A Dynamic View of Strategy

Topics

In late 1988, the newly appointed CEO of the Nestlé subsidiary, Nespresso, was trying to decide how to rejuvenate his subsidiary’s financial fortunes. Jean-Paul Gaillard had just taken over a subsidiary that, despite selling one of Nestlé’s most innovative new products, was facing serious financial problems.

The Nespresso product was a system that allowed the consumer to produce a fresh cup of espresso coffee at home. Though simple in appearance and use, it took Nestlé more than ten years to develop it. The system consisted of two parts: a coffee capsule and a machine. The coffee capsule was hermetically sealed in aluminum and contained five grams of ground roast coffee. The machine consisted of a handle, a water container, a pump, and an electrical heating system. These four parts were cast into a body to form the machine.

The use of the Nespresso system was straightforward. The coffee capsule was placed in the handle, which was then inserted into the machine. The act of inserting the handle into the machine pierced the coffee capsule at the top. At the press of a button, pressurized hot water passed through the capsule. The result was a creamy, foamy, high-quality cup of espresso.

The new product was introduced in 1986. Nestlé’s original strategy was to set up a joint venture with a Swiss-based distributor, called Sobal, to sell the new product. This joint venture (named Sobal-Nespresso) would purchase the machines from another Swiss company (called Turmix) and the coffee capsules from Nestlé, after which it would distribute and sell everything as a system — one product, one price. Offices and restaurants were targeted as the customers and a separate unit called Nespresso S.A. was set up within Nestlé to support the joint venture and to service and maintain the machines.

By 1988, it was clear that the new product was not living up to its promise. Sales were well below budget, and costs were escalating due to quality problems. Nestlé executives were considering halting the operation when Jean-Paul Gaillard was chosen to decide whether and how to strategically reposition the subsidiary. At the top of Gaillard’s list were questions such as:

- Should Nespresso continue targeting offices and restaurants as customers or focus on upper-income households and individuals?

- Should Nespresso continue focusing activities in Switzerland or expand into other espresso-friendly countries?

- Should Nespresso adhere to its strategy of selling the coffee and machines as a system or concentrate solely on coffee?

- Did Nespresso’s distribution policy make sense or should the company choose an alternative distribution method, such as mail order?

The Heart and Soul of Strategy

The answers to these questions were not immediately obvious and several possible alternatives were put forward. Debates and disagreements ensued. Yet, out of this debate and uncertainty, specific choices were made and specific decisions implemented. In fact, this process of asking questions, generating alternatives, and making choices that may prove to be the wrong ones is what strategy is all about.

This is because, in every industry, there are several viable positions that companies can occupy. Therefore, the essence of strategy is selecting one position that a company can claim as its own. A strategic position is simply the sum of a company’s answers to the following questions:

- Who should the company target as customers?

- What products or services should the company offer the targeted customers?

- How can the company do this efficiently?1

Strategy involves making tough choices on three dimensions: which customers to focus on, which products to offer, and which activities to perform. Strategy entails choosing, and a company will be successful if it chooses a distinctive strategic position that differs from those of its competitors. The most common source of strategic failure is the inability to make clear and explicit choices on these three dimensions.

As it turned out, Jean-Paul Gaillard chose correctly for Nespresso — whether by luck or foresight. Nespresso targeted high-income households as its main customer and chose mail order (the “Nespresso Club”) for distributing the coffee capsules. As a result of these choices and other strategic decisions, Nespresso grew tremendously during the next five years. The main point of the Nespresso story is simple: the heart and soul of strategy is asking the “who-what-how” questions, developing alternatives, and selecting specific goals and actions.

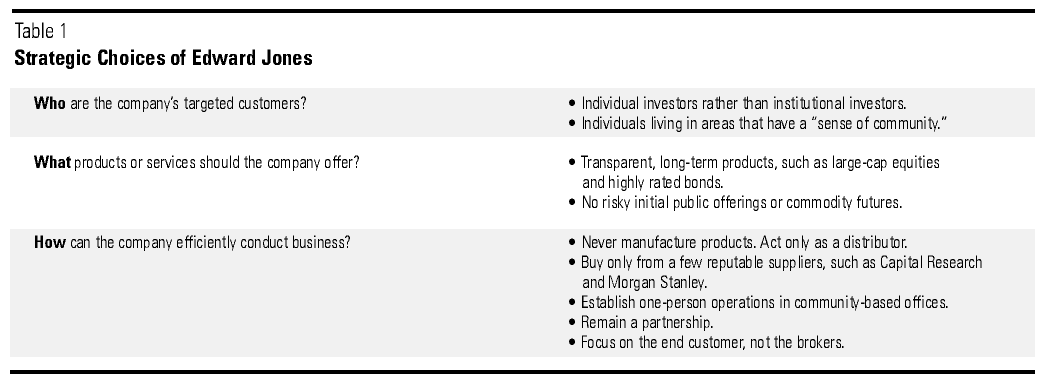

To substantiate this point further, consider the example of Edward Jones. With 1997 revenues of $1.1 billion, the St. Louis, Missouri-based partnership of Edward Jones is the thirty-fourth largest brokerage firm in the United States. However, the firm is one of the most profitable in the volatile securities industry and is growing rapidly. Since 1981, it has expanded its broker force 15 percent annually without making any acquisitions. It now boasts more than 2,500 partners — up from a 1981 count of eight.

As described by many outside observers including management guru Peter Drucker, the firm is a federation of highly autonomous entrepreneurial units bound by a strong set of values and beliefs. The entrepreneurial units are Edward Jones brokers, who are scattered across the United States. They operate out of one-person offices located in small communities, selling selected financial products to people living in their communities. They are united by the strong cultural belief that their job is to offer sound, long-term financial advice to their customers, even if that does not generate short-term fees. The “customer-first” value is ingrained in every broker working in the Jones system.

It wasn’t always like this. During the past fifty years, the firm passed through three evolutionary stages. It was originally set up by Edward Jones, Sr., to be a financial department store able to satisfy all the financial needs of a customer. In the 1960s, the department store concept slowly evolved into a “delivery system” for the rural areas of the United States, as a result of Ted Jones (the owner’s son) setting up small offices in rural communities and expanding the firm into a network of 200 offices. At that time, Edward Jones began assigning brokers to small towns (instead of sending them there every week or two). The idea was to convert Edward Jones into a distribution network to sell mutual funds in rural areas.

The third stage in the evolution of Edward Jones took place in 1970 after the firm’s managing principal, John Bachmann, arrived. In what he describes as a “defining moment” for the firm, he began to convert Jones into a “merchant” — an informed buyer for the end customer. According to Bachmann, the distinction between a distributor and a merchant is crucial:

“A distributor is structured around the product and tries to sell only profitable products. A merchant, on the other hand, is structured around the end consumer. He acts as an informed buyer for the investor, selecting only the products that are good for the investor, as opposed to products that generate fees for the brokers. Most investment firms look at brokers as their customers. We don’t. For us, the customer is the individual investor that signs the checks.”

This vision of being a merchant for the individual investor has guided every move of Edward Jones since 1980. It also has shaped the company’s currently successful strategy, the main elements of which are as follows (see Table 1):

{kind=link}

- Edward Jones targets and sells its products only to individual investors, never to institutional investors.

- The firm sells only selected products — often transparent, long-term products such as large-cap equities and highly rated bonds. It avoids selling risky initial public offerings, options, or commodity futures.

- Edward Jones does not manufacture the products it sells, unlike its major competitors (e.g., Merrill Lynch, Smith Barney) that sell their own in-house mutual funds. Jones acts only as a distributor for the products of a few selected manufacturers, such as Capital Research, Putnam, and Morgan Stanley.

- The firm sets up one-person offices in selected areas — usually small communities or specific areas within cities where there is a “sense of community.”2

- Edward Jones remains a partnership so that individual brokers feel and think like owners, not employees.

- The company behaves like a family whose mission is to help ordinary people invest their money wisely. The glue that holds everything together is Jones’s strong culture.

These are the main elements of the successful Jones strategy. John Bachmann likes to point out that each element involved some kind of trade-off for the company: “We target individual investors not institutional ones. We buy good securities and keep them a long time instead of trying to maximize transaction fees. Rather than have big offices in large cities, our offices are small and are placed in small communities to be convenient to the customer. Our offices are one-person operations not multi-person ones. We do not manufacture our products, and we showcase the products of a limited number of leading houses. We do not sell all products — we select transparent and safe products to promote. We remain a partnership rather than try to go public.”

The company has remained faithful to these judicious choices for more than twenty years. As John Bachmann phrases it: “These principles are cast in stone. We don’t debate these things.”

Uniqueness Is Transitory

Edward Jones built its success on finding and exploiting a singular strategic position in its industry. It did not try to imitate the strategic position of other competitors or try to beat its competitors at their specialties. Instead, Jones’s unique position allowed it to play an entirely different game. Although no position is truly unique, the idea is to create as much differentiation as possible.

Unquestionably, success stems from exploiting an unparalleled strategic position. Unfortunately, a position’s uniqueness will not last forever! Aggressive competitors will not only imitate attractive positions but, perhaps more importantly, new strategic positions will be emerging continually. A novel strategic position is simply another viable who-what-how combination —perhaps a new customer segment (a new “who”), a new value proposition (a new “what”), or a new way of distributing or manufacturing a product (a new “how”). Gradually, such new positions may challenge the domination of existing positions.

This happens in industry after industry: once formidable companies with seemingly unassailable strategic positions find themselves humbled by relatively unknown companies that base their attacks on creating and exploiting new strategic positions in the industry. The rise and fall of Xerox from 1960 to 1990 highlights this simple but powerful point.

In the 1960s, Xerox dominated the copier market by following a well-defined and successful strategy. Having segmented the market by volume, Xerox decided to win the corporate reproduction market by concentrating on copiers designed for high-speed, high-volume needs. This inevitably defined Xerox’s customers as big corporations, which in turn determined its distribution method: a direct sales force. Xerox also decided to lease rather than sell its machines, a strategic choice that had worked well in the company’s earlier battles with 3M.

The Xerox strategy was clear and precise with sharp boundaries. Undoubtedly, lively debates and disagreements within Xerox preceded the firm’s discerning strategic choices. Yet, difficult decisions were made and actions taken. The company prospered because of its distinctive strategic position with well-defined customers, products, and activities. Throughout the 1960s and early 1970s, Xerox maintained a return on equity of around 20 percent.

In fact, Xerox’s strategy was so successful that several new competitors, including IBM and Kodak, tried to enter this huge market by adopting the same or similar strategies. Fundamentally, their strategy was to grab market share by being better than Xerox. For example, IBM entered the market in 1970 with the IBM Copier I, which the IBM sales force marketed on a rental basis to the medium- and high-volume segments. In 1975, Kodak entered the market with the Ektaprint 100 copier/duplicator, a high-quality, low-price substitute for Xerox machines that was aimed at the high-volume end of the market.

Neither of these corporate giants made substantial inroads into the copier business. They failed for many reasons, but their inability to create a distinctive position was undoubtedly one of them. Unlike Xerox, both IBM and Kodak failed to identify or create a distinctive strategic position in the industry. Instead, they tried to colonize Xerox’s position and fought for market share by trying to outdo Xerox. Given Xerox’s first-mover advantage, it is not surprising that IBM and Kodak failed.

In contrast, Canon chose to play the game differently. After diversifying in the 1960s beyond cameras into copiers, Canon segmented the market by end user, targeting small- and medium-sized businesses while producing personal copiers for the individual as well. Canon also decided to sell its machines through a dealer network rather than lease them. Whereas Xerox emphasized the speed of its machines, Canon elected to concentrate on quality and price as its differentiating features. Unlike IBM and Kodak, Canon successfully penetrated the copier market, emerging as the market leader in terms of volume within twenty years. Canon succeeded for many reasons, but particularly because it established a distinctive, well-defined strategic position rather than trying to beat Xerox at its own game.

Continually Emerging New Positions

Canon challenged Xerox by creating a new strategic position in the copier business that undermined Xerox’s position and destroyed its basis of profitability. Such attacks are common (see Table 2). The “dominant” competitors establish unique strategic positions in their respective industries. Over time, “traditional” competitors imitate their predecessors in an attempt to wrest market share from them. Increasingly, though, “strategic innovators” emerge that run away with huge chunks of the market — often a new market that they helped to create.

Incursions into established markets by strategic innovators have resulted in the following notable outcomes:

- Canon’s market share in the copier business jumped from zero to 35 percent in about twenty years.

- Komatsu increased its market share in the earthmoving equipment business from 10 percent to 25 percent in less than fifteen years.

- Launched in 1982, USA Today had become the top-selling U.S. newspaper by 1993, selling more than 5 million copies per day.

- Dell Computer Corporation emerged from its college-dorm beginnings in the mid-1980s to capture more than 10 percent of the global personal computer market in less than ten years.

- Started in 1989 as the United Kingdom’s first dedicated telephone bank, First Direct had nearly 700,000 customers within seven years — an achievement that the business press described as a miraculous cure for the stagnant banking industry.

- Starbucks Coffee grew from a chain of eleven stores and sales of $1.3 million in 1987 to 280 stores and sales of $163.5 million in five years. The store total now tops 1,600.

- Direct Line was launched in 1985 and, within ten years, became one of Britain’s biggest motor insurers (2.2 million policyholders).

These companies achieved their hard-earned successes in a similar way, namely, by proactively breaking the rules of the game in their industries. The hallmark of their success was strategic innovation: proac-tively establishing distinctive strategic positions that were critical to shifting market share or creating new markets.

As industries change, new strategic positions arise to challenge existing positions. Changes in industry conditions, customer needs or preferences, demographics, technology, government policies, competition, and a company’s own competencies generate new opportunities and the potential for new ground rules. Existing niches expand while others die, new niches appear, mass markets fragment into new segments (or niches), “old” niches merge to form larger markets, and so on. This dynamic occurs in every industry.

Now, imagine your company as it tries to compete in its industry. Let’s say that your company has carved out a nice position in the mass market. It has several competitors in the mass market, and several niche players exist on the periphery. While you are competing with your primary competitors, you know that new niches are developing, and you want to ensure that your company does not miss these new opportunities. But, from among hundreds of new niches, identifying a productive one is difficult; so is predicting its growth rate and eventual size. Meanwhile, though your company’s sales are increasing, a winning niche arises —its growth resulting from the creation of an entirely new market. Such developments complicate your ability to understand the magnitude of the problem confronting your company. What can you do in this situation?

After a niche becomes a huge market, hindsight confirms that you should have done something earlier. But, it is hard to know which threat to respond to and when! For example, it is only with hindsight that we can say IBM should have responded to the Dell threat long ago. But, in the early 1980s, even if IBM had spotted this new entrant, should it have worried about a tiny niche player with 1 percent of the market? How about when Dell’s market share grew to 5 percent? Or 10 percent? When did Dell really become a major worry for IBM? Even if IBM wanted to respond to the Dell challenge now, what could it do? Can it play two games simultaneously?

Preparing for the Unknown

No company has perfect foresight in predicting emerging strategic innovations. However, lack of certainty is no excuse for inactivity. A company can face up to all this uncertainty by adopting one or both of the following generic options.

Option One: Become the Innovator.

Established competitors can proactively develop the next strategic innovation in an industry. Just as cannibalizing existing products when creating next-generation products is acceptable, companies should not hestitate to cannibalize an existing strategic position to create the “next generation” position. This is difficult, but not impossible.4

Practically speaking, a company must cultivate the “right” attitude, but also organize itself to compete effectively in its existing business while simultaneously experimenting with new technologies and ideas. How can the old and the new coexist harmoniously?5 This calls for creating an ambidextrous organization, which is a formidable task. As Tushman and O’Reilly point out: “This requires organizational and management skills to compete in a mature market (where cost, efficiency, and incremental innovation are key) and to develop new products and services (where radical innovation, speed, and flexibility are critical).”6

Utterback also forcefully makes this point: “Firms owe it to themselves to improve and extend the lives of profitable product lines. These represent important cash flows to the firm and links to existing customers. They provide the funds that will finance future products. At the same time, managers must not neglect pleas that advocate major commitments to new initiatives. Typically, top management is pulled by two opposing, responsible forces: those that demand commitment to the old and those that advocate for the future. Unfortunately, advocacy tends to overstate the market potential of new product lines and understate their costs. Management, then, must find the right balance between support for incremental improvements and commitments to new and unproven innovations. Understanding and managing this tension perceptively may well separate the ultimate winners from the losers.”7

Option Two: Exploit Someone Else’s Innovation.

Chances are that an established company will not be the source of the next new strategic innovation. For every established competitor, hundreds of new entrants or entrepreneurs are trying to concoct the next “great” innovation, and it is likely that one will succeed. Nevertheless, an established competitor should be poised and ready to take advantage of emerging innovations. But what does “being ready” imply?

Being Ready

Research shows that most established companies fail when a technological innovation invades their market —even when they actually adopt a new technology. Several reasons for this have been identified:

- They lack the necessary core competencies to take advantage of the innovation.

- They are late adopters and abandon an innovation at the first sign of trouble.

- They are trapped in their customary ways of competing, their core competencies having become core rigidities.

- They do not effectively manage the organizational transition from the old to the new when adopting a new technology.8

This implies that to prepare for the inevitable strategic innovation that will disrupt a company’s market, an organization should:

1. Build an early monitoring system to identify turning points before a crisis occurs.

Firms must develop the capability to recognize early whether a new strategic position is emerging that will unsettle their markets. The most effective way to do so is to regularly monitor indicators of strategic rather than financial health — that is, leading indicators of a company’s performance such as employee morale, customer satisfaction, and distributor feedback. Also track and benchmark maverick competitors that operate in small niches or appear to be breaking the rules of the game in the industry. In addition, encourage people close to the market to actively monitor and proactively report changes in the market to the appropriate decision makers. Alternatively, build a strong sense of direction, establish the parameters within which people can maneuver, and then empower them to take action. In short, develop the capability to identify changes early.

2. Prevent cultural and structural inertia.

Cultivate a culture that welcomes change and is ready to accept a new strategic innovation even if it disrupts the status quo. Established companies often wait too long to adopt an innovation. Reasons for this are many — not the least of which is the uncertainty of whether the innovation will be a winner. By developing a culture that welcomes change and encourages experimentation and learning, obstacles to innovation may be overcome. Such a culture may be further enhanced if top management uses “shocks to the system” to acclimate employees to change.

For example, cultural inertia at Raychem is challenged every day. Company founder Paul Cook says: “Raychem is working to make its own products obsolete every day. Right now, we are in the process of making one of our best products obsolete, a system for sealing splices in telephone cables. Now, we could have kept on improving that product for years to come. Instead, we’ve developed a radically new splice-closure technology that improves performance tremendously, and we’re working very hard to cannibalize the earlier generation. Our old product wasn’t running out of steam. Our customers had virtually no complaints about it. But because we knew the product and its applications even better than our customers did, we were able to upgrade its performance significantly by using a new technology. Why are we doing it? Because we understand that if we don’t make ourselves obsolete, the world will become more competitive.”9

3. Develop processes that allow experimenting with new ideas.

New innovations are not adopted quickly because they are not recognized to be winners. If experimentation were to reveal the potential of a new innovation, a company would be more likely to adopt it. Experimentation is the process that Intel’s Andrew Grove terms “let chaos reign” — when people explore novel ideas until enough information is collected to allow the firm to make a decision.

Grove further describes the process: “When danger comes, the adrenaline starts flowing and you want to pull the reins in and take control. But the opposite is what is needed. The reason you need to do the opposite is that, in this phase of the curve, you do not know enough to take charge. The fragmented information will come with fragmented suggested directions. You let things develop, and the way you let things develop is to relinquish control and let people — division heads, geography heads, engineers — pull in various directions. . . . This is the only way to get enough information to really build up a basis on which to decide whether to go for one option or the other.”10

4. Be prepared with the required competencies.

Prepare to exploit the company’s new position by building the appropriate competencies and skills. Unfortunately, this is easier said than done.

Utterback makes the point succinctly: “There is no easy answer as to how firms should choose the core competencies that will assure their progress and survival. Certainly, it is essential to anticipate discontinuities and to try to act in advance of their full impact. Doing so requires constant monitoring of the firm’s external environment to notice forerunners of significant change. We have seen that most firms look in exactly the wrong places for vital signs of technological change: namely, their universe of traditional rivals. . . . Looking toward more obscure new entrants and unconventional sources of competition is more fruitful, although these sources are more diffuse and difficult to monitor. Technological and market uncertainty, however, implies that no one can act with clear anticipation or forecasts. Among equally capable generals, the one with the best contingency plans will usually win the battle. Unexpected departures from the anticipated plan are almost certain to arise and in the best of cases, they will open the way to greater opportunities than at first imagined. This is crucial in the choice of capabilities to foster.”11

In the face of uncertainty, the best a firm can do is build internal variety (even at the expense of efficiency), and let the market mechanism determine what wins. By nurturing variety, a company also builds the competencies needed in the future. Creating and managing internal variety is intrinsically difficult — but it is achievable if learning is allowed to flourish in the organization.

5. Manage the transition.

Finally, a firm must manage the transition to the new strategic position. Two issues are involved.

First, the organization must clearly decide whether to adopt the new position. As Grove puts it: “At last, you have got through the strategic inflection point. In this second phase, it is time to rein in chaos. The phase for experimentation is over. Now is the moment to pull the reins in and to take charge again. At this point, you must be completely explicit in stating the direction of the new business. When you get out of pursuing multiple architectures, you must be completely explicit that the experiment is stopping, that all resources are being put into one option. No ifs or buts: explicit clarity.”12

Second, the company must ensure that the “old” and the “new” coexist harmoniously. Any innovation, by virtue of being small in scope relative to the existing company, will receive little attention and limited resources unless it is protected. The solution is to develop a separate organizational unit for the new position to prevent its suffocation. Dedicated people who consider it “their baby” will fight for it.

To summarize the general approach, a company can prepare to take advantage of a strategic change by developing the ability to recognize an innovation early, by promoting a corporate culture that welcomes change, by developing processes that allow experimenting with new ideas, and by developing skills that allow exploitation of the new position. After introducing an innovation, the company must protect it in a separate organizational unit and nurture it by means of consistent investments.

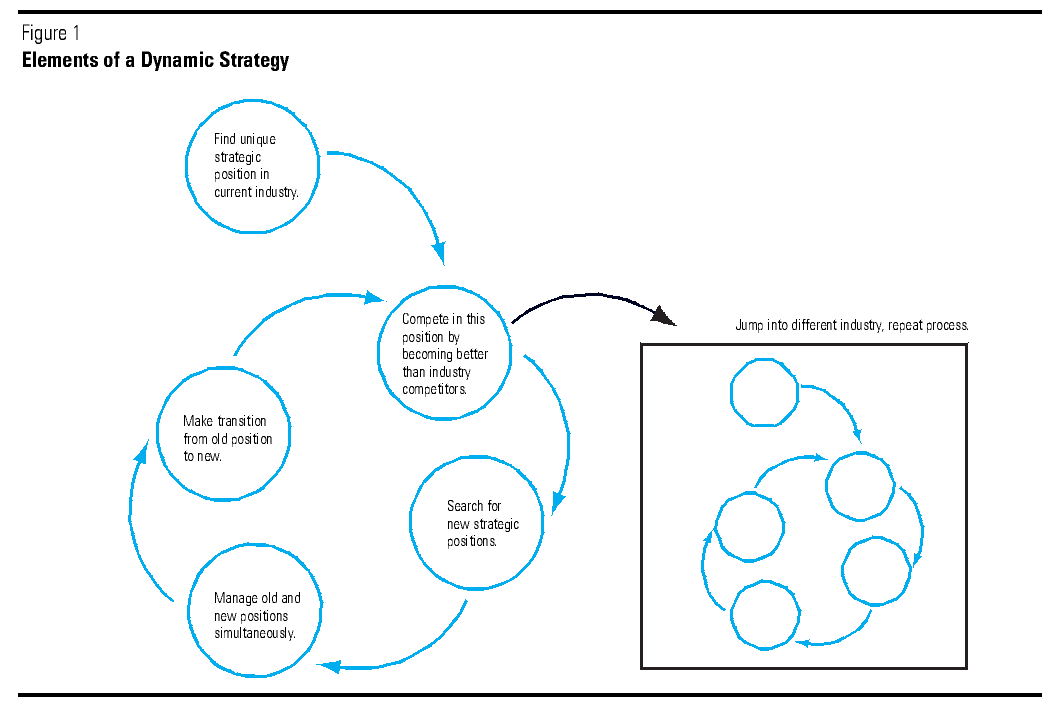

Elements of a Dynamic Strategy

Given the analysis so far, we can now begin to view strategy in a more dynamic way (see Figure 1). In thinking about its strategy, a company must first identify and colonize a distinctive strategic position in its industry. It should then excel at playing the game in this position, thus making it the most attractive position in the industry. While competing in its current position, a company also must search continuously for new strategic positions. After identifying another viable strategic position in its industry, the company then must attempt to manage both positions simultaneously — no easy task. As the old position matures and declines, the company must slowly make a transition to the new, at which point, it must start the cycle again: while fighting it out in the new position, it must again search to discover another viable strategic position to colonize.

{kind=link}

Of course, at any time during this dynamic process, a company could opt to jump into a new technology or industry. This could happen while the company is still competing in its first strategic position, later while the company is striving to balance the demands of two strategic positions, or at any time during the evolution of a firm’s strategy. Notice, however, that after jumping into another industry, the firm must go through the same dynamic process as in its original industry. Moving into another industry does not alter the strategic tasks that a company must undertake in each business — it just makes management more complicated in that the firm faces additional challenges, such as how to manage a diversified portfolio and how to exploit synergies among its businesses.

Thus, designing a successful strategy is never-ending. A company needs to continuously revisit and challenge its answers to the who-what-how questions in order to remain flexible and ready to adjust its strategy if feedback from the market is unfavorable. Changing industry conditions and customer needs or preferences, countermoves by competitors, and a company’s evolving competencies give rise to new opportunities and the potential for new ways to play the game. A strategy adopted a decade ago on the basis of prevailing industry conditions is certainly not a guaranteed game plan for the future.

Even (or perhaps, especially) successful companies must continuously question the basis of their business and the assumptions behind their successful formulas. Because new who-what-how positions spring forth from the mass market almost ceaselessly, established companies must be on the lookout for these new positions. Like modern-day pioneers, corporate executives must set out to explore the evolving terrain of their industries in search of unexploited strategic positions. Only the intrepid who abandon the safety of the familiar to venture into the unknown will have a future worth discussing.

References

1. The “who-what-how” framework was introduced in:

D. Abell, Defining the Business: The Starting Point of Strategic Planning (Englewood Cliffs, New Jersey: Prentice-Hall, 1980), chapter 2.

2. In nearly all cases and contrary to traditional wisdom that emphasizes exploiting economies of scale in such offices, a Jones office is a one-person operation. Each Jones broker has extraordinary autonomy in managing his or her office, and every branch is a profit center. A satellite communications network that broadcasts “home-grown” TV programming ties brokers to the home office.

3. P. Weever, “Growing Call of Telephone Banks,” Sunday Telegraph (London), 22 December 1996, p. 2; and

A. Bailey, “Telephone Banking – It’s for You: The Service Has Scope for Great Popularity,” Financial Times, 3 April 1996, p. 18.

4. See C. Markides, “Strategic Innovation,” Sloan Management Review, volume 38, Spring 1997, pp. 9–23; and

C. Markides, “Strategic Innovation in Established Companies,” Sloan Management Review, volume 39, Spring 1998, pp. 31–42.

5. This same point is also discussed in: M. Tushman and C. O’Reilly, “The Ambidextrous Organization: Managing Evolutionary and Revolutionary Change,” California Management Review, volume 38, Summer 1996, pp. 8–30; and

R. Burgelman and A. Grove, “Strategic Dissonance,” California Management Review, volume 38, Winter 1996, pp. 8–28.

6. Tushman and O’Reilly (1996), p. 11.

7. J.M. Utterback, Mastering the Dynamics of Innovation (Boston: Harvard Business School Press, 1994), p. 216.

8. A. Cooper and C. Smith, “How Established Firms Respond to Threatening Technologies,” Academy of Management Executive, volume 16, May 1992, pp. 92–120;

R. Foster: Innovation: The Attacker’s Advantage (New York: Summit Books, 1986), chapter 6, pp. 139–164;

A. Cooper and D. Schendel, “Strategic Responses to Technological Threats,” Business Horizons, volume 19, February 1976, pp. 61–69; and

Utterback (1994), chapter 9, pp. 189–213.

9. W. Taylor, “The Business of Innovation: An Interview with Paul Cook,” Harvard Business Review, March–April 1990, pp. 96–106.

10. A.S. Grove, “Navigating Strategic Inflection Points,” Business Strategy Review, volume 8, number 3, 1997, pp. 11–18.

11. Utterback (1994), p. 220.

12. Grove (1997), p. 17.