Adding Value in Banking: Human Resource Innovations for Service Firms

More than a decade after the deregulation of the leading service industries, consumers are accustomed to service providers competing on price. Now consumers demand increasingly higher levels of service quality. For service companies, staying competitive in the new market environment means not only offering products at reasonable prices but also tailoring these products to meet individual customers’ needs.1

Some companies have moved quickly to take advantage of this market shift.2 Delta Dental Plan of Massachusetts, a health insurance provider, and MBNA, a credit card provider, have both used quality service delivery to transform mediocre businesses into industry leaders. Merrill Lynch, a brokerage house, and IKEA, a Sweden-based retailer active in many parts of the United States, have relied on quality-oriented service strategies to turn their companies into high-performing, competitive organizations. All four companies have redesigned their work practices to leverage information among different products and provide customers with quick, customized, price-competitive service offers. The companies have trained and empowered employees directly involved in service delivery to undertake a broad range of tasks. They have given priority to minimizing labor turnover on the theory that employees with long tenure better understand both a firm’s customers and its internal work processes and so are better able to meet individual client’s needs.

Yet these companies are the exception. Most service-sector firms have been slow to redesign work practices. From hotels to banks to retail outlets, service-sector managers continue to rely on an “industrial model” of service delivery. They have organized work so as to tolerate low skills and short employment tenures and continue to concentrate on cutting costs rather than adding value.3 By thinking mainly about price competition, most service managers have invested minimally in their employees. Downward pressure on wages, minimal training expenditures, and heavy use of part-time workers have reduced personnel costs and maintained managers’ flexibility to cut the work-force when demand slackens.

Most explanations for service-sector firms’ failure to compete on quality have focused on managerial decision making. Unwarranted faith in the powers of information technology, a commitment to scientific management, and historical antipathies between management and labor are all said to have discouraged managers from designing their competitive strategies around high-skill and high-quality organizations.4 In this view, reorienting business strategies to take advantage of consumers’ new quality consciousness is assumed to be primarily a function of changing managerial attitudes. Once service-sector managers understand the importance of customization to their competitive success, they will simply rewrite their human resource policies and practices.

Using the U.S. banking sector as a case study, we suggest the need to rethink both the causes and remedies for the “cycle of failure” in the U.S. service economy. As the financial services market has become more competitive, an emphasis on building strong financial relationships to support customization of product and quality service delivery seems to be a natural source of competitive advantage for commercial banks. What most distinguishes banks from other financial service providers is their extensive branch network. The high overhead costs of maintaining many branches make it difficult for banks to be low-cost leaders. The high level of customer contact that branch offices provide offers banks many opportunities to use integrated service delivery and relationship management to cross-sell products. While a relationship management strategy is not appropriate for all market segments in which banks operate, it can be a particularly strong source of competitive advantage in attracting high-end retail customers and small- and medium-sized business enterprises. Both types of customers have sophisticated financial service needs, which span various product markets, but may not have the time or knowledge to manage their own finances.

Judging from the recent rhetoric about the need for better customer focus and improved relationship management, banks seem to recognize the importance of integrating quality into their service delivery. In practice, however, most banks continue to focus on reducing labor costs and competing on price. Only a small minority have invested sufficiently in their human resources to support product strategies based on customization and integrated service delivery.

We argue that the failure of more banks to integrate quality into their competitive strategies cannot be explained simply in terms of management decision making, but must be understood in the context of a labor market environment that discourages managers from investing in human resources.5 As in other industries, the low level of educational and vocational attainment among high school graduates means that they come to banks ill prepared for complex job tasks. The mobility of skilled labor also makes it difficult for banks to invest in training and to design services on the assumption of long employment tenures. Both aspects of the U.S. labor market have made it easier for banks to react to higher levels of competitive pressure by emphasizing price competition and standardization, e.g., “commodization,” rather than by adding value.

We suggest two types of human resource and organizational innovations to overcome a low-skill environment and shift to a high-quality service strategy. First, banks can increase skill levels and reduce turnover by creating a new employment contract that emphasizes competence-based career ladders for entry-level employees, modular training for high-skill positions, and higher levels of internal recruitment. Second, banks can lower their training costs and raise the skill level of new recruits through educational partnerships with community colleges and four-year universities. By making completion of certain courses a hiring criterion, banks can get employees and the government to pay for initial general skills training.

This article is based on thirty interviews with branch managers and senior executives at a dozen different banking institutions.6 We also gathered evidence on human resource developments and market trends in the banking industry from industry consultants, bank employers’ organizations, and a review of the relevant literature. While our discussion centers on banks, we believe that our analysis of a low-skill environment’s effects on service firms’ human resource decision making and our suggested remedies have broad applicability.

Banking: An Industry in Transition

These interdependent market trends have led to profound changes in the U.S. banking industry. First, regulatory and market changes have led to increased competition among suppliers of financial service products. The loosening of regulatory restrictions on depository institutions has allowed thrift institutions and commercial banks to expand their range of standard banking services and, in many states, to enter markets for investment and insurance products. Advances in information and communication technology have enabled finance companies, insurance dealers, and other nonbanking firms to enter the retail banking market without branch office networks. Firms like Sears and Ford Motor Company now provide consumer credit, while other traditional one-product companies such as AA Insurance and American Express sell deposit products, checking services, and credit cards.

Second, there has been a shift in consumer demand patterns. Consumers are using some retail products more intensively while also expanding into investment and insurance products. Between 1980 and 1992, deposits as a percentage of personal assets dropped by 10 percent, while investments in mutual funds, money market funds, and government bonds increased by 10 percent and holdings in life insurance by 6 percent.7 Meanwhile, bank loans for personal consumption expanded rapidly during the 1980s, as more individuals took on debt to finance their education, mortgages, and purchases of consumer durables. The interest in and need for help with international financial opportunities also increased as high-end retail consumers invested in international markets, and an increasing number of small- and medium-sized enterprises expanded into overseas markets.8

Third, there has been a trend toward financial disintermediation. As large firms have turned to bond and commercial paper markets to meet their short-and long-term financing needs, diversified commercial banks have competed over lending opportunities to small and medium-sized enterprises.9 Maintaining market share in the middle and low end of the wholesale segment has been complicated by the increasing market presence of venture capital firms and small independent wholesale banks. Both types of institutions have attempted to carve out a market niche by working more flexibly with start-up firms or specializing in particular economic sectors.

Banks’ Competitive Responses

A few banks have responded to these market trends by raising the quality of their service. Two very different banks, Citibank and California Federal Bank, a Los Angeles-based federal savings bank, reacted to consumers’ increasing sophistication with banking strategies aimed at relationship management. Both firms quickly took advantage of loosened restrictions on banks’ involvement in insurance and investment products and the growing demand for consumer credit products to create a financial manager position in their branch offices.

In 1993, Citibank began to train some of its platform employees in deposit, investment, and consumer credit products so they could act as financial advisers for high-end clients. By increasing and sharing information among different areas, Citibank hopes to raise the quality and convenience of financial service delivery to its wealthy private customers. Like Citibank, California Federal Bank has integrated investment services directly into its branch operations, training new account employees to deliver insurance, mutual funds, and progressively more complex investment products. CalFed began a program in 1994 to have its branch-based financial managers develop comprehensive financial plans spanning deposit, investment, and insurance products for its retail clients.

First Federal Bank, a southern California-based federal savings bank, has taken the relationship banking strategy a step farther. To support its niche market strategy of targeting more conservative banking customers, the bank puts a premium on service quality and employee stability. The bank expects tellers and new-account officers to use long-term relationships with clients to cross-sell deposit, consumer credit, and simple investment products. One First Federal executive summed up the bank’s business philosophy, “Knowing customers personally and being familiar with their individual financial needs is a source of competitive advantage. . . . It facilitates customizing products and makes it more difficult for customers to leave the bank.”

In the wholesale segment, while other banks neglect small business customers to focus on large corporate clients, Harris Bank of Chicago has formed a special lending group that focuses on building long-term relationships with firms that have $5 million to $100 million in annual sales. Rather than maximize short-term profits by extending revolving credits, according to a senior executive for commercial lending, the bank’s goal is “to serve its clients’ needs over the life cycle of the company.” The bank has made it a priority to develop a stable group of relationship managers who have a working knowledge of their clients and their clients’ industries.

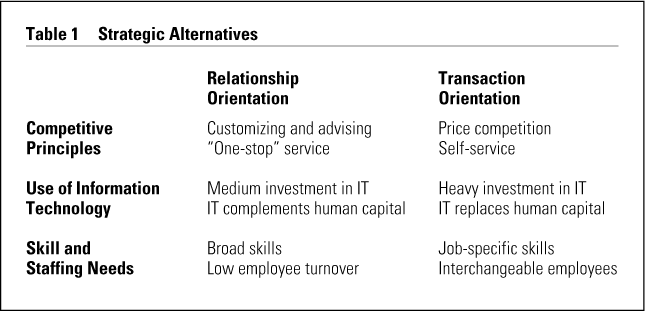

What all these banks have in common is that they are using a relationship model of service delivery to gain competitive advantage (see Table 1). The increasing array of financial products in both the wholesale and retail segments creates a market opportunity for those banking institutions that can use skilled bank employees to minimize customers’ time and cost of navigating through the complex finance world. By allowing a single, broadly skilled employee to attend to all the needs of individual customers, these banks can promise quick, convenient, and customized service delivery.10

{kind=link}

The “Drive toward Commodization”11

By increasing the quality of their service delivery to respond to increased competition, the banks described above are an exception. Most U.S. banks have answered the intensified competition in financial services by adopting a transaction-oriented banking paradigm (see Table 1). Rather than attempting to use their branch offices to cultivate strong customer relationships, most banks have tried to outcompete each other and other financial service firms on price and convenience.

· Retail Banking.

In the retail segment, banks’ primary competitive response to increased competition is to intensify price competition and emphasize the development of new banking products. By frequently changing fee schedules and interest rate returns or by offering special giveaways (e.g., air miles, prize drawings), banks have maintained a fairly high pace of innovation in their product offerings. They use monthly or quarterly product campaigns to undercut competitors and attract price-conscious consumers.

Another strategy to win new business is a redoubled emphasis on convenience in providing service. Investment in automatic teller machines (ATMs) increased steadily during the 1980s, with the number of ATMs growing from 205 per million residents in 1983 to 340 by 1991.12 Open hours on weekends and in the early evenings, promises of short lines, twenty-four-hour telephone banking, and electronic banking have also entered the competitive fray. Bank of America’s recently launched “I can banking” business campaign is typical. It promises an ATM “on every corner,” quickly approved consumer loans, and the ability to conduct much banking business over the telephone.

The drive to reduce costs and increase investment in information technology has been accompanied by a wave of mergers and acquisitions. Between the mid-1980s and mid-1990s, the number of U.S. banks shrank by almost one-quarter from 14,000 to 11,000, and most experts predict continued rapid consolidation.13 Consolidations have been driven in part by the attempt to overcome the inefficiencies created by erstwhile regulatory restrictions on interstate banking. More recently, the drive toward consolidation has been reinforced by the need for higher levels of investment in information technology. The shift toward nonbranch distribution channels and demands for continued cost cutting in administrative areas have made high levels of investment in information technology imperative.

As they have shifted toward transaction-oriented banking strategies, most banks have used human resource policies to generate cost savings rather than to build a skilled, stable workforce. As our research and other industry studies indicate, most banks spend little on training frontline employees and keep work processes highly segmented.14 Tellers perform a limited range of tasks such as taking payments, cashing checks, and checking account balances. Banks frequently subcontract investment services to independent consultants outside the branch offices. The fragmented structure of service delivery allows banks to save on costs by keeping training short and functionally oriented.

Banks have also saved money by shifting from a full-time to a part-time labor force. Across the banking industry, the percentage of tellers working on a part-time basis went from near zero in the mid-1980s to 60 percent by the early 1990s.15 Some large commercial banks are now making the new-accounts positions part-time as well. In a number of banks we visited, part-timers accounted for nearly three-quarters of the branch labor force.

Another strategy to help minimize training costs is the shift to outside recruitment for high-skill branch positions. Our company interviews suggest that while 80 percent of branch managers are promoted from within, half the consumer credit officers and 80 percent of investment advisers are recruited from outside. Of these three positions, only the branch manager can learn most of the required skills on the job. Both consumer credit and investment advising require considerable extra product and technical training.

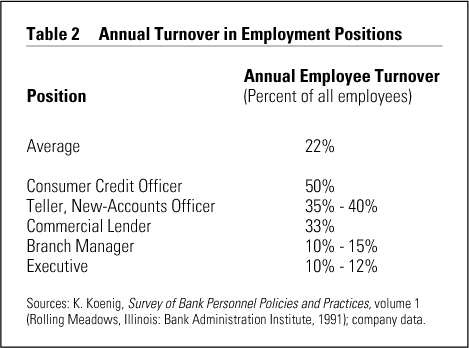

Low investment in human resources has helped banks generate cost savings but has also resulted in high employee turnover. Part-time employees unlikely to move up make less committed employees because they are either constantly searching for a full-time job or have other priorities, e.g., studies or parenting. Similarly, mid-career specialists who have been poached from a rival have little loyalty to their employers. Annual turnover in the banking industry ranges from an average of 35 percent to 40 percent in the teller and new-accounts positions to as high as 50 percent among consumer credit officers (see Table 2).

{kind=link}

Because of their commitment to a transaction-based banking paradigm, bank executives have not been concerned with employee turnover. They expect customers to be attracted to a bank by promises of price reductions and service convenience, not by integrated, high-quality service. One branch manager said that executives in her bank had a “warm body” philosophy of human resource management — they were concerned with having enough employees to fill branch-level positions but did not particularly care who these employees were.

· Wholesale Banking.

In wholesale banking, the shift toward transaction-based banking has been clearest in the small business segment, which is made up of professionals, owners of small retail shops, and artisans, e.g., plumbers or carpenters. Traditionally, these customers have been treated as a special category, with many branch managers acting as relationship managers.

During the past decade, many large banks have tended to strip small business clients of their special status and ask them to develop their investment and deposit services through the same channels as normal private customers. For many banks, evaluation of small business loan applications, just like evaluations of credit cards, has become a centralized, back-office affair. Employees who have no contact with the small business client and no knowledge of his or her business’s particular circumstances evaluate the applications with the aid of a computer risk-assessment program.

In the middle-market segment, many bank managers we interviewed claimed to be moving toward a relationship management strategy, recognizing it as a market segment rich with possibilities for cross-selling products. The typical middle-market firm is a small-or medium-sized manufacturer with between $5 million and $250 million in annual sales. This size firm not only has the credit and deposit needs of a small business enterprise but also requires additional sophisticated investment advising, cash management services, access to other electronic banking products, and, increasingly, international banking services.

Despite this rhetorical commitment to relationship banking, the way banks develop business with their middle-market clients is often characterized more by transaction- than relationship-based thinking. Rather than working with a small- and medium-sized firm over the long term, many commercial banks want to avoid risk and earn what they can from short-term deals. A disproportionate amount of capital offered to clients is in the form of either revolving lines of credit or loans with short-term maturity dates. Estimates suggest that no more than 20 percent to 25 percent of the credit that large commercial banks offer has a term date of three years or longer.16 Commercial banks use short-term loans to pursue procyclical lending. In times of prosperity, when they have excess capital, banks are very generous in their interest offerings. In recessions, they curtail their lending operations severely.17

The transaction-driven strategy also reveals itself in the heavy emphasis that commercial lenders place on acquiring rather than cultivating customers. Our interviews suggest that the typical relationship manager spends at least half his or her time trying to find new clients, an emphasis that reduces the time available for generating new business with existing clients. According to one study, in some banks, the percentage of time commercial lenders spend on customer cultivation may be as low as 20 percent.18

At many large commercial banks where we conducted interviews, two or three individuals per lending group have sole responsibility for soliciting new business. They either follow up on referrals or simply call potential customers, which alone accounts for as much as 65 percent to 70 percent of the new business generated. Efforts to win new customers normally revolve around promises of lower interest rates on loans and lower prices on related financial service products. Price competition among banks is often so intense that the margins earned on loans become razor thin.19

Business Strategies and Economic Outcomes

In some customer segments, the transaction-oriented approach to banking makes clear strategic sense. According to bank executives, large corporations are extremely price sensitive and will play one bank against another to get the lowest possible offer on credit and noncredit products. The large corporate customer has the financial expertise to conduct cash management, investments, and international banking operations and thus expects simple, efficient services from its bank(s). At the low end of the retail banking market, there are customers with relatively unsophisticated financial service needs and low profit potential who are price sensitive and use only minimal bank services.

Banks operating in these more standardized markets need to radically rethink their cost and delivery structures to remain competitive on price with the growing number of nonbank alternatives. They need to dismantle their cost-intensive branch structures, make maximum use of information technology, and figure how to minimize use of human resources in service delivery.

Between these highly price-competitive segments of the banking market, however, there are a large number of customers who need and value a more intensive relationship with their bank. These include small business owners who need help in managing both their private and business finances, middle-sized business owners who want not just bank credit but also a banker with knowledge of their market and industry, retirees who must achieve the appropriate balance between liquidity and investment, and young professionals who need a strategy to pay off student loans while also beginning to invest for their children’s education and their own retirement.

Innovative banks have used a relationship management strategy to generate competitive advantage with customers like these. First Federal’s focus on cross-selling to existing clients rather than on more general product promotions helped the bank significantly reduce single-service clients and increase account retention. In 1995, the number of single-service clients fell by 11 percent, with a corresponding 58 percent increase in account-retention rate. Harris Bank’s strategy of developing in-depth knowledge of its customers and their industries has led to a customer-retention rate well above the industry average. In a market segment in which many customers switch banks every three to five years, Harris Bank has used its intensive relationship management strategy to achieve twenty-year relationships, on average, with its middle-market clients.

CalFed’s strategy of creating comprehensive financial plans for its clients has also supported its efforts to cross-sell customers. Of the customers who participated in the 1994 rollout of the comprehensive financial plan program, 75 percent moved accounts from other banks to consolidate their retail banking products with CalFed. One year after launching its relationship management program for high-end clients, Citibank was able to significantly increase the number of high-end accounts under management and the revenue generated per account.

The failure of more banks to adopt relationship-oriented business strategies in the market segments for high-end retail customers and small- and medium-sized customers has been an important cause of banks’ falling market share in the financial services markets.20 For the retail banking consumer, each new financial account opened with a bank brings new search and information costs. A customer moving from a deposit account to an investment or insurance product will have to deal with a different bank employee and may need to go to a different location. The fragmentation of banks’ service delivery makes it easier for lower-cost, single-service financial service providers to entice customers away.

In commercial lending operations, the shift toward short-term, acquisition-oriented business strategies has harmed banks’ competitive prospects. Given the choice among a bank loan, direct access to capital markets, or raising funds privately, any size firm naturally prefers one of the latter two options. Issuing bonds and equities directly in capital markets or raising funds from private sources not only reduces the capital costs but also minimizes outside interference in internal business decision making. A bank loan becomes more attractive only if it suggests stable funding — even through difficult economic times — and comes with customized service and financial advice.21

As large, diversified commercial banks turned toward standardization and automation, an increasing number of middle-market firms turned to directly accessing capital markets, to venture capital firms, and to independent wholesalers.22 Many small firms have also exited the banking system, choosing to raise funds privately rather than rely on lending from banks. With banker’s adding less value to their business operations, there has been less incentive for small- and medium-sized enterprises to raise funds within the banking system.

A Low-Skill Environment

If market trends support a shift toward relationship management in banks’ key market segments, why have most banks moved toward the transaction-based paradigm? As we noted earlier, conventional explanations for the failure of more service-sector firms to integrate quality and customization into their business strategies have focused on the shortcomings of managerial decision making. What the conventional view misses, however, is that the trend toward commodization of services is a function not simply of management decision making but of the interaction between that decision making and institutional constraints. U.S. banks have found it difficult to generate a skilled, stable labor force because of institutional barriers in the labor market where they operate.

· Poor Vocational Skills.

There are few mechanisms to prepare young people for careers in banking. Entry-level hires typically know little about financial services, have no previous experience working in a bank, and, in many cases, lack a sound educational foundation.23 “It is not just that their basic skills in reading, writing, and arithmetic are lacking,” said one human resource manager, “but we also have problems finding good social skills and proper manners.” Several human resource executives we interviewed noted a steady decline in the quality of applicants for entry-level branch positions. In response, Citibank has petitioned several state governments to absorb some of the costs of training individuals who lack sufficient basic skills.

Even in the case of more highly skilled positions, managers complain that what new recruits learn in the university is far removed from the work world. As the manager of one commercial lending group noted, “We can get accounting majors in here who don’t know how to decipher an annual report for a real company.” The poor vocational preparation of young people at all levels encourages banks to design their product strategies around low skills rather than make the considerable training investment to support high-quality, integrated service delivery.

· Problems of Poaching.

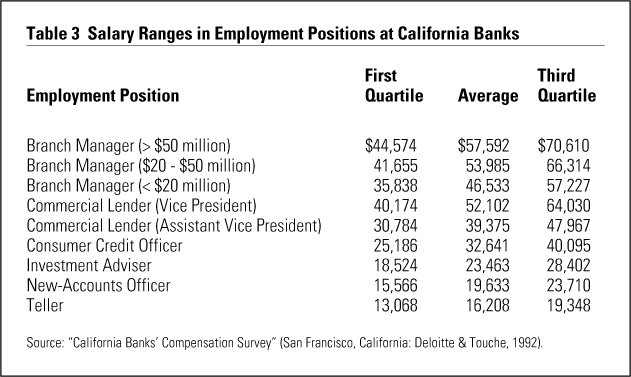

A second barrier to achieving relationship-oriented banking strategies is poaching. As in most U.S. service sectors, collective wage agreements play no role in wage determination in banking. Each bank sets its compensation policies and practices independently. The lack of coordination in wage setting gives banks more freedom to adjust and react to economic change, but also leads to high mobility among skilled employees. Differences of 40 percent to 50 percent in employee compensation for the same job in different banks in the same local economy are common (see Table 3).

{kind=link}

These differentials allow banks to attract skilled employees from other banks by offering wage premiums. As the manager of one bank’s mortgage lending group said, “In a bad business year, turnover is pretty manageable, but, in a good year, our lenders leave in droves to go to competitors offering more money.” In the wholesale lending segment, executive search agencies contribute to rapid turnover, with middle-market lenders reporting constant calls from headhunters. The result is a high turnover rate among commercial lenders; interviews at the banks we studied suggest that the turnover rate is about 33 percent annually.

Poaching creates strong disincentives for firms to invest in training. The failure by a consortium of the largest New York banks to create a program — modeled on the German dual system of apprenticeships — to comprehensively train young people in retail banking skills illustrates the problem. The banks established the program in the mid-1980s to help develop qualified individuals for their branch offices. It had a brief life, however, because high turnover among the trainees made it impossible for the banks to recover their investment of time and resources. More than 80 percent of trainees left their firm within a year or two, often to another New York-based financial service firm that was not in the program.

Poaching has also made it difficult for banks to operate training programs for their commercial lenders. A comprehensive commercial lender course lasts about a year and can cost a bank $50,000 or more. Most banks prefer to train their commercial lenders internally to instill their own lending culture but often end up recruiting for these positions among competitors. Commercial lenders emerge from the training course with very marketable skills without becoming strongly attached to their training bank, which means a competitor can easily entice them away with higher wages.

Several banks where we conducted interviews had recently reduced or ended their lender training programs altogether because of the poaching problem. One Japanese bank had launched a major training program in its effort to penetrate the wholesale lending market in Los Angeles during the late 1980s. After losing eighteen of twenty-one graduates the first year and nineteen of twenty the second year, the bank ended the program and soon became one of the most aggressive poachers in the Los Angeles area.

The cycle of poaching and counterpoaching not only discourages training investment but also undermines attempts to build strong client relationships. High turnover among commercial lenders or branch-based investment advisers makes it difficult to create the trust and mutual understanding necessary for relationship banking. As a result, banks often find that their best competitive option is to earn profits on short-term business relationships.

Beating the Low-Skill Environment

More banks are realizing that, in a highly competitive financial services market, focusing solely on price and transaction volume may not be the best way to remain competitive. Chase Manhattan Bank is facilitating cross-selling by leveraging information among product groups.24 Bank of America and Wells Fargo are both trying to advance into community lending by working flexibly with small business owners.25 However, achieving the shift to a relationship-banking strategy will work only if banks restructure their human resource policies by considering two possible innovations:

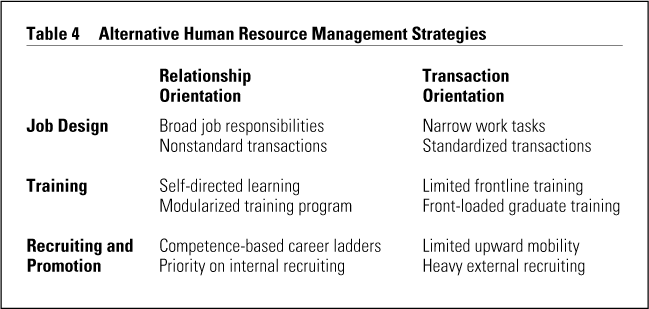

- Create a new employment contract to motivate, develop, and retain high-performing employees. This new contract has three elements: competence-based career ladders for entry-level employees, modular training for high-skill positions, and higher levels of internal recruitment in all positions (see Table 4).

- Work with educational providers to develop courses that ensure higher skills among entry-level recruits.

{kind=link}

A New Employment Contract

If banks are to succeed at a relationship-driven strategy, they need employees with multiple competencies who are able to actively solve customers’ problems. The new contract requires a bargain between employer and employee in which banks offer continual opportunities to develop and use new skills related to career advancement in lieu of employment security. With layoffs spreading throughout the industry, the banks that offer opportunities for continual skill development become relatively more attractive employers. One human resource executive described the new contract between employee and employer, “We can’t promise lifetime employment, but we can give employees the resources they need to take control of their own careers.”

· Competence-Based Career Ladders.

The first part of the contract is to broaden front-line employees’ responsibilities and improve their opportunities and incentives for learning skills. Banks with a transaction-oriented strategy have assumed low skills and high turnover as a given and sought to build service strategies around narrow jobs filled by interchangeable employees.

In contrast, both Citibank and First Federal have sought to align their human resource practices by focusing on customer relationships. They have constructed competence-based reward and promotion systems to broaden the skills of branch employees and to lower staff turnover. As in other banks, entry-level recruits receive short introductory training to prepare them for their immediate job tasks. But, in addition, motivated employees can enroll in ongoing training modules to prepare for upward advancement. Individual employees decide whether to participate in the training classes, but the banks try to show clearly how the training courses link to advancement opportunities in different branch positions. As one Citibank executive said, “It’s up to the employees to take the initiative in developing these skills, but the bank has an interest in helping employees make more informed choices.”

· Modularized Training for High-Skill Positions.

Another part of the contract is to create modularized training for high-skill positions. If the problem for lower-level bank employees has been too little training and career development, the reverse has been the case for graduate training programs, which often require heavy up-front investment and lengthy, unproductive classroom time. In an environment with high levels of poaching, this type of training program is generally not cost effective because new recruits become easy prey for competitors.

An alternative training method for high-skill positions is to alternate skill development with work experience. As they have moved to bring investment and insurance products into their branch offices, both Citibank and CalFed have adopted a modularized training program for their highly skilled branch employees. Rather than spend several months in the classroom, Citibank’s banking officers have a few weeks of introductory training on products and services, followed by training courses that cover investment and consumer credit products as needed. Personal banking officers at CalFed can enroll in one course after another to earn the licenses needed to sell progressively more sophisticated investment products. After completing courses on money market funds and life and disability insurance, personal bankers spend several months at work before taking classes on mutual funds and annuities. They then return to work before taking courses to become certified brokers.

The modularized training programs in each bank are geared implicitly to individuals with longer employment tenures. The longer an employee works for a firm, the more skills he or she acquires. This approach to training has two advantages for banks. Employees do not spend unproductive time in classes learning skills that they do not immediately need. Moreover, modularized training helps mitigate against poaching because employees increase their skills while developing a strong attachment to their employer.

· Priority on Internal Promotion.

A third essential element of the new employment contract is a shift toward more internal promotion. As a natural response to the difficulties they have experienced retaining their own trainees, most banks have relied heavily on external recruiting for high-skill positions, an imperfect solution. Existing employees see their chances for upward mobility blocked and look to the outside labor market for opportunities.

Innovative banks such as CalFed, Harris Bank, Citibank, and First Federal have a different approach to recruiting and promotion. As an extension of their commitment to stronger career paths, all four banks rely on internal recruitment for high-skill positions. While they do not promise their employees job security, they have committed to meeting their hiring needs internally, exploring the external labor market only when there are no qualified individuals within their own organizations. CalFed and Citibank both recruit nearly 60 percent of their branch-based investment advisers from among their own new-accounts personnel, while 70 percent of First Federal’s supervisors and personal financial officers started as tellers. Likewise, to fill its commercial lender positions, Harris Bank draws almost exclusively from its pool of credit analysts rather than recruiting MBAs or a competitor’s lending officers. To allow its credit analysts to build their knowledge of business and market dynamics, it sends them back to school to earn MBAs while they continue to work for the bank.

Stronger internal labor markets support the shift to a relationship banking strategy in two ways. First, employees in high-skill positions learn about the bank, its products, and its customers. Second, stronger internal labor markets help reduce turnover. Clear opportunities for upward mobility encourages employees, even those in the part-time branch-level positions, to remain with their present employer. Internal placement also means that banks promote individuals who have demonstrated a commitment to their present employer. This strategy helped First Federal Bank to reduce its employee turnover to 7 percent or one-fifth the market average. By developing a strong internal labor market for high-skill positions, Harris Bank kept commercial lender turnover under 10 percent annually or less than one-third the industry average.

Cooperation with Education Providers

In addition to restructuring internal human resource policies, a second, complementary innovation for achieving a relationship-based strategy is to form cooperative arrangements with local education providers. The basic product knowledge and technical skills that banks require of their new employees are common to the whole banking industry. All commercial lenders need to learn about finance and accounting, credit and risk analysis, and industry structure. Similarly, retail employees in all banks learn about the same basic deposit, checking, investment, and credit products. One branch manager we interviewed noted, “The core products that employees must learn are the same from one bank to the next. . . . Banks compete not by changing the products but by changing interest returns.” The prevalence of poaching provides additional evidence of banks’ common skill requirements; the skills learned in one bank are often easily transferable to another.

The generic nature of many skills creates the potential for mutually beneficial cooperation between banks and two- and four-year colleges. Partnerships with banks can help educational providers better prepare their students for employment in a volatile labor market. Given the restructuring in the financial services market, new labor market entrants need skills they can transfer from one financial service firm to the next. Because a number of banks hire college students part-time while they complete their studies, the education-bank partnerships could take the extra step of linking work experience more directly with course content, as cooperative education programs do in other economic sectors.26

By working with two- and four-year colleges to prepare students for a career, banks can externalize much of the cost of general skill development. Banks with a relationship management strategy need employees with broad, general skills, but, given the problem of poaching, they cannot afford to develop these skills at their own cost. By encouraging colleges to develop courses directed at the financial service industry that include cases on applied finance, risk analysis, investment strategies, and other technical subjects, and then making course completion a condition of hire, banks can fill their high-skill positions in both retail and wholesale banking at a much reduced initial training cost. Banks will need to provide training only on bank-specific products and procedures to complement the general skills learned at school.

A bank that has established a cooperative training course has no guarantee that those completing the course will apply for employment. As with the training courses that banks run internally, many graduates will go on to other financial service firms. The main advantage of the educational cooperative is that the school, the students, and their parents will pay for most of the costs of initial training. Banks will not need to pay trainees’ salaries while they are enrolled in classroom training. The student or his or her parents will pay for living expenses. The schools will pay for instructors’ costs and most course development. The banks’ only expense is the time that its human resource personnel spend working with schools to align course content with business needs.

Educational providers have been quick to realize the potential benefits of this cooperation. Recognizing the need to help their students generate broad, general skills, schools and colleges in San Francisco, Los Angeles, Chicago, and New York have attempted to set up courses targeted at the financial services industry. The main barrier to making such cooperatives work has been the banks themselves. Our interviews suggest that banks, even more innovative banks, have failed to move beyond their traditional arm’s-length relationship with educational providers. By taking this hands-off approach, banks have missed a tremendous opportunity to improve the overall skill levels of their new recruits cost effectively.

Conclusion

From retail businesses to insurance and hotels, U.S. service firms are trying and often failing to tailor their services more closely to customer needs. As we have suggested, much of the explanation for this failure stems from the interactions between managerial decision making and the institutional environment. The constraints of the U.S. labor market make it easier for service managers to focus on cutting costs than on adding value. Both the poor skills of young people and the endemic problem of poaching make it difficult to base competitive strategies on customized, integrated service delivery.

Banks and other service providers, however, can overcome these constraints by reforming their human resource policies and practices. By working with educational providers to smooth the school-to-work transition, firms will realize higher skill levels in the labor force at a lower cost. And a new employment contract that features stronger career paths in all positions, modularized training programs, and more internal recruiting will encourage broader skill formation and lower employee turnover. Together, these innovative human resource practices can make it much easier for services to meet the emerging quality demands of their customers.

References

1. B. Pine, D. Peppers, and M. Rogers, “Do You Want to Keep Your Customers Forever?,” Harvard Business Review, volume 73, March–April 1995, pp. 103–114.

2. N. Venkatraman, “IT-Embedded Business Transformation: From Automation to Business Scope Redefinition,” Sloan Management Review, volume 35, Winter 1994, pp. 76–77;

F. Reichheld, “Loyalty-Based Management,” Harvard Business Review, volume 71, September–October 1993, pp. 64–73; and

T. Raffio, “Quality and Delta Dental Plan of Massachusetts,” Sloan Management Review, volume 33, Fall 1992, pp. 101–110.

3. L. Schlesinger and J. Heskett, “The Service-Driven Service Company,” Harvard Business Review, volume 69, September–October 1991, pp. 71–81; and

L. Waldstein, Service Sector Wages, Productivity, and Job Creation in the United States and Other Countries (Washington, D.C.: Economic Policy Institute, 1989), pp. 24–25.

4. L. Schlesinger and J. Heskett, “Breaking the Cycle of Failure in Services,” Sloan Management Review, volume 33, Spring 1991, pp. 17–27; and

J. Pfeffer, Competitive Advantage through People (Boston: Harvard Business School Press, 1994).

5. D. Finegold, “Institutional Incentives and Skill Creation: Preconditions for a High-Skill Equilibrium,” in P. Ryan, ed., International Comparisons of Vocational Education and Training for Intermediate Skills (London: Palmer, 1991).

6. Five of these banking institutions were full-service commercial banks, four were federal savings banks, and three were independent wholesalers.

7. For all data on private holdings, see:

“Flow of Funds Accounts—Assets and Liabilities of Households: 1980 to 1992,”Statistical Abstract of the United States (Washington D.C.: U.S. Department of Commerce, 1992), p. 506.

8. “America’s Little Fellows Surge Ahead,” The Economist, 3 July 1993, pp. 59–60;

A. Barrett, “It’s a Small Business World,” Business Week, 17 April 1995, pp. 96–101; and

W. Glasgall, “The Global Investor,” Business Week, 11 October 1993, pp. 54–59.

9. L. Mayne, “How Big Banks Nurture Relationship Banking in the Middle Market,” Journal of Commercial Bank Lending, volume 72, October 1989, p. 23.

10. T. Davenport and N. Nohria, “Case Management and the Integration of Labor,” Sloan Management Review, volume 35, Winter 1994, pp. 11–21.

11. This phrase came from a conversation with Jeffrey Pfeffer.

12. B. Keltner, “Comparative Patterns of Adjustment in the U.S. and German Banking Industries: An Institutional Explanation” (Stanford, California: Stanford University, unpublished dissertation, 1994), Table 3.1.

{kind=link}

13. “American Banking: Roped Together,” The Economist, 28 October 1995, p. 92; and

R. Hylton, “Merger Mania and Fat Profits Make the Big Banks Look Good,” Fortune, 7 August 1995, pp. 259–261.

14. Of the nine thrifts and full-service banks in our study, only two of eight had cross-trained tellers into new accounts, only two of eight were integrating the new accounts and investment banking services at the branch level, and only one of the eight was attempting to offer integrated delivery of all retail products in their branches offices. In another study of branch level work organization, Chip Hunter found a similar pattern of fragmentation in service delivery. See:

C. Hunter, “How Will Competition Change Human Resource Management in Retail Banking? A Strategic Perspective” (Philadelphia, Pennsylvania: The Wharton Financial Institutions Center, working paper #95-04, February 1995).

15. Bureau of Labor Statistics, “Public Use Microsamples of the Census, 1980 and 1990” (Washington, D.C.: Bureau of the Census, 1993); own calculations.

16. S. Vitols, “Banks and Industrial Finance in Germany and the U.S.: An Organizational Perspective on Long-Term Lending” (Wissenschaftszentrum, Berlin: Institutions of Advanced Capitalism, paper presented at conference, March 1994).

17. “Take Our Money, Please,” Business Week, 18 July 1994, pp. 66–67.

18. Vitols (1994).

19. “When to Throw ’em Back,” The Economist, 12 March 1994, pp. 81–82.

20. B. Keltner, “Relationship Banking and Competitive Advantage: Evidence from the U.S. and Germany,” California Management Review, volume 37, Summer 1995, pp. 45–72.

21. J.C. Svare, “Forging Profitable Relationships,” Bank Administration, volume 65, November 1989, pp 14–24; and

J. Kotkin, “The New Small Business Bankers,” Inc., May 1984, pp. 112–125.

22. “A Survey of International Banking,” The Economist, 30 April 1994, p. 9;

E. Sipple, “When Change and Continuity Collide: Capitalizing on Strategic Gridlock in the Financial Services,” California Management Review, volume 31, Spring 1989, pp. 51–74.

23. J. Hargroves, “The Basic Skills Crisis,” The New England Economic Review, 1 September 1989, pp. 56–58; and

P. Lunt, “Entry-Level Workers Get Extra Help,” ABA Banking Journal, volume 82, June 1990, pp. 37–39.

24. K. Holland, “A Chastened Chase,” Business Week, 26 September 1994, pp. 106–109.

25. V. Torres, “Taking Account of the Little Guys,” Los Angeles Times, 27 March 1995, pp. D1–D2.

26. W. Grubb, T. Dickinson, L. Giordano, and G. Kaplan, “Betwixt and Between: Education, Skills, and Employment in Sub-Baccalaureate Labor Markets” (Berkeley, California: University of California at Berkeley, National Center for Research in Vocational Education, December 1992).