How Hadco Became a Problem-Solving Supplier

Topics

Every action has an equal and opposite reaction. We can apply this Newtonian principle to the vertical supply chain: for every part outsourced by an original equipment manufacturer (OEM), there is an equal and opposite opportunity for a parts supplier to furnish that part. While many parts or products have been outsourced to non-U.S. suppliers during the past twenty years in an intensely competitive environment, some U.S. parts suppliers have successfully expanded their share of the business by developing more effective methods to compete against the low labor-cost advantage many offshore suppliers enjoy.

Although no two success stories are exactly alike, there are some general patterns emerging in global competitive markets. We chronicle one company’s efforts to develop successfully a new set of core competencies that give OEM customers what they want, when they want it. The transformation of a manufacturing company from underachiever to a thriving world-class competitor illustrates the more general results we obtained in surveys of small and medium-size manufacturers (SMMs).1 We use a case study of one company, Hadco Corporation, to illustrate specific practices.

First, we discuss the strategic supplier typology we developed using survey data. In the following section, we introduce Hadco and discuss the business and competitive reasons for Hadco’s choice to compete in the printed circuit board (PCB) industry during the 1980s. Next we detail how Hadco changed to take advantage of opportunities in strategic outsourcing. Finally, we synthesize the coarse detail of the survey data with the fine detail of the case data to build a more complete picture of the role of SMMs in the U.S. economy. The lessons we learned from the typology and the Hadco case give clear prescriptions to companies that compete in global markets.

Classifying SMMs

We began our study of SMMs by dividing suppliers into two types: problem solvers and commodity suppliers. We define problem solvers as suppliers that compete primarily on their ability to solve process and product problems for their OEM customers. These suppliers compete in dense vertical and horizontal learning networks, which enhance their ability to absorb and transfer knowledge.2 In contrast to spot-market or commodity suppliers, problem solvers share these characteristics:

- They earn many different certifications from their customers, which usually involve documentation of quality processes and practices (including delivery and service), long-term contracts, and target pricing.

- They engage in early design work with customers, requiring close communications.

- They use advanced management practices, which include strategic planning, quality practices, and employee empowerment programs.

- They develop their own supplier certification programs.

- They have mastered basic manufacturing procedures and take advantage of advanced manufacturing processes and technologies.

- They sell to many customers in various industrial markets.

In general, these six characteristics divide along three dimensions: (1) administrative mechanisms that facilitate collaborative relationships; (2) advanced manufacturing practices and technologies; and (3) a broad market mission in which the firm sells to many customers in many industries. The three dimensions suggest a set of generic strategies. Management scholars have used these dimensions to develop typologies to test Porter’s generic business strategies: low cost, differentiation, and focus.3

We used survey data obtained in questionnaires to 200 manufacturing companies in New Hampshire to develop the dimensions for our strategic supplier typology.4 We chose these companies because New Hampshire’s manufacturing sector outperformed all other states in their efficient use of capital and labor as measured by gross state product over the past twenty-five years. To ensure that we looked at best practices, we selected our sample from only those New Hampshire industries that outperformed the national averages in productivity, wages, and exports between 1967 and 1987.5 More recent data indicate that they continue to outperform other industries in the state. The survey included firms from four industries: fabricated metals, industrial machinery (including computers), electrical and electronic equipment, and scientific instruments.

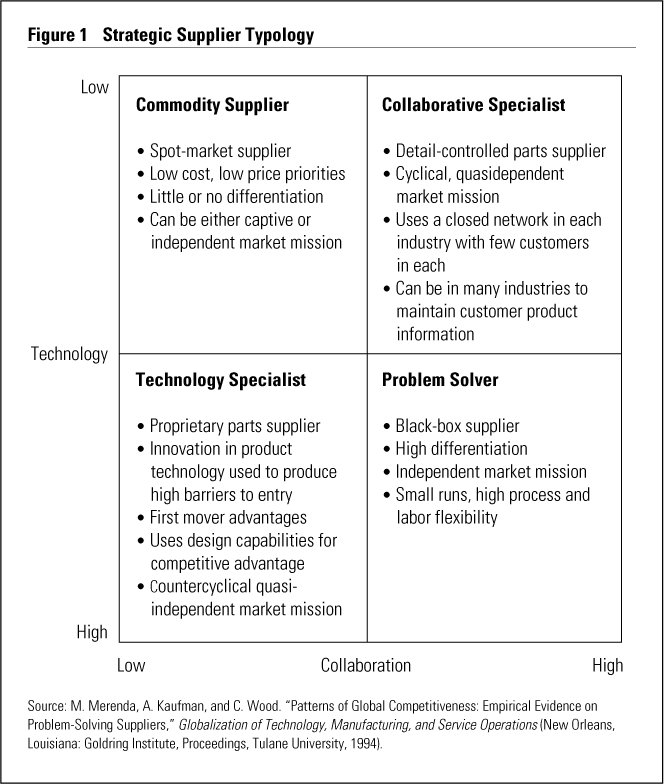

We used correlation and factor analysis to test whether the survey responses clustered together to fit our hypotheses.6 By analyzing the data, we confirmed the three dimensions described above and expanded the typology to include four generic supplier strategies: commodity supplier, technology specialist, collaborative specialist, and problem solver (see Figure 1).7 A commodity supplier operates as a traditional spot-market manufacturer, which makes goods according to OEM specifications and competes primarily on price. Like commodity suppliers, collaborative specialists produce according to OEM specifications but attempt to differentiate products by developing close customer relationships. The technology specialist also pursues a differentiation strategy but does not work closely with customers. Instead, technology specialists manufacture unique components that customers want. Problem solvers seek to develop strong technical and collaborative skills so that they can resolve customers’ design and production problems.

{kind=link}

Problem solvers are similar to the elite companies in the first tier of a Japanese keiretsu, except that they are not partly owned by their major customers, do not have interlocking directorships, and have not yet developed long-term relationships with their customers.8 The collaborative specialist resembles the first- or second-tier supplier of well-defined major components and subassemblies, the technology specialist resembles the first- or second-tier supplier of more design-intensive or customized parts, and the commodity supplier resembles the third- or fourth-tier material or off-the-shelf supplier.9

Our classification shows the changing nature of supplier relationships with their customers. Now we turn to a case history of one of the nation’s leading independent PCB manufacturers, Hadco Corporation, which illustrates those changes.

The Evolution of Hadco

Hadco, one of the companies in our New Hampshire industry group, makes PCBs, an essential component in manufacturing computers and electronic equipment in diverse industries such as automobiles, consumer electronics, telecommunications, and defense. PCBs are nonconductive panels with bonded metallic patterns that interconnect electronic components both mechanically and electronically. The components are composed of various semiconductor devices, such as transistors, rectifiers, diodes, capacitors, and resistors, that affect the electrical current flow. Two or more of these devices on a base material, such as silicon, become an integrated circuit, which forms electronic systems that are the basic building blocks for electronic equipment.

The PCB industry has been forced to adapt to the technological innovations that reshaped product competition in the computer industry. Firms that compete in manufacturing electronic components achieve competitive advantage by improving the electrical circuit designs etched into the PCBs. Japanese lean manufacturing in the auto, consumer electronics, and other industries poses additional competitive challenges.

PCBs are an important example of innovation research. Von Hippel argues that firms innovate to secure higher profits; firms (e.g., users, manufacturers, suppliers) that functionally gain from these innovations tend to initiate the innovation. In studying the PCB industry before 1988, von Hippel found that approximately 70 percent of the innovations occurred among users (e.g., IBM, Wang) that made their own circuit boards and usually engaged suppliers to alleviate supplier bottlenecks associated with the business cycle.10 Thus von Hippel’s study provides an excellent reference point for our effort, since we would expect Hadco to develop greater in-house capabilities as the large OEMs outsourced.

PCB manufacturing shows a growing trend toward outsourcing. Hadco is an excellent example of how SMMs can profitably take advantage of OEM strategic outsourcing: by reorienting itself from a spot-market manufacturer, habitually serving its OEM customers, it evolved to a problem-solving supplier, cooperating with OEMs in innovatively solving product and process problems.

New England-based computer companies like DEC, Wang, and Data General were instrumental in pulling Hadco along the growth curve during the expansionary years between 1966 and 1985. Once harnessed to this new dynamo, Hadco had few important strategic decisions to make. In 1984, however, when the computer industry’s phenomenal growth abruptly ended, Hadco’s management faced a difficult strategic decision: to continue its high-volume, low-cost commodity strategy or to adopt product differentiation as a new strategy.

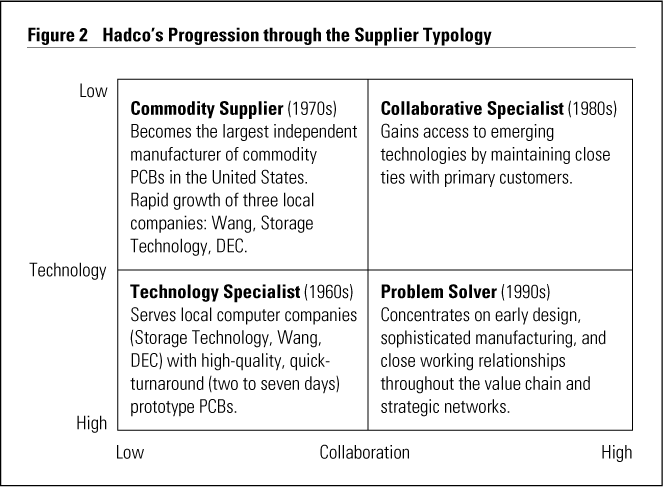

Industry developments forced Hadco management to adopt a differentiation strategy. In vigorously pursuing this strategy, Hadco managers unexpectedly found that OEMs wanted to enter “partnerships” with specialized suppliers to both manufacture and design parts that the OEMs had previously done in-house. Hadco managers quickly recognized the profound implications of such alliances. Hadco could no longer consider itself a spot manufacturer — even a high-end producer — that made PCBs to OEM specification. Instead, it had to redefine itself as a problem solver, helping its OEM customers improve the performance of their electronic components. In 1985, Hadco managers put together a strategic plan to develop the technological, human, and organizational resources to become a problem-solving supplier. Hadco made this transition by first pass]ing through the other three stages: technology specialist, commodity supplier, and collaborative specialist.

From Technology Specialist to Commodity Supplier

Three entrepreneurs founded Hadco in Cambridge, Massachusetts, in 1966. They adopted a strategy of producing high-quality, quick-turnaround prototype PCBs, i.e., the company began as a technology specialist (see Figure 2).11

{kind=link}

Horace Irvine, the company’s long-time chairman, initially set the company’s course. His experience as an account executive with Merrill Lynch and a production control and purchasing manager with a small PCB company gave him hands-on knowledge of the computer’s enormous commercial potential and its opportunities for PCB manufacturers. In its early years, Hadco operated as a technology specialist providing local computer firms with high-quality, quick-turnaround (two to seven days) prototype boards. An OEM customer would supply Hadco with the design for an experimental board. At that time, PCBs were usually rigid and single- or double-sided. Hadco would develop a prototype, assessing whether the PCB could be mass-produced. If the prototype was promising, then the OEM would manufacture it in-house.12

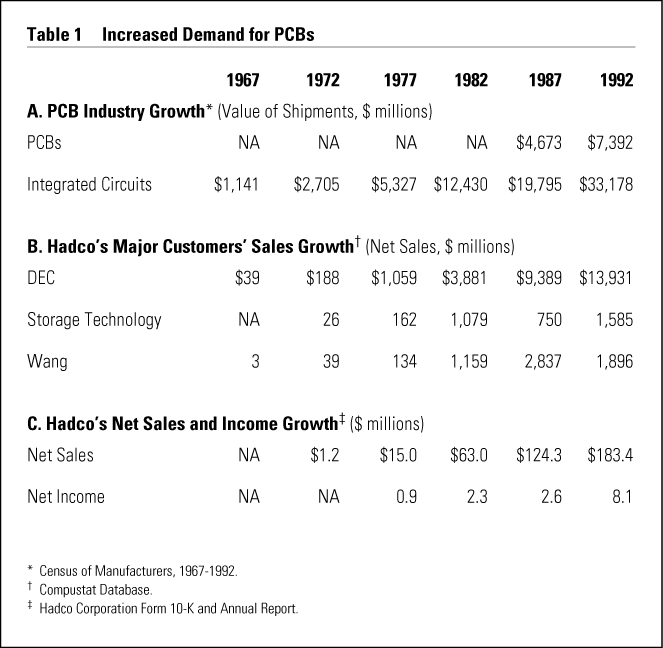

However, as the computer and electronic product markets burgeoned with the advent of the microprocessor, the demand for integrated circuits grew rapidly (see Table 1, part A). With this growth, computer and electronic product companies had to look for PCB suppliers outside. Outsourcing usually involved orders for standard PCBs that were relatively easy to manufacture. By 1984, the PCB industry had grown to more than 2,000 manufacturers, divided into two types: (1) captive manufacturers that operated within large computer or other electronic equipment firms, and (2) independent board suppliers. In 1979, captive producers accounted for 60 percent of production, but declined to only 40 percent by 1984.13

{kind=link}

Initially, large OEMs like IBM, Wang, and AT&T used independent producers to smooth out capacity needs over the business cycle. During an expansionary period when the large OEMs could not produce enough to meet internal demand, they contracted with independent manufacturers to produce predesigned, relatively simple PCBs. Then, when demand slackened, the large OEMs canceled contracts with independent manufacturers and relied solely on their own in-house capabilities. At the same time, in-house production allowed OEMs to reap higher profits from innovations in the design and manufacture of PCBs.

To maintain and improve profitability, OEMs could choose from three alternative strategies: by introducing new production technologies and/or materials, by modifying existing technologies and/or materials to produce new board designs, or by designing the innovation and then seeking small, independent PCB manufacturers that could mass-produce it. These new OEM demands gave independent suppliers the incentive to significantly increase capital investments and seek process innovations.14 Consequently, during the 1970s and early 1980s, independent producers could operate as technology specialists testing OEM design work or function as commodity suppliers mass-producing standard types of PCBs.

As demand for PCBs increased during the early 1970s, Irvine transformed Hadco from a technology specialist into the industry’s largest commodity supplier. Hadco’s small-volume prototype business decreased relative to its high-volume production of single- and double-sided boards.15 For the most part, this change occurred as three fast-growing local computer companies, Wang, Storage Technology, and DEC, increasingly relied on Hadco for a large percentage of their PCBs (see Table 1, part B).16 Irvine made sure that Hadco took advantage of these opportunities, and the company soon outgrew its operating facilities. The company expanded from three employees and $100,000 in sales in 1966 to more than 2,000 employees and approximately $126 million in sales in 1984. In 1983, Hadco built a new corporate headquarters in Salem, New Hampshire, near its 28,000-square-foot Derry, New Hampshire, manufacturing and engineering plant. Irvine stated that Hadco was to “become the dominant and most profitable supplier of high-volume, dense, two-sided, printed, and multilayer circuit boards.”

Experiments as a Collaborative Specialist

Hadco experienced growth in sales by becoming a commodity supplier and manufacturing a standardized, high-volume, low-value-added commodity. But, because of the industry’s cyclical nature and its low entry barriers, Hadco had to compete fiercely. The competitive environment kept earnings flat while sales exploded (see Table 1, part C). This pressure and the industry’s excess capacity in producing one- and two-sided boards forced Hadco’s managers to look for an alternative strategy. Even as Hadco was developing into a commodity supplier, management experimented again, differentiating its product to protect the company from the vagaries of the market.

During this period, Hadco protected its market position by reemphasizing its specialized prototyping and preproduction capabilities. Hadco managers sought to work closely with OEMs that used increasingly complex PCBs. By adopting a collaborative specialist strategy, Hadco managers hoped to gain access to emerging technological innovations in product development.

OEMs had by then crafted multilayer PCBs, which contained as few as four or as many as twenty layers.17 By layering boards through conductive or nonconductive holes, this new design process increased a printed circuit’s speed while decreasing its size.18 This improved efficiency permitted greater design density and product improvements in the computer industry. Because the new multilayering process required sophisticated engineering and production skills as well as heavy capital investments, Hadco managers believed that if Hadco collaborated in prototyping and preproduction of the process and its products, it could erect effective entry barriers.19 Hadco managers believed collaboration would allow Hadco to remain in touch with a technology that continued to shorten product life cycles. As part of this strategy, managers sought to diversify into other industries by transferring know-how to noncomputer firms that used PCBs and wanted close relationships with a technologically advanced supplier.

From 1985 to 1992, Hadco worked to become a collaborative specialist by investing in complex technologies and by instituting administrative methods to work closely with its customers. It expanded its manufacturing facilities for multilayer PCBs when it acquired a new factory in Owego, New York, and two PCB manufacturers, Circuit Image Industries and Qualitron Corporation. Qualitron’s advanced manufacturing equipment for arraying pins on PCBs positioned Hadco to sell its products to OEMs that were using a new technology, surface mount. This enabled them to create circuit boards with electronic components on the exterior, yielding denser designs than with the conventional multilayer techniques.

Hadco invested heavily in upgrading its marketing and technical capabilities. It enlarged and reorganized its sales and service organization to ensure customer communication. In this way, Hadco aimed at becoming market driven rather than engineering driven. Hadco complemented this move into customized products by developing a division to manufacture backplanes, specialized multilayer circuit boards that connect a series of logic boards. Thus Hadco gained an appreciation of the functional design relationships among the component parts that went into its customers’ final products.

To anticipate customer need, Hadco built two technology centers, one in Salem, New Hampshire, and another in Watsonville, California. The centers made prototypes of complex designs to customer specifications and modified them for mass production. The interaction between design and manufacturing helped Hadco improve the management of its production facilities. Finally, in 1983, to ensure laminated board supplies, Hadco integrated vertically by purchasing Lamination Technology, Inc.

Although Hadco vigorously acquired equipment and expertise to manufacture multilayered integrated circuit boards, it continued to concentrate its efforts on boards with fewer than eight layers that required conventional machinery to mass-produce. At the same time, Hadco continued to operate in the single- and double-sided PCB markets. By 1984, Hadco no longer operated as a pure commodity supplier, as the company had developed sophisticated marketing skills and employed more advanced technologies, primarily in the two technical centers, than it had five years earlier. Hadco now had the organizational capability to stay abreast of OEM technological innovations that increasingly shortened product life cycles, particularly in the computer industry.

Hadco had emerged as a collaborative specialist. The company manufactured goods according to customer specification and refrained from functional design work. The technology centers, where Hadco did its most advanced work, operated as specialists, verifying customer prototypes for mass production. By 1984, Hadco had taken significant steps toward becoming a collaborative specialist as a way to master the industry’s business cycles. It had evolved from a company in which a single customer represented 41 percent of sales in 1984 to one in which no single customer exceeded 10 percent of total sales in 1992.

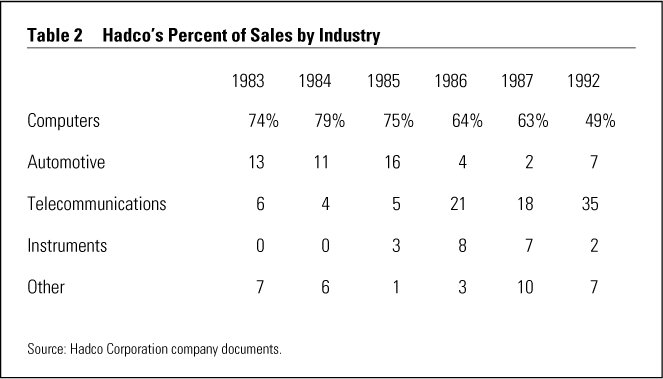

Hadco’s organizational structure still conformed to its basic commodity-supplier strategy. It functioned as a holding company in which profitability came principally from each profit center’s ability to gain scale economies. Irvine oversaw this mechanistic organization, which inhibited cross-functional collaboration both within Hadco and between Hadco and its customers. Hadco remained primarily a computer parts supplier, selling 79 percent of its products to the computer industry.20 Hadco was still a dependent supplier (see Table 2).

{kind=link}

Nonetheless, Hadco managers were confident in their ability to continually gain control over the business cycle. In 1984, when the company made an initial public offering, the financial markets confirmed their optimism, and Hadco netted $12.9 million on 1.3 million shares. However, this confidence was quickly shattered when one of Hadco’s largest customers, Storage Technology, which accounted for 18 percent of Hadco’s sales, filed for bankruptcy in October 1984. By itself, this would have badly damaged Hadco’s position, but Storage Technology’s difficulties also marked the end of the phenomenal growth of mainframes and minicomputers. Two of Hadco’s three primary customers experienced sharp declines in net income.

The computer market’s collapse dramatically affected Hadco’s performance: consolidated net sales went from a record high of $125 million in 1984 to $86 million, leaving Hadco with a loss on continuing operations of $4.7 million. Hadco’s greatest losses occurred in double-sided PCBs, for which three customers — DEC, Wang, and Storage Technology — had accounted for 49 percent of total sales in 1982.

Hadco Becomes a Problem Solver

The computer industry’s sharp decline forced Hadco management to once again find a way to handle downturns in the business cycle. However, the crisis proved so severe that Hadco’s board of directors had to act decisively and rethink its strategy of becoming a collaborative specialist. The board recognized that the firm’s competitive advantage came from its ability to work with customers in prototyping and manufacturing multilayered PCBs. This advantage, however, seemed insufficient to ward off the damaging effects of downturns in the business cycle. Consequently, the board, under Irvine’s leadership, decided to concentrate on high-end products that required design as well as manufacturing sophistication.

Hadco managers now had to think of themselves as problem solvers who collaborated with customers in finding functional design solutions to OEM product and process problems. In so doing, they recognized that they would have to continually improve their product and process technologies as well their administrative procedures. Hadco summarized its new strategy: “We must be more than a supplier. We must solve customers’ problems through creative, ‘hands on’ collaboration. Rapid response to customer needs is our obsession.”

Hadco managers faced difficult organizational challenges. Reorganization proceeded incrementally for the next five years. Jon Kropper, who joined Hadco as president and CEO in October 1985, did the initial restructuring. Until then, Irvine had led the firm as a traditional entrepreneur, seizing market opportunities and building formal structures that reinforced strong centralized decision making. Kropper, a former executive vice president with Wang, wanted to transform Hadco into a decentralized firm to give managers the financial and technical freedom to remake Hadco into a problem-solving supplier. To obtain the necessary financing for the transition, Kropper sold the company’s vertically integrated units and a number of investments designed to penetrate international markets. He divested Hadco’s wholly owned subsidiary, Lamination Technology, sold off its 49 percent interest in SA Comelin, and closed Qualitron.21 Due to these and other cost-saving measures, Hadco’s employment fell from 2,126 to 1,215. The resulting cash infusion helped maintain Hadco’s solvency, so Kropper could proceed with his reorganization plans.

Strategic Outsourcing in the Computer Industry

As Kropper began to refashion Hadco into a problem-solving supplier, the company’s large OEMs simultaneously went through a restructuring process that encouraged strategic outsourcing. Hadco discovered that its own downswing portended revolutionary changes in the mainframe and minicomputer markets.

For example, Wang built its phenomenal success on developing dedicated products for small end users, first in calculators, then in word processing and minicomputers.22 The company’s founder, An Wang, insisted that these products be proprietary, that they work exclusively with other Wang products. A Wang word processor, for example, operated only with Wang software and a Wang printer. By locking in customers, Wang gained high profits from its proprietary system. However, this strategy made Wang vulnerable to general-purpose equipment that could perform multiple functions and operated with an open system that allowed customers to mix and match from the best products on the market.

In 1981, when IBM introduced its personal computer (PC), Wang’s market share quickly eroded.23 IBM’s PC won market share because it was a stand-alone computer with multiple functions. Apple had already demonstrated how advances in microprocessing made a general-purpose, decentralized computer possible. IBM’s revolutionary contribution resided in the PC’s open system. Rather than building the PC from in-house production units, IBM outsourced nearly all of the PC’s components. In part, IBM chose this strategy to reduce the time to market. By relying on suppliers that had manufactured high-quality, reliable components, IBM did not have to acquire the needed equipment and skills in-house.

IBM’s executives had a strategic reason for adopting an outsourcing policy. They believed that the PC could set the industry standard if its specifications were accessible. Third parties could produce an array of add-ons, from software to modems, that would spontaneously give users a wide variety of products; this demand would ensure PC market dominance.24

IBM’s open system strategy worked as expected and fundamentally shifted the way computer companies competed. No longer could firms hope to achieve dominance through proprietary systems in which all components were manufactured in-house or subcontracted to specification. Under the open system, computer companies had to learn how to achieve leadership in those component parts — particularly microprocessors and operating systems — that define a computer’s standards and protocol for processing data.

In this highly competitive environment, it no longer made sense for a company to produce each part of the computer system. Now, managers had to decide where their firms had unique skills to win and sustain a lead in the computer’s basic design. Managers of vertically integrated firms quickly began to outsource much of the work they had formerly done in-house in order to concentrate on the firm’s core competencies. Wang refused to consider an open architecture that would allow for this kind of interchangeability, a disastrous decision.

Because computer OEMs were strategically outsourcing and developing new governance rules through the use of long-term contracts and certification programs, Hadco sought to take on more responsibility for improving PCB design and process technologies. The OEMs found it strategically cost effective to let sophisticated suppliers both invest in the latest production technologies and devise ways to improve performance. So long as OEMs had governance mechanisms to coordinate suppliers, they needed only the design engineers to work with suppliers to meet functional design requirements. Process innovation thus moved down the value chain.

Strategic outsourcing did not remain confined to the computer industry. Other U.S. industries faced their own competitive problems that did not arise solely from technological advances. Japanese firms adopted lean manufacturing techniques that emphasized strategic outsourcing. In automobiles, consumer electronics, office products, and communications, companies were imitating Japanese manufacturers and learning to compete on both quality and price. All of these changes offered Hadco important opportunities if it could manage the transition to becoming a problem solver.

Hadco Reorganizes

After salvaging the company from near bankruptcy by downsizing in 1985, Kropper began to invest in new capital equipment to meet customer needs. By 1990, the company had spent $54.4 million or 8 percent of net sales on new capital equipment, compared to an industry average of 5.9 percent.25

Hadco purchased new equipment to solder at high volume in high-quality lots. It installed an advanced system at the Owego and Derry plants that allowed for finer line drawings in producing double- and triple-track circuits and for components to be surface-mounted on either side of the circuit board. Together, these brought about a 60 percent reduction in board size and a 90 percent savings in board weight. Along with these savings came higher board performance and reliability as well as greater opportunities for automation and cost savings. Hadco made additional gains by installing computer-aided inspection equipment to verify that products met design specifications and by purchasing advanced drilling machines.

Kropper recognized that these capital investments would be worthless unless Hadco satisfied its customers’ increasingly sophisticated needs. To understand their needs and communicate them to design and production teams, Kropper upgraded Hadco’s communications capabilities in 1985 by installing proprietary software to receive electronically printed circuit designs and drill tape data. As part of this program, Hadco made major investments in computer-aided engineering equipment that improved PCB manufacturing yields. Hadco also had installed computer-aided design and manufacturing equipment to ensure that the company could support customers in designing PCBs. Through these investments, Hadco shortened the time from prototyping to mass-manufacture of a new PCB.

Simultaneously, Kropper upgraded the company’s sales force. In 1985, manufacturing representatives accounted for 64 percent of Hadco’s sales; by 1990, this number dropped to 29 percent. The change occurred as Hadco added fifteen employees to its direct sales force, bringing the total to twenty-eight in 1990. At the same time, Hadco established seven regional sales offices with a technical specialist liaison between the customer and Hadco’s manufacturing executives.

As Hadco upgraded its sales operations, the company gradually became less dependent on customers in the computer industry. By 1992, Hadco had thirty-nine major OEM customer partnerships in industries that required sophisticated electronics, chiefly industrial automation, instruments, and communications. Total sales to computer companies fell from 79 percent in 1984 to 50 percent in 1991. In 1992, no single customer exceeded 10 percent of Hadco’s sales. With this diversified customer base, the company found that OEMs were demanding improved buyer-supplier relationships through certification programs. These formal documentation programs forced Hadco to continually upgrade its operating policies and procedures and to meet stringent quality and delivery requirements. To make sure that its technology centers functioned as early warning systems for customer needs, Hadco provided the centers with the latest process equipment.

The strategic investments in process technologies and customer service forced Kropper to restructure the firm. His first step was to decentralize decision-making authority from Irvine to the technical managers. From 1985 to 1987, Kropper created the position of vice president for technology development, replaced executives in finance and international production, and elevated human resources from a staff to corporate executive function. Pat Sweeney took over as vice president of international manufacturing, after leaving a similar position at Wang in 1986; he eventually become CEO in 1991.

Together, these strategic investments and structural reforms produced results that Hadco could boast about in its 1988 annual report. The company cited three examples of how Hadco had recreated itself as a problem solver, collaborating on early functional design work with its customers, and responding quickly to customer needs:

- Stromberg-Carlson, a large electronics firm, had given up producing circuit boards and elected to work with Hadco in manufacturing PCBs for the switches that Stromberg-Carlson sold to its telecommunications customers. This decision to outsource came as Stromberg-Carlson augmented the density of its PCBs to meet sophisticated telecommunications customers’ demands. Although multilayer PCBs were an important part of Stromberg-Carlson’s switches, its managers found that investments in the equipment needed to produce them did not add strategic value to the company. Consequently, Stromberg-Carlson worked with Hadco engineering and purchasing teams to adapt Stromberg-Carlson’s designs to Hadco’s process.

- Honeywell developed a collaborative relationship with Hadco after reassessing its make/buy decisions and reducing its supplier base. Hadco formed a close working relationship with Honeywell’s industrial programmable controls operation, so close that Honeywell viewed Hadco as an extension of its own operations. The two companies melded their engineering, quality control, and materials groups to ensure that Hadco delivered defect-free products on time.

- With Tandem Computers, Hadco improved its capacity to meet customer needs rapidly. Hadco did not “partner” with Tandem as a problem solver, but instead demonstrated its new prowess to act flexibly and quickly when Tandem ordered a large number of complex PCBs with a short lead time.

Successes such as these, however, were not enough to convince Hadco’s board that Kropper had fully restructured the company. Kropper had proven himself an adept turnaround manager and able administrator who had moved Hadco from an entrepreneurially to a managerially run company on the path to becoming a problem solver. Hadco’s organizational structure, however, made it difficult to repeat this success story regularly. Kropper’s reforms remained mired in an outdated paradigm in which technology and administrative innovations like JIT were used solely to enhance productivity. Hadco had not learned to use the company’s new technologies and managerial practices to educate employees in anticipating customer needs and staying ahead of technological and market changes.

Managers were still part of a top-down organization, with Kropper setting policy. Hadco remained a company divided along business segment and functional lines; the hierarchy inhibited managerial intrapreneurship, while divisions fostered rivalries that worked against cross-functional teams (design, engineering, marketing) vital to concurrent engineering. Rivalry hindered internal cooperation and establishment of cross-functional design teams to enable early involvement in customers’ new-product development efforts.26

The board recognized that Hadco had to have a more people-oriented, less autocratic manager at the helm and promoted Pat Sweeney to CEO in 1991. To transform Hadco into a problem solver, Sweeney initiated a cultural revolution that broke the firm’s traditional hierarchy and fostered development of a learning environment.27 Sweeney advocated a two-pronged approach: develop a common vision and educate managers and employees in total quality management (TQM). Through a vision statement, Sweeney hoped to identify needed cultural changes to build collaboration within the firm. By introducing TQM, Sweeney expected to upgrade Hadco employees’ skills. By integrating employees’ commitment to Hadco’s future with their commitment to continuous learning, Sweeney hoped to create an environment that would foster their involvement in making Hadco a world-class PCB supplier.

In 1991, Sweeney hired a consultant to work with top management to develop and implement a vision statement (see the sidebar).28 In developing the statement, Sweeney and top management agreed that Hadco’s goal was to be the best supplier in its industry segment. This goal required Hadco to solve customers’ functional design problems, benchmark products (both internally and externally), and deliver products on time. Hadco had to go beyond meeting customers’ current needs to recognize their latent needs, i.e., to deliver a service or product that customers did not currently demand but would value when offered.

To adapt Kropper’s infrastructure to Hadco’s vision statement, Sweeney initiated a TQM program throughout the company. Sweeney hoped that TQM would rapidly bring in more customer information and provide training on assembling and operating cross-functional work teams to solve customers’ problems and refashion Hadco’s process technology. Sweeney felt that TQM would force Hadco’s employees to learn how to continuously improve their practices. By setting incremental goals, Sweeney recognized that employees would collectively develop routines to enhance performance. He hoped that by working together on problems, employees would develop an appreciation for learning and make Hadco a problem-solving organization. In 1992, as part of the TQM implementation effort, Hadco instituted a certification program and supplier symposium for its material and equipment suppliers. Certification ensured quality parts, timely delivery, the possibility for additional technical input in solving customer design problems, and long-term reduced costs.29

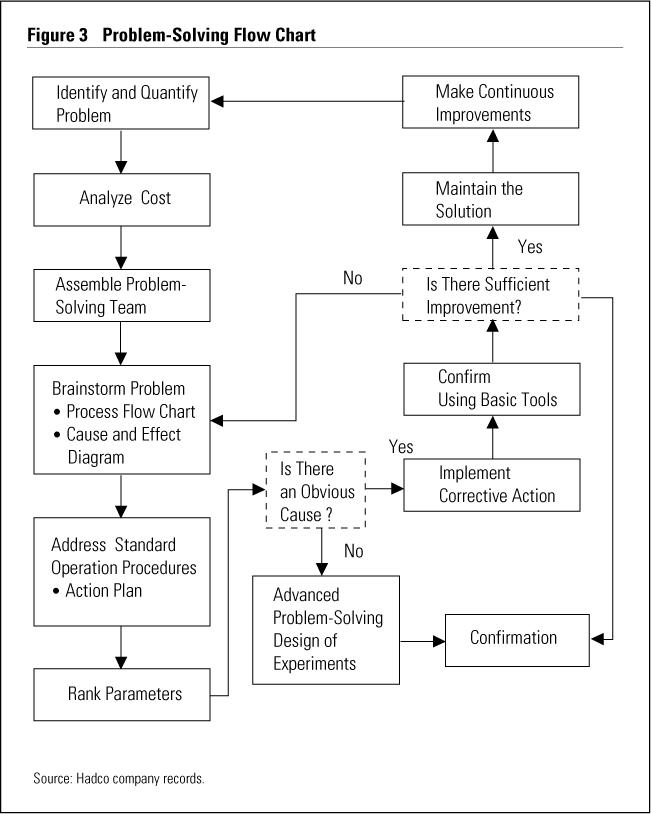

By 1992, Hadco had made sufficient strides toward becoming a learning organization, so Sweeney felt confident in beginning to make structural reforms. He imposed cross-functional teams focused on quality and operational processes onto the firm’s basic divisional structure. At the top of the new structure was a corporate steering committee of senior managers and a divisional/ functional vice president. The committee oversaw the TQM process that now has a formal steering committee in each divisional and functional unit. Continuous quality improvement teams report to the steering committees and join as multifunctional units to address specific customer problems (see Figure 3 for Hadco’s problem-solving procedure).

{kind=link}

Hadco also established a five-member corporate development project team “to improve the product and process development cycles with Hadco’s customers.” The team evaluates customer requests and technology changes before prototyping or manufacturing and works on corporate approved projects.

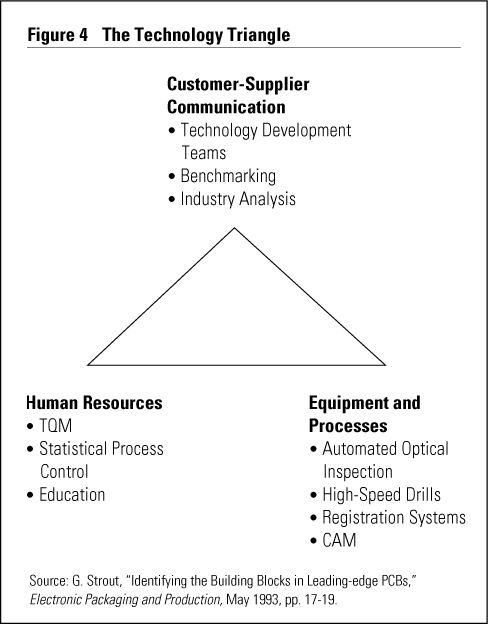

Overall, Sweeney established a “pipeline management” structure, which ensured that customer problems flowed into the company to reach the appropriate work/design teams and flowed back through the production process to deliver a product that met a customer’s needs.30 The structure reinforced Hadco’s capital investments in CAE and CAD/CAM, which had the potential to satisfy the needs of both existing and new customers. Taken together, Hadco’s commitment to invest in the latest technology, to establish customer-supplier partnerships, and to use advanced human resource practices formed a triangular policy by which Hadco defined itself as a problem solver (see Figure 4). To measure its success as a problem solver, Hadco benchmarked its performance internally and used OEM certification standards and the Baldrige Award criteria as external benchmarks.31

{kind=link}

Even though Sweeney focused the company on people and systems improvement in transforming Hadco into a problem solver, the company did not fully achieve its objectives. Management readily acknowledges that more employees, particularly production workers, need to be involved in the planning process and in cross-functional and quality improvement teams. Furthermore, management has not found ways to fully evaluate performance on a team or process basis while rewarding individual productivity.

A more important challenge for Hadco has been how to respond to OEM strategic outsourcing. Customers now expect Hadco to be simultaneously a leader in PCB technology and a responsive manufacturer of complex, high-volume PCBs. Such expectations require resources, particularly R&D expenditures and expertise, that surpass a medium-size firm’s capabilities. To operate at this level of sophistication, Hadco has had to leverage itself by partnering with other firms, including competitors, and public institutions on specific projects. Managing strategic alliances has become a new task for Hadco managers.

Conclusion

Our strategic supplier typology and the Hadco case suggest these lessons for SMM managers:

1. Learn from Hadco, don’t imitate it.

Hadco used the technology specialist and collaborative specialist stages to make a transition to the problem-solver stage. But by knowing its customers, a firm can design itself to be the type of supplier that best deals with those customers.

2. Corporate transformation is not a linear process.

Successful firms know where they stand along the typology dimensions and act accordingly. For instance, commodity suppliers do not invest in technology or organizational development unless they intend to transform themselves; collaborative specialists spend money to improve their organizational effectiveness, not to hire more technology expertise.

3. Successful SMMs provide distinctive competencies for OEMs.

Survival in a strategic outsourcing environment requires that suppliers have the internal capabilities to adapt and quickly respond to new customer demands. One way to do this is by developing strategic alliances with customers, suppliers, and even competitors. Problem solvers provide the highly specialized knowledge that can handle messy design-through-manufacturing problems as a single turnkey step. In contrast, commodity suppliers offer a standard product to supply a well-defined demand.

4. The old paradigm applies: structure follows strategy.

Structure must be adjusted to reflect the chosen strategy. New structures that emphasize organizational learning are necessary to respond effectively to the increased demands of OEMs.

5. Problem solving is cultural, not tactical.

Management strategy and leadership drives organizational transformation. Hadco learned this when its first two attempts to install a material requirements planning system failed. Two years into a TQM implementation, the system was successfully reintroduced as an organizational development project rather than an information system installation.

Hadco has had to master new organizational skills to transform itself into a problem-solving supplier. Over nearly three decades, it has demonstrated all four strategies suggested by the strategic supplier typology we developed from our survey data. Each strategy has unique administrative and organizational aspects. Hadco’s approach in the 1990s has been threefold: (1) to use operations management programs such as certification, concurrent engineering, TQM, and competitive benchmarking to improve product and process practices; (2) to use a vision statement with these programs to develop a learning organization; and (3) to closely coordinate its customer and supplier relationships to acquire advanced know-how. By pursuing this strategy, Hadco demonstrates how both incremental improvement and process innovation have moved the company along the value chain.

References

1. M. Merenda, A. Kaufman, and C. Wood, “Collaboration and Technology Linkages: A Strategic Typology” and “Empirical Evidence on Problem-Solving Suppliers” (Durham, New Hampshire: University of New Hampshire, Whittemore School of Business and Economics, New Hampshire Industry Group Working Papers, 1994).

2. N. Rosenberg, “Technological Change in the Machine Tool Industry, 1840–1910,” Journal of Economic History 23 (1963): 413–443;

S. Helper, “Strategy and Irreversibility in Supplier Relations: The Case of the U.S. Auto Industry,” Business History Review 65 (1991): 781–824; and

J.F. Quinn and F.G. Hilmer, “Strategic Outsourcing,” Sloan Management Review, Summer 1994, pp. 43–55.

3. M. Porter, Competitive Advantage: Creating and Sustaining Superior Performance (New York: Free Press, 1985).

4. Our survey utilized a questionnaire developed by the Northeast Manufacturing Technology Center. See:

National Institute of Standards and Technology/Northeast Manufacturing Technology Center and New York State Department of Economic Development, “Quick View: Manufacturing Intake Questionnaire” (Troy, New York: NEMTC/RPI, 1992).

5. A. Kaufman, R. Gittell, M. Merenda, W. Naumes, and C. Wood, “Porter’s Model for Geographical Competitive Advantage: The Case of New Hampshire,” Economic Development Quarterly 8 (1994): 43–66.

6. Merenda et al. (1994).

7. K.B. Clark and T. Fujimoto, Product Development Performance: Strategy, Organization, and Management in the World Auto Industry (Boston: Harvard Business School Press, 1991).

8. T. Nishiguchi, Strategic Industrial Sourcing: The Japanese Advantage (New York: Oxford University Press, 1994).

9. R. Howard, “Can Small Business Help Countries Compete?,” Harvard Business Review, November–December 1990, pp. 88–103; and

Clark and Fujimoto (1991).

10. E. von Hippel, The Sources of Innovation (New York: Oxford University Press, 1988).

11. S.J. Balog and H.G. Macnguyen, “Hadco” (New York: Shearson Lehman Hutton, 21 November 1989), p. 3.

12. Throughout this case study, we used Hadco annual reports, forms 10-K, and internal documents for much of our information about Hadco.

13. Balog and Macnguyen (1989).

14. Von Hippel (1988), pp. 4, 19–24.

15. R.A. Rasmussen, “Hadco: The Change,” CircuiTree, October 1992, p. 28.

16. B.R. Watts and M.M. Pompian, “Hadco Corporation” (New York: Needham & Co. Investment Analysis, 30 June 1988), p. 5.

17. Von Hippel (1988), pp. 20–21.

18. Balog and Macnguyen (1989), p. 14.

19. Watts and Pompian (1988), p. 3.

20. Balog and Macnguyen (1989), p. 3.

21. Watts and Pompian (1988), pp. 1, 5.

22. C.C. Kenney, Riding the Runaway Horse: The Rise and Decline of Wang Laboratories (Boston: Little, Brown, 1992), pp. 69–70, 94–105.

23. C.H. Ferguson and C.R. Morris, Computer Wars (New York: Times Books, 1994), p. 138; and

Kenney (1992), pp. 166–169.

24. Ferguson and Morris (1994), chapter 2; and

Kenney (1992), chapter 10.

25. Rasmussen (1992), p. 28.

On the importance of capital investments in this industry, see:

N. Rosenberg, Inside the Black Box: Technology and Economics (Cambridge: Cambridge University Press, 1987), pp. 180–183.

26. Rasmussen (1992), pp. 25–26.

27. P.M. Senge, The Fifth Discipline: The Art and Practice of the Learning Organization (New York: Doubleday Currency, 1990).

28. “The Hadco Vision,” New Hampshire High Tech News, June 1992, p. 1.

29. For a more complete discussion of the competitive advantage provided by supplier certification, see:

G. Walker, A. Kaufman, M. Merenda, and C. Wood, “The Transmission of an Interfirm Innovation” (Dallas, Texas: Academy of Management Proceedings, 1994).

30. Rasmussen (1992), pp. 31–32.

31. G. Strout, “Identifying the Building Blocks in Leading-Edge PCBs,” Electronic Packaging & Production, May 1993, pp. 17–19.