Understanding the Dynamics of Value-Driven Variety Management

Managing product variety can be easy but hard to do well. And the difference can be significant.

As businesses add more and more products to their portfolios, they face diminishing returns on variety and more costs in bringing their products to market.1 As a result, managers must balance the costs and benefits of variety in determining their product line-ups. Experiences at Hewlett-Packard Co. and elsewhere indicate that effective variety management can lead to bottom-line improvements of up to 20% of operating profit over a less systematic approach.2

One of the biggest challenges to effective variety management is obtaining a good understanding of the costs of variety. It is necessary to invest time up front to understand these costs and develop a set of guidelines that allow the business to make the right cost-benefit trade-offs. Then these guidelines can be incorporated into a comprehensive business process for managing variety on an ongoing basis. By applying the principles and the process described below, organizations can walk away with a clearer understanding of how product variety affects costs, enabling them to make smarter decisions not just for their current product line but also for future product launches.

We worked with a wide range of businesses (see “About the Research.”) with products ranging from computers to laboratory filtration equipment, all struggling with the difficulties of exploding product variety, and discovered that despite sometimes intense efforts on the part of the businesses, their approaches exhibited several common pitfalls. In particular, a widespread approach to managing product variety is to cut low-volume products. This is also known as “trimming the tail.” Trimming approaches vary: Products can be discontinued when volumes fallbelow a threshold, a hurdle can be set on forecasted volumes for new product introductions, or a cap may be set on the total number of product variants in a product line. Regardless of the method used, these approaches are only partially effective and can often be too simplistic to truly enable decisions that are in the best interest of a company. Pitfalls are that these approaches can be:

Inconclusive – Looking only at product revenue or even gross margins can exclude key costs and benefits from the equation, causing stakeholders to feel that they have not been heard and leading to constant debate over where to draw the line between “good” and “bad” products.

Inconsistent – It is sometimes inappropriate to measure all products against the same revenue or margin scale. Some high-volume products may have close substitutes that could capture the same revenue nearly as well, while other low-volume products may contribute little to revenue but open up opportunities in new markets. Further, the cost impact of adding and maintaining products in the organization’s line-up may vary considerably depending on the product type.

Limiting – Trimming the tail often comes at the expense of other higher-value approaches to variety management. It may well be the case that a postponed differentiation strategy, for example, would allow the organization to achieve the variety that marketers desire under a dramatically reduced cost structure.

Backward-Looking – Backward-looking analyses, common with many trim-the-tail approaches, miss the opportunity for proactive management of product variety. They also miss the fact that the majority of complexity-driven costs associated with offering a product may be up-front costs that are sunk at the time of launch.

Five Lessons for Maximizing Value from Product Variety Management

Given these drawbacks, companies need a better way to define a set of criteria for when products should be added or eliminated from line-ups and how variety should be managed on an ongoing basis. We discuss five critical lessons for maximizing the value and effectiveness of variety management and present a process for making value-driven variety management successful.

Lesson 1: All Products Are Not Created Equal.

Both complexity costs and benefits may vary considerably for different types of product variants. Complexity-driven costs for new stock-keeping units can range from as low as a few dollars for products with virtually no differentiation to hundreds of thousands of dollars for products that require significant process changes or create significant impacts on the manufacturing and processing efficiency of other products. For example, a paper manufacturer may produce a wide range of paper grades, colors, cut sizes and package sizes. The complexity costs associated with adding a SKU may vary significantly, depending on the type of paper being produced. A simple change in package size may increase processing and inventory costs but may have little impact on up-front design, product validation or testing costs. On the other hand, introducing a new photo paper that uses specialty coatings to better preserve ink life may require significant development, testing and marketing investments, even if the product is a variant of an existing offering. The cost guidelines that the variety-management process is built upon should make room for these important differences.

It is not only the costs of complexity that vary widely but also the benefits. To accurately evaluate the return on product complexity, the incremental benefit of a new product variant should be compared to its incremental cost. For example, one driver of variety in notebook PC products is the portfolio of features offered — like hard drive capacities, central processing unit speeds, liquid crystal display sizes and battery-life lengths. Incremental benefits of such feature types vary widely. Some key features drive incremental sales because they are critical to competing in a certain customer segment or price band, while other features may have close substitutes. For these close substitutes, a high-volume feature may contribute little incremental profit if its volume is derived mainly from the cannibalization of other products. That is, low volume probably means low value but high volume does not necessarily mean high value. Consider the specific case of providing customers a choice between two very similar hard disk drives. Two drives with the same storage capacity may be available but with one offering faster performance. The higher-speed drive may cost only $2 more. With such a small cost differential, there may be little reason to offer the lower-speed option. Selling only the high-speed drive would not likely reduce sales but would allow for consolidated inventories and purchasing, the impacts of which may outweigh the $2 cost differential. When products or features are highly substitutable, the incremental benefit of adding a second variant can be an order of magnitude lower than that of the first.

Lesson 2: Be Exhaustive.

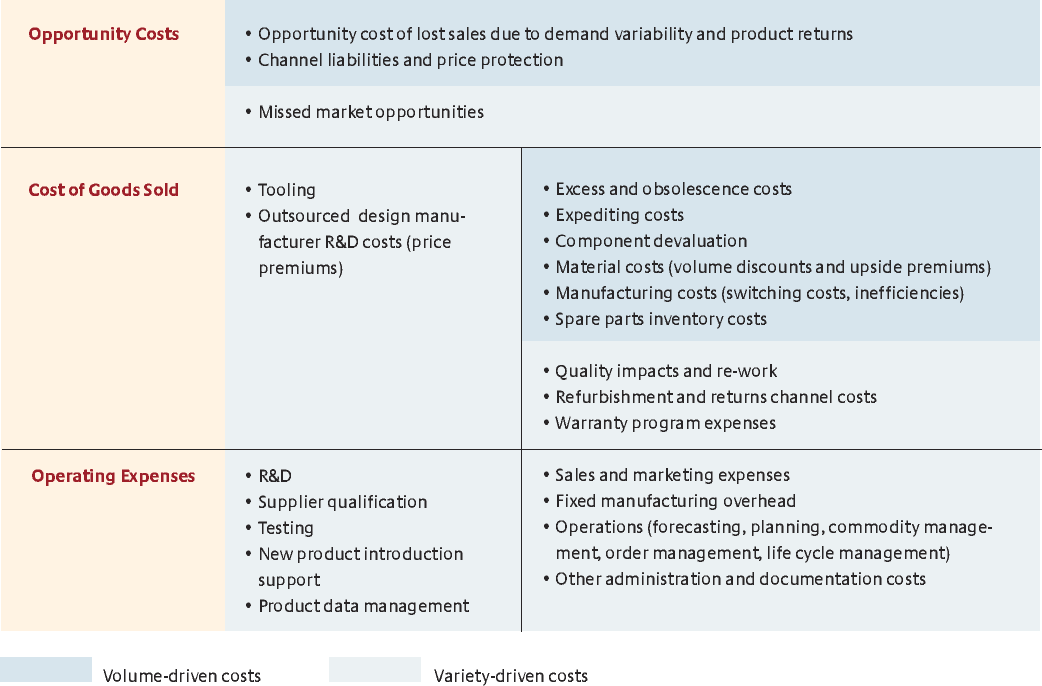

Many complexity cost analyses tend to focus on a limited set of costs rather than on an exhaustive set, spanning short-term and long-term impacts as well as fixed and variable costs. The problem with complexity is that its impact on any one cost area may be insignificant; however, it is the compound effect of a large number of impacts across a wide range of costs that create the complexity monster. Referring to the checklist (see “Complexity Cost Checklist”) ensures an exhaustive look across the entire profit and loss to see the impacts of complexity.

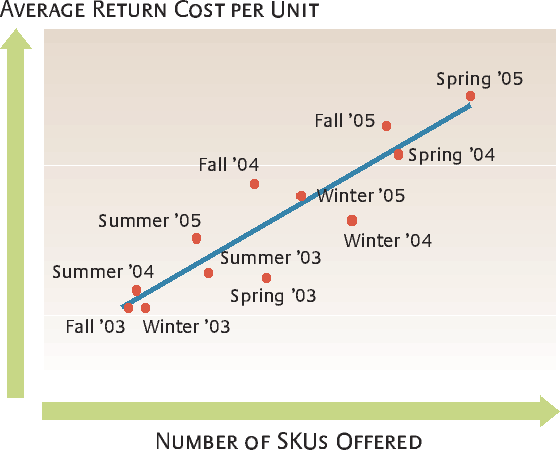

It is important to distinguish between “variety-driven” costs and “volume-driven” costs. Variety-driven complexity costs are the per-SKU costs required to bring new products to market, as well as the costs to support the products over their life cycles. They are mainly classified as fixed costs. The cost of adding a new SKU can often be estimated through activity-based costing and interviews with cost-center managers. In some cases, variety-driven costs can be nonlinear, hidden or complex. For example, factory capacity constraints can cause delays in production if too many products are launched simultaneously. In cyclical industries where all SKUs in a seasonal product line-up are typically introduced in a two-to-three-week window, factory capacity can easily become a binding constraint. There is also a strong correlation between return costs and portfolio size. (See “Variety-Driven Cost Example.”)

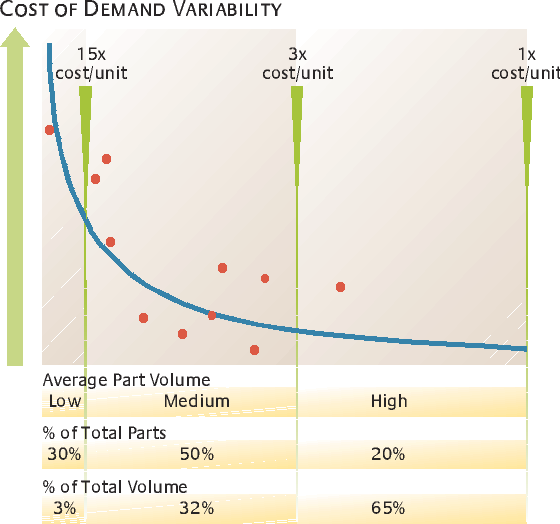

Volume-driven complexity costs are increases in the unit variable cost of a SKU or part resulting from insufficient volume to reach an operationally efficient scale. They are mainly costs that are classified as variable costs. For example, material costs may be higher on lower-volume parts due to inadequate negotiating leverage for the buyer or economies of scale for the supplier. Another major source of volume-driven costs is those costs associated with demand variability. Demand for low-volume parts or SKUs is much more variable, resulting in significantly more excess costs (devaluation, excess and obsolescence) and shortage costs (freight expediting, supplier price premiums and lost sales). An illustrative example of how those costs of demand variability increase exponentially as fewer and fewer units of a part are sold can be seen in one of Hewlett Packard’s PC product lines. (See “Volume-Driven Cost Example.”) A low-volume CPU, for example, may have a ten-times-greater-per-unit cost of variability than a high-volume CPU. In a business where these costs of variability may be as large as the operating profit itself, managing these volume-driven costs is essential. It is also not unusual, as the data in the example suggest, that most of the volume-driven costs come from “medium-volume” parts or SKUs where both the volume and cost/unit premiums are significant.

Note that being exhaustive does not require a deep analysis into every single line item of cost. One can begin with a broad list and then prune it down to a subset of the most relevant costs for more detailed investigation. (See “Complexity Cost Checklist.”) This can usually be accomplished by accounting for historical cost data and conducting a series of interviews to quickly size up the complexity cost profile of the business. The next step is to select a short list that covers at least 80% of the complexity-driven costs in the business and then focus further analysis on these short-listed costs. This is crucial, as many variety-management efforts fail by focusing on the wrong elements. It is natural to seek out the components that are familiar or for which hard data are readily available. But such anchoring can come at the expense of other more important costs. For example, cost assessments led by supply chain sponsors that focus exclusively on the inventory-driven costs can significantly underestimate the full costs of variety.

Lesson 3: Take a Return on Investment View.

Some costs of adding product complexity occur once, such as tooling costs, up-front research and development and supplier qualification. Others are recurring. A business case for adding variety should consider impacts of both one-time and recurring costs over the whole product life cycle and balance these against the incremental benefits over the life cycle. In addition, many of the costs are also investments of scarce human resources (researchers, engineers, product managers, marketers, production planners, procurement staff, etc.). Although it is possible to grow the labor force over the long term, variety decisions should consider short-term constraints and ensure that value is maximized from the resource base. Should an engineer spend her time validating a low-margin, low-volume one-off product, or should she spend her time improving the design and time-to-market on the next big thing? The best approach when approving a new product variant is to be certain that the return on invested resources required to support the variant meets or exceeds the return those resources generate for the overall business. For example, suppose the product R&D expenses are 1% of revenue in a business with a gross margin of 10%. If those R&D resources are the key constraint to introducing variety, then the incremental margin (less other complexity-driven costs) should exceed the incremental R&D costs by a 10-to-1 ratio to just be at the average for the business. A common mistake is to sum all incremental costs and benefits and approve the product if the sum is positive. If other opportunities exist for the R&D resources to generate more than a 1-to-1 return, then the projected return on R&D investment from any new product should exceed the ROI of those other opportunities. The ROI approach acknowledges that certain resources are scarce, and a hurdle should be set for allocating those resources.

Lesson 4: Tailor the Variety-Management Strategy to the Type of Complexity Cost.

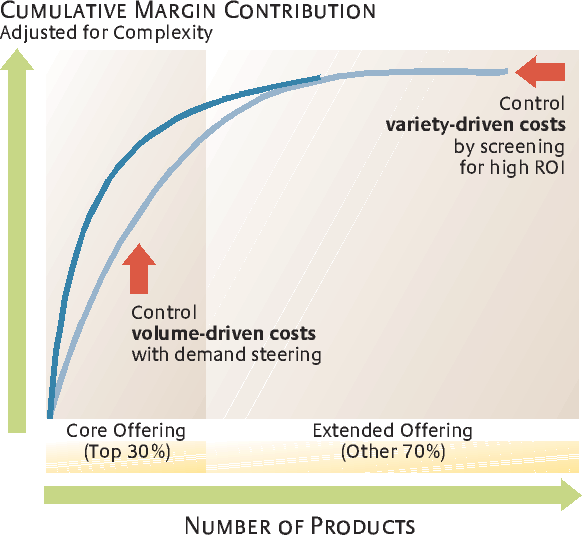

Variety-driven and volume-driven complexity costs call for very different management strategies. (See “Tailoring the Strategy.”) Managing variety-driven complexity costs involves screening out those proposed variants for which the incremental benefit does not exceed the incremental costs. This requires careful and objective assessment of the costs, benefits and ROI of potential new products. The main targets here will be some low-volume products, although a simple trim-the-tail screen would miss out on the important differences discussed above.

For volume-driven costs, on the other hand, the focus will be on high-volume products. Cutting low-volume products will have little impact on volume-driven costs, since so little of the total costs of goods sold comes from those products. Instead, managing volume-driven complexity costs requires segmenting the portfolio into “core” and “extended” components and then focusing on the high-volume items that make up the core offering. Costs are reduced by steering as much demand as possible to operationally-efficient, high-volume core products. Demand can be steered through various marketing actions, for example, by offering a shorter delivery time on the core offering or higher prices on the extended offering. This rewards the customer for helping to reduce the volume-driven costs of complexity.

The relative importance of variety-driven and volume-driven complexity should follow from the up-front analysis in order to develop complexity cost guidelines. Generally speaking, product types requiring significant ongoing management or up-front investment will benefit from controls on variety-driven costs, and product types that require high volumes to achieve operational economies of scale will benefit from controls on volume-driven costs. Both kinds of costs may even exist at different levels in the product architecture. For example, variety in platforms may drive high up-front development costs, while variety in industry-standard components may drive high operating costs. It’s essential to understand which problem you are trying to solve and to select the right tool(s) for the job.

It is common to see strategies that are not appropriately tailored if the spectrum of costs is not well understood in the first place. And depending on who is driving the variety-management effort, it may be very likely for those involved to have an incomplete view of the costs. Take the volume-driven costs: Although these may be all too familiar to the supply-chain function, they may not be as familiar to marketing or R&D teams, who frequently are the owners of decisions on product variety. One personal computer business had focused almost entirely on balancing marketing benefits with (variety-driven) R&D costs in its ad hoc variety-management process. It was a surprise to some to earn that the volume-driven, supply chain costs exceeded the variety-driven R&D costs by a factor of 7-to-1. As a counterexample, a high-end server business where a supply chain manager helped to initiate a variety-management project discovered that the R&D costs of variety exceeded the volume-driven supply chain costs by a factor of ten.

Tailoring the variety-management approach extends beyond simply selecting the cost categories to include in the assessment. It also means making sure that the right metrics are in place to monitor the business’s adherence to the strategy. Metrics to help contain the size of the “extended” offering target variety-driven costs, while metrics to promote use of the “core” offering target volume-driven costs.

Lesson 5: Reduce Product Complexity Costs without Reducing Product Complexity.

Tailoring your variety-management strategy to the most significant types of complexity cost in your business is not just about limiting variety and driving demand to high-volume products. Marketing levers, such as pricing and differentiated product-delivery times, are potential tools to minimize the impact of complexity on costs. Additionally, there are a range of approaches, starting with product and process design, which can have enormous impacts on a company’s ability to offer variety cost-effectively. Techniques such as postponed differentiation, part commonality and reuse and process optimization are all critical in enabling businesses to offer greater variety at lower cost. A successful complexity-management program should extend beyond variety management into other aspects of product and process complexity management.

A Value-Driven Variety-Management Process

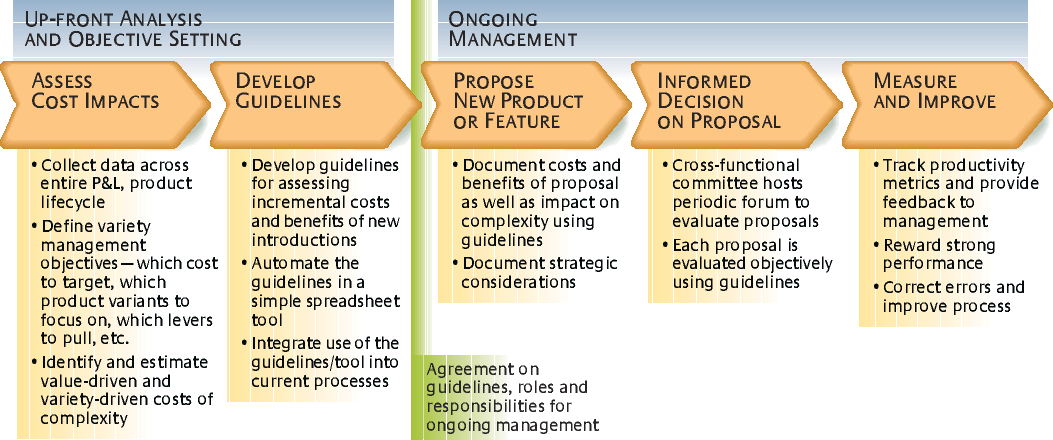

With these lessons in mind, we can construct a process for value-driven variety management. (See “Variety-Management Process.”) Initially, an up-front phase is required to codify the costs and benefits of variety management. Then, the second phase is to incorporate the learning from phase 1 into an ongoing process for the business.

Phase 1 (Step 1) – Assess Cost Impacts.

The first step is to develop an understanding of the real complexity-driven cost drivers in a business. Begin with the business’s P&L statement as a view into which costs are significant and which are not. Through a review of the data and interviews with key stakeholders, an initial assessment of where to focus can be made. Determine on which cost elements to focus and what product variants (e.g., end-SKUs, features or other higher-level constructs) to manage. After the initial part of the assessment, more effort can be spent analyzing each of the important impacted cost relationships in detail, estimating the degree of cost impact from variety in each key category. The relationship may be in the form of “dollars per SKU” (estimated from activity-based costing assessment and interviews), in the form of “dollars per unit” (for volume-driven impacts), or in a more complicated form such as “$X/SKU if the SKU count is greater than Y plus an additional $Z for each SKU with certain characteristics.”

Broad participation in this discovery phase by all the stake holders (R&D, marketing, supply chain) is essential to building the required organizational knowledge and awareness. A costly mistake can be made by allowing your analysis to be led by your business’s operations or supply chain function without the active participation and support of marketing and R&D personnel. Although supply chains may feel the pain of product complexity, they do not own the product roadmap decisions. Building a common understanding across functions about complexity costs is critical. The insights from the cost analysis can then be used to set objectives and develop a variety-management strategy targeted specifically at controlling the most significant cost drivers.

Phase 1 (Step 2) – Develop Guidelines.

Because decisions that have an impact on product variety occur regularly and involve many different stakeholders, it is not enough to have the knowledge reside with specialized experts or sophisticated tools. Implementing the strategy requires a broad awareness of complexity costs and benefits and the encoding of the newfound knowledge in the form of simple decision rules, guidelines or spreadsheet tools. Benefits of variety are more difficult to generalize into simple decision rules, but a framework should be agreed upon so that these can be assessed transparently by product or marketing managers. Finally, stakeholders should agree on how to manage product decisions on an ongoing basis with clear decision rules, roles, responsibilities and metrics.

Phase 2: Ongoing Management.

Once the up-front analysis phase is complete, the ongoing management phase begins. It is useful to have a process in which proposals for new introductions are clearly documented and assessed systematically using the guidelines developed in phase 1 (which may include “second chances” for some proposals that do not meet strict financial or return on investment criteria but which serve some important strategic purpose). Periodic reviews would then be led by a cross-functional committee to evaluate proposals in an objective manner. Each new proposed product should be required to demonstrate its worth (based on the guidelines) before it can be approved.

Despite the value of the process, many mature businesses lack any sort of formal approval process for launching new product SKUs. For instance, at one time at Hewlett-Packard, it was harder to get a travel request approved to travel from San Francisco to Houston than it was to gain approval for a new SKU to be launched.

ONCE A BUSINESS HAS A COMPREHENSIVE PROCESS in place to manage variety, it should begin to see benefits that surpass the more traditional trimming of the “tail.” When the perceived costs of a new SKU are brought closer in line with its real costs, better educated decisions can be made regarding portfolio size and variety. Unnecessary costs due to excessive customer returns, wasted resources and personnel, inventory costs and even angry stakeholders can be limited. The goal is to bring the entire organization into the decision-making process. Permitting a voice to all stakeholders in an organization eliminates emphasis on a single aspect of the problem and replaces single-cost decisions with a more complete view of total return on investment. This new focus will allow companies to trim the right products from their line and introduce new products with more confidence and profitability.

References

1. For related discussion and examples see M. Draganska and D. Jain, “Product Line Length as a Competitive Tool,” Journal of Economics & Management Strategy 14, no. 1 (Spring 2005): 1–28; M. Gottfredson and K. Aspinall, “Innovation Versus Complexity: What Is Too Much of a Good Thing?” Harvard Business Review (November 2005); and M. George and S. Wilson, “Conquering Complexity in Your Business,” (New York: McGraw Hill, 2004).

2. Based on Hewlett Packard’s projections of potential impact. For additional examples, see George and Wilson, “Conquering Complexity in Your Business.”