How Can Service Businesses Survive and Prosper?

Presently the service sector of our economy is characterized by both profusion and confusion. By profusion, I mean that it has done wonderfully well at generating jobs, for new kinds of services are sprouting continually. By confusion, I mean that service businesses seem to rise and fall from Wall Street grace with regularity. Moreover, as many are markedly entrepreneurial in spirit, they all claim to have idiosyncratic operations. For example, while manufacturing management enjoys the benefits of various professional societies (i.e., those for materials management, manufacturing engineering, industrial engineering, and quality control) whose roles are to find management principles that apply across many different kinds of manufacturing enterprises, service business management does not enjoy such cooperation. All too often, service companies view themselves as unique, and consequently they do not promote service operation management techniques with the same vigor as does the manufacturing sector.

Some manufacturers, of course, also claim that they are unique. However, over the years, manufacturers have been unified by their acceptance of certain terminology to describe generic production processes — job shop, batch flow, assembly line, continuous flow process. This not only helps to solidify manufacturers of sometimes widely divergent product lines, but it also helps to reveal the challenges manufacturers face.

The Characteristics of a Service Business

The confusion surrounding service operations can be lessened in part by looking at key aspects of service businesses that significantly affect the character of the service delivery process. Specifically, there are two elements that can be used to classify different kinds of service businesses. These elements will serve later as a springboard for investigating the strategic changes of service operations and the challenges that lie ahead for managers.

Labor Intensity

The first key element is the labor intensity of the service business process. Labor intensity is defined as the ratio of the labor cost incurred to the value of the plant and equipment. (Note that the value of inventories is excluded because the concept seems “cleaner” without taking inventories into account.) A high labor-intensive business involves relatively little plant and equipment and considerable worker time, effort, and cost. For example, professional services are typically a high labor-intensive business. A low labor-intensive business, on the other hand, is characterized by relatively low levels of labor cost compared to plant and equipment. Trucking firms with their break-bulks and other kinds of terminals, trailers, and tractors are an example. It is important to think of labor intensity as a ratio. Many, for example, think of hospitals as labor intensive — after all, hospitals are filled with nurses, technicians, orderlies, and doctors. Nevertheless, despite employing large numbers of people, a hospital has a comparatively low labor intensity because of the very expensive plant and equipment it must have. Table 1 documents the labor intensity of some broad service industries.

{kind=link}

Consumer Interaction and Service Customization

The other key element of a service business is somewhat more confusing because it combines two similar but distinct concepts: (1) the degree to which the consumer interacts with the service process; and (2) the degree to which the service is customized for the consumer. This joint measure has a high value when a service evidences both a high level of interaction and a high level of customization for the customer. Similarly, when both individual measures are low, the joint measure has a low value. Where there is a mix of high interaction with low customization (or the other way around), the joint measure falls somewhere in between.

What exactly do these measures mean? A service with a high level of interaction is one where the consumer can actively intervene in the service process, at will, often to demand additional service of a particular kind or to request that some aspects of the service be deleted. However, high visibility or duration of contact with the process is not enough to indicate high interaction. College teaching, for example, is a highly visible service activity in that students are in class for long periods of time. However, seldom do student consumers actively intervene in the process. Thus college teaching has a comparatively low level of interaction.

A service with high service customization will work to satisfy an individual's particular, and perhaps full range, of preferences. A physician typically gives very individual, customized service. Furthermore, good physicians are always open to feedback from their patients and willing to rethink and modify the service they provide. College teachers, on the other hand, are reluctant to throw out the syllabus to accommodate student desires: they “teach what they know.”

To clarify further this joint measure, consider the restaurant industry. At the low end of the spectrum are McDonald's and Kentucky Fried Chicken. Here, the consumer's interaction with the process is typically brief and controlled (i.e., order, payment, and pickup), and customization does not prevail. The service is prompt and courteous, but everybody is treated the same. At Burger King and Wendy's consumer interaction is similarly brief and controlled. However, these fast-food chains offer measurably more customization for the consumer — you can have a burger “your way.” This process permits some customization.

Cafeterias provide even more customization for the consumer (i.e., the opportunity to choose from a wide range of foods) and a modest increase in interaction (e.g., as one proceeds down the line, one can often request the staff to replenish an item or to serve a rarer cut of roast beef). Next in line are restaurants with salad bars that have some waiter assistance. Such restaurants offer customization similar to that of a cafeteria but there is more customer interaction: the waiter can be called on, at will.

Finally, there are restaurants with extensive waiter services. Such restaurants typically permit a high degree of customization and interaction: the customer decides what he or she wants to eat and when he or she wants to be served (e.g., “we'd like to enjoy our cocktail now and order later”; “coffee later, thank you”), and the waiter is on call, at will, to fill any particular desires. However, it should be noted that the haute— cuisine restaurant is not necessarily at the highest end of the customization/interaction spectrum, as some of them offer limited menus and many even decide the particular seating time. In this case, consumers are willing to trust the chef because of the food's known quality and the restaurant's ambience.

For many services, customization and interaction go hand in hand: if one is high, the other is high; if one is low, the other is low. There are services, however, where they differ. Insurance underwriting, especially at Lloyd's of London, offers considerable customization but a low degree of interaction with the client. On the other hand, an advertising agency typically is high on both customization and interaction. A travel agency provides a different example. The typical business traveler service is fairly standard and often involves merely presenting the schedule options to the traveler and issuing the ticket. Here, the degree of customization is not nearly as great as it is for planning a pleasure trip. On the other hand, business travel often demands rescheduling and a good deal of tinkering with timetables. Thus, business travel agency work often involves more interaction than customization.

Other Service Classification Schemes

Other observers have sought to classify service operations, notably Richard Chase, David Maister, and Christopher Lovelock. Chase arrays various services along a continuum from high to low “contact.”1 For Chase, contact refers to the duration of a customer's presence in the service system. According to this scheme, hotels are high contact, “pure” services, while the postal service is low contact. Repair shops are medium contact services, lying in between the prior extremes.

Although Chase makes a useful distinction, his distinction is not as helpful as it could be. A number of services can be judged high contact even though they only “shelter the customer” and in the process have very little interaction with the client. To use Chase's example, a hotel is a high-contact service, but, to me, hotels are vastly less demanding than are hospitals, primarily because hotels interact with customers in limited and very structured ways, whereas hospitals must interact with patients in irregular and frequently sustained ways. Hospital management is much more demanding, and is, therefore, worthy of classification apart from that of hotel management.

Chase's classification scheme becomes even more problematic when he turns to examining potential operating efficiency.2 Here, Chase asserts that

By this mode of thinking, the greater the ratio of customer contact time to service creation time (a somewhat nebulous term that refers to the work process involved in providing the service itself), the lower is the potential efficiency of the service facility.2 If this is so, hotels have lower potential efficiencies than do either the postal service or repair shops. If I am not misinterpreting Chase, the implication of his assertion is curious. For many people, hotels are often viewed as considerably more efficient, and certainly more profitable, than the postal service or many repair shops. As far as I am concerned, contact time simply does not capture completely what is challenging about service sector management.

Maister and Lovelock come closer to the mark.3 They use both the extent of client contact and the extent of customization to dimension a two-by-two matrix that distinguishes among the factory, the job shop, mass service, and professional service. Unfortunately, Maister and Lovelock do not spend much time either describing or pursuing this characterization. They do not identify particular services as belonging to one or the other of their matrix quadrants, and, therefore, it is difficult to take them to task. However, they do use client contact, and, as was discussed above, the notion of client contact may be fraught with more ambiguity than is necessary.

Here, I argue that services are better classified by using both the degree of labor intensity and the degree to which (1) the consumer interacts with the service and (2) the service is customized for the consumer. By expanding the two-by-two matrix, it is possible to analyze the challenges service managements face and the dynamics of operation changes in their businesses.

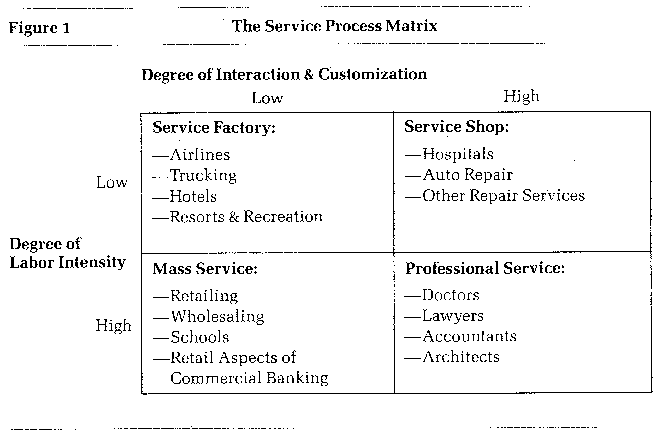

The Service Process Matrix

I have characterized services as being either “high” or “low” in terms of client interaction and customization. Naturally, not all service businesses fit cleanly into these extremes: there are many shades of gray. Nevertheless, these extremes are helpful in developing a two-by-two matrix that can categorize a whole host of diverse service businesses. Figure 1 displays a service matrix and indicates some of the classic service businesses that fit neatly in one of the four quadrants. As this figure shows, service businesses that have a relatively low labor intensity and a low degree of customer interaction and customization are labeled “service factories”: airlines, trucking, hotels, and resorts are classic examples. As the degree of interaction or customization for the consumer increases, however, the service factory gives way to the “service shop,” much as the line flow operation gives way to a job shop operation when customization is required in manufacturing. Service shops still have a high degree of plant and equipment relative to labor, but they offer more interaction and customization. Hospitals, auto repair garages, and most restaurants are examples of service shops.

{kind=link}

“Mass service” businesses have a high degree of labor intensity but a rather low degree of interaction and customization. Many traditional kinds of services can be found in this category, such as retailing, wholesaling, schools of all types, and many services like laundry, cleaning, and many routine computer software and data-processing functions. If the degree of interaction with the consumer increases and/or customization of this service becomes the watchword, mass service gives way to “professional service”: doctors, lawyers, accountants, architects, investment bankers, and the like are the archetypal examples.

Challenges for Service Managers

Variations in the managerial challenges of different services stem from the high and low distinctions made of labor intensity and interaction/customization. For example, in the case of low labor intensity (e.g., hospitals, airlines, hotels), the choice of plant and equipment is heightened. Monitoring and implementing any technological advantages are also critical. In such low labor-intensive services, capacity cannot be augmented easily and so demand must be managed to smooth out any peaks and to promote off-peak times. The inflexibility of capacity also implies that scheduling service delivery is relatively more important for these low labor-intensive businesses than it is for others.

As for services with high labor intensity (e.g., stores, professional associations), managing and controlling the workforce becomes paramount. Hiring, training, developing methods and controls, employee welfare, scheduling the workforce, and controlling work for any far-flung geographic locations are critical elements. If new units of operations are contemplated, startup may become a problem and managing the growth of such units can often be difficult.

Different managerial challenges also surface when we consider the distinction made between high and low levels of consumer interaction and customization. When the degree of interaction and customization is low (i.e., airlines, retail stores, commercial banks), the service business faces a stiff marketing challenge. Such a business must try to make the service it provides warm, even though it does not give all the personal attention that a customer might want. This means that attention to physical surroundings becomes important. In addition, with a low degree of interaction and with little customization, standard operating procedures can be instituted safely. In this type of service, the hierarchy of the operation itself tends to be the classic pyramid with a broad base of workers and many layers of management. Furthermore, the relationships between levels in the pyramid tend to be fairly rigid.

As the service takes on a higher degree of interaction and customization (i.e., professional associations, hospitals, repair services), management must deal with higher costs and more talented labor. Managing costs effectively — either by keeping them down or by passing them on to consumers — becomes a significant challenge. Maintaining quality and responding to consumer intervention are also important. In addition, talented employees demand attention and expect advancement in the organization. In effect, what this all means for many service businesses with high interaction and customization is that the hierarchy of control tends to be flat and unlike the classic pyramid. As the relationship between superiors and subordinates tends to be much less rigid, management must continually strive to keep workers “attached” to the firm by offering innovative pay and benefits packages and by paying close attention to quality of worklife issues.

As Figure 2 demonstrates, the high versus low differentiation made for labor intensity and the degree of consumer interaction and customization yield distinct combinations of management challenges for the four service types identified. Typically, well-run service factories, service shops, mass-service firms, or professional firms pay close attention to all of the managerial challenges that apply to their quadrant of the matrix.

{kind=link}

Innovations and Strategic Changes

Categorizing service businesses into quadrants can be used to investigate the strategic changes of service operations over time. At least some of the current confusion has occurred because service industries are changing rapidly. The most salient development in the service sector is vast segmentation and diversification. Services that were once clearly service shops or mass service firms are no longer clearly labeled as such. Service firms are spreading themselves out across the service matrix. Below are examples illustrating this trend.

Fast-Food Restaurants.

A classic strategic change involved the development and evolution of fast-food restaurants. The traditional restaurant could be positioned as a service shop with relatively high customization and interaction for the consumer and a middling labor intensity. The elegant gourmet restaurant may even be classified as a professional service. On the other hand, with the advent of fast foods, interaction and customization for the consumer have been lowered dramatically, as has labor intensity. As a result, the restaurant industry today encompasses a wide diversity of operations.

Hospitals.

Another interesting innovation within the service shop quadrant involved hospitals. The new kinds of hospitals developed by Humana, Hospital Corporation of America, and others are different from the traditional community hospital or university medical center. Whereas the traditional hospital (especially the university medical center) is set up to diagnose and treat any disease by investing in all of the latest equipment and technology, this new breed of hospital customarily deals with the more routine kinds of medical treatment: intensive care units and other high expense units for very sick or dying patients are often not a part of these hospitals. Very ill patients are referred to larger, and better-equipped hospitals. For its part, the new type of hospital offers a much lower cost service that is convenient for the consumer. In this respect, this new breed of hospital offers less customization but, at the same time, demands a higher degree of labor intensity. As Table 1 shows, there is a lower capital-to-labor ratio for “for-profit” hospitals than there is for traditional community hospitals. For-profit hospitals are not burdened with all the capital expenditures that are part of the traditional hospital. Table 1 also shows that teaching hospitals, perhaps for understandable reasons, are more labor intensive than are community hospitals.

Mass Services.

Another series of changes occurred in some of the mass service operations. Retailing offers some interesting examples. The expansion of catalog stores (e.g., Best's), warehouse stores (e.g., Toys R Us), mail-order sales (e.g., L.L. Bean), and brand-name discounters (e.g., Loehmann's) has shifted the emphasis of traditional retailing operation toward a lower degree of labor intensity. This was made possible because such services provide less than department store-type “full service.” On the other hand, the proliferation of boutiques and specialty operations within stores like Bloomingdale's is evidence of a different kind of change, one where interaction and customization are stressed. This often demands higher labor intensity (more than “full service”). By being more “professional” — frequently by putting salespeople on commission — such stores hope to convert more “browsers” into “buyers.”

The deregulation of commercial banking and financial services also created some intriguing strategic operation changes within the mass service quadrant. Automation in commercial banking (i.e., automatic teller machines, electronic transfers, and other new technological advances) has made commercial banking less labor intensive. Indeed, credit-card operations and check clearing are now placed in their own facilities (often at quite a distance from the commercial banks themselves), and they do essentially the kind of work that one would expect in a service factory. A similar change is evident in some other financial service companies. One of the justifications given for the acquisition of Lehman Brothers Kuhn Loeb by Shearson/American Express was the fact that the trading operations of Lehman Brothers could be absorbed easily by slack capacity in the backroom operations at Shearson.

However, even though technological advances have made it possible for some aspects of commercial banking to become less labor intensive, there is still a move to customize other services even more. Customization in this business grew out of the removal of interest rate ceilings on certificates of deposit, the cessation of fixed brokerage commissions, the demise of Regulation Q, which affects interest rates on bank accounts, and the initial steps toward interstate banking. Moreover, many of the services that have been acquired by the “financial supermarket” companies are essentially services that will give those companies greater interaction and customization. Consequently, the increasing menu of services provided by the traditional brokerage houses may cause the old-time broker, who tried to be all things to his client, to become an anachronism. Merrill Lynch, for example, is promoting both greater automation and increasing customization of its services.

Choosing Appropriate Operations

Service-business innovations, which have resulted in increasing segmentation and diversification of this sector, point up the need to assess the industry's operational choices. The insights of Wickham Skinner are as relevant to service businesses as they are to manufacturing organizations.4 Service operations, like factories, have to be tailored to do certain things well at the expense of doing other things well. Moreover, one cannot assume that the “formula” that has been so successful in one service business will necessarily carry over to another service business, even if that business is merely a segmentation of the old one. Thus, the more explicit a service business can be about the demands of the business in light of its operations choices, the more appropriate those choices are likely to be.

McDonald's, for example, has been adamant in maintaining its focus on the fast-food business and has resisted diversifying into other types of fast-food chains or service businesses. On the other hand, Toys R Us has moved away from the warehouse-type store operation and has ventured into children's clothing, Kids R Us. Recognizing that children's clothes cannot be sold like toys, the company has altered its operations to provide more interaction and customization. At Kids R Us, the store sizes and layouts are different, the workers (clerk-counselors and clothes “runners”) that are hired and trained to provide a more personalized service are different, and the inventory control systems are different.

Moving toward the Diagonal

Given the quickening pace of segmentation and diversification of service businesses, several observations concerning the dynamics of service processes bear mentioning. First, many of the segmentation steps that service businesses have taken have been toward the diagonal that runs from the service factory to the professional service firm. Figure 3 illustrates this move. Still, one may ask, What makes the diagonal so attractive to existing services? The answer seems to be better control. However, it should be noted that the kinds of controls needed for mass services are different from those needed for service shops.

{kind=link}

On one side of the diagonal, mass service controls often relate to labor costs and efficiency, for these services are trying constantly to get a grip on labor scheduling and productivity. Here, plant and equipment are rarely constraints. For example, in retailing, labor is a critical variable cost, and, therefore, scheduling labor is an important activity. The increased use of point-of-sale terminals has permitted the tracking of sales of different items by 15-minute intervals throughout the day. Such information, in combination with sales per salesperson per hour (a productivity measure), is tremendously useful to inventory control, not to mention workforce scheduling. Moves toward more customization (e.g., the department store boutique and its commissioned salespeople) can also be understood as a move to increase control of the selling situation, with higher revenues, profits, and productivity as the end result.

On the other side of the diagonal, the service shop frets about control of the service itself. With this kind of service, plant and equipment are constant constraints. Therefore, there are concerns for how frequently unpredictable jobs (e.g., auto repairs, patients) can be scheduled through expensive capital equipment. Control is also affected by the uncertainty over when and how people can tell when a service is rendered satisfactorily. Hospitals, for example, have a high proportion of fixed costs and thus worry a great deal about capacity utilization. Current debates about who should dictate the utilization of hospital resources — administrative staffs or medical staffs — are, at the core, debates about resource control. In this context, one can understand pressures to provide less customized and/or interactive service (e.g., fewer tests, more ambulatory care).

The service factory and the professional service firm, on the other hand, suffer less from loss of control. Although control is still an issue for both kinds of services, for the professional service firm, control is more of an individual concern, relatively free of constraints of plant and equipment. The high degree of interaction and customization required of such firms is at least matched with a high degree of training and skill in the workforce.

The service factory can develop its “production process” to foster more control. The process that defines the service and the flow of information and materials is relatively smooth. In this regard, the service factory shares many of the benefits that manufacturing operations enjoy. The labor needed is well known for given levels of demand, and scheduling of labor, plant, and equipment is fairly straightforward.

Even though there are pressures for existing operations to move toward the diagonal, there is no reason to think that all service shops or mass service operations will become extinct. Many operations will be able to adhere to their traditional operations. Moreover, marketing pressures for increased customization and generation of completely new services are likely to replenish the supply of service shops or mass service operations. Witness, for example, the demand for luxury airplane travel or luxury hotel accommodation. These are new services that are rendered to particular market niches. Note too the recent change in how computers are sold — that is, through mass outlets as opposed to individual salespeople. The recent shift by J.C. Penney toward more “full service” is yet another example.

Moving up the Diagonal

Another observation centers on some of the service businesses already located on the diagonal. The professional service firm and the service factory are not immune to strategic changes. Of those services that have changed their positions within the service process matrix, most have moved up the diagonal. Consider, for example, the changes that have occurred within many law firms over the last decades. The institution of paralegals and other lower cost labor and the increasing specialization of many law firms have driven many firms within that industry toward lower labor intensity and less customization (i.e., less full service). Similarly, other professional service firms have invested in equipment, much of it for word processing or data processing.

Commercial banking in California is an example of a service business in the throes of change. Given its faltering economic position, the state is currently applying pressure on bank loan portfolios. Deregulation has also pressed heavily on the industry. Banks have been forced to seek lower costs to compensate for the increased rates they have had to pay to attract funds. In addition, deregulation has permitted banks to explore new lines of business. Given these pressures, it is understandable that BankAmerica, for instance, closed 132 branches in 1984 and reduced its workforce by 4 percent. Such decisions reflect a move up the diagonal, away from the old “formula.” Furthermore, the bank scouted out the insurance industry as a potential source of earnings.

In a similar vein, the deregulation of trucking and air travel has meant significant change for the service factories. Trucking deregulation has forced many of the old-line common carriers to invest dramatically in breakbulks and additional freight terminals for less-than-truckload shipments. While such capital investments have meant increased barriers to entry for trucking firms, these firms can no longer afford to offer as customized a service as they used to for their clients. Today, their services are more specialized. In addition, their pricing structures have been changed to encourage the clients to ship in particular ways. Consequently, common carriers are moving up the diagonal.

A similar story can be told of the airlines. Deregulation encouraged major airlines to shift to hub-and-spoke systems, which means that a number of “pushes” can be made from their major airport hubs during any day. Where once competition focused on time of day and elegant service, competition these days centers more on price and less on the number of flights and the optimum time of day. The result for most airlines has been both less customization and lower labor intensity, given the significant investments that have been made at the hubs.

But just as movement toward the diagonal does not necessarily mean that service shops and mass service firms will cease to exist, the move up the diagonal does not necessarily mean that professional service firms will become small service factories. There will always be some firms that will be able to maintain successfully a high labor intensity and high interaction and customization. Furthermore, new professional services will spring up that will demand, at least initially, a combination of high labor intensity and high interaction and customization.

Conclusion

For many existing services, the pressures for control and lower costs will tend to drive them toward the diagonal and/or up it. For many service firms, such positions will be the most profitable ones. Understanding such pressures on a service operation is well advised because it can help existing service businesses anticipate the nature of competitors' changes as well as many of the management challenges they will face over time (see Figure 2). In fact, what will be demanded of many newly created service businesses will be very different from what was demanded of their predecessors. Therefore, companies that appreciate and anticipate these differences will be at a strategic advantage. Those businesses that are diversifying or segmenting will know that the old “formula” may have to be changed for the new business, and they will have more than an inkling about how such operations should change. Competing service businesses that understand these changes will have a better appreciation for competitor moves and will also better understand relative strengths and weaknesses of their own operations.

Service managers who continue to claim that their operations are unique may be left in the dust by those who see their operations as more generic. When service firms begin to appraise themselves as service factories, service shops, mass service, or professional services — much as manufacturers see themselves as job shops, assembly lines, continuous flow processes, and the like — the service version of the not-invented-here syndrome will fade away and management minds will be more receptive to general, and generalizable, service management concepts.

References

1. R.B. Chase, “The Customer Contact Approach to Services: Theoretical Bases and Practical Extensions,” Operations Research 29 (1981): 698–706;

R.B. Chase, “Where Does the Customer Fit in a Service Operation?” Harvard Business Review, November–December 1978, pp. 137–142;

R. B. Chase and D.A. Tansik, “The Customer Contact Model for Organizational Design,” Management Science 29 (1983): 1037–1050;

R.B. Chase and N. Aquilano, Production and Operations Management (Homewood, IL: Richard D. Irwin, 1985), ch. 3.

2. Chase (1981).

3. D.H. Maister and C.H. Lovelock, “Managing Facilitator Services,” Sloan Management Review, Summer 1982, pp. 19–31.

4. W. Skinner, “The Focused Factory,” Harvard Business Review, May–June 1974, pp. 113–121.