Winning in Smart Markets

Topics

The past two or three years will likely be remembered as the time when the long-heralded, but often postponed, “information age” finally became a reality. For business, the information age has led to the emergence of “smart” markets, or markets defined by frequent turnover in the general stock of knowledge or information embodied in products and possessed by competitors and consumers. In contrast to traditional “dumb” markets, which are static, fixed, and information-poor, smart markets are dynamic, turbulent, and information-rich. They are based on new kinds of products, competitors, and customers:

- Smart products. These consist of products and services that have intelligence or computational ability built into them (e.g., microprocessors). More generally and more important, smart products include any offering that adapts or responds to changes in the environment as it interacts with (or is used by) consumers (for example, the process of ordering a customized computer from Dell or the crafting of a personal financial portfolio from Charles Schwab).

- Smart competitors. These are competitors that, from a company’s standpoint, are changing or about which a company continually needs to update its information. The pervasive phenomenon of “convergence” — where firms from historically separate industries now find that they are direct competitors (in such areas as entertainment, telecommunications, and financial services) — is a direct consequence of smart competitors.

- Smart customers. These are customers that, from a company’s standpoint, are changing or about which the firm continually needs to update its information. As customer demographics (e.g., where they live, their family and job status) and purchasing patterns (including increased switching among competing firms) display more frequent changes than in the past, firms are finding that an ever larger portion of their consumer portfolio is made up of “smart customers.”

Smart companies have tried to sustain a competitive advantage in the face of the challenges raised by smart markets largely through their information technology (IT) infrastructure. Indeed, IT is transforming business practice. The experiences of companies as diverse as American Airlines, USAA Insurance, Federal Express, Dell Computer, and pharmaceutical wholesaler McKesson — each of which has altered the dynamics of its industry and changed the requirements for competitive success — are among the most prominent recent business stories.

In almost all cases, the companies involved first put in place an IT infrastructure to solve the bandwidth problem, thus making possible dramatic increases in channel capacity (the speed with which information is transmitted and the amount of information that can be processed). What has distinguished firms that have gained a significant competitive advantage is that, having introduced an IT infrastructure, they have then gone beyond the technology to view the information itself as the core asset and the management of information as their main priority. In so doing, they have been pioneers in the development and execution of what have come to be called “information-intensive” strategies.1

Information-intensive strategies are an appropriate response to the emergence of information-intensive or smart markets. Individual business functions (and the discipline of strategy itself) are being reshaped by both the need and the ability to incorporate higher levels of information processing into their activities. Many of the most important developments have arisen in marketing, typically the function charged with managing the relationships between the company and its customers. An understanding of how consumers are adapting their behavior to the demands of an increasingly information-intensive environment has been the starting point for companies that have achieved success in smart markets.

Consumer Behavior in Smart Markets

Emerging research suggests that consumer behavior in smart markets is based on twin expectations: freedom of choice and help in making choices. The emergence of smart products — which, by definition, are not really complete until they have interacted with the customer — leads consumers to expect greater freedom of choice in product and service selection. Consumers increasingly assume that firms can provide anything with respect to the product or service in question. They become more demanding and expect to be treated as individuals.

At the same time, the resulting proliferation of options produces information overload and a marked increase in consumers’ desire for help in processing information. Of course, consumers have always wanted help in making choices; this is the essence of “solutions selling.” In traditional markets, however, consumers’ desire for help is rooted in the assumption that information is in short supply. In smart markets (and, more generally, in the information economy), information is abundant. What is scarce is the ability to process information. The need to conserve that ability drives consumers’ desire for help in choosing among alternatives.

The twin requirements of freedom of choice and help in making choices point to three consumer benefits beyond those associated with a particular product category:

- Convenience (one-stop shopping). Customers wish to purchase the widest set of related products and services from the same supplier, thus conserving their most valuable resource — time spent attending to any particular product or service.

- Participation. Customers desire the supplier’s cooperation in the design, production, and delivery of the product or service. The goal is to break down the boundary between company and consumer by, for example, having the company provide a menu of options from which the customer can choose.

- Anticipation. Customers want the company to be able to read their minds. The firm should be proac-tive with certain product or service offerings and communication interventions, based on an understanding of customer lifestyles and behaviors.

Information-Intensive Customer Management

How to deliver the value proposition that consumers want — convenience, participation, and anticipation — is the key marketing challenge that a company faces as it tries to develop a sustainable competitive advantage in smart markets. Leading-edge firms have responded to the challenge by creating information-intensive customer-management strategies that are designed to manage proactively the full set of potential relationships between company and customer. These firms have moved well beyond the limited goals of customer retention or data mining that have received so much attention. By observing the activities of these firms across industries, we can identify generic strategies and develop a preliminary taxonomy, or categorization scheme, that can be used to compare and contrast them. The placement of individual strategies within a conceptual framework provides managers with guidance in making customer-management decisions.

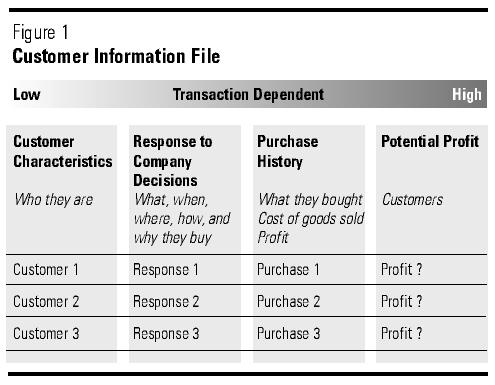

The activities observed are rooted in an expanded view of what the company is offering: its capabilities as an information processor as opposed to a set of products and services. The organizing tool, or asset around which the full range of strategies is based, is the customer information file (CIF) — a single virtual database that captures all relevant information about a firm’s customers. The database is described as virtual because, while it operates as if it were an integrated single source housed in one location, it may in reality be composed of several isolated databases stored in separate places throughout an organization.

While the concept of the CIF as the core corporate asset should be acceptable to marketers, for many, it is an unconventional idea. Many companies pay lip service to the notion that “our customers are our most important resource,” but the typical firm views its real assets as its products or services and the facilities and operations that support them. This perspective is reflected in the product (or brand) management organizational structure — in which profit-and-loss responsibility is defined in relation to a set of products — that still predominates in most companies (even those leading the way in information-intensive strategies).2

Furthermore, it is important to recognize the degree to which the procedures and practices of most organizations have been designed to minimize actual interactions with customers. By contrast, underlying the notion of the CIF as the key asset is the assumption that the firm’s operational goal is to maximize its communication with its customers — to look for every opportunity to “talk” with them — since the data collected from these interactions are the raw materials from which companies craft information-intensive strategies.

The company thus sets as its main objective the maximizing of returns to the CIF (as the key corporate asset). It then chooses any one or several information-intensive strategies to accomplish that objective. This approach represents a shift in performance goals. In particular, concepts such as profitability or market share per product are being replaced with concepts such as profitability per customer (sometimes referred to as “lifetime value of a customer”) or customer share (the total share of a customer’s purchases in a broadly defined product category — e.g., McDonald’s or Coca-Cola’s “share of stomach,” Levi’s “share of closet,” or VISA’s “share of wallet”).

Before discussing the strategic alternatives, I describe the composition of the CIF (see Figure 1). The rows (or records) represent individual customers (actual and potential), not customer segments.3 The columns contain data that have been collected about customers. At least conceptually, these data can be organized into three categories:

{kind=link}

- Customer characteristics — typically, demographic information about customers that is independent of the firm’s relationship with the customer.

- Response to company decisions — perception and preference (for example, product attribute importance) and other marketing-mix response information (for example, price sensitivity, sources of information, channel shopping behavior) that describes customers (when, where, how, and why they buy), based on some level of interaction between the company and its customers.

- Purchase history — information on what products customers have purchased, along with the revenues, costs, and profits associated with these purchases, based on the firm’s actual transactions with its customers.

So far, the matrix is two-dimensional. Technically, however, the CIF is at least three-dimensional, since each entry is indexed by time. Furthermore, the categories of data — customer characteristics, response to company decisions, and purchase history — are arranged in order of the degree to which they are dependent on actual transactions or contact between the firm and its customers. This sequence does not necessarily parallel the degree of difficulty in collecting the respective data. Thus, both purchase history data and customer characteristics data are typically much easier to collect than response-to-company decisions data. (Purchase history for potential customers is, of course, empty.)

What I describe is “normative” in scope — that is, what an ideal CIF would look like, independent of the degree to which any given company has implemented it in practice. Indeed, since records are associated with individual customers, and since most marketing-mix response data are collected (at best) at the segment level, many of the individual entries in response to company decisions must be inferred from what has been gathered at an aggregate level. In a similar vein, few organizations know the actual costs associated with having sold a product to an individual customer and thus are unable in practice to identify the respective profits. My discussion assumes that firms have collected and organized all relevant information at the level of each individual customer.

The CIF contains an additional column of information (at the far right), labeled as potential profit (see Figure 1), or the amount that the firm could have realized from a given customer had it made optimum use of its information assets (or the lifetime value of the customer). Potential profit minus profit represents forgone or unrealized profits. The purpose of executing information-intensive strategies is to minimize those forgone profits across all customers in all periods and to maximize the value of the CIF. (If one is serious about the CIF’s role as the key corporate asset, then this may also be a measure of the firm’s value!)

I now discuss a range of information-intensive strategies in light of this framework. The goal of any strategy is to use information collected about customers and their previous dealings with the company to increase the revenues and/or decrease the costs associated with future transactions. As is true in typical marketing research, in implementing a given strategy, the key questions are: To what extent can a company use customer characteristics data to understand and influence response-to-company decisions? To what extent can a company use response-to-company decisions data to understand and influence purchase history?

Using this framework, we can conceptualize three classes of generic strategies — column, row, and whole file — and six strategies:

- Mass customization (column)

- Yield management (column)

- Capture the customer (row)

- Event-oriented prospecting (row)

- Extended organization (whole file)

- Manage by wire (whole file)

The strategies are not mutually exclusive. They differ only in the degree to which managers focus their attention in particular ways and develop a set of programs that capitalize more on one subset of information in the CIF than on another.

Column Strategies

Customers are different and have different responses (tastes, preferences, and so on) to a firm’s decisions. Column strategies represent an extension of the traditional marketing concept (“find out what consumers want and give it to them”): they are taken to the individual customer level in a way that was not possible before the adoption of information technology.

Mass Customization.

This most prevalent column strategy takes advantage of developments in flexible manufacturing that enable companies to tailor or customize individual offerings at little additional marginal cost.4 Typically, it involves a significant initial investment in fixed costs that effectively replaces hardware-intensive processes with software-intensive ones (the factory as a computer). Thus, customers of National Bicycle in Japan (the Panasonic brand in the United States) sit on a smart bike at the dealer’s showroom that takes their vital statistics (height, weight, length of legs, and so on) and relays the data to the factory, where a customized offering is manufactured (in three minutes!) from more than 1 million templates (based on data collected from customers). Levi’s has prototyped a similar system for women’s jeans, and Motorola’s Pager Division has implemented a mass customization strategy that guides telephone customers through a menu of 30 million possible permutations of pagers. R.R. Donnelley is reported to print as many as 8,000 different editions of the monthly Farm Journal — each targeted to a narrow subset of the overall readership.

While mass customization is usually associated with flexible manufacturing and operations, it can also refer to strategies based on flexible marketing methods, that is, customizing the nonproduct elements of the marketing mix. The mail-order catalogue company Fingerhut customizes promotions on different products for individual customers. Furthermore, Fingerhut engages in flexible pricing by offering specialized credit terms on an individual basis to customers (many of whom have low household incomes but are deemed to be credit worthy). Other businesses that are pioneering what are essentially price-discrimination or continuous pricing initiatives range from airlines, where passengers pay different prices for the same service depending on when they purchase the ticket, length of stay, and so on, to computer companies like Dell, which offers different prices for essentially the same product depending on time of purchase, minor variations in features, and competitive activity. In all these instances, the data in the CIF, and the knowledge about individual and aggregate customer preferences and marketing-mix sensitivities, guide the degree and kind of customization that the company is willing to undertake.

Yield Management.

The second major information-intensive column strategy, yield management, builds on flexible or discriminatory pricing. It takes advantage of customers’ heterogeneous price sensitivity with respect to time (as well as the firm’s technical and legal ability to price discriminate) in order to maximize the total return to a fixed asset — particularly when the marginal cost of providing an additional unit is low and the product in question cannot be inventoried. Typically observed in service businesses, yield management has been practiced in its most sophisticated form by the airlines (although the actual pioneers have been the utilities with their peak-load pricing strategies). For example, American Airlines’ SABRE division has used the data collected from its frequent fliers to predict temporal ticket-purchase patterns and selectively discount seats on a given flight. If a competitor initiates an advanced-purchase-required, across-the-board price cut on a flight, American may match on only 70 percent of its seats, knowing that the remaining 30 percent will be purchased (at the last minute) by price-insensitive business customers. Information-intensive retailers have also used flexible pricing to move inventory quickly and manage the store’s overall yield.

While yield management to date has been used primarily in service businesses, an important, if under-appreciated, relationship exists between this strategy and mass customization that suggests its applicability to manufacturing and the evolution of information-intensive strategies in general. As noted, the conditions under which yield management is appropriate are (1) a high fixed-cost asset where, (2) the marginal cost of providing an additional unit is low, and (3) the product cannot be inventoried. Increasingly, these are the same conditions that underlie the implementation of mass customization. Thus, although technically National Bicycle or Motorola can inventory their products (whereas American Airlines cannot), much of the impetus for mass customization has been just-in-time manufacturing and the elimination of inventory. Indeed, for both National and Motorola (as for American), the real cost is “downtime on the system,” that is, moments when the expensive fixed asset (whether a plane or a factory) is not being used to capacity. At these times, any revenue at all will be a contribution to fixed costs (since marginal costs are so low); to the extent that customers can be separated according to their price sensitivity with respect to time, the mass customizing manufacturer (like the service provider) has the incentive to practice yield management.5

Row Strategies

As their name implies, information-intensive row strategies work by attending to particular rows of the CIF, that is, by maximizing both the quality and quantity of the interactions and transactions with individual customers. Given a particular customer, the goal is to learn as much as possible about the widest possible set of responses to the firm’s decisions and offerings over time. A focus on the lifetime value of the customer is central to successful row strategies.

Capture the Customer.

Also known (perhaps more benignly) as customer intimacy, affinity marketing, or relationship marketing, the objective of the capture-the-customer strategy is to realize as high a share as possible of a customer’s total (lifetime) purchases in a given (often expanding) set of product categories.6 The capture-the-customer approach relies heavily on interactive communications (telemarketing and, increasingly, the Internet or other on-line media) and capitalizes on the firm’s ability to use the information collected and processed from previous encounters with a customer to influence subsequent encounters and transactions. The company views marketing expenses (particularly communications) associated with any one customer as an essentially fixed cost that it would like to amortize over as many different product or service transactions as possible. By contrast, column strategies such as mass customization revolve around an initial investment in fixed manufacturing costs that the firm hopes to spread over many different product variants (targeted at different customers).

Companies have implemented capture-the-customer strategies in several ways. Oracle Software’s telemar-keting sales effort is driven by a sophisticated relational database, from which an Oracle representative interacting with a prospect can call up all relevant information on the product in question, competitors’ offerings, and all previous interactions with the caller (including other people at the prospect’s firm who have interacted with Oracle). The system has documented yields or hit rates of over 90 percent — referring to the proportion of prospects who, after a single call, have either purchased some product or service or been converted into highly qualified leads. American Express has implemented a relationship-billing program with its commercial customers (e.g., restaurants), in which it first provides a given establishment with a demographic analysis of its customers and then uses this information to sell the establishment advertising space in specialized publications (e.g., restaurant guides) targeted at the same demographic groups. More generally, firms as diverse as Fidelity and Charles Schwab in financial services and Pioneer in seeds and agricultural commodities have used capture-the-customer strategies to cross-sell an increasingly wide range of products to the same customer.

Event-Oriented Prospecting.

An increasingly important version of the more general capture-the-customer strategy is the event-oriented prospecting approach, which is based on the firm’s ability to store and process life-cycle-related and other situational information about its customers that might trigger a purchase (sometimes referred to as “magic-moment marketing”). The goal is to anticipate the customer’s life-cycle or other situational needs and to time the interaction so that the company appears with a solution just when the problem arises — creating the appearance of literally “reading the customer’s mind.” A leader in using this strategy is USAA Insurance, whose information system will, for example, automatically direct that information about driver education (and automobile insurance) be sent to a client whose teenage son is about to receive his license.

Whole-File Strategies

These strategies typically rely for their successful implementation on treating the entire CIF as an integrated file rather than focusing on particular rows or columns. For the sake of completeness, I briefly describe the two leading types of whole-file strategies but leave a more detailed discussion of these approaches (which represent perhaps the ultimate to date in information-intensive strategic thought) for future research.

Extended Organization.

Also known as the “virtual company,” extended-organization strategies go beyond the more traditional EDI (electronic data interchange) processes and involve one firm’s use of the CIF to manage a set of activities of another firm in its value chain — in effect, dissolving the functional boundaries between the two (technically distinct) organizations. Thus, Federal Express has built on its original COSMOS customer-service system, which tracks every movement of every package in the network, and now provides customers with terminals and/or software so that they can tie into the system directly — in effect, allowing Federal Express to manage its own shipping department and, in the process, creating high customer switching costs. McKesson, the pharmaceutical wholesaler, whose pioneering ECONOMOST system (placing terminals in drugstores tied to McKesson’s central computer) was originally designed to expedite order processing and control inventory, rejuvenated the wholesale drug distribution industry (not coincidentally resulting in the elimination of dozens of competitors) and is now effectively managing retail drugstores for many of its clients by selling back to them summaries of information collected daily. Inland Steel effectively differentiated itself in a mature “commodity” product category by helping customers manage their own operations after installing and operating an interactive computer network; that effort began as an attempt to keep customers informed about the status of their orders and now provides a wide range of value-added services, from billing and funds transfer to consulting on technical product specifications.

Manage by Wire.

By analogy to the “fly by wire” methodology in aviation (in which computer systems are used to supplement a pilot’s ability to adjust to dynamic environmental changes), the manage-by-wire concept is based on the ability to manage a business essentially by understanding its “informational representation.”7 Drawing on the CIF and other databases, as well as appropriate expert systems and other decision tools, companies seek to model the enterprise and commit to code as much as possible the procedures that form the basis of managerial decision making. The objective is not to replace, but to augment, the managerial function; the assumption is that the complexity associated with information-intensive environments demands a “sense and respond” (as opposed to “command and control”) orientation that can be achieved only by combining the decision-making and data-processing capabilities, respectively, of human beings and machines.

To date, no companies have fully achieved the potential inherent in manage-by-wire strategies, but several have undertaken pioneering efforts in limited domains. Mrs. Fields Original Cookies has been able to run a worldwide network of more than 800 stores (company owned and franchised) with a small corporate staff from rural Utah on the basis of its ability to capture in software the way Debbi Fields managed her first store in Palo Alto, California. Brooklyn Union Gas of New York has codified a major portion of its customer-service operations (meter reading, bill collection, and so on), allowing the company to respond quickly and cost-effectively to the individualized service needs of its large customer base. Aetna Insurance has embarked on a similar program in the financial services area, with the goal of enabling its account executives to respond to customer requests for new products and services in rapidly changing and increasingly competitive markets.

Information-Intensive versus Traditional Strategies

It is helpful to understand how the information-intensive strategies fit in the typical strategic framework. Most theorists on marketing strategy describe a trade-off between the two generic strategies of “efficiency” (i.e., cost/volume or market-share leadership) and “effectiveness” (i.e., differentiation or niche). Given a distribution of customer preferences (“ideal points”) in a product-market space, the cost/volume or market-share strategy relies on choosing a single point near the center of the overall distribution. By locating its offering in the middle of the distribution, the company hopes to capture as large a segment of customers as possible, knowing that it risks not really satisfying the preferences of any one customer. At the same time, with a single standardized offering, it hopes to become the low-cost producer, taking advantage of both the economies of scale and experience effects that will accrue if the high volume is achieved.

By contrast, the differentiation or niche strategy involves positioning as close as possible to specific segments, with a unique offering for each segment. The company is assured of satisfying the preferences of each group, but at a higher cost for each offering provided, and is thus constrained in the number of segments (and offerings) it can reach.

The conventional prescription is that the firm must choose one or the other strategy. (Typically, successful efficiency-oriented companies become leaders, and successful effectiveness-oriented firms become profitable followers.) At the marketing level, the decision stems from the need to choose among two different market segments or sets of customer targets. At a more fundamental level, the choice reflects the core notion of strategy as essentially a process of allocating resources across, while at the same time coordinating among, a wide range of separate value-chain activities, with the result that the firm cannot be all things to all people at one time.8

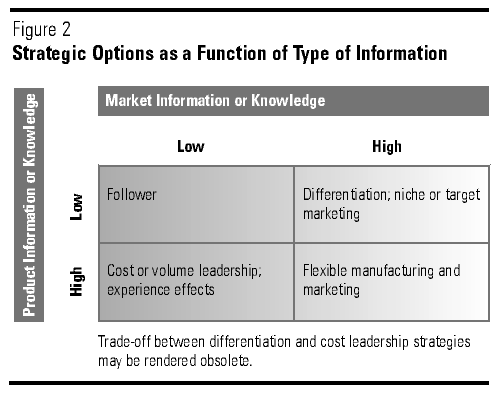

One useful way of explaining the choice of strategy is in terms of the associated trade-off between two types of “information” — that is, the trade-off between product- or production-related experience or knowledge and market experience or knowledge.9 The company focuses on or develops expertise in processing one or the other. This trade-off reflects the prevailing view of market-share and differentiation strategies as polar opposites on the continuum of strategic options, since cost or volume leadership is incompatible with the ability to serve the idiosyncratic needs of specific and diverse segments. The essence, however, of information-intensive strategies is that they permit the company to focus on gaining knowledge and experience in both products and markets. The strategic options open to firms can be viewed as a function of knowledge in a matrix, where the dimensions are product information or knowledge and market information or knowledge, each of which can be either at a (relatively) low or high level (see Figure 2). While, historically, firms have chosen to compete in the upper right or lower left cells, the demands of the changing information environment and the capabilities afforded by information-intensive strategies increasingly are leading firms to excel on both dimensions and compete in the lower right cell.

{kind=link}

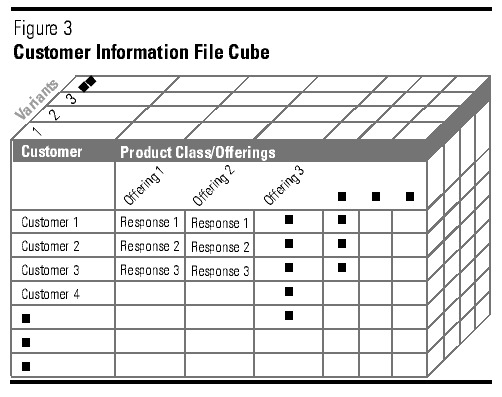

Considering the different ways in which the respective strategies, in particular, the column and row strategies, employ the CIF offers further insight into the nature of information-intensive strategies. It is helpful to modify the original formulation of the CIF to include an extra dimension — one that represents a set of offerings where the firm can produce each of multiple versions within several different product classes.10 The dimensions of the cubic CIF are customers × product class × variant, and the entries in the matrix are the responses to the company’s decisions (see Figure 3). (Purchase history has been eliminated for ease of exposition.)

{kind=link}

Within this framework, I can now describe the different strategic alternatives. I focus first on a single product class:

- The classical market-share leadership approach is essentially a one-dimensional strategy, with the firm offering one version in a single product class for as many customers as possible. The strategy is rooted in the belief that a sufficiently large set of different customers will nevertheless respond in essentially the same way to the offering.

- The differentiation or niche approach introduces a second dimension, with the company offering several versions in a single product class. The strategy recognizes that customers will respond differently to different offerings; because of cost considerations, the company is limited in how large the set of offerings and therefore the set of customers can be.

In other words, when compared with the market-share approach, the differentiation strategy trades off a smaller set of customers for the added value that comes with the addition of a second dimension. Minimizing the company’s need to make the trade-off between customers and offerings is the essence of information-intensive strategy.

I now introduce the third dimension into the framework and allow the company to offer multiple product classes. This addition does not fundamentally change the analysis: the same trade-off exists for each product class. The issue is how many product classes can profitably be supported. It is interesting to note that (ignoring prescriptions for the flow of cash resources within product portfolio models), traditional marketing strategy formulations typically focus on a single category. To a large extent, this presumption of product-class strategy independence can be traced to the information-poor environments in which companies are assumed to compete and the absence of real CIFs. Let’s consider the strategy of those organizations that traditionally have taken an integrated approach across different product categories, namely, large retailers.

Using the terms of the framework, the large retailer offering “one-stop shopping” is implementing a two-dimensional strategy; in contrast to the differentiation approach, however, the dimensions focused on are customers × product class, and the variants within each class are usually limited in scope. To the extent that the retailer’s offerings attract a number of customers, the retailer uses more of the CIF asset than either the market-share leader operating in a single dimension or the differentiation leader operating in a more limited two-dimensional space — which suggests why even traditional “mass market” retailers have been gaining market power at the expense of manufacturers. At the same time, to the extent that the CIF is, in fact, three-dimensional, the traditional retailer is still functioning in a subspace compared with what is possible and is not implementing those information-intensive strategies that are truly three-dimensional in scope.11

In summary, while the emergence of information-intensive strategies compared to more traditional approaches may seem like a matter of degree rather than kind, my framework suggests that this is not the case. Whether the analysis is done at the single- or multiple-product class level, the fundamental impact of information-intensive strategies is that they generalize the traditional strategic alternatives by adding depth, or an additional dimension, to the CIF — thus allowing the firm to compete in a richer space with a fuller set of alternatives.

Choosing among Alternatives

The implication so far is that, for the firm to maximize the return to the CIF asset — that is, to take complete advantage of the full three-dimensional space — it must implement a range of the strategies described (for example, an integrated mass-customization plus a capture-the-customer approach). At the same time, it is helpful to explore the conditions under which one particular strategy is preferable to another.

As is true with the choice among traditional strategic alternatives, the desirability of a particular strategy is likely to depend on the congruence or fit between a company’s resources and capabilities and the demands and constraints of the market environment. More specifically, three factors influence the process by which a company will prefer a particular information-intensive marketing strategy over another: (1) the relative costs of the respective strategies, (2) the data in the CIF about customer response to the respective strategies, and (3) the firm’s capabilities and motivations as a processor of CIF data.

How, for example, might a company choose between a generic column and a generic row strategy? Formally, the firm’s objective is to choose a set of offerings so as to maximize its profits. The choice between the two strategies can be framed in terms of whether the company would prefer to choose a maximum set of offerings to a smaller number of the same customers (cross-selling) or a narrower set of offerings to the maximum number of different customers. In other words, to take the simplest case as an example, would the firm prefer to produce two versions of a single offering — each sold to one of two different customers (column strategy) — or single versions of two offerings both sold to the same customer (row strategy)?12

Given two customers, assume that both customers are equally positive about their respective offerings and that the first customer is equally positive about its respective offerings. The firm’s choice between the mass-customization column strategy and the capture-the-customer row strategy will then depend on the relative costs associated with each. Let us assume that there are both fixed and variable manufacturing and marketing costs associated with the two strategies. As noted, the mass-customization column strategy relies on the company incurring heavy fixed manufacturing costs (which it hopes to spread over as many additional units as possible) and low marginal or variable costs for each additional variant produced. At the same time, the marginal marketing cost of reaching additional customers is likely to be high. By contrast, the capture-the-customer row strategy involves an initial fixed marketing cost to reach each customer (which the firm hopes to spread over as many additional products as possible) and low marginal or variable costs for each additional product offered. However, the marginal manufacturing cost of producing additional products for that same customer alone is likely to be high. Within this framework then, if we assume that the fixed manufacturing costs and variable marketing costs for the row strategy are relatively minor, as are the fixed marketing costs and variable manufacturing costs for the column strategy, the row strategy will be preferred to the column strategy if the fixed marketing costs plus variable manufacturing costs for the row strategy are less than the corresponding fixed manufacturing costs plus variable marketing costs for the column strategy.

A second factor influencing the choice of strategic alternatives is the information on consumer response to the respective strategies. Let us assume that the costs associated with the column and row strategies are constant and focus on response-to-company decisions and the extent to which differences in the available information about customer response will lead the company to prefer one strategy over another. Whether the firm will prefer the column strategy over the row strategy will depend on whether, in the aggregate and at the margin, the responses of multiple customers to the single (multiversion) offerings are more positive than the response of a single customer to the multiple offerings.

Assuming perfect information about customers, the set of customer responses will depend on the firm’s actions and skills in responding to a wide variety of tastes through customization (column strategy) and/or developing a deep relationship with a given customer through communication (row strategy) — that is, on how well its offerings actually meet customer needs.13 At the same time, in practice, customer response will depend on the firm’s ability to learn about what these needs are in the first place — on how well it is able to collect and process information about its customers. In particular, if I move beyond the simple example, as both the sets of customers and offerings expand, the assumption of perfect information is likely to prove false. If so, then the choice between the two strategies is likely to depend on the relative quantity and quality of the data in the CIF about customer response that are associated with each of them.

Many factors will influence how much and what kind of data make their way into the CIF — that is, which particular subsets of customer response to firm decisions are populated with reliable and valid information about customer-response patterns. These factors include technical marketing research capabilities and resources as well as the firm’s history in dealing with its customers. At the same time, whether a given subset of data exists in principle somewhere in the CIF is far less important than whether it exists in fact as an aid to decision making and is actually used.

The final factors influencing the choice among strategic alternatives are the capability and motivation of the firm and its individual managers as information processors. As noted earlier, in smart markets, the ability to process information, not the information itself, is the scarce resource; a large, influential body of literature has demonstrated persuasively that individuals’ restricted capacity to process information should often be considered the constraining factor in decision contexts. Managers as decision makers do not process the full range of information pertaining to a decision, but instead restrict their attention to a reduced subset.14 In so doing, they often violate what is referred to as “procedural invariance” — the normatively appealing principle that the relative weights applied to various items of information should be independent of the specific procedure used to process the information. The specific procedure used may be based on any number of factors: the perception of its necessity, the information’s accessibility, or the ways in which the information is framed or presented.15

While any of these and other factors may lead managers to favor a particular strategy over another, one that is perhaps most relevant for decisions based on processing the CIF is the way in which the company organizes and accesses information. For example, the CIF may be a relational database in which presentation is dependent on the different views of the data available, often within a query processing program. Thus, if a manager asks the program to “show me all the information about customer i,” he or she is asking for a row view. If the manager asks the program to “show me all customers who respond to my product in this way” (e.g., who is price sensitive?), he or she is asking for a column view. Within this context, we can ask, Can a manager’s choice of one information-intensive strategy (e.g., column or mass customization) over another (e.g., row or capture the customer) be influenced by organizing the way the data in the CIF are presented, independent of other considerations such as cost? In particular, if information is presented by column (row), will that bias managers to undertake a mass-customization (capture-the-customer) strategy? Will the bias persist even if other normative considerations (such as the relative costs associated with different approaches) suggest that the chosen strategy may be inappropriate?

The answers to these and related questions are occupying a major part of researchers’ activities in the area of managerial decision making — as companies seek to understand the degree to which their own capabilities and motivations as information-processing “organisms” are crucial in enabling them to extract maximum value from their customer information assets. In the final analysis, the company that successfully answers the question, “What kind of computer do we want to be?” will win in smart markets.

References

1. M. Porter and V.E. Millar, “How Information Technology Gives You Competitive Advantage,”Harvard Business Review, volume 63, July–August 1985, pp. 149–160;

R. Glazer, “Marketing in Information-Intensive Environments: Strategic Implications of Knowledge as an Asset,” Journal of Marketing, volume 55, October 1991, pp.1–19;

R. Glazer, “Measuring the Value of Information: The Information-Intensive Organization,” IBM Systems Journal, volume 32, number 1, 1993, pp. 99–110; and

R.C. Blattbert, R. Glazer, and J.D.C. Little, The Marketing Information Revolution (Boston: Harvard Business School Press, 1994).

2. Firms are beginning to experiment with the concept of a “customer manager”; it is still too early to draw conclusions from these experiments. In industrial marketing, key account management is, of course, organized by customer; even so, the firm’s accounting systems typically favor profit and loss by product. The customer manager has bottom-line, profit-and-loss responsibility for a set of customer targets — i.e., he or she is charged with developing and delivering a set of offerings to chosen customers and will develop “customer plans” that specify the strategic objectives to be achieved with respect to the designated customer targets.

3. The extent to which some firms take the notion of “potential customers” in building the CIF is extraordinary. Implementation issues aside, several organizations conceptualize their potential customers as every household on the planet.

4. J.B. Pine II, Mass Customization (Boston: Harvard Business School Press, 1992).

5. The emergence of yield-management systems, which are effectively auctions, leads naturally to the notion of promotions as options and/or future contracts in which the seller offers the buyer the opportunity to buy a product at a later date for a specified price. See:

R.C. Blattberg and R. Glazer, “Marketing in the Information Revolution,” in Blattberg et al. (1994), pp. 9–29.

6. See:

R.C. Blattberg and J. Deighton, “Interactive Marketing: Exploiting the Age of Addressability,” Sloan Management Review, volume 33, Fall 1991, pp. 5–14; and

D. Pepper and M. Rogers, The One to One Future (New York: Doubleday, 1993).

7. S.H. Haeckel and R.L. Nolan, “Managing by Wire,” Harvard Business Review, volume 74, September–October 1993, pp. 122–132.

8. See, for example:

M.E. Porter, “What Is Strategy?” Harvard Business Review, volume 74, November–December 1996, pp. 61–81.

9. Glazer (1991).

10. The concept of an “offering,” as used here, includes all elements of the marketing mix — the product itself as well as its price, mode of distribution, associated communications activities, etc.

11. Increasingly, evidence shows that many catalogue mail-order companies are operating in the three-dimensional space, although they are doing so with a limited range of customers; so-called category stores (e.g., Circuit City, Home Depot) also compete in the three-dimensional space, although they do so with a limited set of product classes.

12. These issues echo the traditional distinction between product development and market development as alternative growth strategies.

13. Applications of behavioral decision research to marketing strategy suggest that, rather than responding to “exogenous” consumer preferences, firms may play a more active role in actually shaping these preferences. See, for example:

G.S. Carpenter and K. Nakamoto, “Consumer Preference Formation and Pioneering Advantage,” Journal of Marketing Research, volume 26, August 1989, pp. 285–298.

To the extent to which this is true, the desirability of the column or row strategy depends on the relative effectiveness of that strategy in influencing the structure of consumer preferences.

14. J.G. March and H. Simon, Organizations (New York: Wiley, 1958); and

J.G. March and Z. Shapira, “Managerial Perspectives on Risk and Risk Taking,” Management Science, volume 33, number 11, 1987, pp. 1404–1418.

15. A. Tversky, S. Sattath, and P. Slovic,

“Contingent Weighting in Judgment and Choice,” Psychological Review, volume 95, number 3, 1988, pp. 371–384;

J. Pfeffer and G.R. Salancik, The External Control of Organizations (New York: Harper & Row, 1978);

D.C. Hambrick, “Environmental Scanning and Organizational Strategy,” Strategic Management Journal, volume 3, April–June 1982, pp. 159–174; and

M.D. Cohen, J.G. March, and J.P. Olsen, “A Garbage Can Model of Organizational Choice,” Administrative Science Quarterly, volume 17, March 1972, pp. 1–25.