Investment in Technology — The Service Sector Sinkhole?

OVER THE PAST DECADE, senior managers in banking, insurance, health care, and other service industries have invested billions of dollars in computers and communication equipment—technology investments that promise to hone operations into an acute competitive weapon. But executives have been deluded; the payoffs have not been fully realized.

- Recent studies by the American Quality & Productivity Center show that in the service sector—finance, insurance, wholesale, retail, and business service companies—the effectiveness of labor and capital utilization is only slightly higher today than it was ten years ago.1 This despite nearly $180 billion invested in hardware and software to automate the spectrum of manual-intensive tasks.2

- Service quality, while difficult to measure, is generally perceived to be deteriorating. The news media frequently call this deterioration to our attention, as does our day-to-day experience as consumers of services. Bank teller lines seem longer. Flight delays are more frequent.

- Operating and administrative costs—driven in large part by technology expenses—continue to spiral upward. For its investment, management expected just the opposite.

- Pretax profitability is deteriorating in the service sector, declining from a high of 10 percent in 1965 to 5 percent in 1987.3 In addition, foreign competition is making inroads. The balance of trade has dropped to about $30 billion from $70 billion in 1981.4 The financial service, entertainment, and real estate industries have been most vulnerable.

Why have technology investments in the service sector been so disappointing? The leading reason is that companies are relying too heavily on technology to achieve competitive advantage. Firms have invested in technology in hopes of leapfrogging their rivals using competitive barriers, improved service levels, technology-based products and services, and lower employee-related expenses. There have been some success stories—most notably American Airlines’ reservation booking system and Federal Express’s letter and package tracking database. But for most companies the goal has been elusive.

The primary reason is that technology alone does not determine corporate performance and profitability. Employee skills and capabilities play a large role, as do the structure of day-to-day operations and the company’s policies and procedures. In addition, the organization must be flexible enough to respond to an increasingly dynamic environment. And products must meet customer requirements.

Technology Investments Are Staggering

During the past twelve years, service industry investments in technology have grown at an inflation-adjusted compound annual rate of 20 percent. Service industries have invested more than $180 billion in information and communication systems. Eighty percent of all technology investments are now made by service sector companies.

Since the mid-1970s, automation has exploded. Today, service companies spend an average of $3,000 per employee per year on computers and other technology—twice the amount that industrial companies invest annually in new plants and equipment per employee.5 In addition, since 1982, the service sector has surpassed the industrial sector in capital stock per employee. In other words, service sector employees now have more computers than industrial sector employees have machine tools and assembly lines.6

Of course, this massive investment has not been entirely fruitless. Technology has enabled companies to cope with the increasing volume of business associated with the sector’s explosion during the past fifteen years, when service consumption grew by 50 percent, service sector employment jumped by one-third, and contribution to GNP leaped from 55 percent to nearly 71 percent. Technology played a crucial role in the development of new and sophisticated products and services, many of which focus on customer convenience. Similarly, it helped build client relationships through consolidating and sharing comprehensive databases.

But these contributions are not good enough. Managers expected more for their $180-billion in vestment. Regrettably, other promised payoffs-improved employee productivity and customer service, and reduced operating expenses—have scarcely materialized:

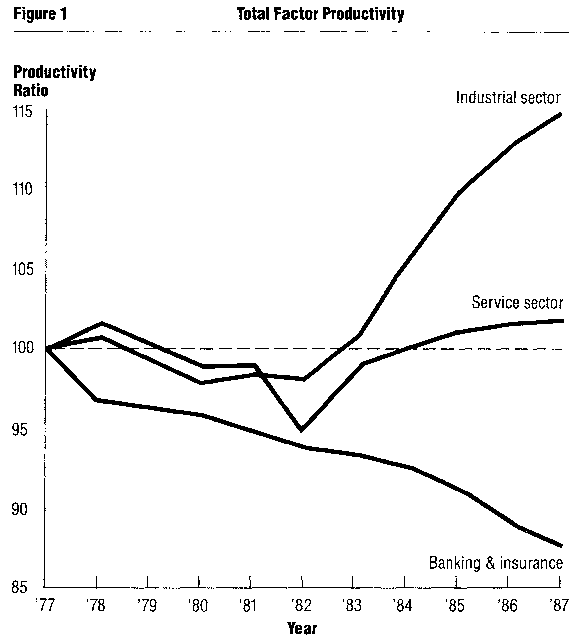

- Productivity in the service sector—the value of outputs measured against the value of labor and capital inputs—has shown little growth since 1977; industrial sector productivity has risen five times faster in the same period. Most troubling is that in the service sector’s largest industries—banking and insurance—productivity has actually declined in recent years (see Figure 1).

- Outstanding service is becoming uncommon. Consumers blame this decline on undertrained employees and the increasing use of computers in self-service schemes. Employees make excuses to consumers, blaming computer errors. Customization seems impossible. Increasingly, customers interact with machines rather than with people, whether depositing money in a bank or choosing shoes in a retail store.7

- Service industry operating and administrative expenses have dramatically increased, outpacing both inflation and revenue growth. Increases in systems and automation expenses lead this trend, as they become a larger part of a company’s operating budget. In the banking industry, for example, automation expenses have doubled in a decade to nearly 14 percent of total operating expenditures.8

- Increased operating and administrative expenses are squeezing profitability, since they are not offset by improved productivity and lower employee-related costs.

{kind=link}

Service sector executives are clearly chagrined at the results of their technology and automation investments. A recent survey of CEOs found that less than half think their companies receive above-average returns on technology investments.9 Half believe their investment levels are too high.

However, nearly 45 percent of the executives feel that their levels of investment were needed just to keep up with the competition. And 70 percent expect to maintain —or increase—their technology investments in the years to come.

Operations and Technology Are Decoupled

Why is productivity so flat? What can be done to reduce operating expenses and improve profitability? Operations managers point to poor systems design, criticizing their technological tools as incomplete, inflexible, impersonal, and too complex. While these criticisms have some validity, the real problem is not that systems design is poor, but rather that operations and technology are not being coupled.

Generally, payback shortfalls can be attributed to three factors.

- Overall, day-to-day operations become outdated. An external perspective matching operations to increasingly sophisticated marketplace needs is lacking.

- The implementation of technology generally superimposes systems on inefficient and outmoded day-to-day operations.

- Service industry systems tend to be excessively complex. Companies are overdependent upon automation; they automate processes and activities that would be better left manual since volumes are low, products are unique, or automation is prohibitively expensive.

Highly competitive companies build automated systems on a foundation of well-designed and executed operations. In most cases, to achieve sustainable improvements, operations must first be restructured for efficiency and effectiveness and then be integrated with technology. This sequence requires the development of a comprehensive operating strategy similar to those employed by manufacturing corporations.

Tying Operations to the Business First

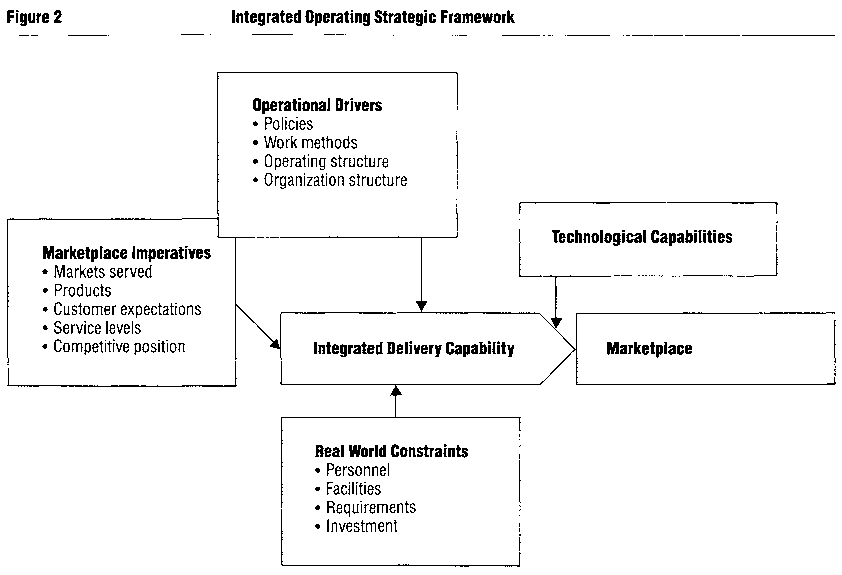

Successful operating strategies must be grounded in marketplace and competitive requirements. The combination of operational drivers and technological capabilities, tempered by real-world constraints, defines how well a company can deliver its services (see Figure 2). This holistic approach ensures that customer needs are met, that internal competing factors are balanced, and that technology is fully integrated into operations. The problem always resides in a company’s ability to deliver services to its customers, rather than in the “product” (service) itself.

{kind=link}

Many operational units were never planned. Instead they evolved to fit the apparent needs of the business they support. Work tends to be executed in the same fashion as it was a decade ago, while the competitive environment has become much more complex. Organizations, methodologies, and policies have not changed to fit the new market-place realities.

For example, a major West Coast savings and loan association was originating $3 billion annually in mortgages using twenty-year-old operating strategies. First, an account executive took a customer’s application. The executive then transferred the application to a processing center, where some-one collected information about the customer’s credit history and ability to repay the loan, and about the collateral’s security. This information was forwarded to an underwriter, who typically requested additional data from the customer before making a decision. This process of cycling back to the customer could occur three or four more times—substantially stretching out the decision period— before the underwriter was satisfied. The entire process usually took thirty days or longer to complete. Almost one-third of the applicants were eventually turned down.

The thrift’s competitive environment had evolved over time, leaving the institution at a disadvantage. Quick decisions had become a competitive imperative—final decisions needed to be rendered in as few as ten to fifteen calendar days. In addition, unsuitable applicants had to be notified very early in the process so they could seek alternate financing. And traditional application fees, which offset processing costs, were being waived to attract new customers.

Management’s initial approach to meeting the new requirements was to computerize the processing and tracking systems. Upon investigation, it was determined that the process itself was ineffective; automating the approach that had been used for the past twenty years would not change the thrift’s competitive advantage.

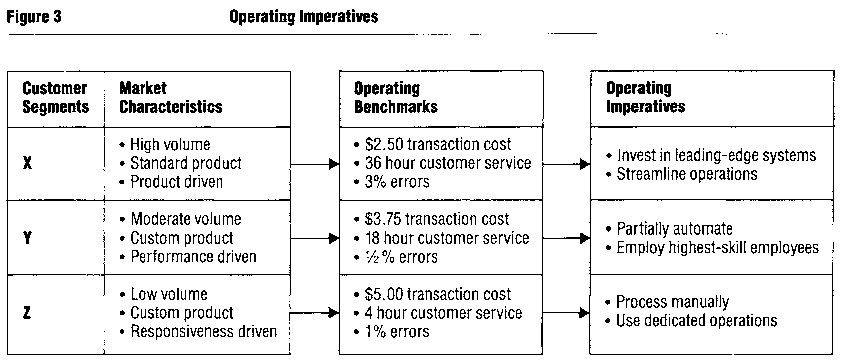

Creating a successful operations strategy begins with converting marketplace requirements into a series of operating imperatives (see Figure 3). These imperatives include customer wait time, the cost of providing service, flexibility and customization of the product or service, and error rates. The marketing department may know what the customer desires, but this knowledge typically has not been translated into a well-defined operating mission. Often, there is a vague directive such as “good service and low cost.” Such directives most often lead to the delivery of average service across the board. Banking is a good example. Upscale customers wait as long in teller lines as traditional passbook savers. Some customer segments are underserved, while others are overserved.

{kind=link}

Defining imperatives begins with basic market research to identify customer segments. The next step is to determine the exact market characteristics of each segment—high or low volume, standard or custom product, and price sensitivity, for example. Specific operating benchmarks that are based on these characteristics and tied to the marketing strategy need to be established. These include maximum cost per customer segment, specific error rates, and processing lead time.

Given such detailed benchmarks, the operating imperatives—level of technology to be employed, work flow, organization structure, employee skills— may now be defined. The imperatives may be substantially different for each customer segment.

Thinking about Automation in a Fresh Way

The most frequent approach to implementing technological improvements is to superimpose new systems and applications onto existing operations. Major change is resisted, and management tends to replicate current procedures regardless of how out-dated or inefficient they are. Or sometimes an off-the-shelf software application that appears to match present operations is customized a bit. This approach dangerously institutionalizes inefficient and ineffective operating procedures, making it difficult to streamline and update operations— and to achieve optimal payoff from technology investments.

For example, a major East Coast servicer of mutual funds invested more than $20 million to automate its operations. But the 15 percent expected productivity improvements (including a 200-person head-count reduction) upon which the system was justified never materialized. Instead, operating expenses went up, and customer service deteriorated. The firm had automated inefficient operating practices and failed to recognize the distinct market requirements of the different customer segments of its business.

The problem was particularly bad in mutual fund accounting. Before automation, most tasks—such as filling out forms—were completed manually. One accountant was assigned to each fund, and the accountants were utilized about 80 percent of the time. After automation, utilization dropped to only 55 percent, but the same accountant structure was maintained. Paperwork was now processed by the computer, and the accountants had more time but less work to accomplish, although work was not reduced enough to break the one accountant/one fund profile. The accountants’ jobs became clerical and boring, turnover increased, and customer continuity was broken. In the end, the automation was wasted.

This approach to technology and operations integration is like driving a Ferrari in a traffic jam. The potential for high performance exists, but there are too many limiting factors—restrictive policies, outdated procedures, cumbersome organizations, and untrained employees. Adding high-powered automation to an obsolete operating environment constrains technological potential and is counter-productive. In addition, post-implementation audits show that users tend to employ only a portion of a system’s full capabilities. New systems utilization can be as low as 50 percent, even after a reasonable implementation period. For example, note the number of terminals and personal computers not in use at any given time in an organization.

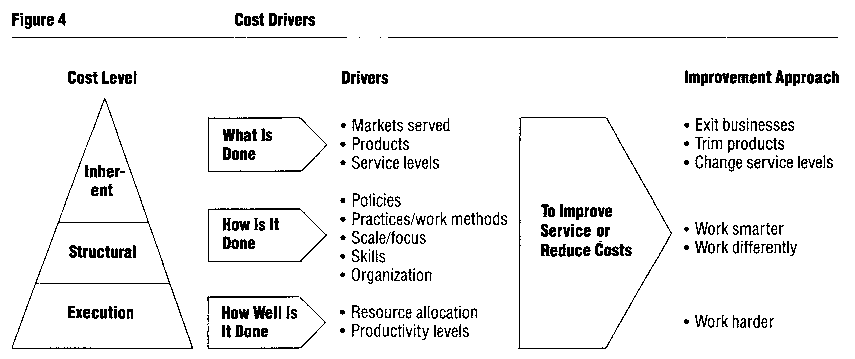

However, by analyzing operations at the appropriate level of precision, managers can identify major cost and service improvements before investing in automation. Doing this requires developing a detailed understanding of cost and service drivers. The different types of operating costs are influenced in fundamentally different ways (see Figure 4):

{kind=link}

- Inherent costs are driven by marketplace and competitive requirements and by the service levels and products the company offers. Influencing these costs normally involves longer time commitments and strategic redirection, including product-line repositioning or service level changes. However, opportunities for cost improvement and marketplace differentiation are large.

- Structural costs are driven by operational configuration and performance on a daily basis. Structural change can be achieved by working differently or working smarter.

- Executional costs are driven by how well the operations are currently managed. Improvements can be realized through tighter controls and harder work.

Structural changes—”working smarter”—offer the largest opportunity for improving operations and leveraging technology investments. Companies can eliminate handoffs and streamline work flow, build flexibility into operations, minimize controls, reduce management layers, increase spans of control, eliminate low-value-added work, consolidate similar operations, and retrain employees. All of these actions can substantially improve customer service and reduce operating costs. More important, these restructured operations are bases from which technology investments can effectively be leveraged.

Managing to Minimize Complexity

Many firms now unquestioningly reduce employee-related expenses by automating as many products and processes as possible. After all, computers work faster than humans, make fewer mistakes, are easier to manage, and don’t need to be trained. When taken to the extreme, this approach leads to substantial systems complexity, which in turn leads to higher initial investment requirements, as well as increased support and maintenance costs. For example, in the health insurance industry, only 10 to 15 percent of the products drive 75 to 80 percent of a system’s complexity and resulting costs. Low-volume, low-value-added products and processes—the smaller, complex operations that tend to have high demand variability—are automated.

In addition, overautomation trades variable employee costs for fixed systems costs, and makes downsizing in soft periods of business to reduce expenses extremely difficult.

There is a point where automating minor products and processes adds substantially to a system’s complexity and costs. Such incremental automation neither adds substantial value for the customer in terms of service or convenience, nor dramatically reduces operating expenses.

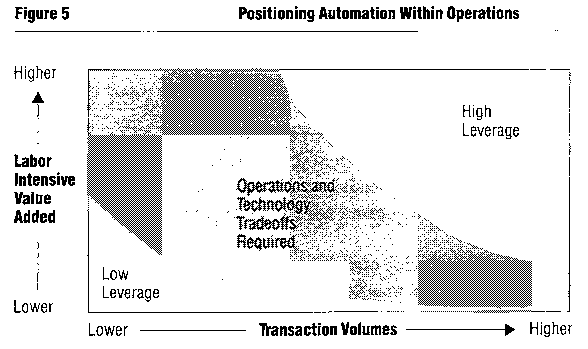

A balance point between labor-intensive operations and automation must be determined. But at what point is automation more effective and efficient? Products and processes with low levels of value-added labor and low transaction volumes are not prime candidates for automation. Instead, high-labor-content operations, with moderate to large transaction volumes, should receive automation priority (see Figure 5). In between the two extremes, the decision to invest in technology should be based on total operating costs and expected quantifiable strategic and marketplace benefits. In addition to comparing operating costs, the evaluation should include employee turnover, recruitment and training, management costs, amortized technology investments, and ongoing system support expenses.

{kind=link}

Conclusion

Taking this holistic approach to leveraging technology can result in a 15 to 25 percent reduction in expenses, service improvements recognizable in the marketplace, reduced error rates, and increased operating flexibility.

The promise of technology has yet to be realized. The challenge for service sector executives is to create competitive advantage by providing high levels of customer service while minimizing operating costs. Technology can play an important part in meeting these goals, but automation in itself is no panacea.

The latent value of technology cannot be tapped unless the operations strategy is developed in a broadly defined context. In addition, day-to-day operations must be restructured before technology is added. Finally, tough choices must be made about the level and magnitude of technology to deploy.

Coupling technology with other operational drivers will be imperative for the service company of the future. Companies that persist in developing their operations strategy solely from a technology perspective can look forward to tougher competition as their rivals realize the incremental benefits of an integrated, holistic approach.

References

1. Multiple Input Productivity Indexes (Houston: American Productivity & Quality Center, December 1988).

2. "Annual IS Survey," Datamation, 1977–1987.

3. U.S. Department of Commerce, Bureau of Economic Analysis, Survey of Current Business, July 1988, July 1984, Special Supplement, July 1981;

U.S. Department of Commerce, Bureau of Economic Analysis, Business Statistics 1986: A Supplement to tbe Survey of Current Business;

U.S. Department of Commerce, Bureau of Economic Analysis, Tbe National Income and Product Accounts of tbe United States, 1929–1976, Statistical Tables, September 1981.

4. Council of Economic Advisers, Economic Report of tbe President, January 1989.

5. S.S. Roach, "Information Economy Comes of Age," Information Management Review, September 1985. Supplemented by Booz, Allen & Hamilton interview with representative of the Federal Reserve System.

6. Ibid.

7. Based upon the author's experience shopping for shoes at the Florsheim Shoe Shop, Belden Village Mall, North Canton, Ohio.

8. National Operations and Automation Survey (Washington, DC: American Bankers Association, 1986).

9. R. Lane and R. Hall, "Elusive Returns—Managing Information Technology Investments," Booz, Allen & Hamilton, Information Technology Viewpoint, 1987.