Capture and Communicate Value in the Pricing of Services

Topics

The pricing of services in the United States is a mess. Consider these examples:

- In 1992, Congress enacted the Cable Act to rein in prices in the cable television industry. This legislation, prompted by widespread consumer dissatisfaction with price increases and poor service, gave broad regulatory powers to the Federal Communications Commission and local communities. Although the sweeping 1996 telecommunications bill phases out price regulation for cable television beyond a basic “broadcast tier,” concerns persist about whether the industry can be trusted with pricing freedom. By 1994, two years after the Cable Act had been enacted, the FCC had received 10,600 complaints dealing with cable rates.1

- In 1994, a Gallup survey of 1,000 bank customers found that 49 percent believed that bank fees were too high. Moreover, 20 percent indicated that they had changed banks recently, primarily because of poor customer service, followed closely by fees and interest rates.2

- In 1990, a Maritz Marketing Research national consumer poll indicated that 61 percent of the respondents thought the automobile insurance industry needed more regulation to ensure fair practices and prices. Subsequent research shows that many automobile insurance customers believe they are being ripped off and resent what they perceive to be price gouging and false promotional promises.3 In 1988, California voters approved the controversial Proposition 103, which regulates pricing and profits in the industry. The California Supreme Court upheld the law in 1994; the U.S. Supreme Court upheld it in 1995.

- In 1992, a Brookings Institution study, commissioned by Aetna Life & Casualty Company, concluded that hourly billing for legal services leads to unnecessary, more expensive work.4 Many corporate clients are currently fighting this practice. Companies such as Walt Disney, Citicorp, and Merck have adopted guidelines that limit hourly fees and reimbursable charges and standardize billing formats. General Motors has developed a database that tracks litigation and determines average expenses for handling different matters. GM questions law firms whose fees exceed the averages and sometimes insists that fees be reduced. Dow Chemical’s on-line computer monitoring system “looks for people billing who weren’t approved to work on the case, looks for hourly rates that weren’t consistent, and looks for duplicate billing.”5 Some companies are hiring outside auditors to monitor their legal bills for improper or inaccurate charges.

These examples from the cable television, banking, auto insurance, and legal services industries are indicative of widespread pricing mismanagement in the service sector. Clearly, much of what is happening is not working, and marketers need fresh approaches.

Common services pricing practices are benefiting neither customers nor companies. Basic to the problem is the fact that services marketers too often ignore the special challenges involved with pricing intangible products. They formulate their pricing strategies without really understanding how their customers use and benefit from the services that they offer. Customers, in turn, are confused about the true prices they are paying and wonder whether they are getting the best value. An atmosphere of mistrust has developed in many service markets, opening the door to government intervention. Moreover, in numerous service industries ranging from car rental to health insurance, profit margins are narrowing or, in some cases, disappearing altogether.

In this article, we discuss the implications of pricing intangible products in today’s intensely competitive markets and offer a framework that reconciles these implications with customers’ quest for value. Following our advice will not be a simple matter for some companies. It may mean carving out a new strategy for the business and earning customers’ confidence gradually. Pricing services effectively calls for a longer-term perspective than some executives may feel is practical.

Implications of Pricing Intangibles

Unfortunately, little research exists on the pricing of services, and few people understand the special challenges involved.6 But services are a special breed of product, and marketers need to treat them as such. Services are performances; therefore, they are intangible. Goods, on the other hand, are objects; they can be seen and touched. Customers can see tangibles associated with the service, such as the people who provide the service and the equipment, but they usually cannot see the service itself. This inherent invisibility creates conditions that are far from ideal for services marketers, but they need to consider it if they want to improve their pricing practices.7 Purchasers of goods acquire tangibles — a couch, a VCR, a necktie, tennis shoes, toothpaste. Purchasers of services incur an expense rather than add to their accumulation of goods. They might, for example, take a trip, visit the doctor, or get a haircut, but at the end of the day, their “market basket” is empty. Purchasers of goods buy ownership and use; purchasers of services buy only use. A dry cleaner or an auto mechanic returns customers’ property to an earlier state: clean clothes or a well-running automobile. Credit card issuers rent money and hotels rent space, but no transfer of possession occurs. Automobile insurance “pays off” for customers only when something bad happens.

Recognizing this subtle but important distinction between tangibility and intangibility can provide useful clues to understanding customers’ reactions to services prices.8 Take, for example, a plumbing company that charges $60 to fix a leaky toilet. By charging that amount, the plumber aims to recoup the fixed and variable costs of operating the business (facilities, trucks, labor, telephones, insurance, gasoline), as well as to generate a profit. Customers, on the other hand, might be shocked at a price of $60 for twenty-three minutes. They could have bought a new sweater or some compact disks for that, they might say. The psychology of the transaction is not favorable to the plumber.

Comparing Prices, Making Choices, Assessing Value

The intangibility of services makes it more difficult for customers to compare prices. In a supermarket, prices are affixed to tangible products grouped by category, but the nonphysical nature of services impedes price and product comparisons. Since the products are invisible, customers cannot easily see their costs. For example, they have no fast method for comparing AT&T, MCI, and Sprint long distance services or prices before deciding which to select. Thus intangibility accentuates the complexity of services prices for customers.

Services differ from goods in the degree to which they possess search, experience, and credence attributes, three categories that help marketers distinguish among products. Those that can be evaluated before purchase and use have search attributes, those that can be evaluated only after they have been used have experience attributes, and those that cannot be fully evaluated even after use have credence attributes.9 In general, tangible products are more likely to possess search attributes, whereas services tend to be higher in experience and credence attributes.10

Clients who hire a lawyer, for example, will want to hire a competent and conscientious person, but how are they to do that? Few search attributes exist to guide their decision process. There are no tires to kick, nothing to test-drive. Word-of-mouth can help if available, or a lawyer’s years of experience may be a useful indicator. A prospective client may choose to phone or visit various law firms to get cost estimates, but estimates frequently are inaccurate in the long run. Even if a client believes that an estimate will be reliable, how can it guide the choice of a lawyer? Who would be better, the least expensive or the most expensive? Lacking firsthand experience with a product, customers often use price as a surrogate indicator of quality. They assume that the least expensive lawyer may also be the least skilled, and vice versa.

Legal services typically are high in experience and credence attributes. The legal client evaluates quality and value when experiencing the service and, to some degree, may never know if the lawyer performed optimally. Services having credence properties usually are technical in nature or are not performed in the customer’s presence. Automobile repair, medical, marketing research, and many other services have one or both of these characteristics. Customers wonder, were all the repairs necessary? Were they done properly? Were the laboratory tests performed correctly? Did the patient actually have all the tests that the hospital bill lists? Did the marketing research firm train its interviewers?

Services in general, and credence services in particular, invite pricing and performance abuses. Customers know that they are vulnerable to such abuses, so they are suspicious about being taken advantage of and become resentful and angry when it happens. For that reason, Sears has never completely recovered from the widely publicized charges that it defrauded its auto center customers by selling unneeded parts and services. Service customers tend to remember that kind of experience for a long time.

The difficulty in evaluating the pricing of some services has opened the door to companies that specialize in monitoring the accuracy and appropriateness of charges within a particular industry. Accu-Pay, for example, checks hospital bills for accuracy and has had astounding results. In 1993, the company’s first full year of operation, Accu-Pay didn’t find a single bill that was completely accurate. The average overcharge was 11 percent.11 Legalgard, a company that monitors law firm invoices, claims it finds suspicious charges in four of every five bills.12

Undifferentiated Offerings

The lack of physical differentiation among competing services is another factor that contributes to poorly executed pricing. The styling of an automobile, the fit and feel of a pair of slacks, the color and pattern of a necktie, even the picture on a cereal package differentiate a product from its competitors and give customers a reason not related to price for favoring it. Tangibles — for example, the appearance of service facilities and providers — play a role in differentiating services too, but often the tangibles associated with a service are relatively unimportant to the purchase decision or differ little from the competition.13 For this reason, marketers try to differentiate their service through nonphysical means — quality or price, for example — and, frequently, they concentrate on the price tool. Price may seem easier to implement, faster in its effects, or more persuasive with targeted customers.

The pricing of airline services, which by and large are marketed as a commodity, is a case in point. When one carrier announces a price cut, its competitors usually match the cut within hours. The industry makes thousands, even hundreds of thousands of domestic fare changes daily, creating a nightmare of confusion for customers and employees. American Airlines’s best fare from Dallas to Memphis today may cost $200 more or less tomorrow.

The perceived similarity of the service, plus its perishability (once the plane leaves, empty seats cannot generate revenue), plus the high fixed costs of offering the service (some revenue is better than none), plus the necessity for financially weak companies to generate cash flow combine to create an airfare system of bewildering complexity. In fact, the situation has given rise to new services: for a $5 fee, TravelFest, an Austin, Texas-based travel agency, monitors clients’ reservations and notifies them if a lower fare becomes available. Airline executives’ perception that they must lead with price marketing to compete is not the only reason for the industry’s frantic, confusing pricing practices, but it is an important one.

Airlines services are only one of many in which pricing practices are not working well. To alleviate the situation, we propose three distinct but related strategies tailored to the unique pricing challenges that services present. When executed well, they can enable services marketers to capture and communicate value.

Value Strategies for Services Pricing

The key to improved services pricing is to clearly relate the price that customers pay to the value that they receive. A customer may or may not look for the absolute lowest price available for a service, but everyone wants something worth the price he or she pays. Services pricing strategies often derail because they lack any obvious association between price and value.14

For customers, value means benefits received for burdens endured. No product is free of cost, which comes in two forms: monetary (the economic price) and nonmonetary (for example, time or physical or mental effort). When making purchasing decisions, customers want to feel they are getting at least as much as what they are paying; that is, the benefits should be commensurate with the burdens.

Not understanding this trade-off, services marketers frequently undermine the effectiveness of their pricing strategies. Consider an advertising campaign for a service that claims the lowest available prices but presents them in a complex series of combinations. That kind of pricing message carries a heavier burden for customers than the advertiser realizes. Customers have to figure out how the different pricing plans work, which one is the best, and whether any of them actually give them more value, or whether they are all just hype. The nonmonetary burden of such a pricing strategy increases the customers’ overall burden and therefore weakens the marketer’s benefits-to-burdens offer.

The importance of considering nonmonetary cost as part of the value message in services pricing is illustrated by the avalanche of calling plans that the big long distance telephone companies have unleashed during the past few years. Collectively, they spent hundreds of millions of advertising dollars for an unrelenting stream of lowest-price claims and pricing counterattacks.

Through its “True USA Savings” program, AT&T offered a 10 percent discount to customers spending $10 to $24.99 per month, a 20 percent discount for spending $25 to $74.99, and a 30 percent discount for charges of $75 or more. Then, through its “True Rewards” campaign, AT&T allowed frequent callers to accumulate frequent flyer points, cash, or free talk time.

MCI’s pricing options included “Friends & Family,” which offered a 20 percent discount on calls to a preset group of MCI customers; “Friends & Family II/Sure Savings,” which included a 40 percent discount to current MCI customers and a 20 percent discount to non-MCI customers; and “Personal Thanks,” which featured points for merchandise, free minutes, and even airline tickets.

Among Sprint’s programs was “The Most,” which gave customers a 20 percent discount on calls to the most called number, as well as to other Sprint customers, and a 36 percent discount if they were one and the same. Sprint also offered “The Most II,” a feature that included tiered discounts based on long distance spending, and “Priority Rewards,” which tabulated points for airline tickets, merchandise, and free phone time.

Although this strategizing had some impact on shifting market shares — particularly MCI’s original “Friends & Family” plan, which represented a departure from prevailing offers in the market — survey results reveal many turned-off, unpersuaded customers. A 1995 study of customers’ perceptions of long distance telephone providers conducted by CDB Research & Consulting found that 60 percent of the respondents were confused by the many different calling plans. Among customers with incomes of $50,000 or more and those aged 18 to 34 — two coveted markets — 78 percent indicated they were tired of all the advertising and hype about long distance rates. Moreover, 60 percent of the respondents felt that all the major long distance companies charge essentially the same.15

In an interesting footnote, customers’ frustration resulting from the complexity of the big companies’ calling plans provided a window of opportunity for new entrants such as LCI International, which offered a simple, flat-rate pricing plan in 1992. Sprint offered its own flat-rate pricing scheme in 1995, and others have recently followed suit. AT&T and MCI have also moved toward more simplified pricing structures. The industry seems to be grasping the significance of straightforward pricing for value. The complexity and risk associated with buying many services underscores the need for services prices to be straightforward, easy for customers to understand, and clearly linked to the customers’ perception of value. Such an approach lessens the complexity of customers’ buying decisions and conveys pricing integrity. Prices are more credible when they are understandable and simple, and customers don’t suspect pricing tricks or hidden charges. The risk that customers take on when they buy services with experience or credence properties lends persuasive power to pricing strategies that instill trust and confidence.

Not only should marketers avoid needless complexity in their services pricing, they should also avoid simplistic approaches that fail to recognize the heterogeneity of customers’ wants.16 Prices can be straightforward, easy for customers to understand, and communicate value without being simplistic. Sometimes, customers realize the most value from a service by being able to buy different benefit levels at different price levels. Movie theaters, for example, increase the value of their service by allowing customers to choose whether to pay a higher price for prime time or a lower price for non-prime time. Such segmented pricing also lets the movie theaters synchronize demand patterns with supply capacity. Without segmented pricing, more customers would go to the movies in the evening, and the facilities would be underutilized during the day.

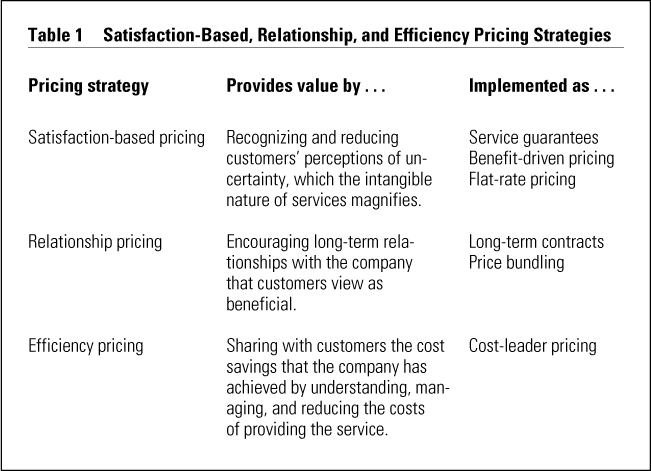

In order to price for value, services marketers must first understand what constitutes value for their target markets. Their goal then becomes capturing and communicating this value proposition — as clearly and compellingly as possible — through the pricing. We suggest three distinct but related pricing strategies for capturing and communicating the value of a service: satisfaction-based, relationship, and efficiency pricing. They can be used independently or in combination. (See Table 1 for a brief description of how each strategy works.)

{kind=link}

Satisfaction-Based Pricing

The intangible nature of services challenges both company and customer to clearly establish the value of the service. Some uncertainty is associated with any purchase, whether it is a service or a tangible product, but intangibility accentuates the uncertainty. The goal of satisfaction-based pricing strategies is to alleviate customers’ uncertainty. Companies can do this in several ways, including service guarantees, benefit-driven pricing, and flat-rate pricing.

· Service Guarantees.

Explicitly guaranteeing a service can be a powerful reassurance for customers. Even if they end up dissatisfied with the service, the guarantee gives them a recourse — usually a reduced price or refund —for a burden that they have endured. When executed well, service guarantees symbolize both a company’s commitment to customer satisfaction and the confidence it has in the quality of its service.17 After all, no one would expect a business to guarantee a poor service. Companies should not adopt this strategy lightly, however. A service guarantee is a bold step, calling for a thorough analysis of the reasons for doing so, as well as the risks involved.

One success story is that of Bank One, which found itself in the unusual situation of having to start a trust division. In 1989, Bank One acquired a failed Texas bank that had sold its trust department. Managers of the start-up trust unit believed that only a positioning of superior service would make the fledgling operation competitive. Since it had no reputation that could reassure prospective clients, senior managers decided to guarantee its service unconditionally.

The guarantee that Bank One adopted is straightforward: any clients dissatisfied with the service need not pay the fee. The written guarantee reads: “If you are not satisfied with our service quality in any given year, we will return to you the fees paid, or any portion thereof you feel is fair.” Customers wishing to invoke the guarantee must inform the bank in writing within ninety days of the end of the account year.18 Between 1989 and 1995, seven clients (of 4,500 accounts) invoked the guarantee and received refunds. According to management, all the claims were justified and were for essentially the same reason: making promises to clients during the sales process that were not kept.

Today, Bank One Texas Trust is one of the fastest growing trust banks in the nation. Clearly, its service guarantee has contributed to its success by reducing clients’ uncertainty about the service, as well as by giving staff a strong incentive to understand and meet clients’ expectations. In effect, Bank One Texas Trust is offering a price that is adjustable down to zero, based on the clients’ perception of satisfaction with the service.

Service guarantees make the most sense for companies that market services perceived as high-risk, that wish to capitalize on their superior service quality, or that need a differentiating message to enter a market against established competitors. All three conditions apply to Bank One Texas Trust. Companies with poor or mediocre service should improve their service significantly before considering a service guarantee.

Implementing satisfaction-based pricing through a service guarantee is a potent strategy under the right conditions. To muscle into the pizza delivery sector, Domino’s used a no-charge policy, then a $3 rebate, for pizzas delivered beyond its thirty-minute guarantee. Later, this powerful strategy created a huge problem for Domino’s — publicity and lawsuits alleging unsafe driving to beat the clock —but it is doubtful that Domino’s would have a 34 percent market share today if it had not led with such a strategy.

· Benefit-Driven Pricing.

Satisfaction-based pricing also can be based on how a service is used and how it creates value. Benefit-driven pricing involves explicitly pricing the aspect of the service that directly benefits customers. The result is that customers usually feel more satisfied and less uncertain than if a service’s price is unrelated to the benefits it delivers. While identifying what customers value in a service is crucially important for developing an effective benefit-driven pricing strategy, determining what customers do not value is equally important.

One big complication arises from the possibility that valuations can vary significantly across customer segments. Once such information has been gathered systematically, however, it can serve as a secure foundation for implementing benefit-driven pricing. Generally, the pricing must establish and communicate a clear association between the price and the service attributes that customers value.

Consider, for instance, computerized on-line information services, which are notorious for their complicated pricing schemes. Often, customers using these services are charged for log-on time, but it is the information browsed and retrieved that customers really value. In such a situation, value creation and pricing are out of sync. When ESA-IRS, a major European player in the on-line information business, implemented its new pricing structure called “pricing for information,” it noticed several significant changes in customers’ searching behavior. With the old pricing structure, which was based on time connected, customers rarely used a powerful (but time-intensive) feature called ZOOM. This feature lets users search several complex databases simultaneously with increased precision. With the new pricing structure based on information extracted or viewed, ZOOM’s use tripled. People generally stayed on-line longer and conducted more extensive searches, with the result that their experiences were more relaxed and satisfying. This pricing change represented a fundamental shift in the company’s marketing approach — from then on, it focused its marketing efforts on selling information (the benefit), rather than on time.

· Flat-Rate Pricing.

An important source of uncertainty for some customers is the actual costs that they will incur. For many labor-intensive services, the exact price cannot be established before delivery. The cost of legal representation, for example, often is influenced by events that cannot be known fully in advance. Flat-rate pricing alleviates customers’ uncertainty by agreeing on a price beforehand. In effect, the service provider assumes the risk of any cost overruns. Flat-rate pricing can be an effective strategy for companies in industries in which service prices are unpredictable and costs are badly managed, or in which competitors make low estimates to win business but have no intention of honoring them.

Flat-rate pricing needs at least three conditions to make sense. First, the flat-rate price must be competitive. If customers perceive it as too high, it will dilute the risk-reduction benefits that make the strategy appealing. Second, the company must develop and maintain a highly efficient, streamlined cost structure to provide some cushion for unanticipated costs. Costs in the service system that do not add value to customers must be eliminated. Third, the potential for relationship marketing must be high; that is, even if unexpected costs drain the profit from one service episode with a customer, additional opportunities to serve the customer — and make money — still loom on the horizon.

The New York law firm of LeBoeuf, Greene, Leiby, and MacRae won Alcoa’s legal business in 1993 by agreeing to an unusual three-year, flat-rate pricing arrangement. LeBoeuf would handle all of Alcoa’s litigation — more than 500 cases — for an annual fee of approximately $7 million. The fee was aggressive, representing almost a 25 percent saving for Alcoa. But despite the steep price reduction, the law firm expected to increase its profits from Alcoa’s account through the additional volume of business and efficiency gains. Opening a new office in Pittsburgh dedicated to Alcoa’s litigation needs, which the increased caseload justified, was a key factor that improved efficiency. The flat-rate pricing deal further cemented LeBoeuf’s long relationship with Alcoa.19

In summary, satisfaction-based pricing strategies can effectively reduce customers’ uncertainty in purchasing services. Service guarantees compensate customers if they are not satisfied. Benefit-driven pricing aligns the pricing specifically with the benefits that the customer perceives. Flat-rate pricing negates any dissatisfaction that might result from higher than anticipated prices. These strategies apply only under certain conditions, however, and they are definitely not for timid competitors. Each strategy is risky in its own way, and each requires strong commitments: to service excellence for the service guarantor, to understanding how the service creates value for the benefit pricer, and to a highly efficient cost structure for the flat-rate pricer.

Relationship Pricing

Relationship marketing, which involves “attracting, maintaining, and — in multiservice organizations — enhancing customer relationships”20 is increasingly viewed as a desirable marketing strategy because of its profit potential and its appeal to customers. Service companies clearly gain if they can do more business with existing customers for a longer period of time. Equally important, customers gain if they can establish a relationship with a competent, dependable provider of a high-risk service that presents a complex decision with regard to purchase and is difficult to evaluate. A customer fortunate enough to have an excellent auto repair person, physician, or real estate agent has a lower effort and risk burden than someone who needs the service but hasn’t yet developed a satisfactory relationship.

The question is, what role should pricing play in relationship marketing? An obvious approach is to use price reductions to initiate relationships. That approach is easy to implement and has considerable intuitive appeal, but it is also the most easily imitated — which is why relationships based solely on price incentives disappear so swiftly.21

Services marketers can develop creative pricing strategies that contribute to sustainable relationships. Such strategies offer an incentive for customers to consolidate more of their purchasing with the company and to resist the entreaties of competitors. Marketers first need to understand their customers’ needs and their motivations for developing a long-term relationship with the company. They should also analyze potential competitors’ moves and implications for profitability.

· Long-Term Contracts.

Marketers can use long-term contracts that offer customers price and nonprice incentives to enter into multiyear relationships, either to strengthen existing relationships or to develop new ones. Such contracts can alter fundamentally a service provider’s relationships with its customers. They can transform business transactions from relatively isolated events to a series of steady, sustained interactions. Each transaction provides one more snapshot of customers’ needs and therefore facilitates learning and efficiency gains for the company — which also may result in greater savings for customers as the relationship evolves. The steady revenue stream from long-term relationships enables the service provider to concentrate more resources on widening the value gap between what it offers and what competitors offer.

After years of fighting short-term discounting battles in the shipping business, United Parcel Service is now aggressively pursuing the strategic advantages of long-term contracts. Having shipped a majority of Lands’ End orders for almost thirty years, UPS signed an ambitious three-year contract in 1994 to become the catalog retailer’s primary carrier. To win the multiyear contract, UPS offered enhanced efficiency, which enabled Lands’ End to reduce its average shipment time by 50 percent, without charging its customers extra for expedited delivery. Such efficiency gains became possible because the multiyear commitment enabled UPS to integrate its operations more seamlessly with those of Lands’ End. A more efficient delivery system allowed Lands’ End to operate with lower inventory levels, thus reducing its risk of surplus and obsolete inventory.

A similar win-win proposition prompted UPS and Ford Motor Company to enter into a multiyear contract that involved the automaker’s package shipments to its 5,700 U.S. dealers. The arrangement made Ford UPS’s largest customer in terms of receiving locations. Ford’s motivation for the multiyear contract was to control shipping costs and to consolidate electronic billing. Further underscoring the growing strategic significance of long-term contracts in the delivery industry, UPS signed its biggest ever multiyear contract in 1995: a five-year deal with J.C. Penney Company valued at $1 billion.

· Price Bundling.

This strategy, which also aims to enhance and sustain customer relationships, involves selling two or more services bundled together.22 Price incentives assure buyers that purchasing the services together is less expensive than buying them separately. Service providers can benefit in three ways from price bundling. First, bundling can reduce costs. The cost structure of most service companies is such that providing an additional service costs less than providing the second service alone. In a bank, for instance, shared account-opening and computer-processing costs result in economies when the bank can sell a certificate of deposit and a savings account along with a checking account. If the bank passes some or all of the economies to customers in the form of reduced fees or higher interest, it is giving them an incentive to buy the bundled services.

A second benefit of bundling that appeals to customers is purchasing related services from one service provider. They can save time and money by interacting with and paying one provider rather than multiple providers.

Third, bundling effectively increases the number of connections a service company has with its customers. The greater the number of these linkages, the greater the access to customer information and the potential for learning about customers’ needs and preferences. When a customer purchases home insurance from the same company providing auto insurance, the amount of information available to the company increases significantly. That kind of data, if used productively, can help the company develop and sustain long-term relationships with its customers.

AT&T did just that when, in 1990, it shocked the credit card industry by successfully introducing its Universal card, a discount calling card that also functioned as a credit card. Consumers enthusiastically received the Universal card, with its attractive pricing incentives such as no fee for life and below-average interest rates. Almost overnight, AT&T became the second largest issuer of credit cards in the United States. Several factors made this growth possible. First, AT&T used its database of long distance customers to select creditworthy prospects for its promotional mailings. That selectivity decreased substantially the company’s risk exposure because it was mailing to millions of prospects. The second reason for AT&T’s success was the creative bundling of two services that are notorious for customer switching: credit cards and long distance telephone communications. By combining the two in a service package that offered attractive features, AT&T effectively combated customer defections in both.

Relationship pricing aims to encourage the development of profitable, long-term customer relationships. It can be applied under many varied conditions. A careful analysis of mutual benefits is essential to determine the factors that make the relationship work. Such an analysis will suggest how much emphasis the service company should place on price incentives. Consolidating purchases of services with a single supplier must have the potential of offering customers increased benefits, reduced monetary and nonmonetary costs, or, ideally, all of the above. The service should be one that customers use on a recurring or continuous basis, with movement by customers among multiple suppliers a common phenomenon, and there should be potential for expanding relationships with customers through increased use of one service or the purchase of multiple services.

Efficiency Pricing

Understanding, managing, and reducing costs are the cornerstones of efficiency pricing. Some or all of the resulting cost savings are passed on to customers in the form of lower prices. To be effective, the leaner cost structure must be difficult for competitors to imitate in the short run. Furthermore, cost savings passed on to customers must genuinely enhance their value perceptions. Cost trimming that results in a less expensive but unsatisfactory service will not be successful.

Understanding costs is particularly difficult for service companies. Traditional cost-accounting procedures were designed to monitor costs associated with the consumption of raw materials, depreciation, and labor. In the case of services, for which the final product is a composite of performances, traditional accounting practices are inadequate.

Activity-based costing (ABC), which focuses on resources consumed by specific activities that lead to the final product, may be a more useful tool. Take, for example, a pizza delivery operation. ABC would estimate the cost of each activity in the service chain, from taking the order to delivering the pizza. Once the cost elements were identified, cost-reduction efforts could be focused on streamlining or eliminating activities that don’t add enough value for customers.23

Southwest Airlines’s relentless cost-reduction efforts are based on a keen understanding of the cost-value relationships of specific activities that make up air travel services. While other airlines focused on establishing expensive hub-and-spoke networks in the 1980s, Southwest became the industry’s most productive airline, in part by flying shorter, more direct routes and by using less congested, less expensive airports whenever possible — Houston’s Hobby Airport to Dallas’s Love Field, instead of Houston’s Intercontinental Airport to the Dallas-Fort Worth Airport, for example. Southwest keeps its training and maintenance costs low because the shorter routes enable it to use only one type of aircraft (Boeing 737s). Aircraft turnaround time averages twenty minutes, which means that Southwest planes spend more time in the air — the only way an airline generates revenue. No assigned seats and no meal service speed aircraft turnaround and reduce operating costs, and Southwest enjoys further savings by not subscribing to the industry’s automated reservation systems.

In January 1995, Southwest became the first airline to offer ticketless travel on all flights. Passengers calling the airline for reservations receive a confirmation number instead of a ticket. They can get their receipts mailed or faxed to them, or they can pick them up at the gate. By early 1996, 30 percent of Southwest’s passengers were flying ticketless, a savings of $25 million a year for the airline. With an average seat per mile cost 2 to 4 cents below other major airlines, a reputation as the industry price leader, a far simpler price structure than most other airlines, excellent on-time performance, and an unsurpassed safety record, Southwest is the United States’s most consistently profitable airline. By 1995, Southwest was flying 45 million passengers a year, twice as many as in 1990. It is first or second in boardings in the vast majority of airports that it serves and has affected dramatically the competitive dynamics in every market it has entered.

By designing a service system that aligns the cost of an activity with its value to targeted customers, along with eliminating some activities entirely, Southwest has, in effect, redefined the airline industry’s cost structure. It is the price leader because it is the efficiency leader, making it very difficult for competitors to catch up. United made a determined effort to challenge Southwest in California with its low-fare Shuttle by United service, but it has been forced to retreat from numerous routes. Continental tried to imitate Southwest with Continental Lite and failed. American tries to avoid head-to-head competition with Southwest whenever possible. A flock of new low-fare airlines has begun flying in the past few years, but it is questionable how many can survive.24

Efficiency pricers almost always are industry heretics, shunning traditional operating practices in search of sustainable cost advantages. No better example exists than the discount securities brokerage firm of Charles Schwab. Eschewing the conventional route of dispensing investment advice through a commission sales force, Schwab concentrated on developing a highly automated, low-cost system that could efficiently handle millions of transaction requests made by individual customers. Over time, this high-tech, low-cost structure has enabled Schwab to market a portfolio of financial services with attractive pricing incentives, including in 1989, Telebroker, which allows customers to make stock trades using a push-button phone; in 1992, OneSource, which offers no-load investment in more than 250 mutual funds; in 1992, no-annual-fee individual retirement accounts; in 1994, a no-fee dividend reinvestment plan for more than 4,000 stocks; and in 1995, e.Schwab, an aggressively priced, state-of-the-art computerized trading service for individual investors.

Like Southwest in air travel, Charles Schwab has redefined the cost structure in financial services. For example, Schwab requires mutual funds that participate in its OneSource program to pay the fees that customers traditionally pay. With a combination of marketing muscle, innovation, and pricing ingenuity, Schwab has leapfrogged traditional industry leaders. Millions of dollars flow out of commercial banks into Schwab accounts every day. In the four-year period ending in 1994, customer assets in Schwab’s accounts increased from $31 billion to more than $100 billion. In the same period, profits soared from $17 million to $130 million.

To summarize, efficiency pricers reduce customers’ monetary burden through efficient operating practices. They focus on delivering in the best and most cost-effective way the customers’ most valued aspects of the service. They either streamline or eliminate low-priority elements of the service chain. Gradually, the focus on efficiency through innovation becomes embedded in the company’s culture, a factor that makes catching up even more difficult for competitors.

Conclusion

In buying a performance, services customers buy a promise. They cannot see the intangible product that they are buying and agree to pay for it before experiencing it. They can try on a dress or test-drive an automobile, but they cannot try on a hotel or test-drive a lawyer. Instead, they sign on for the service and expect it to be delivered competently and fairly. The difficulty that customers have in evaluating services before (and sometimes after) purchasing them, coupled with the reality that buying services involves incurring expenses rather than acquiring tangible goods, makes a strong case for marketing practices that simplify the buying decision and reassure the customer. Successful services marketers pursue these goals in their pricing. Unfortunately, many still use pricing approaches that have the opposite effects.

Services pricing practices that do not capture and communicate value open a window of opportunity for a Southwest Airlines, a Charles Schwab, an AT&T Universal card, or a Bank One Texas Trust division. Value is the dominant purchase motivation among consumers and institutional customers today. Pricing practices that are designed to create an illusion of value that doesn’t really exist, that purposely obfuscate, that are riddled with restrictions, exceptions, and options, or that require considerable fine print in advertisements serve neither the customer nor the company. They are burdensome for customers and are doomed to failure in this value-dominated era when tomorrow morning’s competitor may emerge from outside the industry with a fresh pricing approach — just as AT&T invaded the credit card industry and Charles Schwab, the securities brokerage industry.

Successful marketers in the service sector will increasingly use satisfaction-based, relationship, and efficiency pricing to expose and exploit the vulnerabilities of competitors’ pricing practices. Some innovative competitors will combine aspects of all three strategies. Executives can assess their companies’ pricing vulnerability by answering the following questions:

- Are our prices easy to understand?

- Do they represent genuine value to our customers?

- Does our pricing encourage customers to do more business with us and be loyal to us?

- Does our pricing reinforce customers’ trust in our company?

- Does our pricing ease customers’ uncertainty about the purchase decision?

A negative response to even one of these questions warrants a careful reassessment of the company’s pricing and a broader marketing strategy. Enlightened services marketers may differ from one another on the specific pricing strategies that they implement, but all agree on the goal: capturing and communicating value.

References

1. For a discussion of these and related issues, see:

Electronic Media, 21 March 1994, p. 1;

New York Times, 11 November 1993, p. A1; and

Wall Street Journal, 19 November 1993, p. B9; 2 February 1966, p. B1.

2. USA Today, 9 October 1995, Money section.

3. A. Parasuraman, L.L. Berry, and V. Zeithaml, “Understanding Customer Expectations of Service,” Sloan Management Review, volume 33, Spring 1991, pp. 39–48.

4. Business Week, 17 August 1992, p. 108.

5. Business Week, 6 September 1993, p. 62.

6. V.A. Zeithaml, A. Parasuraman, and L.L. Berry, “Problems and Strategies in Services Marketing,” Journal of Marketing, volume 49, Spring 1985, pp. 33–46.

7. For a general discussion of the issues involved in pricing services, see:

K.B. Monroe, “The Pricing of Services,” in The Handbook of Services Marketing, eds. C. Congram and M. Friedman (New York: Amacom, 1990); and

M.R. Schlissel and J. Chasin, “Pricing of Services: An Interdisciplinary Review,” The Service Industries Review, volume 11, July 1991, pp. 271–286.

8. T. Levitt, “Marketing Intangible Products and Product Intangibles,” Harvard Business Review, volume 59, May–June 1981, pp. 94–102;

R. Thaler, “Towards a Positive Theory of Consumer Choice,” Journal of Economic Behavior and Organization, volume 1, March 1980, pp. 39–60;

R. Thaler, “Mental Accounting and Consumer Choice,” Marketing Science, volume 4, Summer 1985, pp. 199–214; and

B.E. Kahn and R.J. Meyer, “Consumer Multiattribute Judgments under Attribute-Weight Uncertainty,” Journal of Consumer Research, volume 17, March 1991, pp. 508–522.

9. For an excellent discussion of search and experience goods, see:

P. Nelson, “Information and Consumer Behavior,” Journal of Political Economy, volume 78, March–April 1970, pp. 311–329.

Issues related to credence goods are discussed in:

R. Darby and E. Karni, “Free Competition and the Optimal Amount of Fraud,” Journal of Political Economy, volume 81, April 1973, pp. 67–86.

10. V.A. Zeithaml, “How Consumer Evaluation Processes Differ between Goods and Services,” in Marketing of Services, eds. J.H. Donnelly and W.R. George (Chicago: American Marketing Association, 1981), pp. 186–190.

11. R. Recchi, “It’s the Math, Stupid,” Knight-Ridder News Service, 25 September 1993.

12. Business Week, 6 September 1993, p. 63.

13. M.J. Bitner, “Servicescapes: The Impact of Physical Surroundings on Customers and Employees,” Journal of Marketing, volume 56, April 1992, pp. 57–71.

14. For a discussion of the importance and profit implications of pricing decisions, see:

G.E. Smith and T.T. Nagle, “Financial Analysis for Profit-Driven Pricing,” Sloan Management Review, volume 35, Spring 1994, pp. 71–84;

H. Simon, “Pricing Opportunities — And How to Exploit Them,” Sloan Management Review, volume 33, Winter 1992, pp. 55–65; and

M.V. Marn and R.L. Rosiello, “Managing Price, Gaining Profit,” Harvard Business Review, volume 70, September–October 1992, pp. 84–94.

For a comprehensive examination of pricing decisions, see:

T.T. Nagle and R.K. Holden, The Strategy and Tactics of Pricing(Englewood Cliffs, New Jersey: Prentice Hall, 1995);

K.B. Monroe, Pricing: Making Profitable Decisions (New York: McGraw-Hill, 1990); and

H. Simon, Price Management (New York: Elsevier Science Publishers, 1989).

For an integrative review of research on value and its relationship with price and quality, see:

V.A. Zeithaml, “Consumer Perceptions of Price, Quality, and Value: A Means-End Model and Synthesis of Evidence,” Journal of Marketing, volume 52, July 1988, pp. 2–22.

15. “Reach out and Confuse Someone,” Services Marketing Today, June 1995, p. 4.

16. T.T. Nagle, “Pricing as Creative Marketing,” Business Horizons, volume 26, July–August 1983, pp. 14–19.

17. D.H. Maister, “The New Value Billing,” The American Lawyer, volume 16, May 1994, p. 40.

18. L.L. Berry, On Great Service: A Framework for Action (New York: Free Press, 1995).

19. For more details, see:

J.E. Morris, “Two Pioneers Make Their Fixed-Fee Deal Work,” The American Lawyer, volume 15, December 1993, p. 5.

20. L.L. Berry, “Relationship Marketing,” in Emerging Perspectives on Services Marketing, eds. L.L. Berry, G.L. Shostack, and G. Upah (Chicago: American Marketing Association, 1983), p. 25.

21. F.F. Reichheld, “Loyalty-Based Management,” Harvard Business Review, volume 71, March–April 1993, pp. 64–73.

22. J. Guiltinan, “The Price Bundling of Services: A Normative Framework,” Journal of Marketing, volume 51, April 1987, pp. 74–85.

For buyers’ responses to price incentives in bundle offers, see:

M.S. Yadav and K.B. Monroe, “How Buyers Perceive Savings in a Bundle Price: An Examination of a Bundle’s Transaction Value,” Journal of Marketing Research, volume 30, August 1993, pp. 350–358.

23. For additional details about the ABC approach, see:

R. Cooper and R.S. Kaplan, “Measure Costs Right: Make the Right Decisions,” Harvard Business Review, volume 66, September–October 1988, pp. 96–103.

24. Wall Street Journal, 2 November 1995, p. A4.

Comments (2)

Sean M. Brown

Orlando E. Contreras