currency movements, while still maintaining conditions that would contribute to improving their competitive positions.

Currency movements have put companies out of business before and will do so again, probably with even greater frequency. Global competition will see to that. Companies that take the time now to analyze their strategic foreign exchange position to prepare for the future will be on the right track to be winners in the competitive global markets of the 1990s.

References

1. Representatives of forty-four nations met in Bretton Woods, New Hampshire, in 1944 to forge the Bretton Woods Agreement that established the International Monetary Fund and the International Bank for Reconstruction and Development.

2. The Economist, 4 April 1987, p. 81.

3. J. Madura, International Financial Management, 2d ed. (St. Paul, Minnesota: West Publishing, 1986), p. 249.

4. Egon Zehnder International, Inc., “1989 Directors Survey,” Corporate Issue Monitor 4 (1989): 3.

5. With the recent adoption of SFAS 105, which deals with the disclosure of information about financial instruments with off balance sheet risk, outside analysts should be better able to identify the financial actions taken by individual compa-