Strategy as Options on the Future

“It is a great piece of skill to know how to guide your luck even while waiting for it.” — Baltasar Gracián (1601–1658)

In 1984, The Economist asked sixteen people — four finance ministers, four chairman of multinational companies, four Oxford University economics students, and four London dustmen (or garbage collectors) — to generate ten-year forecasts. They were the kinds of forecasts that underpin many long-term, strategic plans: the average growth rate in Organization for Economic Cooperation and Development countries over ten years, the average inflation rate in OECD countries, the exchange rate between pound sterling and the U.S. dollar, the price of oil, and the year when Singapore’s GDP per capita would overtake Australia’s (double Singapore’s at the time). In 1994, The Economist checked the sixteen people’s forecasts against what had actually happened.

On average, the forecasts were more than 60 percent too high or too low. The average forecasted price of oil, for example, was $40 compared with an actual price of just $17. All the respondents said Singapore’s GDP per capita would never overtake Australia’s, but that had actually happened in 1993. The most accurate forecasters were the London dustmen and the chairmen of multinational companies (a tie for first place); the finance ministers came in last. But the performance of every group was quite abysmal. The unpalatable fact is that no one can predict the long-term economic and market environment with any real accuracy.

Yet many strategic plans are meticulously constructed on these foundations of sand, perched on top of forecasts that, in all probability, will prove to be hopelessly off the mark. Consider how many companies approach strategic planning: The numbers in the long-term plan are dominated by a sales forecast that is produced by product and customer type or region (often a projection of around five years); the companies then allocate the investment to business units consistent with achieving the long-term sales forecast. Then they compute the implied costs and profits, and the process iterates until they produce an acceptable “long-term plan.” The plans often include erudite SWOT analysis (strengths, weaknesses, opportunities, and threats) or other market and trend analyses, but the decisions are made on the basis of forecast sales, investments, and costs.1 The forecasts are often heavily influenced by straight-line projections with forecasts of sales growth of existing products in existing markets. This implies that the company will maintain significant percentages of its costs as fixed, so that when these are spread over the greater sales volume, profits will grow.

The large forecast error in projecting variables like those in The Economist experiment and, hence, sales levels over the long run creates problems for the kind of strategic planning I described above.

Companies will tend to overinvest in building assets and capabilities that are highly specific to a particular strategy, relative to what would be optimal if the planning approach explicitly acknowledged that its forecasts would most likely be off the mark. A framework that encourages planners to optimize the configuration of investments on the assumption that they know the sales volume for particular products and markets will underinvest in flexibility.

By making investment decisions on “single line” forecasts, a company risks becoming a prisoner of its existing investments in capabilities and market understanding. Rapidly repositioning a company when investments in the capabilities and market knowledge necessary have not been made in advance will leave it like “an aircraft carrier turning on a dime.” The company will suffer “diseconomies of time compression” (extra costs of trying to accelerate the rate of change).2 Contrast this with a company that has invested in experiments to understand potential new markets and in seeding new capabilities (such as a small-scale project to supply a particular product direct to customers). These investments, and the learning they produce, effectively create a portfolio of strategic options on the future, a series of alternative “launching pads” that the company can use to rapidly change its strategic direction in response to market developments. A competitor that has aligned its investments with a single, and different, trajectory will struggle to catch up in the race to reposition.

For example, in 1990, USX (formerly United States Steel) had the choice of investing in new equipment to gain experience in a new steel-casting technology — compact strip production (CSP) — or in equipment using its traditional hot-rolling technology. USX chose to invest further in the hot rolling. A competitor, Nucor Steel, piloted the CSP technology and, in the process, created an option not available to USX. Commenting on USX’s ability to catch up once CSP had proven successful, Nucor’s CEO remarked: “It will take them two years to build a plant and another year to get it running properly. We’ve got at least three-and-a-half to four years on them.”3

My message is that, while companies may focus on executing a single strategy at any point in time, they must also build and maintain a portfolio of strategic options on the future. Building that portfolio of options requires investments in developing new capabilities and learning about new, potential markets. By putting in place a set of strategic options on the future, a company will be able to reposition itself faster than competitors that have focused all their investments on “doing more of the same.” But this requires changes to traditional strategy processes and a new way of thinking about how planning and opportunism interact in determining strategy.

Next I discuss a strategy that embodies a coherent portfolio of options, sketch a process managers can use to develop this kind of strategy, and explain how planning and management opportunism can reinforce each other. Establishing a portfolio of future options involves four main steps:

- Uncovering the hidden constraints on the company’s future.

- Establishing processes for building new strategic options.

- Optimizing the portfolio of strategic options.

- Combining planning and opportunism.

Step 1. Uncover the Hidden Constraints

Successful companies often get ahead of competitors by focusing on a particular segment of customers or geographic market and learning more about their behavior and needs than anyone else. The companies design a profit-generating engine, based on a particular price, margin, and cost structure, that is underpinned by investments in the capability to source, produce, distribute, and support a product or service that these customers value. Over time, this profit engine is continually fine-tuned, often reaping economies of scale, scope, and learning. For example, Frank Winfield Woolworth, who founded Woolworth Corporation in 1879, pioneered the idea of selling merchandise at no more than five cents. He refined this “five and dime” profit engine to become a finely-tuned general merchandising machine. Initial concepts of “no frills” service, cheap products, and items that were nonperishable formed the core. The Woolworth Corporation subsequently developed competencies in managing a wide product range while keeping stock turnover high, competencies in site selection and development, and logistics to reap economies of scale from a chain of stores.

When its founder died in 1919, Woolworth boasted a chain of 1,081 stores with sales of $119 million (an incredible figure for its day). The power of the formula was reflected in the company’s New York headquarters building at 233 Broadway; at 792 feet, it was the world’s tallest building until the Chrysler building was completed in 1930. After World War II, the company continued to improve on the winning formula, adding new competencies in the management of advertising, consumer credit, and self-service, and in site selection and management in the new retailing environment of U.S. suburbs.

Woolworth’s strategy had the advantages of focus: it was able to deepen its existing competencies and incrementally expand both its competency base and its knowledge of different market environments. However, competitors were developing retail formats that required both competencies and market knowledge that were outside the “box” in which Wool-worth was operating. Competitors like Wal-Mart (general-merchandise, discount superstores) attacked on one flank, while specialty “category killers” like Toys-R-Us attacked on the other.

Despite a decline in its overall sales figures in real terms, Woolworth failed to invest in creating new capabilities or understanding the behavior of shoppers using the new retail format so it could expand into either superstores or specialty retailing. When, in the late 1980s, Woolworth eventually tried to respond with its own discount and specialty stores, it ran into a hidden constraint: while the strategy made sense, Woolworth didn’t really have the option to change its strategy quickly, because it had not invested in creating new capabilities and knowledge outside its existing formula. Thus, by 1995, Woolworth was forced to sell its new specialty stores “Kids Mart” and “Little Folks,” established in the early 1990s, because of poor profitability. The company had become a prisoner of its past.

In 1993, Woolworth closed 400 stores in the United States and sold its 122 Canadian Woolco stores to Wal-Mart. In 1997, Woolworth shut down its last general-merchandise store in the United States. It had refined and polished its economic engine and deepened its narrow range of competencies into almost perfect extinction. The company had invested in new strategic options too late to build the competencies and knowledge necessary to pursue a new strategy.

In the quest to achieve challenging new missions, Woolworth managers kept bumping up against two constraints: they didn’t really understand the customers they needed to attract to achieve a new, broader strategy; and they didn’t have the capabilities to compete with rivals that were already established. When they decided to respond to lost sales caused by market changes, well-established Woolworth managers kept hitting the dual constraints. They had not invested in real options soon enough to replace their dying profit engine and were caught in a box (see Figure 1).

{kind=link}

Woolworth did, however, invest in one new strategic option that partially saved it, when, in 1974, it backed an experiment in specialty retailing — “Foot Locker.” Using new capabilities in the retailing of athletic footwear and its market knowledge, Woolworth exercised this option to build a chain of athletic-shoe stores when growth in the market took off in the 1980s. It subsequently introduced new formats, including Lady Foot Locker in 1982 and Kids Foot Locker in 1987. Over time, Woolworth opened more than 7,100 specialty stores, and in June 1998, it changed its corporate name to Venator Group. In some ways, this is an example of successfully repositioning a company whose core business had become obsolete. But, in fact, Woolworth paid a high price for failing to recognize the hidden constraints on its strategy choices and underinvestment in new strategic options. Venator is a much smaller company; it now occupies only half the floors in that famous New York skyscraper, which it sold in April 1998.

To avoid becoming a prisoner of hidden constraints, a company must build new capabilities and simultaneously expand its knowledge of new market segments and customer behavior. If the outcome of uncertain market developments falls within the range of that portfolio of options, the company will then be able to exercise one or more relevant options. Thus the company will be able to outperform the competitors that have not made these investments. Alternatively, it will be able to close the competitive gap with rivals that already possess the necessary capabilities and market knowledge.

Companies should distinguish between capability constraints and market knowledge constraints (see the “existing” box in Figure 1). Some companies’ options are not seriously constrained by their market knowledge. Through various processes I describe later, they have created a large internal pool of knowledge about new customers and competitive behavior. This may include knowledge about new potential users of the company’s products or services, new geographic segments, existing users with changed needs and buying behavior, or competitors changing the rules of the game. The dilemma these companies face is that market knowledge itself can still leave them with few ways to exploit that knowledge (other than, perhaps, selling it to someone else). The “trader” is a company with potentially valuable market information, but no capability to use it to create value except by trading the information or using it to arbitrage a commodity (see Figure 2). Obviously, some profitable companies are based on trading information, but for most, this option does not allow them to leverage their existing competence base and therefore support an adequate return on their asset and skill bases.

{kind=link}

To avoid having capabilities that are too narrow to exploit the knowledge of different markets and customer behaviors, such a company needs to systematically expand its pool of value-creating capabilities (adding, for example, the capability to manufacture products or deliver services that utilize that market knowledge). For example, the British trading house, Inchcape, had a geographic reach extending from southeast Asia to the Americas, the Caribbean, India, Europe, and Africa, with interests in more than 500 companies in forty-four countries. It became a professional distributor, marketer, and seller of the products and technologies of its “principals” (the owners of the branded products and services it traded) and a provider of specialist services. As a trader, it successfully expanded its options into new markets (the horizontal dimension in Figure 2). But as the principals for whom Inchcape acted as agent became more familiar with the local markets, they wanted more control over their market positioning and built the scale to cover the fixed costs of local operations. They began to invade Inchcape’s business. As a traditional trader, it had few places to turn. With finely-honed trading skills, but lacking the breadth of capabilities to add value in other ways, its strategic options were tightly circumscribed. Some of Inchcape’s competitors, like Swire Pacific, for example, had invested more in creating options by developing new capabilities in areas such as property development and airline management. By the time that pure trading as a mechanism for extracting profit from local knowledge came under serious threat, Swire used these expanded capabilities to extract an increasing proportion of total profit from its local knowledge in new ways.4

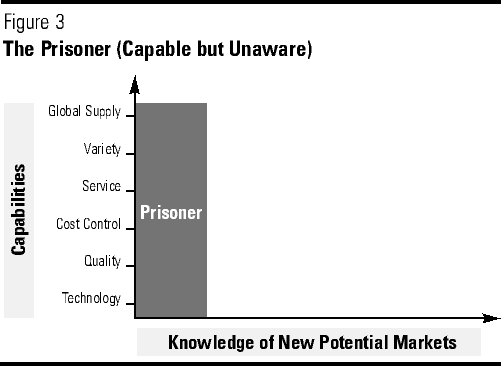

Some companies have the opposite problem: they have created formidable capabilities but are prisoners of their lack of market knowledge (see Figure 3). AT&T, immediately after deregulation, had capabilities in technology, communications infrastructure, and experience in sales and customer service. As a result of domestic regulation and government monopolies overseas, however, the potential of AT&T’s capabilities was imprisoned by a lack of market experience outside the long-distance, voice, and data sector in the United States. These constraints meant that AT&T could not fully utilize its existing capabilities so that it had underutilized capacity for value creation (in the sense that the marginal costs of using these capabilities would have been less than the marginal revenues earned had AT&T had the option to broaden its offering and the range of markets it served). Gradually, AT&T has opened new strategic options by building its knowledge base of the markets for new domestic service and users in national markets overseas. It is thus able to increase the effective capacity utilization of its existing capabilities.

{kind=link}

To develop new strategic options, therefore, two sets of processes are required: (1) processes that fundamentally expand the company’s capabilities, and (2) processes that expand the company’s knowledge of new markets and market behavior. However, opening new options does not necessarily imply unrelated, or even related diversification in the traditional sense.5 Strategic options on the future are not full-fledged new businesses. Instead they are the “doors to the future” that are created when a company undertakes pilot projects, reconnaissance, and experiments that expand its knowledge of alternative market segments and value propositions and that seed new organizational capabilities.

In the case of Woolworth, the relevant options turned out to be experiments with new retailing formats, which can be seen as a type of related diversification. But, alternatively, new options can often involve finding new ways to either deliver enhanced value to or reduce the costs of serving an existing customer segment, as in Monsanto’s use of biotechnology to replace traditional chemicals in its weed-control business or Schwab’s introduction of “E-Schwab.” In almost every case, however, creating new options involves some combination of fundamentally extending the company’s existing capabilities and, at the same time, its knowledge of customer and market behavior. E-Schwab, for example, requires new capabilities in the design and management of an Internet interface between the customer and Schwab’s internal systems. Many E-Schwab customers use the existing telephone trading system, but they are likely to behave differently in electronic trading. Schwab needed to understand, for example, which customers would pay a price premium and how it could change its ability to build customer loyalty.6

I am not arguing that companies should develop an infinite number of capabilities or exploit them across every possible market. Such approaches would eventually drown in diseconomies of complexity as the variety of activities increased.7 There is an optimal portfolio of options that a company can create in order to strike the right balance between the cost of creating and maintaining an option and the payoffs in the ability to reposition itself more rapidly and at lower costs.

What do these processes look like? How broad a range of options should a company create? Wool-worth, for example, continually expanded its capabilities and knowledge of customer behavior within its existing retailing format; its error was to limit the range of new options, given the rate and nature of changes occurring in its industry.

Step 2. Establish Processes

As we have seen, creating new strategic options combines expansion of the company’s knowledge about new, potential markets or customer behaviors with simultaneous development of new capabilities. The processes need to minimize the costs of building and maintaining the portfolio of strategic options — a particularly important factor given that many options are likely to remain unexercised.

Cost-effective methods of expanding knowledge about new potential markets and customer behavior include leveraging customers’ and suppliers’ knowledge and learning from “maverick” competitors and related industries. Market research is perhaps the most obvious way to leverage customers’ knowledge. Traditional market research is limited by the current perceptions and orthodoxies of existing consumers. Companies should focus on customers’ complaints to understand their perceptions of the existing offering. In some industries, companies can become partners with customers that have articulated an unserved need.

The geographic periphery of the company’s existing markets or concentrations of highly sophisticated customers can also supply knowledge about potential new customer segments or emerging customer behavior. The company must ensure the right environment for the broad potential of these adaptations. It may enter a new market simply to learn what is potentially relevant for its global operations, rather than earn profits from that market directly. The costs of such a market are an investment in expanding the portfolio of strategic options.

Partnerships with leading-edge suppliers, exchange of technical information, or purchase of minority equity stakes in suppliers with potentially innovative technologies are processes that can provide the raw material to generate new options. Likewise, the company can scan related industries for potentially applicable technologies, service systems, or patterns of changing customer behavior as a way to form new options.

Companies should continually ask which companies are breaking the rules in the industry. A company with a single strategy, from which sales and efficiency must be optimized, dismisses these competitors as irrelevant or as following a different strategy. However, the behavior of maverick competitors can be a source of ideas for creating a portfolio of strategic options.

Analogous processes build the new capabilities that allow a company to expand its strategic options. Leonard-Barton analyzed the processes, including building a company’s capabilities base through problem solving, experimentation, importing knowledge, and implementing and integrating new capabilities.8 The combination of capability-building initiatives involved in a total quality management system includes physical and technical systems, managerial systems, and values and norms, all aligned to the process of building a new capability, in this case “quality.”

Acer used these processes to grow from a small electronics company in Taiwan to become the third largest supplier of personal computers in the world (see Figure 4). Just like its competitors, Acer lacked a reliable crystal ball to forecast the future, but had a broad sense of which markets it should learn about to expand its strategic options. Acer recognized that because Americans are sophisticated PC buyers, understanding these customers would give it a head start against competitors in other global markets. That understanding would open many options for Acer both to respond more rapidly and to lead change as other markets followed the U.S. lead. According to Acer’s Chairman Stan Shih, this is why Acer has maintained its presence in the United States despite sometimes extended periods of local financial losses.9

{kind=link}

Acer also knew it would be suicidal to attack the established PC giants across a broad front, so it concentrated on understanding the Asian consumers. Most of the major PC suppliers had traditionally sold only to the high-end, high-price segment of Asian markets. Acer developed capabilities, products, and consumer understanding so it could access the much lower-price mainstream markets in Asia. After rounds of redesigns to cut costs, interspersed with test marketing, Acer learned how to sell computers to the mass-market segment in emerging Asian economies ahead of competitors. This opened new options to enter other low-price, emerging markets like Mexico, South Africa, and Russia.

Acer didn’t follow a strategy of straight-line forecasting based on its existing products and procedures. When it entered a new market, it didn’t always know exactly what product it would sell to whom. Its initial investment in entering a market amounted to buying an option. Rather than simply selling its products to the kinds of customers it served at home, Acer invested in partnerships with local distributors and suppliers designed to maximize its opportunities to learn about the market and further develop its capabilities. In the United States, partnerships with discount retailers taught Acer how to use a previously underserved channel. Its alliance with California-based Frog Design built its capability to develop nontraditional computer designs and ergonomics. It subsequently exercised this option when it launched the unconventional, sleek, grey “Aspire” — a multimedia home PC.

In Mexico, competitors like IBM and HP believed that only large corporations could afford branded personal computers, while private consumers bought low-quality clones. Acer invested with its local partner in working with small- and medium-sized companies to discover a gap in the market of smaller businesses. It then used its capabilities to create a suitable product. Having established a new option, it moved aggressively to exercise it, building its market share in Mexico to 32 percent by 1996.

Acer did not exercise all the options it created. In 1996, Acer built an assembly plant in Lappeenranta, Finland, from which it could efficiently supply computers to Russian distributors. Developments in Russia during 1996 and 1997, including the rapid emergence of strong, domestic competitors, meant that the Russian market became less attractive than when Acer had made the investment. However, given Finland’s membership in the European Union, Acer could easily transfer resulting excess capacity into other European markets.10 Its experience points to another important factor: a company should design an option to minimize the costs incurred, should it decide not to exercise it.

Acer’s approach was that strategy is creating options and exercising in new markets. It expanded its capabilities in successive waves, by first exploiting its basic capabilities in low-cost manufacturing and flexibility to rapidly introduce new technology as a supplier of components and sub-assemblies to other PC suppliers. Each wave of Acer’s initiatives opened new, broader options for positioning. No amount of planning could enable it to pinpoint exactly which option it would exercise in an uncertain future. Unlike Woolworth or Inchcape, however, it created an expanded strategic space in which it could maneuver.

Step 3. Optimize the Portfolio

How does a manager know if he or she has created the right portfolio of strategic options for the future? First, by setting aside traditional spreadsheets. Instead, managers need to consider two factors:

- What alternative capabilities might profitably meet probable customers’ needs? (For example, digital or analog technology, localization or individual customization, high levels of variety, reduced lead times, bundled products and services, and so on.)

- Which potential future markets (geographic, customer, or nonuser segments) or new customer behavior (such as effects of e-commerce) does the company need to know about?

If they stay at the level of future capabilities and potential new markets, far above the detail of unit sales and prices, companies can probably forecast with reasonable accuracy. In 1984, the same year as The Economist forecasting competition, John Naisbitt analyzed 6,000 U.S. newspapers to isolate ten “mega-trends.” They were developments such as “customers would demand a combination of high-tech combined with high-touch,” “globalization would mean a combination of more shared production with more cultural assertiveness in individual markets,” or customers would demand an “option explosion,” not just chocolate or vanilla, but a huge variety of alternative product or services.11 Most of these broad “predictions” came to pass, largely because they were not predictions at all, but trends already underway that simply gathered pace over time. They are exactly the views that companies need to assess the capabilities necessary to generate a sound portfolio of strategic options. What kind of capabilities does a company need to increase options and provide future customers with more variety? What does this mean for operations, for inventory systems, for salesforce training? The answers will obviously differ by industry and by company.

Various techniques exist to develop needed alternative capabilities and to understand market environments or customer behavior. One approach is scenario planning.12 Hamel and Prahalad suggest isolating potential “discontinuities” by looking for the likely collision of different trends that will create a step-change in the environment.13 An example of such discontinuity is the combination of a twenty-four-hour demand for news broadcasts, emergence of a new cable media distribution channel, and development of low-cost satellite communications.

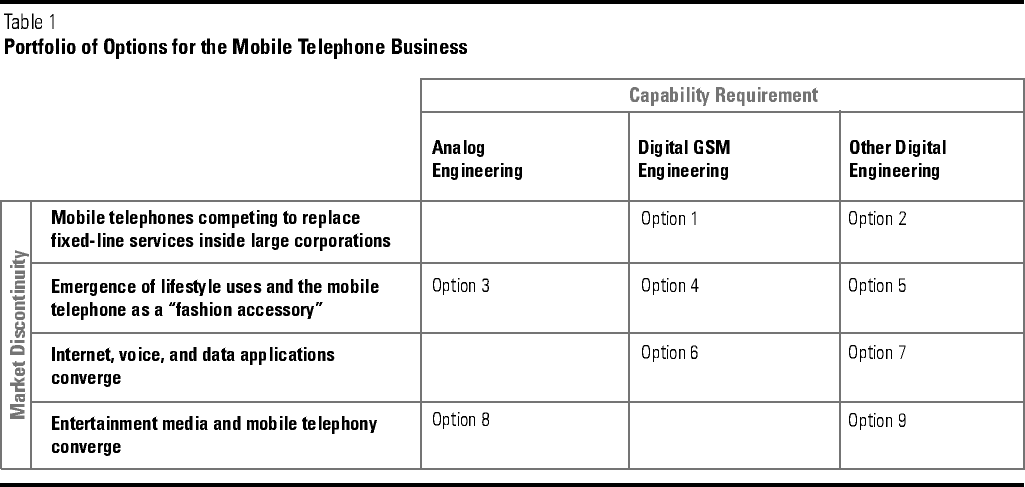

Once a company lists alternative new capabilities and market environments and behavior, it can create a table of its main alternatives (see Table 1). Not all combinations of future potential discontinuities and possible capabilities required to underpin competitive advantage will be technically feasible (Internet-mobile telephony convergence and analog technology, for example). Once planners identify the feasible options, they must decide whether to make the necessary investment to include a particular option in the portfolio. In looking at Table 1, for example, each competitor has to decide whether to include option 3 and option 8 in its portfolio by investing in the continued development of analog technology.

{kind=link}

These decisions should result from three considerations:

- The costs of creating and maintaining the option.

- The estimated probability that the company will exercise the options.

- The probability that creating the option will itself spawn future options, even if it remains unexercised (e.g., a company may value option 3 or option 8, not for its direct profit-making potential, but because of its capacity to open future options that rely on analog technology).

When strategy is viewed as the creation of options on the future, minimizing the costs of creating and maintaining them becomes a critical managerial concern. The costs can be reduced by careful design of efficient experiments, test marketing, and prototyping; by sharing the costs in partnership with interested customers or suppliers; and by leveraging new information sources.

In attempting to optimize the company’s portfolio of options, management must clearly distinguish between the cost of investing in the option and the cost of exercising that option (the latter being the cost of scaling up the option into a profit-generating business). In the case of Woolworth, for example, the cost of its initial experiment to establish its first Foot Locker store was the cost of creating an option to move into specialty retailing. If Woolworth had not exercised this option, the cost would have amounted to writing off the cost of the experiment. The cost of exercising the option included all the investments required to establish and operate a competitive chain of stores that achieved the minimum efficient scale. The cost of Acer’s option on the Russian market amounted to the investment in its Finnish plant less the expected present value of cash it could obtain from selling the product elsewhere in Europe if it decided not to exercise the option to enter Russia. The costs of exercising its Russian option, meanwhile, would have included the costs of investing in brand building and distribution capacity in Russia, and so on.

This distinction is critical because the decision whether to include a particular option in a portfolio should be made by comparing the estimated value of that option with the cost of creating the option, not with the costs of exercising it.14

By viewing the first role of good strategy as the creation of a portfolio of options for the future, that strategy’s success does not rest on the ability to predict continuing trends. Depending on the future environment, not all options will be exercised. However, those discarded are not wasted, but serve the useful purpose of insurance against an uncertain future.

Step 4. Combine Planning and Opportunism

Planning and opportunism both have an essential role in the strategy process. A company can plan the successive capabilities needed and new potential markets in order to create sufficient strategic space —the room to maneuver in the future. It can plan the proactive creation of strategic options.

A company cannot plan the precise options to select: exactly which products and services will it sell to which customers in which markets at what prices? That is the purview of opportunism. For example, as part of building its “localization” capability, Acer began assembling its product in a suburb of Mexico City in 1993. By careful planning, it expanded its strategic options in respect of the market. During the peso crisis in December 1994, Acer exploited one of these strategic options. Having shifted a significant part of its cost structure to Mexico, it broke with the industry custom of quoting U.S. dollar prices and listed its products in pesos. When the computer market shrank by 40 percent, it launched a new model, continued to buy TV time, and targeted new customers, winning prestigious contracts to supply the national, state-owned power company and the main public university. Its market share rocketed, allowing it to retain a 32 percent market share when the market improved by 1996. Through timely opportunism, Acer decisively exercised its option to its advantage. It didn’t predict the peso crisis, but when unexpected events unfolded, it had the strategic option to turn adversity to its advantage.

Another example of the interplay between strategic options and unexpected opportunities is the introduction of Acer’s “fast food” model of PC supply. When Acer began to build its original localization capability, it didn’t need to know exactly how to use it. It knew that localization would become an important capability and that, having analyzed the possibilities, the investment in this option was justified. Having this strategic option allowed Acer to outpace its competitors when the market moved toward “customized” PCs. Opportunism guided Acer’s tactics for using its localization capability and market knowledge to gain a specific competitive advantage.

A critical element is to keep tactical opportunism within the bounds of the company’s overall direction and to rule out the options that would cause it to wander from its long-term mission. The selection and management of a portfolio of options, with some options expiring and new ones added, based on the decision rules I discussed earlier, is a good way to set bounds. To make “bounded opportunism” work in practice, every manager should ask the following question about each tactical opportunity: “Is it a weed or a flower?” An unexpected opportunity that diverts the company from pursuing its long-term mission is a “weed.” Meanwhile, opportunities that allow it to take advantage of its options to accelerate progress toward long-term goals are “flowers.” In this way, top management can set bounds that are sensitively applied without crushing the organization’s entrepreneurial spirit.

Conclusion

Traditional strategic planning draws from forecasts of parameters like market growth, prices, exchange rates, and input costs. As The Economist experiment aptly demonstrates, we are unable to predict those variables five or ten years in advance with any accuracy. Spreadsheets try to predict exactly what products and services to sell to which customers in what volumes at what prices. In the process, these traditional frameworks lead to betting everything on straight-line strategies and risk boxing the company into a corner when reality inevitably turns out differently from predictions.

The trends we can predict with reasonable confidence — more localization, increased variety, and faster response times — can’t be acted on by classic strategic planning systems driven by forecasts of sales, prices, and costs. Strategic planning systems deploy exactly the input we have no way to accurately predict, while discarding the new capabilities and knowledge of new market segments that will give companies the option to respond to broad, long-term trends.

To break from this trap, companies need to understand that successful strategy must combine both planning and opportunism. Planning builds new capabilities and augments knowledge of new, potential markets and customer behavior. Because investing in these options costs money, however, the number of strategic options must be optimized and managed. Actively managing a portfolio of strategic options allows a company room to maneuver and reposition. Short-term opportunism must determine which precise option a company chooses to exercise.

References

1. These techniques are well described in: R.M. Grant, Contemporary Strategy Analysis, second edition (Oxford: Blackwell Business, 1995).

2. See I. Dierickx and and K. Cool, “Asset Stock Accumulation and Sustainability of Competitive Advantage,” Management Science, volume 35, December 1989, pp. 1504–1514.

3. R. Wrubel, “The Ghost of Andy Carnegie?,” Financial World, volume 1, September 1992, p. 50.

4. P. Lasserre and C. Butler, “The Inchcape Group (A): The End of an Era” (Fontainebleau, France: INSEAD, case 04/93-317, 1993); and

C. Kennedy, “Can Two Hongs Get It Right?,” Director, February 1996, pp. 34–40.

5. See, for example:

M. Lubatkin and S. Chetterjee, “Extending Modern Portfolio Theory to the Domain of Corporate Strategy: Does it Apply?,” Academy of Management Journal, volume 37, September 1994, pp 109–36.

6. A. DeMeyer, “E*Trade, Charles Schwab, and Yahoo!: The Transformation of On-line Brokerage” (Fontainebleau, France: INSEAD, case 05/98-4757, 1998).

7. P.J.H. Schoemaker, “Strategy, Complexity, and Economic Rent,” Management Science, volume 36, October 1990, pp. 31–43.

8. D. Leonard-Barton, Wellsprings of Knowledge (Boston: Harvard Business School Press, 1995).

9. P.J. Williamson and D. Clyde-Smith, “The Acer Group: Building an Asian Multinational (Fontainebleau, France: INSEAD, case 01/98-4712, 1998).

10. “Laptops from Lapland,” The Economist, 6 September 1997, pp. 89–90.

11. J. Naisbitt, Megatrends (New York: Simon & Schuster, 1984).

12. See, for example:

C.A.R. McNulty, “Scenario Development for Corporate Planning,” Futures, April 1977; or

A. de Geus, “Planning as Learning,” Harvard Business Review, volume 66, March–April 1988, pp. 70–74.

13. G. Hamel and C.K. Prahalad, Competing for the Future (Boston: Harvard Business School Press, 1994), p. 145.

14. The subject of valuing real options is a large topic in its own right. There is insufficient space to cover it here. For relevant techniques and methods, see, for example:

M. Amram and N. Kulatilaka, Real Options: Managing Strategic Investment in an Uncertain World (Boston: Harvard Business School Press, 1999).