Robust Adaptive Strategies

Topics

In 1988, I was wandering the floor of Comdex, the computer industry’s enormous annual trade show and could feel a palpable sense of anxiety among the throngs of participants. Since the birth of the IBM PC six years earlier, Microsoft’s DOS operating system had been the de facto standard of the industry, and the stability it had provided had led to explosive growth for the entire industry. But by 1988, DOS was beginning to show its age, and the big buzz on the floor of the show was “Are Microsoft’s days numbered?”

Apple, then at the peak of its powers, had one of the largest, fanciest booths at the conference. Its dazzling graphical operating system made DOS look like an antique. Aggressive Sun Microsystems had teamed up with AT&T and Xerox to combat Microsoft with a graphical version of Unix called OpenLook. Across the hall, another powerful group of companies including Hewlett-Packard, Digital Equipment Corporation, Apollo, and Siemens Nixdorf had combined forces in a consortium called the Open Systems Foundation, which was pushing its version of Unix, also with a slick graphical user interface. Meanwhile, IBM was determined not to let Microsoft advance on it again. The highlight of its booth was OS/2, a product in which it had invested heavily, and which it claimed combined DOS compatibility with the power of Unix and the Mac’s ease of use.

There was something very curious about the Microsoft booth. First, it was by no means the largest or splashiest booth. Microsoft had been quite successful, but was still dwarfed by many of its competitors. More important, the content of the booth was more Middle Eastern bazaar than trade-show booth. In one corner, Microsoft was previewing the second version of its much delayed and much criticized Windows system, which as yet had little significant market share. In another corner, the company was pushing the virtues of its latest release of DOS version 4.0. In yet another area, it was displaying OS/2, which it was codeveloping with IBM. And across from OS/2, it was demonstrating major new releases of Word, Excel, and other applications for the Macintosh. Although Microsoft was a distant second to Lotus and WordPerfect in DOS applications, it had quickly become the leader in applications for the Mac. Finally, in a back corner, it was showing SCO Unix. SCO was the largest provider of PC-based Unix systems at the time, and Microsoft had entered a marketing agreement with the company and would buy a major stake in it a few months later.

A corporate buyer standing next to me grumbled, “What the hell am I supposed to make out of all of this?” It seemed to sum up the situation. Along with the confused customers, the press was also grumbling. Columnists claimed that Microsoft was adrift and Gates had no strategy. The press also reported that tension and infighting inside the company was caused by the fact that groups on one part of the Redmond campus were furiously working on Windows and DOS, while others down the hall were pouring their energies into OS/2, the Mac, and Unix.

The ending to this story is well known, and the success of Windows has helped make Microsoft one of the most valuable companies in the world. But Window’s success was not preordained. Standing on the Comdex floor in 1988, it was far from obvious who would win. But whether it was by intent, instinct, or luck, Bill Gates created a very robust strategy for securing Microsoft’s position. Clearly, his preferred outcome was Windows’ success, but he could see that this was by no means certain. His strategy was aimed at those uncertainties. If customers wanted evolution in DOS and not revolution with Windows, he could provide that. If OS/2 won, he would share the wealth with IBM. If the Mac won, he would lose the operating system but win in applications. If Unix won, he would no longer be the major player, but at least with SCO, he could be a contender. In addition to making bets on multiple horses, he also took steps that would pay off no matter what the outcome. So, for instance, he invested heavily in building skills in graphical user interface design and object-oriented programming — two technologies that would be a factor no matter which operating system won.

This scenario is playing itself out again as Microsoft makes a bid to lead the Internet. Microsoft’s constantly shifting portfolio of development projects, investments, acquisitions, and joint ventures with software, cable TV, telecommunications, and media companies looks quite confusing if we ask, “What is Microsoft’s strategy?” It makes a lot more sense if we ask, “What are Microsoft’s strategies?”

Unreliable Minds in an Unpredictable World

Strategy development inherently requires managers to make a prediction about the future. Based on this prediction, managers make big decisions about company focus, the investment of resources, and how to coordinate activities across the company. Big decisions are hard to reverse. They usually involve serious commitments of capital and people, and once a company is heading down a particular path, it may be very costly, time consuming, or simply impossible to change.1 This is why managers often have that pit-in-the-stomach, “I really hope I’m doing the right thing” feeling when they make strategic decisions.

Developing strategies based on narrow predictions about the future is entirely the wrong mind-set for an inherently uncertain world. Recent scientific work suggests that, in fact, our intuition about uncertainty may be understated, and that the business world is even less predictable than we think — and that our minds are even worse at forecasting than we might hope.

Scientists have gained an understanding of complex systems, systems made up of many parts in which the parts dynamically interact with each other. Examples of complex systems include galaxies, ecosystems, insect colonies, brains, the Internet, cities — and business markets. While, on the surface, these systems may seem quite different, they have some deep commonalities, just as the laws of statistics apply to phenomena as diverse as gas clouds and poker games.2

Most importantly for strategists, scientists have discovered that complex systems are difficult and often impossible to predict because they exhibit punctuated equilibrium and path dependence. Punctuated equilibrium occurs when a system’s behavior is characterized by periods of relative quiescence interspersed with episodes of dramatic change. This means that occasional major upheavals (like stock market crashes) are inherent in the dynamics of the system and not the result of some unusual external shock.3 Path dependence means that small, random changes at one point in time can lead to radically different outcomes down the road — something usually illustrated by the overused metaphor of a flapping butterfly causing a hurricane.4

A particularly insidious consequence of punctuated equilibrium and path dependence is that the past is not a reliable guide to the future, as illustrated by our limited success in predicting both the weather and the stock market. The problem, however, is that people tend to recognize patterns. Research shows that people try to interpret situations in the context of patterns they have seen before (“Oh, this is just like the Latin American banking crisis of the early eighties.”) and then take action based on rules of thumb associated with those historical patterns.5 People also have a strong tendency to extrapolate current trends into the future; so, for example, we are usually more comfortable buying a rising stock than a falling one. Our drive to see patterns and trends is so strong that we will even see them in perfectly random data.6

So complex systems are almost perversely designed to trick our minds. We like to make predictions from patterns, yet in complex systems, the patterns do not have great predictive value. Punctuated equilibrium lulls us into thinking that we really do understand the world and then suddenly throws an earthquake at us. And we tend to assume linear relationships between cause and effect and extrapolate current trends into the future; yet, in a path-dependent world, extrapolation can be quite wrong.

Strategy, then, requires good predictions, but the world is inherently unpredictable, and our minds are often tricked by the patterns we see. What is a strategist to do?

Nature faces a similar problem in designing species that can survive in constantly changing and unpredictable environments. There are many examples of ingenious survival strategies that are incredibly robust and have proved quite adaptive to complex environments. Yet nature lacks even our limited forecasting abilities and relies solely on the blind process of evolution to create its strategies.

In this article, I argue that we should take a cue from nature and change the way we develop business strategy, relying less on our ability to make accurate predictions and more on the power of evolution. Specifically, I suggest that, precisely because both biological evolution and business evolution are complex adaptive systems, we can employ some of the tools scientists have used to better understand biological evolution to understand business strategy.7 Businesses should not have singular focused strategies, but instead cultivate and manage populations of multiple strategies that evolve over time.

By harnessing the forces of evolution acting on a population of strategies, those strategies will be both more robust and more adaptive than a traditional, singular, focused strategy. A robust population of strategies will produce positive results under a wide variety of circumstances, even though it may not be optimal in some scenarios. An adaptive population of strategies keeps an array of options open over time, minimizing long-term and irreversible commitments. Robust, adaptive strategies willingly sacrifice the focus, apparent certainty, efficiency, and coordination that traditional strategies provide for the sake of flexibility and a higher probability of success. Microsoft’s population of operating system strategies was neither focused, certain, efficient, nor always coordinated. Nor is its population of Internet strategies today. But the first represents the greatest business success since Rockefeller and Carnegie, and the second may prove greater still.

Strategy as Evolutionary Search

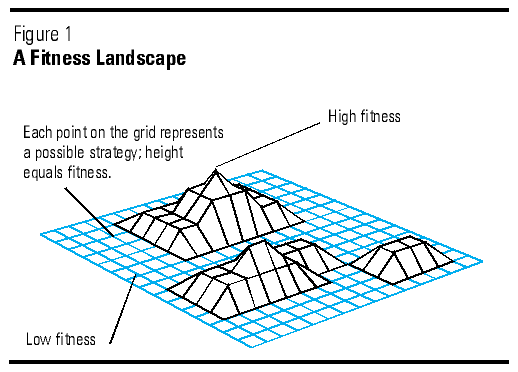

Let’s perform a thought experiment.8 Imagine a very large flat grid. Each point on the grid represents a possible strategy your company could pursue. So one point might represent “Focus on U.S. customers with a narrow product offering that is differentiated on technology and has cost advantages achieved through vertical integration.” Another point on the grid might be “Sell globally with a broad one-stop-shop product line, competing on price, and using a network of suppliers, distributors, and joint venture partners.” Say, further, that the profitability or fitness of each possible strategy on the grid is represented by its height, taking the grid to three dimensions. The grid is now a mountainous landscape of profitable peaks and loss-making valleys (see Figure 1).

{kind=link}

Scientists use just such an imaginary grid, called a fitness landscape, to understand patterns of evolution in nature.9 In a biologist’s landscape, the points on the grid represent possible gene combinations rather than business strategies, and the heights of the points represent fitness for survival rather than profits.10 We can think of evolution as the process by which species (or businesses) search for the high points in their fitness landscapes. Fitness landscapes have a number of regular properties, and by understanding those properties, we can better understand how evolution works and how it finds good survival strategies on the landscape.11

Fitness landscapes can take various shapes. Stuart Kauffman, a researcher at the Santa Fe Institute and the Bios Group, suggests that one can imagine a “Mt. Fuji” landscape with a single high point representing a strategy superior to all others. We can also imagine a random landscape with lots of jagged peaks and valleys. In most complex systems, whether biological or business, the landscapes have lots of peaks and valleys, but the heights of different points on the landscapes are correlated so that strategies differing slightly are near each other and have similar fitness levels. Thus high mountains tend to be near other high mountains, and low valleys near other low valleys, creating a complex landscape of Rocky Mountain highlands and Death Valley lowlands.12

The landscape is not fixed, like a mountain range, but is constantly bucking and heaving. As the environment and the strategies of competitors change, the fitness attributable to any given potential strategy will also change. So the height of any particular point on the landscape is moving up or down over time. What is successful today may not be successful tomorrow.

If formulating business strategy is an evolutionary search for high points in a fitness landscape, then you, as a strategist, are an Alpine hiker whose goal is to reach and stay on the highest possible peaks. However, you face several challenges. First, there is food only on the higher peaks and you can only carry a limited amount on the journey; if you get stuck in a low valley for too long, you might die of starvation. Second, you have no map of the region and must rely only on sight. Third, it is very foggy and you can only see a few feet ahead. And fourth, this region of the Alps experiences periodic earthquakes. How would you survive in such an unfriendly landscape? What would your strategy be for searching for the high peaks?

Prospering in the Wilderness

If we accept that the search for profitable business strategies can be described by a fitness landscape, then it follows that the rules for success in fitness landscapes in general also apply to business problems.

One caveat: while I contend that these rules hold true generally, their specific application will vary significantly by company and situation. They are also not perfect recipes for success and will not yield the right answer under all circumstances. However, just as they increase the odds of survival in nature, they can increase the odds of survival in business.

Three elements are vital for finding high peaks in fitness landscapes: keep moving, deploy platoons of hikers, and mix short and long jumps across the landscape.

Keep Moving

Stasis is death. If you are not constantly exploring, you’ll never find new peaks. Even if you are fortunate enough to be on a high peak, at some point, that peak will collapse as the environment changes or competitors’ actions deform the landscape. In the biological world, species respond to a constantly changing environment and relentless selection pressures through mutation and sexual recombination, constantly reshuffling the genetic deck in search of higher fitness. Since every individual in a species is slightly different from all others, even species that are relatively stable over time are constantly testing the value of that stable strategy with millions of individual experiments.

Collins and Porras, in a set of detailed case studies of successful companies, identify a common attitude they describe as “good enough never is.”13 In the language of fitness landscapes, this attitude describes a desire to try always to find higher peaks, to never settle for the current peak, and to always keep moving. Collins and Porras describe how companies such as Procter & Gamble, Merck, and Hewlett-Packard, which have remained successful for many years, create a culture of restlessness, discomfort with the status quo, and constant striving for improvement.

Deploy Platoons of Hikers

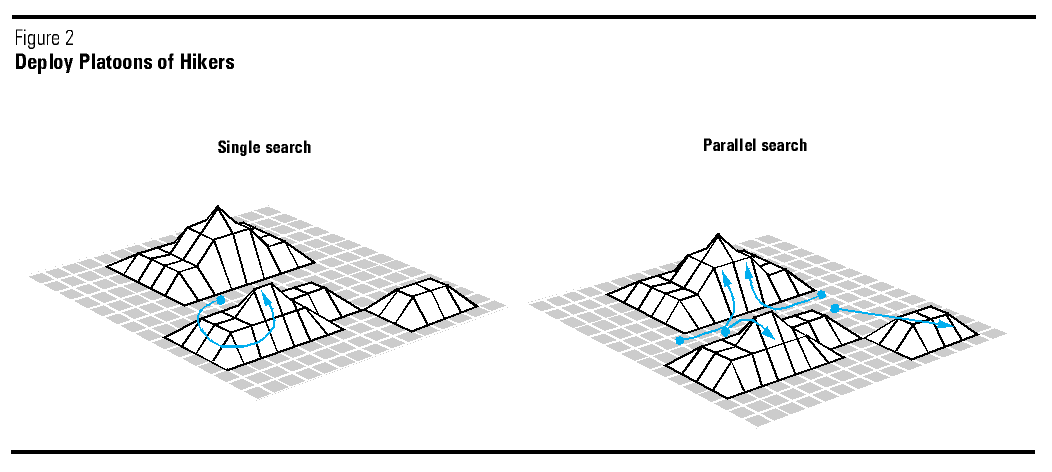

Another key to searching fitness landscapes effectively is parallelism: the more places you are simultaneously exploring, the more likely you are to find a new higher peak or to know where good spots are when your peak begins to collapse. You will find the high peaks more quickly with a platoon of hikers than with a single explorer (see Figure 2). Natural evolution is massively parallel, in that each member of a species is a different experiment on the fitness landscape, some closer and some farther from the average location of the group. Parallelism has three benefits:

{kind=link}

- Innovation and progress require experiments, yet experiments by their nature are risky; parallelism in experiments increases the odds that one or more will work out.

- What is fit today may not be fit tomorrow; having a population of strategies allows some diversity, which increases the odds of survival when the environment changes.

- Parallelism breeds boldness; having multiple experiments allows you to take a few risks without “betting the farm.”

The highly successful credit card company Capital One uses parallelism.14 At any one time, it is running scores of experiments with various product market strategies. The company rapidly develops many new ideas, tries them out in the marketplace, sees what works and what doesn’t, backs the winners, and unsentimentally kills off the losers. In this way, it generates more hits than its less prolific competitors, is better prepared to shift its focus when a particular product strategy starts faltering, and can afford to try things that more traditional competitors would shy away from.

High-performing pharmaceutical companies such as Merck apply a similar philosophy in drug discovery. They understand the uncertainty inherent in finding a new drug and improve their odds by creating populations of initiatives in new therapy design that range from incremental to radical. Although their short-term performance may be highly dependent on one or two blockbuster products, their pipeline of future opportunities always contains many possibilities.

Markets themselves are highly parallel. In the packaged goods, banking, industrial equipment, biotech, or energy markets, for example, at any time, there are scores of experiments going on with different types of strategies, in places ranging from Fortune 500 boardrooms to entrepreneurs’ garages. Thus markets deploy platoons of hikers, with different companies trying out different spots, which results in tremendous innovation in strategy, technologies, products, and processes. Most companies, however, pursue relatively singular strategies and thus occupy only one spot on the landscape. Although no one company can replicate the parallelism of the entire marketplace, it is important that companies be more like the market and simultaneously explore multiple areas of the landscape.

Mix Short and Long Jumps

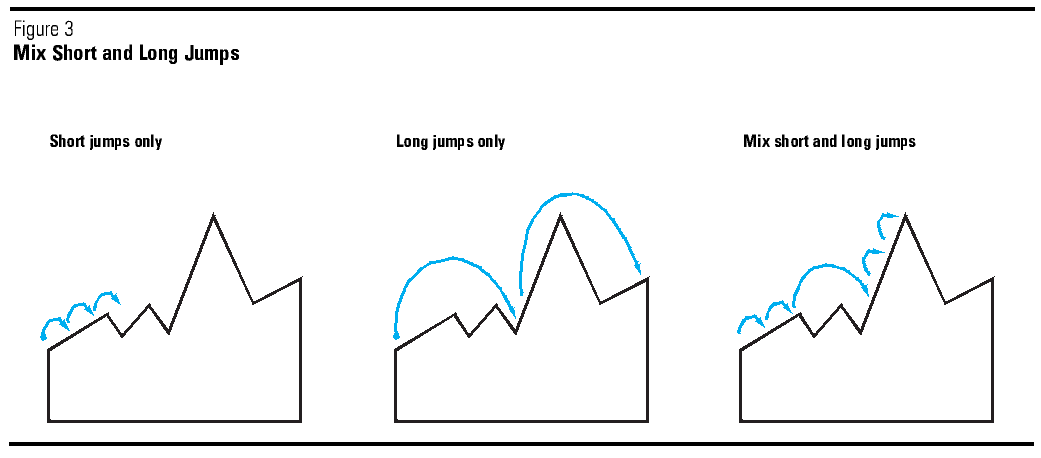

So you need to keep moving in the fitness landscape and deploy a platoon of hikers. How do you decide where your hikers should go? Although it is foggy, they can see some of the surrounding area. Sometimes the fog lifts a bit; sometimes it thickens. So the first thing to do is to look for a path leading upward in the landscape, taking incremental steps. Biologists and mathematicians call such a process of incremental upward steps in the landscape an adaptive walk.

Adaptive walks are a very efficient method for searching fitness landscapes, especially if the peaks are correlated, i.e., high peaks are near other high peaks. However, adaptive walks have an important flaw: you might arrive on a peak that is a local maximum — the highest point in its immediate vicinity but not the highest in a larger region — and get stuck, because every direction will lead down. You may get stuck on a peak where, just across a narrow valley but not visible through the fog, lies a much higher peak.

So let’s consider a second strategy. Imagine a very powerful pogo stick that lets you spring to points far away in the landscape. In nature, this ability to jump to new spots is provided by sexual reproduction, which shuffles the genetic deck more radically than point mutations of DNA, nature’s mechanism for adaptive walks. The advantage of the pogo stick is that you can get away from a local maximum and find higher peaks. The disadvantage is that, because of the fog, there’s no way to predict where your pogo hop will take you. You might land in a low valley. In nature, this is represented by the occasional appearance, through sexual reproduction, of much less fit offspring than would likely occur with a single mutation. Given that high peaks tend to be near other high peaks and low valleys near other low valleys, the farther you jump, the greater the probability you will land someplace significantly lower than where you started.

The best strategy for searching a correlated fitness landscape is really a mixture of an adaptive walk with the occasional medium and long pogo jump (see Figure 3). This can be proven mathematically and through computer simulation but makes intuitive sense as well.15 The adaptive walk ensures that most of the time you are heading toward a higher fitness level, while the jumps keep you from getting stuck on local peaks and occasionally yield significant improvements, though at the cost of occasional drops in fitness.

{kind=link}

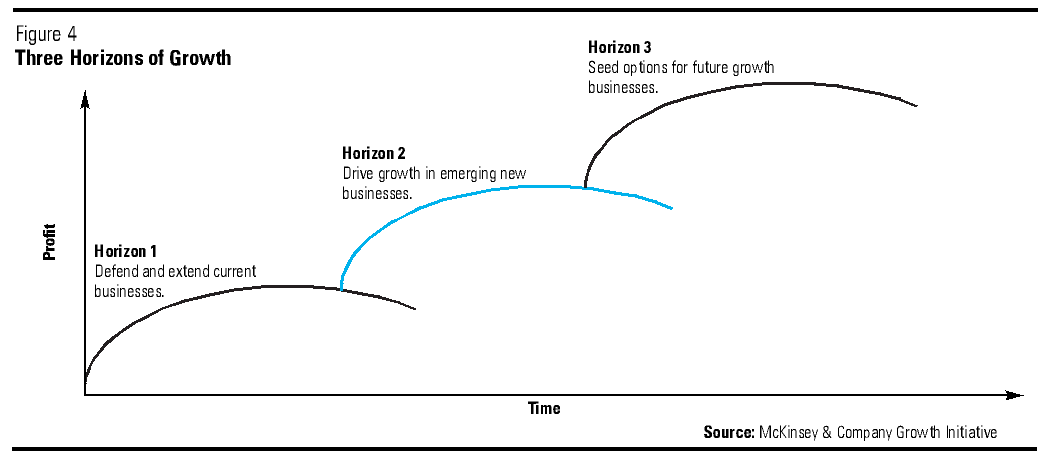

McKinsey & Company, in a study of thirty of the leading growth companies in the world, found that their actions are consistent with the notion of mixing short and long jumps.16 In general, successful growth companies manage a portfolio of strategic initiatives across three horizons:

- Horizon 1 initiatives are efforts to extend and defend existing businesses (adaptive walks).

- Horizon 2 initiatives seek to build off existing capabilities to create new businesses (medium jumps).

- Horizon 3 initiatives plant the seeds for future businesses that do not yet exist (long jumps).

The study found that most companies focus on Horizon 1 activities, but not on Horizon 2 and 3. Distinctive growth companies in contrast had much more balanced portfolios across all three horizons (see Figure 4). For example, Bombardier, the Cana-dian aerospace, transportation, and recreational vehicles company, has achieved more than 20 percent annual revenue and earnings growth for ten years by constantly creating and harvesting strategic initiatives that cover all three horizons. Current initiatives include a new class of ultra long-range business jets (Horizon 1), military aircraft maintenance services (Horizon 2), and electric vehicles for neighborhood transportation (Horizon 3).17

{kind=link}

Thus, in creating a population of strategies, it is essential that the population contain a balanced mixture of initiatives ranging from short-jump incremental extensions of the current business to long-jump initiatives that have longer time frames, are higher in risk and farther afield, but have the potential to build capability and create opportunity.

Having a mixture of jumps not only increases the odds of discovering high peaks; by providing some diversity to current strategies, it also provides some protection when the landscape unexpectedly changes. In nature, genetic diversity is critical to species survival. If a species has a diverse portfolio of genetic experiments, and the environment changes and reduces the fitness of typical members, the existence of atypical members, some of whom have a quality useful in the new environment, makes the species’ survival more likely. By mixing short and long jumps, the population of strategies will include a greater diversity of experiments, which will undoubtedly produce some unfit mutants; more importantly, however, the diversity may contain the seeds for success in an unknown future.

How different is this way of thinking about strategy? While some companies excel in individual elements of these three imperatives, few beside Microsoft and some others have put all three together to manage their strategies as an evolving population. Companies more commonly pursue singular, focused strategies that are either explicitly or implicitly based on a particular view of the world and prediction of the future. (For questions to help you determine the status of your company’s strategy, see the sidebar.)

Can We Create Populations of Strategies?

While the notion of creating evolving populations of strategies may sound appealing in theory, some practical issues and questions come to mind:

We can’t afford to do everything. Won’t we spread ourselves too thin?

A common objection to parallelism is “we cannot bet on everything.” But an equally valid truism is “we should not put all our eggs in one strategy basket.” So the best course likely lies somewhere in the middle. Nature is also frugal with resources: in the population of a species, we find significant variation, but not wild random diversity.

If we turn back to the notion of growth horizons discussed earlier, the really big dollars are committed to Horizon 1 investments, to the extension and defense of existing businesses. For Horizon 2 and Horizon 3 businesses, the dollars involved tend to scale down. Thus Bombardier is investing significantly more in the success of its new Global Express airplane than in its experiments with electric vehicles. What distinguishes Bombardier from many of its competitors is not the specific amount invested in its Horizon 3 experiments; it is the fact that it has these experiments at all.

A company will also want to bet more on a preferred outcome than on a hedging bet. So, for example, Microsoft invested more in developing Windows than it did in OS/2 or Unix. Again, what distinguished it from competitors was not the amount of money it could spend (IBM and AT&T at the time had far deeper pockets), but rather that, in addition to its preferred outcome, it had a set of hedging bets at all. A lack of money rarely keeps companies from creating a true population of strategies. Rather, issues having to do with organization, culture, incentives, and mind-set prevent it.

Diversity sounds great, but what about sticking to core competencies?

History is littered with companies that got too far from what they knew how to do and failed. Although the population of strategies should contain a diversity of strategies, they should be built from a common base of knowledge and capabilities. Thus Bombardier’s Horizon 3 initiatives, although bold, build on its capabilities in systems integration, composite technologies, and knowledge of certain customer groups. Likewise, Microsoft’s hedging moves, while diversifying its strategy, built on its software competencies. However, while long jumps should build on existing skill platforms, they should also provide opportunities to create new skill platforms. Thus Microsoft’s population of Internet initiatives is helping the company add new skills in communications technologies and media. Remember that, in nature, the population of a species may be diverse, but all are related in the end.

Can a company achieve competitive advantage without real commitment?

Many strategy theorists have noted that a decision is strategic when the company makes a commitment to irreversible investments in assets or resources that are difficult for others to copy and thus lead to competitive advantage.18 Microsoft has made enormous commitments to Windows, but the decision was not all or nothing at one point in time. Rather, the commitment built up over time, as Microsoft experimented with Windows, sometimes in fits and starts, and as it hedged its bet with other investments. If necessary, Microsoft could have shifted its commitment into OS/2: it would have lost much of its Windows investment (except for its “no regrets” investments in interface design and object-oriented programming), but at least it would not have completely lost the desktop operating system market. And again, Microsoft was not successful because of deeper pockets with which to make commitments; its pockets at the time were shallower than most of its competitors.

Competitive advantage does not come from the act of commitment itself; rather, it comes from the strategy ideas and innovations that eventually lead to commitments. A company needs a portfolio of ideas or innovations it might want to commit to as the future unfolds and uncertainties begin to resolve themselves. My approach does not negate the need for commitments; rather, it makes available a larger stream of choices to which a company can possibly commit over time.

Does this approach differ by industry or company?

Many of my examples come from software or other industries with low economies of scale. The approach may be fine for Microsoft, but how many strategies can Boeing, for example, afford to pursue? Or a small start-up? Exactly what constitutes a robust population of strategies will be different from industry to industry and company to company. The mix of short and long jumps or of shaping and hedging moves will all be highly specific. Capital One can probably maintain a larger population of strategies than can Boeing. Likewise, Monsanto, in the fast-moving biotech world, probably needs to make more effort in Horizon 3 initiatives than a commodity chemicals producer. But these are matters of degree; the general principles still hold. Both Boeing and the commodity chemicals producer should be cultivating a portfolio of strategies that contains near-term strategies, the seeds of future growth businesses, and hedges against key uncertainties, rather than pursuing singularly focused strategies that presume predictability.

So, if we believe that it is at least possible in principle to create evolving populations of strategies, how do we make them work?

Creating Robust Adaptive Strategies

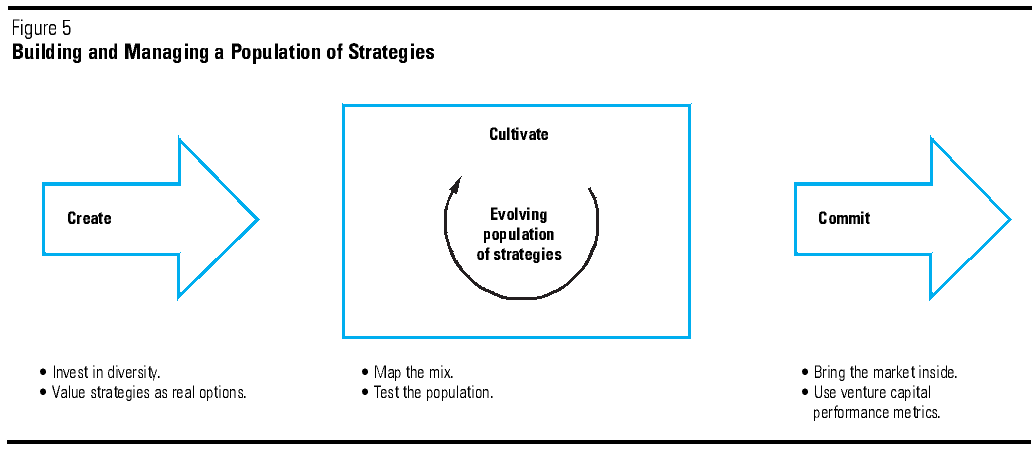

The lessons of fitness landscapes offer an untradition-al picture of what is needed for successful strategy development. Strategists need to build and manage an evolving population of strategies (see Figure 5). New ideas and innovation create new strategies that are added to the population. Those strategies are cultivated and their performance monitored as they evolve over time, and decisions are made on levels of commitment or abandoning a strategy.

{kind=link}

However, shifting an organization to this way of thinking about strategy is not easy. Often the organizational processes, measurement metrics, and incentives are geared toward a linear view of strategy and must change to support the new mind-set. In this section, I briefly discuss six actions that can reinforce the robust adaptive mind-set. This is by no means a comprehensive discussion: for example, stimulating creativity in strategy development is itself a significant issue. The individual tools are not themselves new. However, viewed through the lens of fitness landscapes and the imperatives for successful strategic search discussed in the previous section, it becomes clearer that these tools, which many companies do not use, are essential to good strategy formulation.

Invest in Diversity

In order to build and manage a diverse population of strategies, a company needs a diverse population of people. New strategy ideas are developed through inductive insights drawing on past experiences, analogies from other industries and situations, and mixing and matching elements of other successful strategies. Strategy creation is thus highly dependent on people’s experiences and frames of reference; group-think is the death of strategic diversity. This is not just demographic diversity (age, sex, race, national origin, and so on), but a diversity of experience. A McKinsey & Company study describes how companies such as General Electric create diversity by deliberately hiring from diverse talent pools and then giving employees varying experiences in different businesses, functions, and geographies.19 While many companies would see all this moving people around as inefficient, the dangers of not doing so are the same as those created by inbreeding. Diversity must be viewed as an investment and actively cultivated.

Value Strategies as Real Options

Most companies assign a critical role to the financial valuations of potential strategies. But, unfortunately, the most frequently used measures for evaluating new investments, net present value (NPV), payback period, operating profit, and return on capital, discourage strategic experimentation. All these measures share a common flaw; they fail to account for the uncertainty of the future and the probability distribution of different potential outcomes. One investment might open up entirely new avenues of exploration and another might be a dead end, but traditional analysis gives them the same value. Evaluating investments as real options can compensate for this bias and reveal the true value of experimentation.20

In the financial world, an option is a right, but not an obligation, to buy an asset within a certain time at a certain price. Options have value because they create and preserve an opportunity to do something (“the right”) for a period of time, without commitment if it later becomes unattractive (“not an obligation”). A strategy also has option value because of what it could lead to, as well as what it is intended to lead to. The strategy may open future possibilities (not certainties) that the company did not have available to it before. A strategy that locates a company in the fitness landscape so that it has many potential routes up the mountain range is worth more than a strategy that puts it in a dead-end canyon, even if the strategies have the same immediate level of fitness. Not only is there value in having lots of choices, there is also value in having a choice available over time, as it provides flexibility in an uncertain world.

Real option techniques help a company appropriately value flexibility as well. Adoption of tools for incorporating real options into decision making can influence the behavior of managers and remove the biases built into traditional measures that undervalue experimentation and flexibility.

Map Jumps on the Landscape

Most companies quite naturally make incremental moves in their strategy and are occasionally willing to make a big bet. But few companies step back, look at their population of strategies, and ask if the mix is right. The population of strategies, needs to be diversified along three dimensions: length of time frame, risk, and relatedness to the current business. Often these attributes will correlate; for example, long-term initiatives and those farther afield from the current business tend to be riskier. But sometimes they do not correlate; for example, a high-risk but near-term investment in a brand in a current business or a low-risk but long-term joint venture in a new business. Managers should categorize their strategies and initiatives as to whether they are near-, medium-, or long-term in their payoff, whether they are low, medium, or high risk, and whether they are extending or defending the current business, building a new business, or laying the foundations for future possible businesses. This provides a simple but useful map of the population of strategies.

Test the Population of Strategies

In addition to ensuring that the mix of jumps is appropriate, the company needs to ensure that the population of strategies has enough initiatives covering a sufficiently diverse but promising area of the landscape. Most companies resist parallelism; it is expensive, seems inefficient, and can put people at cross-purposes when there is internal competition. One way to see the value of parallelism is to test the population against potential scenarios by asking:

- What are the major likely future scenarios?

- Which scenarios, whether likely or unlikely, could present major threats or provide major opportunities? Have we covered ourselves for these eventualities or do we accept the risk?

- What is the preferred scenario — the one we’d like to shape?

- How will we adapt in the other potentially likely scenarios?

Classical scenario analysis, system dynamics modeling, and new frameworks for categorizing and managing uncertainty are all helpful tools for identifying areas where parallel exploration is important.21

Bring the Market Inside

In making decisions on whether to commit to strategies in the population or to abandon them, it is critical that the selection pressures on the internal population of strategies reflect as far as possible the selection pressures operating on the population of strategies in the marketplace. In many companies, investment dollars often flow to the politically powerful or to those who have yesterday’s revenues instead of tomorrow’s possibilities. In the marketplace, venture capitalists and stock market investors all try to invest in the most exciting Horizon 3 opportunities, whereas in most companies, big Horizon 1 businesses get all the attention. Thermo-Electron avoids this pitfall by inviting outside venture capitalists to participate in its early stage investments and by spinning out parts of new businesses to the stock market in IPOs, thus providing market validation to its commitment decisions.

Similarly, most companies find it difficult to abandon poorly performing strategies. Egos, career concerns, and turf battles can keep poor strategies alive. Capital One carefully distinguishes between failed experiments and failed people to encourage greater risk taking and more objectivity, and to make it easier to abandon unsuccessful strategies. It even shuts down successful efforts simply to free up good people and resources for high-potential experiments.22

Use Venture Capital Performance Metrics

Many companies apply the same performance metrics to a mature plant making widgets in Ohio and a start-up Internet operation in India. It may be entirely appropriate to measure the performance of short-jump initiatives on things like near-term operating profit or return on capital. But if a company applies these metrics to long-jump growth options, it will never allow any to survive. In addition to using real options to evaluate the initial investment decision, the metrics for evaluating the performance of the various strategies in the portfolio over time need to be different. In evaluating long-term growth options, a company needs to be more like a venture capitalist. It needs to monitor financial measures, but such measures as meeting the milestones against a business plan, progress in technology development, establishing key relationships, building talent, and market acceptance are often better indicators of value creation.

Evolution provides a powerful and effective recipe for solving problems and creating strategies in an unpredictable environment. Fitness landscapes demonstrate how evolutionary search creates robustness and adaptability through constant experimentation, parallel search, and mix of adaptive walks and long jumps. By creating and cultivating evolving portfolios of strategies, managers can make it more likely that their company will stay out of the strategy wilderness and enjoy the high fitness peaks.

References

1. See P. Ghemawat, Commitment: The Dynamic of Strategy (New York: Free Press, 1991).

2. For a discussion of complex adaptive systems and business, see:

E.D. Beinhocker, “Strategy at the Edge of Chaos,” McKinsey Quarterly, number 1, 1997, pp. 24–39.

For a general overview of the science behind complexity, see:

M.M. Waldrop, Complexity (New York: Simon & Schuster, 1992).

For technical discussions of complexity and economics, see:

P.W. Anderson, K.J. Arrow, and D. Pines, eds., The Economy as an Evolving Complex System (Redwood City, California: Addison-Wesley, 1988); and

W.B. Arthur, S.N. Durlauf, and D.A. Lane, eds., The Economy as an Evolving Complex System II (Redwood City, California: Addison-Wesley, 1997).

3. For a discussion of punctuated equilibrium in complex systems, see:

P. Bak, How Nature Works (New York: Springer-Verlag, 1996).

4. For a discussion of path dependence as applied to economics, see:

W.B. Arthur, Increasing Returns and Path Dependence in the Economy (Ann Arbor, Michigan: University of Michigan Press, 1994).

5. See J.H. Holland, K.J. Holyoak, R.E. Nisbett, and P.R. Thagard, Induction: Processes of Inference, Learning, and Discovery (Cambridge, Massachusetts: MIT Press, 1986).

6. See D. Kahneman, P. Slovic, A. Tversky, Judgment under Uncertainty: Heuristics and Biases (Cambridge, England: Cambridge University Press,1982); and

M. Bazerman, Judgment in Managerial Decision Making, third edition (Chicago: Northwestern University Press, 1994).

7. Evolution can be thought of as a general purpose process for solving complex dynamic problems. See:

J.H. Holland, Adaptation in Natural and Artificial Systems (Cambridge, Massachusetts: MIT Press, 1992).

As such, biological evolution is just one sub-class of a universal class of evolutionary processes. I take the position in this article that the search for business strategies is another sub-class of this more general class. So, although there are differences in biological and business evolution, both sub-classes are subject to the same general principles that govern all evolutionary systems. This is stronger than saying that business is metaphorically like biology, and there are some interesting analogies to be made. Rather, this position claims that any principles that make for effective or ineffective evolutionary searches in general will also apply to business strategy.

8. This thought experiment is borrowed from:

D.C. Dennett, Darwin’s Dangerous Idea (New York: Touchstone, 1995), pp. 107–113.

9. For general discussions of fitness landscapes, see:

S. Kauffman, At Home in the Universe (New York: Oxford University Press, 1995); and

Dennett (1995).

For a technical discussion, see:

S. Kauffman, The Origins of Order (New York: Oxford University Press, 1993).

10. A real fitness landscape would have a very large number of dimensions, but a three-dimensional space is easier to visualize, so I have discussed the landscape in three dimensions, although the same principles apply in higher dimensional spaces.

11. Fitness landscapes can be represented mathematically and exhibit regularities that provide insights into how evolution works. For example, Kauffman and others have borrowed the mathematics of spin-glasses from physics to explore the characteristics of evolutionary searches on fitness landscapes. See:

Kauffman (1993) and (1995).

12. Kauffman (1995).

13. See J.C. Collins and J.I. Porras, Built to Last: Successful Habits of Visionary Companies (New York: HarperCollins, 1994).

14. From presentations by J. Donehey and G.Overholser, Capital One (Boston: Ernst & Young Embracing Complexity Conference, 2–4 August 1998).

15. Kauffman (1993) and (1995).

16. See M.A. Baghai, S.C. Coley, and D. White, The Alchemy of Growth: Kickstarting and Sustaining Growth in Your Company (London: Orion Business, 1999).

17. See M.A. Baghai, S.C. Coley, R.H. Farmer, and H. Sarrazin, “The Growth Philosophy of Bombardier,” McKinsey Quarterly, number 2, 1997, pp. 4–29.

18. See P. Ghemawat and P. Del Sol, “Commitment vs. Flexibility,” California Management Review, volume 40, Summer 1998, pp. 26–43.

19. See C. Fishman, “The War for Talent,” Fast Company, August 1998, pp. 104–107.

20. See K. Leslie and M. Michaels, “The Real Power of Real Options,” McKinsey Quarterly, number 3, 1997, pp. 4–22. See also:

A.K. Dixit and R.S. Pindyck, Investment under Uncertainty (Princeton, New Jersey: Princeton University Press, 1994); and

T.A. Luehrman, “Strategy as a Portfolio of Real Options,” Harvard Business Review, volume 76, September–October 1998, pp. 89–99.

21. See, for example:

P. Schwartz, The Art of the Long View (New York: Doubleday, 1991); and

K. van der Heijden, Scenarios: The Art of Strategic Conversation (New York: Wiley, 1996);

P.M. Senge, The Fifth Discipline (New York: Doubleday, 1990);

H. Courtney, J. Kirkland, and P. Viguerie, “Strategy under Uncertainty,” Harvard Business Review, volume 75, November–December 1997, pp. 66–79.

22. Donehey and Overholser (1998).