Achieving Full-Cycle Cost Management

Companies tend to assume that a large percentage of a product’s costs are locked in by design — that little can be done to reduce costs once the design is set. This belief has shaped many cost-management programs across diverse products’ life cycles. Because of it, firms will often focus on cost reduction during the design phase and cost containment during manufacturing. But are much of a product’s costs truly locked in during design?

To answer that, we studied the consumer-products division of Olympus Optical Co. Ltd. in Tokyo, Japan. In-depth field observations of the life cycle of the new Stylus Zoom camera helped provide a detailed understanding of how the company applies various cost-management techniques across a product’s life cycle. (See “About the Research.”) In particular, we investigated the level of costs that are designed in because that shapes the way a company manages costs across the product life cycle. If a significant portion of costs is designed in, we would expect to observe aggressive cost management predominantly in the design (and not the manufacturing) phase of the life cycle.

Instead, we found that Olympus Optical achieves significant cost reductions in manufacturing, contradicting the widely held assumption that a large percentage of costs are locked in during design. Indeed, our research demonstrates that costs can be aggressively managed throughout the product life cycle. Furthermore, we found that Olympus Optical applies various cost-management techniques in an integrated manner, with the outputs of some techniques acting as inputs to others, thereby increasing the program’s overall effectiveness. Our observations suggest that companies competing aggressively on cost might consider the adoption of some form of an integrated cost-management program that spans the entire product life cycle.

Five Techniques

A commonly quoted statistic is that 80% to 95% of the cost of a product is determined by its design and is therefore set before the item enters manufacturing.1 That assumption has been used to suggest that the dominant focus of cost management should be during product development, not manufacturing.2 In fact, as one textbook states, “Once a product has been designed and gone into production, not much can be done to significantly reduce its cost.”3 Similar assumptions also appear in the practitioner literature.4

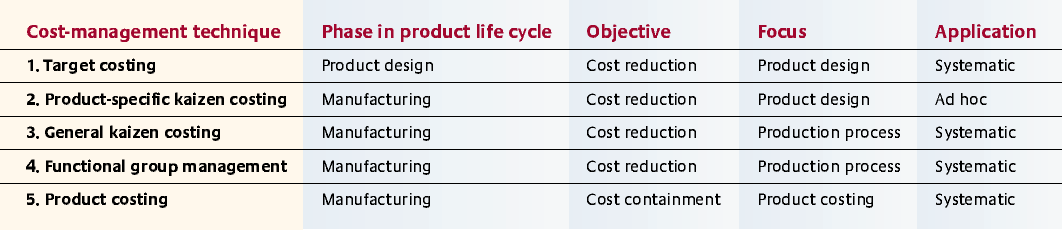

But our research suggests otherwise. Specifically, we found that Olympus Optical is able to manage costs throughout a product’s life cycle. To do so, the company deploys five major techniques: (1) target costing,5 (2) product-specific kaizen costing, (3) general kaizen costing, (4) functional group management and (5) product costing. (See “Five Techniques for Managing Costs.”) Each plays a crucial role in the firm’s integrated approach to cost management.

Target Costing

This technique is applied during the design stage as a feed-forward mechanism through which engineers retool the design of a new product to reduce costs while maintaining a desired level of product functionality and quality. At Olympus Optical, the first step is to identify the price point at which a new camera model would sell and from that to determine the free-on-board price — the amount the company would receive on the sale of the product. Target costs are then established by subtracting the product’s desired profit margin from its free-on-board price. Next, product engineers look for creative ways to attain the desired level of functionality and quality at the target costs.

For major cost reductions, the company applies value engineering in four different areas. First, it tries to reduce the number of parts in the product. Second, it eliminates expensive, labor-intensive and mechanical-adjustment processes whenever possible. Third, it replaces metal and glass components with cheaper plastic ones when appropriate. Lastly, it pressures suppliers (both internal and external) to reduce costs more aggressively.

Olympus Optical’s senior management places particular importance on target costing because the manufacturing phase of the life cycle of modern point-and-shoot compact cameras is short. (The typical product is on the market for only 12 to 18 months.) A short manufacturing phase makes it difficult for product engineers to correct any design problems (including those that result in high manufacturing costs) after an item has entered production. Thus the company encourages people to solve as many cost problems as they can during the design phase.

Product-Specific Kaizen Costing

This technique enables the rapid redesign of a new product during the early stages of manufacturing to correct for any cost overruns. During the trial production of the Stylus Zoom, for example, management discovered that costs were about 10% above target. Furthermore, when the product entered mass production at Tatsuno, Japan, the costs were found to be even higher. Overall, the production costs were an additional 5% more than the trial costs, making the total cost overrun 15%. Normally, the earlier 10% cost overrun would have led to either the postponement or cancellation of the project. But Olympus Optical proceeded with the Stylus Zoom because the company considered it to be a flagship product.

For the new camera, the window of opportunity for product-specific kaizen costing was just 11 months after product launch — shorter than might first be anticipated for such a high-volume product with a multiyear manufacturing life. During that time, Olympus Optical reduced costs in four major ways: by decreasing the number of parts in the product, by replacing certain materials with cheaper ones, by managing supplier costs and by transferring production overseas where overall costs were lower. The primary rule was that the product’s functionality and quality had to remain constant. From the customer’s perspective, the last Stylus Zoom off the production line had to be identical to the first.

General Kaizen Costing

This technique focuses on the way a product is manufactured; the assumption here is that the product’s design is already set. (This contrasts with target and product-specific kaizen costing, which do not treat a product’s design as a given.) General kaizen costing can be particularly effective when it addresses manufacturing processes that are used across several product generations. In such cases, savings achieved during the manufacturing cycle of a particular product could continue long after its withdrawal from the market.

In general kaizen costing, management sets cost-reduction goals for production processes and empowers the workforce to find ways to achieve them. Olympus Optical’s approach focuses primarily on reducing material, labor and some overhead costs. For example, sales, general and administrative costs associated with the control and procurement departments are included in the analysis. At Tatsuno, the company set individual cost-reduction goals for each assembly line and thus for each internally produced component of the Stylus Zoom. To achieve those goals, which were designed to be challenging but attainable, workers undertook a variety of actions, including finding ways to speed up manufacturing processes by integrating certain steps so that the same person could perform them.

Functional Group Management

This technique consists of breaking the production process into autonomous groups and treating each as a profit (instead of a cost) center.6 There are two reasons for doing so. First, the switch to profit as opposed to cost centers allows the groups to increase the throughput of their production processes even if those changes result in higher costs. That is, functional group management supports actions that increase both costs and profits through greater revenues —something that general kaizen costing, which focuses solely on reducing costs, does not. The second motivation is the change in mind-set that functional group management induces. Converting the production lines to profit centers helps the groups to better understand their contribution to the company’s overall profitability.

The production process at Tatsuno was broken into 10 autonomous groups. By finding ways to increase their output levels, those groups were able to generate additional revenues and greater profits. The capacity of the factory increased as a result, leading to real performance improvements. For example, in the first three years of functional group management, about 80% of the profit improvements were from changes that increased output, with the remaining 20% from cost-reduction initiatives.

Product Costing

This technique helps coordinate the efforts of the other four techniques by providing them with important, up-to-date information. The process consists of three major functions. The first is to determine if new products are indeed being manufactured at their target costs. The second is to ensure that the production processes are operating at the expected level of efficiency. And the third is to identify unprofitable products for further action, such as replacement or aggressive cost reductions.

Application of Techniques

At Olympus Optical, the total amount of resources dedicated to cost management is high, as is expected for any company in an intensely competitive environment.7 The important point, though, is that the organization does not assume that the majority of costs are locked in during the design phase. In fact, Olympus Optical applies cost-management techniques throughout the product life cycle, with just one technique (target costing) taking place during product design and the rest during manufacturing. And there are other important aspects of how the company deploys the five cost-management techniques. (See “Five Techniques for Managing Costs.”)

Cost Reduction Versus Containment

Four of the techniques reduce costs, while the other (product costing) contains them. In cost reduction, people actively try to lower costs to preestablished levels. Cost containment is a more passive process that tries to sustain previously achieved cost-reduction objectives. During the design phase, target costing helps reduce the anticipated manufacturing cost of a product to a preestablished level, namely the target cost. Of the four techniques applied during the manufacturing phase, three (product-specific kaizen costing, general kaizen costing and functional group management) are used for cost reduction and the other (product costing) for containment.

Olympus Optical relies on product costing to monitor the actual costs during the manufacturing phase. When those costs rise to unacceptable levels — due, for example, to increases in component prices — general kaizen costing is applied to bring those numbers back in line with the previously established objectives. This limited role for product costing might seem surprising given the recent popularity of activity-based costing, but it reflects the way that Olympus Optical has designed its cost-management program.8 In the company’s approach, the primary role of product costing is monitoring — specifically, ensuring the maintenance of previously achieved cost-reduction objectives. Thus the firm dedicates just one technique to such a passive activity. In contrast, Olympus Optical deploys multiple techniques and greater resources to cost reduction, which is a more open-ended and active objective for achieving significant savings.

Product Design Versus Process Improvement

Cost management during the design phase consists solely of target costing, which necessarily focuses on improvements to the product design. In contrast, cost management in the manufacturing phase includes three techniques (product-specific kaizen costing, general kaizen costing and functional group management), of which only one (product-specific kaizen costing) is targeted toward product redesign. The other two techniques focus on making the production processes more efficient, and they each play different but reinforcing roles. General kaizen costing helps reduce the cost of performing production processes, whereas functional group management tries to increase output either by speeding up those processes or by increasing their yields. Lastly, product costing focuses on product costs because of the technique’s role of cost containment.

Ad Hoc Versus Systematic Application

Of the five techniques, only one (product-specific kaizen costing) is applied in an ad hoc manner. Specifically, it is used only for products that fail to achieve their target costs but for strategic reasons are launched anyway. The goal is to find any savings that people might have missed during the design phase. (Management at Olympus Optical views both product-specific kaizen and target costing as part of a continuous process for achieving the target cost through innovative product design.) Olympus Optical has a reason for limiting the use of product-specific kaizen costing. According to management, changing a product’s design (and hence the associated production processes) during the manufacturing phase can be highly disruptive, and in most cases the anticipated savings for products that have already achieved their target costs is not sufficient to justify the effort. Consequently, the company deploys product-specific kaizen costing just for high-volume products that have been launched above their target costs. Furthermore, the technique is applied immediately after the product is launched and only in the early stages of manufacturing to ensure that an adequate number of units are sold after the intervention to justify the upfront investment.

One interpretation of those policies is that management believes there is a limit to the level of cost reduction that Olympus Optical can achieve through product design and that the company’s target costs are close to that level. Many managers described the target-costing objectives as “stretch” or “tiptoe” in nature. The objectives were specifically set so they could be achieved only 80% of the time. According to management, that tactic resulted in the optimum amount of pressure: The objectives were difficult to achieve but reasonable enough for the engineers to take seriously. Consequently, trying to attain additional savings when a product is launched at its target cost is not worth the effort. But when a product is launched above its target cost, the benefits can outweigh the costs, as was the case with Stylus Zoom.

Olympus Optical deploys the four other cost-management techniques systematically for all of the company’s products. Their application, though, might be delayed to some extent when product-specific kaizen costing is also being used.

Olympus Optical’s Cost-Management Philosophy

All products at Olympus Optical undergo the same cost-management program, although some products under prespecified conditions might be subject to additional efforts. The Stylus Zoom camera, for example, underwent product-specific kaizen costing because it was a high-volume, strategic product launched above its target cost, not because it was fundamentally different in its cost-management requirements. In other words, Olympus Optical does not have two types of products, those with high locked-in costs and those without.

More importantly, our observations did not support the expectation that a high level of product costs at Olympus Optical would be locked in during design. Instead, we found that cost reduction in the manufacturing phase was a significant source of savings even when aggressive cost management had occurred in product design. The philosophy at Olympus was that costs can be reduced throughout the product life cycle and that savings can be achieved through a mix of low-cost product design and improvements to the production process. This philosophy was so ingrained that the team leaders and foremen in manufacturing met daily to discuss their progress in achieving their production-process objectives for reducing costs. Weekly meetings were also held to keep people on track. If a group did not meet its weekly objectives, its leader had to explain the reasons for the failure and then present a plan of corrective actions, which might include a request to engineering for help. When a group repeatedly failed to meet its objectives, management would occasionally send in engineering assistance — an action viewed as a serious blow to the reputation of that group.

If a high level of costs had been designed in, we would expect the application of target and product-specific kaizen costing (since both are design-related techniques) in combination with product costing for cost containment. And we might also expect some minor level of cost reduction in the manufacturing phase that was not related to product design. Instead, we observed the aggressive use of both general kaizen costing and functional group management in the manufacturing phase. Moreover, Olympus Optical products do not appear to fall into the other dichotomous category of having costs that can be lowered only through improved operating efficiency and productivity (as opposed to better design).

Our observations suggest that Olympus Optical has spent considerable time thinking through the design of its integrated cost-management program. According to management, the program has evolved purposefully with the goal of integration: When a new technique such as functional group management is adopted, the other techniques are modified to take advantage of it. The resulting integration demonstrates a significant level of sophistication. For example, the way that product-specific kaizen costing is applied demonstrates how carefully the company manages the cost-benefit trade-offs, with cost-management techniques deployed only when the expected benefits outweigh the costs. With Stylus Zoom, the high level of cost overrun required dramatic intervention from product-specific kaizen costing. The lens assembly, for example, was redesigned to significantly reduce the number of separate integrated circuits (and hence the product’s cost). Similarly, Olympus Optical’s recent addition of function-group management to the company’s suite of cost-management techniques indicates an active, ongoing effort to improve the program. Furthermore, it suggests that management believes that significant savings are possible via improvements in the production process, even given the presence of general kaizen costing.

Because we carefully selected Olympus Optical as our research site to favor the assumption that a significant portion of costs are designed in, our observations place considerable doubt on the validity of that assumption. Of course, we cannot dismiss the possibility that other products have a high level of costs that are locked in by design, but our findings suggest that for manufactured goods like those at Olympus Optical those types of products are the exception and not the rule. And we would expect that many manufactured products share the same characteristic of costs that are manageable across the entire life cycle.

Integrated Cost Management

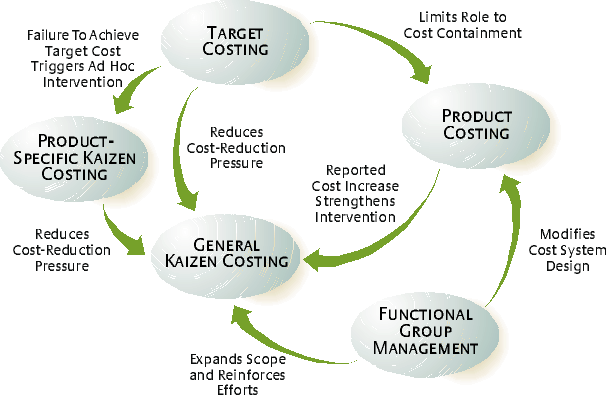

Another crucial aspect of Olympus Optical’s cost-management program is that it is more than just five independent techniques. Instead it is an integrated system, with the outcomes from some of the techniques used as inputs for others. (See “Integrated Cost-Management Program.”) Management asserts that such integration is necessary to achieve the company’s profit objectives. The belief is that integration provides additional savings above and beyond those associated with the individual techniques.

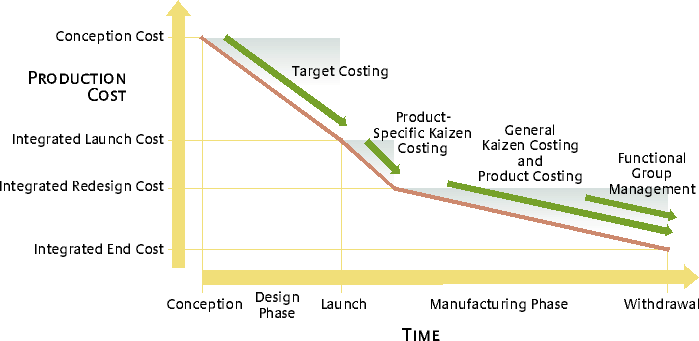

According to Olympus management, there are three major benefits to integrated cost management. First, it leads to overall lower costs throughout the product life cycle. Not only do products cost less at launch (thanks to target costing), but the ongoing activities also ensure that they have steadily decreasing costs all the way through to discontinuance. (See “Reduction of Production Cost Over Time.”) Typically, the annual cost reduction during the manufacturing phase (including savings from suppliers) is about 17%. So for a product with a two-year life, the savings during manufacturing could exceed 30%, and the designed-in cost would thus be below 70%. Products with a longer life would potentially have even greater cost reductions during manufacturing. Second, Olympus’ experience has shown that more products are launched on time. Without an integrated program (and, in particular, without the discipline of both target and product-specific kaizen costing), a greater number of product launches would have to be delayed to bring their costs in line with their selling prices. Finally, fewer product introductions are cancelled. The tight discipline of target costing with its emphasis on target prices forces the design process to be cost-sensitive from the very beginning.

To attain those benefits, the five cost-management techniques at Olympus Optical are linked in various ways. For example, integration between target and product-specific kaizen costing enables the continual redesign of products. Target costing also reinforces the effectiveness of product-specific kaizen costing by identifying those products with cost overruns before they enter production. Thus, target costing provides an early warning of the need for intervention. The major difference between the design activities under the two techniques is that target costing has the ability to change product functionality, whereas product-specific kaizen costing does not, due to management’s decree that the functionality of the first product off the manufacturing line must be identical to the last. When a product is launched, its design is frozen for the first few months of production until workers have learned to manufacture it efficiently. During that period, though, engineers are busy identifying ways to reduce costs by redesigning the product.

Target costing also reinforces general kaizen costing by identifying the savings that the company should achieve during manufacturing and by isolating that amount from the cost reductions that could reasonably be anticipated during product development. By setting the appropriate target costs for new products, Olympus Optical can ensure that the cost-reduction objectives for general kaizen costing and functional group management are attainable. In other words, target costing helps avoid the application of excessive cost-reduction pressures during manufacturing. This is important because general kaizen costing (and any cost-reduction technique, for that matter) is most effective when the objectives are considered achievable, even if they require considerable effort.

Product-specific kaizen costing also helps ensure that general kaizen costing isn’t subjected to undue pressures. It achieves this by continually decreasing costs through product redesign during manufacturing. If a product’s costs can be reduced as close as possible to the target level, then the pressure on general kaizen costing won’t be excessive.

Typically, Olympus Optical does not include the anticipated savings from general kaizen costing in the company’s target-costing analysis. However, if the life cycle profitability analysis indicates that a product won’t achieve its target profit margin, the anticipated general kaizen savings are included. If those savings enable the product to achieve its target margin, the product-development process continues. On the other hand, if the savings aren’t sufficient and the product is not considered strategic, the project is cancelled. The general practice of excluding the anticipated general kaizen savings (unless their inclusion is necessary to support the launch decision) reflects Olympus Optical’s conservative approach to cost management.

The interaction between target and product costing is subtler. In companies that lack a sophisticated target-costing system, one of the roles of product costing is to determine whether new (as well as existing) products are profitable. But that responsibility often conflicts with the other primary purpose of product costing, which is operational control.9 Olympus Optical frees product costing to focus solely on cost containment because the company also deploys target costing and operational control through kaizen costing and functional group management.10 Thus, Olympus Optical does not consider product costing to be a source of cost savings. Instead, the primary role of product costing is to support the other techniques and to help maintain the cost savings that they achieve.

General kaizen costing and functional group management are integrated in that the role of the latter is to enhance the former by giving workers a new way to think about cost reduction. In particular, functional group management shifts the task from cost reduction to profit enhancement. This change expands the type of activities that people can consider to include ways for increasing throughput (thereby enhancing revenues) without incurring undue costs (thereby generating additional profits). In addition, Olympus Optical management believes that the shift to profit enhancement has led to workers being more motivated toward cost reduction. In fact, the cost-reduction objectives set by the individual groups have been consistently more aggressive than those established by divisional management.

Functional group management relies on product costing for information necessary to generate profit-and-loss statements for the different groups. Those reports then enable Olympus Optical to make better decisions for increasing the company’s profitability by pursuing different ideas for generating additional revenues.

Finally, general kaizen and product costing work in tandem to contain costs that have climbed above previously achieved levels. When that happens, new cost-reduction targets are established for general kaizen costing to bring those numbers back in line. The cause of the increase is irrelevant; the objective is to keep costs at previously achieved levels so that the company can sustain the budgeted profits.

Implications

Our research at Olympus Optical has three major implications. First, even in an environment of products with short life cycles and aggressive cost management focused on product design, a company can still achieve significant savings through efforts targeted at making the production process more efficient. That is, the costs of products can be aggressively managed throughout their life cycle. Second, companies should consider using multiple cost-management techniques across the entire product life cycle. Third, the stand-alone use of those techniques might limit their effectiveness. Integrating them can lead to even higher levels of cost reduction and superior overall performance as measured by on-time launches of profitable products.

One critical aspect that companies need to consider is the length of the manufacturing phase of their product’s life cycle. As its duration increases, so does the opportunity for cost reduction in that phase. Therefore, firms that have products with a long manufacturing phase should be especially active in exploring the value of integrating multiple cost-management techniques during manufacturing. The same holds true for organizations that rely on production processes that are stable over time even though the product mix varies.

Obviously, field research at a single site will not always be applicable to other locations. But because our study investigated a widely held assumption at a site where that assumption was likely to apply, we could reasonably argue that the preponderance of costs is not designed in at many other settings. Thus we recommend that companies that compete aggressively on cost should consider adopting a cost-management program consisting of multiple techniques applied in an integrated manner to different phases of the product life cycle. The techniques might have different objectives (for example, cost reduction versus containment) and a different focus (product design versus production processes). Furthermore, some of the techniques might be applied systematically to all products, while others might be used in an ad hoc manner on just those products that require special attention.

Those recommendations aside, the exact nature of the program, the techniques that are deployed and the way that they are both applied and integrated will no doubt vary at different companies. Olympus Optical, for example, does not use activity-based costing, possibly due in part to two factors related to cost management. First, Olympus may not need an activity-based costing system to obtain accurate product costs because the company only performs high-volume manufacturing. Second, the cost-reduction insights that activity-based costing provides might be redundant because of Olympus’ use of general kaizen costing and functional group management. Information from those two techniques might substitute to some extent for an activity analysis of the firm’s production process.

But many companies, especially those with a highly diverse production volume and product complexity, might want to include an activity-based system in their integrated cost-management program. Still other organizations might decide against adopting target costing because their products are too innovative. (Target costing works best when information about previous generations of products is highly predictive of the costs of future generations.) Finally, some companies might want to integrate their Six Sigma efforts into their cost-management program. Because of such differences, Olympus Optical’s program might best be used as a model of general concepts for other organizations to consider.

References

1. The origin of this statistic is difficult to identify but it appears to derive from B.S. Blanchard, “Design and Manage to Life Cycle Cost” (Portland, Oregon: M/A Press, 1978).

2. R.S. Kaplan and A.A. Atkinson, “Advanced Management Accounting,” 3rd ed. (Upper Saddle River, NJ: Prentice Hall, 1998), 223; and C.T. Horngren, S.M. Datar and G. Foster, “Cost Accounting: A Managerial Emphasis,” 11th ed. (Upper Saddle River, New Jersey: Prentice Hall, 2002), 417–418.

3. R.H. Garrison and E.W. Noreen, “Managerial Accounting,” 9th ed. (Chicago: Irwin McGraw Hill, 2000), 814.

4. See, for example, J.M. Brausch, “Beyond ABC: Target Costing for Profit Enhancement,” Management Accounting 76 (November 1994): 45–49; R. Henkoff, “New Management Secrets From Japan — Really,” Fortune, Nov. 27, 1995, 135–146; G. Böer and J. Ettlie, “Target Costing Can Boost Your Bottom Line,” Strategic Finance 81 (July 1999): 49–52; G. Schmelze, R. Geier and T.E. Buttross, “Target Costing at ITT Automotive,” Management Accounting 78 (December 1996): 26–30; J.H. Hertenstein and M.B. Platt, “Why Product Development Teams Need Management Accountants,” Management Accounting 79 (April 1998): 50–55; and S. Ottosson, “Dynamic Product Development —DPD,” Technovation 24 (March 2004): 207–217.

5. For a thorough description of target costing, see R. Cooper and R. Slagmulder, “Target Costing and Value Engineering” (Portland, Oregon: Productivity Press, 1997).

6. Other firms have introduced similar systems for the same reason. For example, Kirin Brewery Company, Ltd. used its Kyoto Brewery System and Higashimaru Shoyu Co. Ltd., a soy sauce manufacturer in Japan, introduced its price control system to motivate cost reductions in their production processes; see R. Cooper, “When Lean Enterprises Collide: Competing Through Confrontation” (Boston: Harvard Business School Press, 1995).

7. P.N. Khandwalla, “The Effect of Different Types of Competition on the Use of Management Controls,” Journal of Accounting Research 10 (autumn 1972): 275–285.

8. R.S. Kaplan and R. Cooper, “Cost and Effect: Using Integrated Cost Systems To Drive Profitability and Performance” (Boston: Harvard Business School Press, 1997).

9. Ibid.

10. Y. Monden, “Cost Reduction Systems: Target Costing and Kaizen Costing” (Portland, Oregon: Productivity Press, 1995); and R.S. Kaplan and A.A. Atkinson, “Advanced Management Accounting,” 3rd ed. (Upper Saddle River, New Jersey: Prentice Hall, 1998).