Japanese-Style Partnerships: Giving Companies a Competitive Edge

“Japanese manufacturing industry owes its competitive advantage and strength to its subcontracting structure.” — Ministry of International Trade and Industry1

Was Japan’s powerful Ministry of International Trade and Industry (MITI) serious when it made this statement? Is it possible that much of Japan’s competitive advantage can be attributed simply to its subcontracting structure? Indeed, evidence from an increasing number of industries and sources suggests that much of the Japanese success can be attributed to Japanese-style business partnerships. Consider the auto industry, for example. From 1965 to 1989, the combined Japanese market share of worldwide passenger car production jumped from 3.6 percent to 25.5 percent. In striking contrast, the market share of U.S. firms dropped from 48.6 percent to 19.2 percent.2 Moreover, by the early 1980s, Japanese firms had achieved a 20 percent to 25 percent cost advantage, per car, versus U.S. automakers, while receiving customer satisfaction scores 50 percent higher than those of competing U.S. cars. Can we attribute the astonishing Japanese success to their partnership approach? Consider the following:

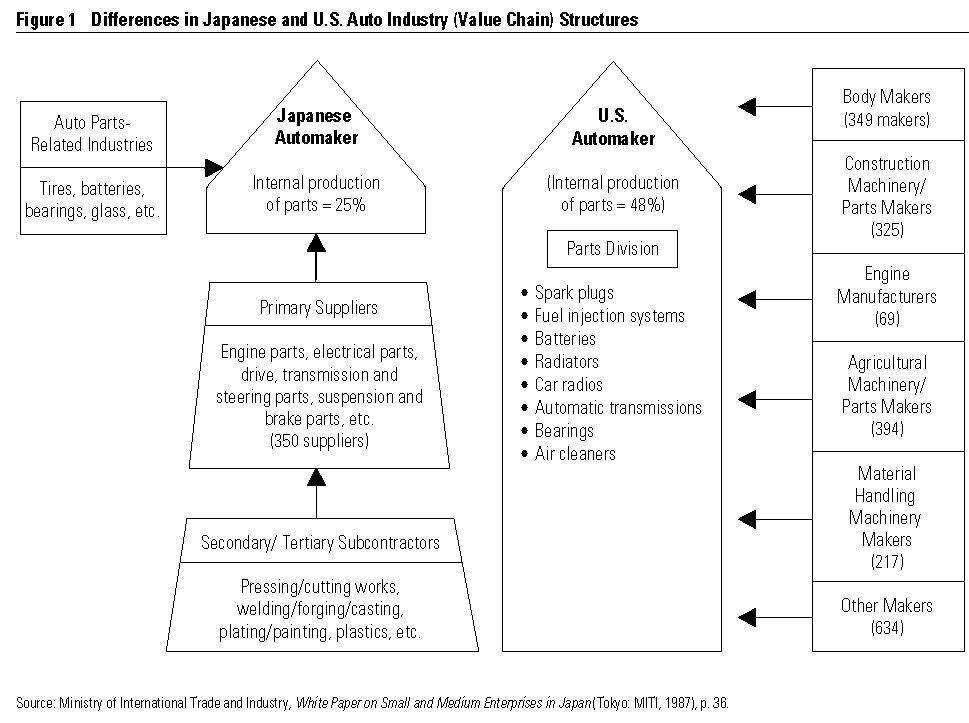

- American automakers are more vertically integrated than their Japanese counterparts, with approximately 48 percent of parts manufactured internally as opposed to 25 percent for Japanese automakers (see Figure 1).

- Even though U.S. automakers are more vertically integrated, they contract directly with 1,500 to 3,000 parts suppliers for the parts they don’t make. Toyota, by contrast, works with approximately one-tenth that number, buying more — in many instances, entire subsystems — from each supplier.

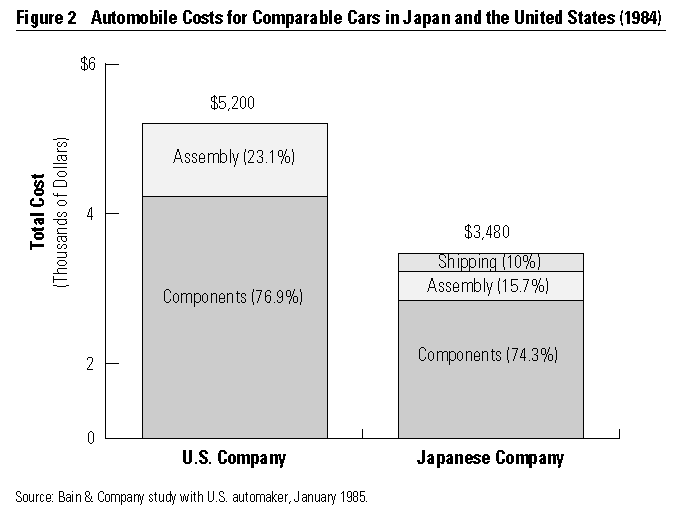

- A study conducted by Bain & Company found that the total cost of components for a Japanese car was more than 30 percent below that of a comparable U.S. model in 1984 (see Figure 2).3 A similar comparison of component costs reported in Fortune indicated that, in 1985, U.S. automakers spent an average of $3,350 on parts, materials, and services for small cars (priced at $6,000), while the average Japanese company spent $2,750 — a cost savings of more than 22 percent that was achieved mainly “through more efficient vendor relations.”4 While the gap has narrowed, Japanese automakers still have a cost advantage over U.S. makers.

- Japanese-owned plants in the United States purchase more than 50 percent of their auto components from Japanese suppliers (these Japanese suppliers sometimes have operations in the United States). As a result, even in their U.S. plants, they enjoy a $700-per-vehicle cost advantage over U.S. automaker plants, or about 10 percent of the retail cost of a small car.5

- Japanese automakers develop new vehicles at least 30 percent faster than U.S. automakers, which means that products include the latest in technology.6 Apparently, this advantage is due largely to Japan’s subcontracting structure. According to Clark, “In U.S. companies, the projects in our sample were heavily influenced by the traditional system in which suppliers produced parts under short-term, arm’s-length contracts and had little role in design and engineering. In the Japanese system, in contrast, suppliers are an integral part of the development process: they are involved early, assume significant responsibility, and communicate extensively and directly with product and process engineers.”7 Japanese suppliers frequently give automakers a head start in development by starting work on projects even before they are assured of winning the project.

{kind=link}

{kind=link}

Although these and other studies point to supplier relationships as critical to Japanese success, they don’t explain why Japanese suppliers are more cooperative and willing to take risks, nor do they explain why they are more productive than traditional arm’s-length supplier relations. Recently, U.S. automakers and other U.S. businesses have been making changes (notably, consolidating suppliers) that have moved U.S. supplier management practices closer to Japanese business practices. However, simply consolidating suppliers or moving to sole-source supply is not the key to Japanese-style partnerships and in fact may lead to problems if it is an isolated act. If U.S. companies are to adopt Japanese intercompany practices successfully, they must understand how and why they work. Consequently, two questions are critical:

- Why are Japanese-style partnerships more productive than either buying suppliers or customers (vertically integrating) or rotating business across numerous suppliers?

- Why are Japanese suppliers so cooperative and willing to take risks? (Doesn’t that make them overly dependent?)

What Is a Japanese-Style Partnership?

A Japanese-style partnership (JSP) is an exclusive (or semi-exclusive) supplier-purchaser relationship that focuses on maximizing the efficiency of the entire business system (value chain). These supplier partners are typically called kankei-gaisha (affiliated companies) in Japan and are considered to be the vertical keiretsu of the parent company. (Companies that are not kankei-gaisha are typically referred to as dokuritsu-gaisha or independent companies. Independent companies will often work with parent firms in much the same way as the kankei-gaisha.) Our findings are primarily from a two-year study of fifty kankei-gaisha in the automobile industry compared to fifty U.S. supplier-U.S. automaker relationships (see the appendix for a brief description of the study).

The goal of Japanese partnerships is to increase quality while minimizing the total value-added costs that both the supplier and the purchaser incur. In short, the goal is to create a “see-through” value chain where both party’s costs and problems are visible. Then both parties can work jointly to solve the problems and expand rather than split the pie. JSPs also take advantage of economies of scale in both production and transaction costs. In short, JSPs attempt to capture most of the synergies that would exist if the two firms (or portions of the firms) were combined under common ownership without actually incurring the costs or many of the dysfunctional aspects of combining the firms. (The disadvantages of acquisition include: paying a 30 percent to 40 percent acquisition premium; a tendency toward increased wages in the acquired firm since the larger firm, which usually does the acquiring, typically pays higher wages that are then transferred to the acquired company; and a loss of market discipline because a captive customer reduces the supplier’s incentive to innovate and continuously improve. Indeed, as we shall describe, the Japanese partnership structure creates substantial incentives for firms to improve continuously.) In summary, the key characteristics of JSPs in the auto industry are:

- Long-term relationships and commitments with frequent planned communication, which reduces transaction costs and eliminates intercompany inefficiencies.

- Mutual assistance and a focus on total cost and quality, working together to minimize total value chain costs (not just unit costs).

- Willingness to make significant customized investments in plant, equipment, and personnel as well as share valuable technical information.

- Intensive and regular sharing of technical and cost information to improve performance and set prices, which share equally the rewards of the relationships.

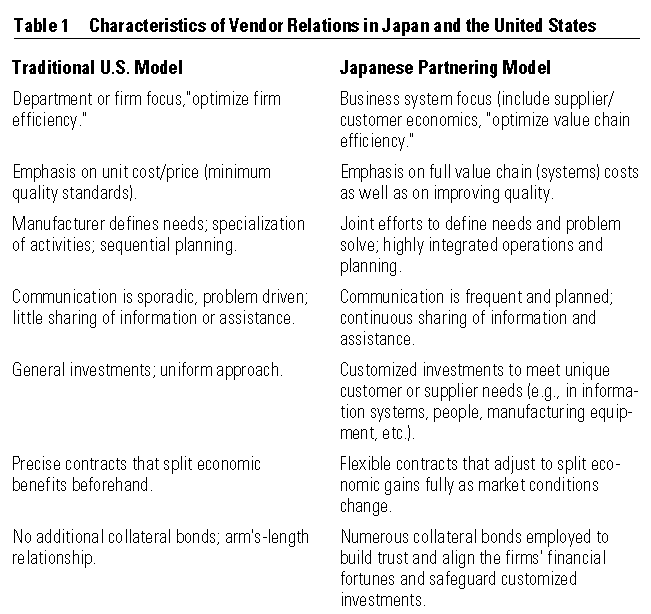

- Trust-building practices like owning stock (e.g., stock swaps), transferring employees, having guest engineers, and using flexible legal contracts that create a high degree of goal congruence and mutual trust (see Table 1 for a comparison of the traditional U.S. model of vendor relations with the Japanese partnering model).

{kind=link}

Why Are JSPs More Efficient?

JSPs realize economic benefits not available to firms that either vertically integrate or keep a large supplier base. There are usually three types of benefits: (1) fewer direct suppliers, (2) customized investments, (3) forced competition.

Fewer Direct Suppliers

It is no secret that reducing the total number of direct suppliers can lower costs while increasing quality. Using fewer suppliers can create value by providing economies of scale and experience curve benefits that lower either transaction costs or production costs.

Reducing Transaction Costs.

Transaction costs, as defined here, are all the costs associated with effecting an exchange (e.g., information gathering and analysis, negotiation, contracting, product movement costs, and so on). While most managers understand that greater economies of scale can reduce production costs, many fail to consider the extent to which they also affect transaction costs. Just as scale economies can lead to lower per-unit production costs, the economies of scale associated with increasing the volume of exchanges with a given supplier or customer can also lead to lower per-unit costs associated with completing the transaction. For example, a 1985 study of sourcing for wiring harnesses (electrical wiring) comparing the number of suppliers used by Toyota and a U.S. automaker revealed that Toyota gave virtually 100 percent of its volume to two suppliers while the U.S. manufacturer used more than twenty different suppliers.8 Naturally, the costs associated with managing twenty suppliers (preparing and analyzing bids, comparing products, negotiating prices, writing contracts, and so on) were substantially higher for the U.S. manufacturer than for Toyota, and tracking quality problems was a nightmare for the U.S. carmaker.

The total costs of managing multiple suppliers can quickly add up. For example, in 1986, General Motors employed approximately 3,000 purchasing people to procure goods and services for 6 million cars (2,000 cars per buyer). In contrast, Toyota employed 340 people to procure goods and services for 3.6 million cars (10,590 cars per buyer).9 Thus, GM’s procurement costs were approximately five times higher than Toyota’s. (In fact, the difference was greater because the GM buyers were buying only 50 percent of the value of the car — due to higher vertical integration — while Toyota buyers were buying 75 percent.) Why are the purchasing departments within U.S. automakers so large? Apparently, they were created to rotate the business and reduce the company’s dependence on any one supplier. When asked why GM has so many suppliers, one executive explained, “Our purchasing activities are huge and extensive. Most activities have been geared to making sure we don’t get stung by an unscrupulous supplier out there.”10

Reducing Production Costs.

Within most industries, as cumulative production experience in producing a product or service increases, quality is improved and costs are reduced. More specifically, each time accumulated experience doubles, costs per unit typically fall (in real terms, adjusted for inflation) by 10 percent to 30 percent, with comparable increases in product quality.11

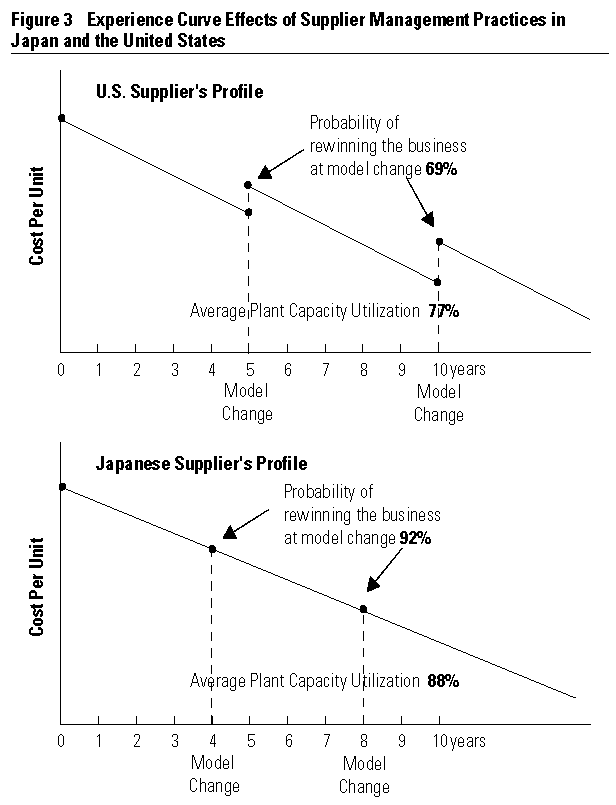

By applying the partnership approach, Japanese automakers have consolidated their business with a few highly efficient suppliers and created conditions that permit the suppliers to make the investments necessary to accelerate down the experience curve and to share the full advantage of this volume (and the resulting lower costs per unit) with the carmakers. When a Japanese supplier wins a contract with Nissan or Toyota, it is essentially guaranteed four years of business (or the life of the model). Moreover, if the supplier performs up to expectations, it can usually win the business for the next model as well. The Japanese suppliers in our sample indicated that historically they have a more than 90 percent probability of winning the contract again when the model changes (see Figure 3). While a supplier may have a contract for four years, in reality, Toyota’s and Nissan’s partners have essentially open-ended contracts that, according to a Nissan purchasing manager, “have no real termination date.” As one Toyota supplier said, “Once we win the business, it is basically our business unless we don’t perform. It is our business to lose.”12 Naturally, these practices encourage long-term plans and investments. Suppliers invest in developing ideas and plans for the next model well in advance. Engineers from the two companies have long-term experience working together, making it easier to rapidly develop designs for the next model. When the model change occurs, suppliers continue to move down the experience curve depicted in Figure 3.

{kind=link}

In contrast, U.S. auto manufacturers have attempted to keep input prices low by maintaining size and bargaining power over suppliers. By splitting their business among many suppliers and rotating them frequently, U.S. manufacturers have repeatedly destroyed the experience curves of suppliers by ensuring that no one supplier could accelerate down the experience curve to accumulate decisive cost advantages. The U.S. suppliers in our sample claimed that they typically have only a 69 percent chance of rewinning the business at a model change. Thus, at each model change, the experience of the previous supplier is destroyed and a new supplier must incur start-up costs. Supplier engineers typically do not develop long-term relationships and experience with automaker engineers. Moreover, U.S. suppliers are unable to effectively plan long-term production and investments, which is reflected in lower average plant capacity utilization (an average of 77 percent for U.S. suppliers versus 88 percent for Japanese suppliers; see Figure 3).

A 1989 survey found that the average length of the contract between U.S. suppliers and automakers was only 2.5 years, up from 1.3 years in 1984.13 The survey also found that, as the length of the contract between the supplier and automaker increased, so did the supplier’s investments in CNC machine tools, CAD/CAM systems, robotics, and manufacturing cells. Without long-term commitments, U.S. suppliers rationally refuse to make long-term investments in capital equipment. Moreover, without the ability to make long-term forecasts, it is very difficult to make maximum use of capacity and capital equipment.

A final benefit of having fewer suppliers is the positive effect on quality. When more suppliers are used for a given part, variation increases and reliability goes down. As quality guru W. Edwards Deming notes, “Even with a single supplier, there is substantial variation lot-to-lot and within lots.”14 Using multiple suppliers only increases the variation of parts that causes production problems and poor quality.

Customized Investments

Developing a Japanese-style partnership is much more complex than simply reducing the number of suppliers you use. The differences between JSPs and more traditional supplier relationships are illustrated by the following questions. How often do supplier-purchaser agreements in the United States involve:

- building a supplier plant within fifteen miles of the customer plant to reduce transportation costs, improve delivery, and generally improve coordination?

- allowing supplier engineers to work daily at customer technical centers with customer engineers in designing new products?

- transferring the purchaser’s executives or employees to the supplier to work on a temporary (one to two years) or permanent basis?

- sending in consultants (paid by the purchaser) to work with the supplier (often for months) to improve production methods, implement just-in-time delivery systems, or assist in solving other problems?

The answer to all four questions is, “Rarely.” Most U.S. companies are simply not willing to take the risk in making customized investments. Consequently, they forgo the value that these investments can create.

JSPs generally require various types of investments in customized assets (investments specifically related to the relationship) by one or both firms in order to optimize the production and flow of goods and services. Three types of customized investments are employed:

- Site-specific investments — plants are located so that they are dedicated largely to a particular customer in order to improve coordination and economize on inventory and transportation expenses.

- Physical investments — manufacturing equipment such as tools, dies, molds, jigs, machinery, and so on is customized.

- Human capital investments — dedicated design or manufacturing engineers develop significant partner-specific knowledge.

These partner-specific investments create substantial buyer and supplier switching costs and, once made, make the two parties highly interdependent. This interdependence can create potential contracting problems if the parties do not completely trust each other. (Contracting problems may arise because these investments are not marketable or redeployable; thus one party may act opportunistically since it, in effect, has a monopoly on the customized investments.) However, the investments also create value substantially beyond what could have been achieved without them.

Toyota’s just-in-time (JIT) systems are a good example of how customized investments can create value. JIT was designed to reduce complexity and costs by eliminating inventories and work in process and to ensure that there were no redundant buffer stocks, distribution facilities, or quality inspections. However, to effectively implement JIT, Toyota and its partner suppliers had to make customized investments in information systems, plants, and flexible manufacturing systems that created mutual dependency. For example, in our survey of twenty-five Toyota partner-suppliers, we found that the average (median) distance from the supplier’s manufacturing plant to the Toyota assembly plant was only seventeen miles. The close proximity of these plants makes it economical for suppliers to make an average of 7.4 deliveries each day (over 30 percent of Toyota suppliers make hourly deliveries) and keep minimal inventories.15 Naturally, this site-specific plant investment, more than 75 percent of which is dedicated to Toyota, keeps inventories extremely low. In a comparison of the now-closed GM (Framingham) plant and the Toyota (Takaoka) plant, Womack et al. found that, while the GM plant had an average of two weeks of inventory, the average buffer inventory at the Toyota plant would last only two hours.16 Thus, in this particular case, GM and its suppliers needed to invest in and store as much as 200 times the inventory, on average, as Toyota and its suppliers (assuming the plants operate sixteen hours a day). While this may be an extreme example, clearly the savings from Toyota’s supplier investments in customized assets (i.e., site-specific investments in plants) can be substantial.

Of course, one must remember that these investments tend to bind suppliers to customers. However, JSPs work because these partner-specific investments that reduce costs and increase quality outweigh the costs (risks) associated with being dependent on outside parties. Thus, these investments expand the pie for both parties. As Deming notes, “A supplier assured of long-term contracts is more likely to risk being innovative and modify production processes than a supplier with a short-term contract who cannot afford to tailor a product to the needs of a buyer.”17

Forced Competition

The first two benefits explain why partnerships may be better than rotating business among a large number of suppliers. However, by vertically integrating, you get all of the benefits of fewer direct suppliers and customized investments. But vertical integration removes the supplier from the discipline of the market and essentially eliminates competition because the supplier has a captive customer base. The autonomy and incentives that keep the company innovating and focused on continuous improvement are lost. Moreover, numerous studies show that critical managerial and technical employees often leave small entrepreneurial companies after they are acquired.18 This does not occur in Japanese partnerships because they are structured to provide substantial incentives for the suppliers to continue to compete and innovate. They employ at least two important mechanisms so that suppliers continue to reduce costs and improve quality.

Assistance to the Weaker of Two Suppliers.

Previous researchers have noted that Japanese firms usually employ a two-vendor policy to force competition, even though they may forgo economies of scale.19 According to the 1990 International Motor Vehicle Program (IMVP) World Assembly Plant survey, the proportion of parts single-sourced by Japanese auto companies in Japan was 12.1 percent, while, due largely to a higher level of vertical integration, it was 69.3 percent for U.S. automakers.20 Thus Japanese automakers are less likely to rely on one supplier than U.S. automakers are. They maintain competition so that one supplier’s ability to generate cost or quality improvements provides an incentive for the other supplier to keep up. The intense competition often begins at the design stage when the automaker invites guest engineers from the two suppliers to work at the automaker’s technical center as part of the design team. The competitor engineers work in the same room during the initial design development. The automaker meets with each separately to review proprietary ideas and designs and eventually decides which supplier has a superior product design and cost, thus becoming the major supplier for the model. The losing supplier may become a secondary supplier for that model or may simply have an opportunity to develop a design for a different model.

The buyer can strengthen the incentives for cost or quality improvements by making the price paid (or volume given) to each supplier dependent on relative performance, like paying a bonus. The second-place supplier loses out on additional business and the bonus for good performance. However, the buyer does not abandon a weak supplier, but works with it to help it compete with the stronger supplier. A manager of an NEC supplier explained the process:

We were always in competition with another supplier to produce the lowest-cost, highest-quality circuit boards. NEC would often provide assistance to both of us by sending in teams of engineers to help us improve. We usually won the competition but NEC didn’t just give us all the business. Instead, it seemed like they renewed their efforts to help the other supplier compete. They would send in people to help them improve production methods. They would buy our technology and then share it with them. In short, they would try to help them to keep up with us. Of course, they praised and rewarded us for being their best supplier but they would always remind us that they could go elsewhere if we didn’t continuously improve.21

This practice of helping weak suppliers is not unusual in Japan. Toyota and Nissan have large supplier-assistance management consulting groups with specialized expertise that work full time — free of charge — with suppliers to help them improve their production techniques and achieve total quality, cost, and delivery. Both Nissan and Toyota have at least one consultant for every four to six suppliers. According to a Nissan internal consultant:

We will often expend additional resources to help the weaker suppliers improve their capabilities. To have really good competition between suppliers, their abilities should be about the same. However, if suppliers do not make changes and respond to our recommendations, then we suggest to the buyer that they cut back on their purchases from that particular supplier.22

Providing assistance to suppliers is a highly effective method for both helping and forcing suppliers to continuously innovate and improve to stay ahead of the competition. However, this puts tremendous pressure on suppliers to improve. In Japan, a commonly used phrase in the supplier community is Toyota jigoku (Toyota “hell”). Toyota jigoku refers to the process of working and negotiating with Toyota. Toyota is extremely demanding of suppliers and puts tremendous pressure on them to be more efficient. The result is that Toyota and its suppliers make 50 percent higher profit returns than U.S. automakers and their suppliers. Suppliers often feel indebted or obligated to the parent company, but they also have mixed feelings about the system. On the one hand, they sometimes feel that sharing the business with another supplier is inappropriate when they are clearly ahead in both cost and quality. Moreover, they have to share not only the business but also information or technology in order to help their competitor improve. On the other hand, since they realize that someday they may need such assistance, they view the system as insurance. Toyota or Nissan suppliers rarely go bankrupt because of the help they receive if they are experiencing difficulties. Only suppliers that are unwilling or unable to improve continuously are cut off completely, and suppliers will do almost anything to avoid such damage to their reputations.

Finally, in addition to giving the automaker a standard for comparison, keeping two suppliers on equal footing protects the buyer against unforeseen supply interruptions. And suppliers know that they cannot afford to have a strike or other interruption that would give the buyer a chance to immediately shift more business to the competitor — business that they may never recover.

Experience Curve Pricing.

According to McMillan, the Japanese recognize that, due to the experience curve described earlier, the supplier’s costs are expected to fall during the model life cycle. Thus, when initial prices are set, there is an experience curve-based “price path” set in advance that reflects a reasonable expectation of learning by the supplier.23 Our research on the automobile industry indicates that, in most cases, a specific price path is not set in advance. Instead, every six to twelve months, the customer usually negotiates a lower price based on how much it has been able to reduce costs during that period. The supplier is expected to reduce its price, but it is difficult to set in advance due to differences in market conditions, technology (e.g., maturity), and so on. U.S. automakers are much more likely to be price focused, meaning they put constant pressure on suppliers to reduce prices, regardless of whether the supplier reduces costs. Moreover, for a supplier to get a long-term contract, it must first agree to explicit price decreases each year. Conversely, Japanese automakers are much more cost focused, meaning they are constantly working with suppliers to reduce costs so that suppliers can afford to reduce prices. But they do not explicitly set those rates in advance because, in some cases of mature technology, the rate of cost reduction may be only two percent to three percent, while in other cases of new technology, it may be ten percent or more. What the automaker cares about is that the supplier is constantly improving and sharing its savings.

To share ideas on how to reduce costs or improve quality, Toyota suppliers often set up a jishuken (cooperation and assistance group) that includes other suppliers and consultants from Toyota. Since the suppliers conduct this continuous improvement activity without the Toyota purchasing organization’s knowledge, the improvements realized through jishuken activities accrue primarily to the supplier in the short term, and suppliers are highly motivated to improve (of course, suppliers must share those savings over the long term).

This method of forced competition and giving assistance typically produces more overall learning and innovation than would occur in a highly integrated, bureaucratic firm. Numerous research studies have shown that innovation is more likely to come from small firms than large ones.24 Developing partnerships rather than huge bureaucracies enables the Japanese to maintain a decentralized economy in which two-thirds of the Japanese labor force are in establishments with under 300 workers, while in the United States, two-thirds are in establishments with over 300 workers.25 Moreover, as Friedman observes, “From 1954 to 1977, the contribution of small and medium-sized firms to Japan’s manufacturing value-added rose from about 49 percent to 58 percent of total manufacturing. In contrast, small and medium firms accounted for approximately 35 percent of American value-added in manufacturing, a share that remained steady throughout the postwar era.”26 In short, during the past forty years, small manufacturers have become markedly more important throughout the Japanese economy. Perhaps this explains why Japanese firms are so good at rapid incremental innovation — there are thousands of entrepreneurs trying to make rapid, albeit minor, improvements to their products as they try to stay one step ahead of their roughly equal competitors.

Why Are Japanese Companies More Cooperative?

The Japanese have recognized the need to be interdependent (especially on highly complex tasks) and have responded by developing bonding mechanisms that build trust and goal congruence between companies. There are numerous competing theories on why the Japanese have developed networks of partnership firms. Perhaps the lack of an open market for corporate control in Japan explains why firms have not attempted to integrate more frequently. This suggests that the Japanese were forced to develop new organizational arrangements because of constraints on mergers and acquisitions. Also, the Japanese government has provided protection and financial support for small companies, thereby making it easier for small firms to be competitive.27 And finally, cultural reasons may explain the relationships among firms — they are simply an anomaly of a homogeneous and unique culture.28

The Japanese do not rely on legal contracts to protect their interests in exchange relationships. Indeed, Asanuma describes how Japanese firms use a flexible legal contract that is a very general “constitution” for a relationship and can be constantly adjusted and renegotiated.29 However, the key issue is understanding why Japanese companies can use such a flexible agreement. Next we discuss some of the most important Japanese practices in developing intercompany trust.

Stable, Long-Term Employment

Much has been written about the Japanese practice of long-term employment within one firm.30 Its importance in developing trust among individuals both within the firm as well as across firms cannot be ignored. There is real personal contact between the purchasing manager of Toyota and the manager or owner of a subcontracting firm. Naturally, you are more likely to trust someone with whom you’ve done business for a long period of time. It is much harder to build a trusting relationship with someone if you think they will be gone in six months, as happens in many U.S. companies. Hence, because people can develop long-standing relationships with their counterparts at the supplier or buyer, it is not surprising that the Japanese have developed significantly greater trust across firms.

Career Paths between Firms

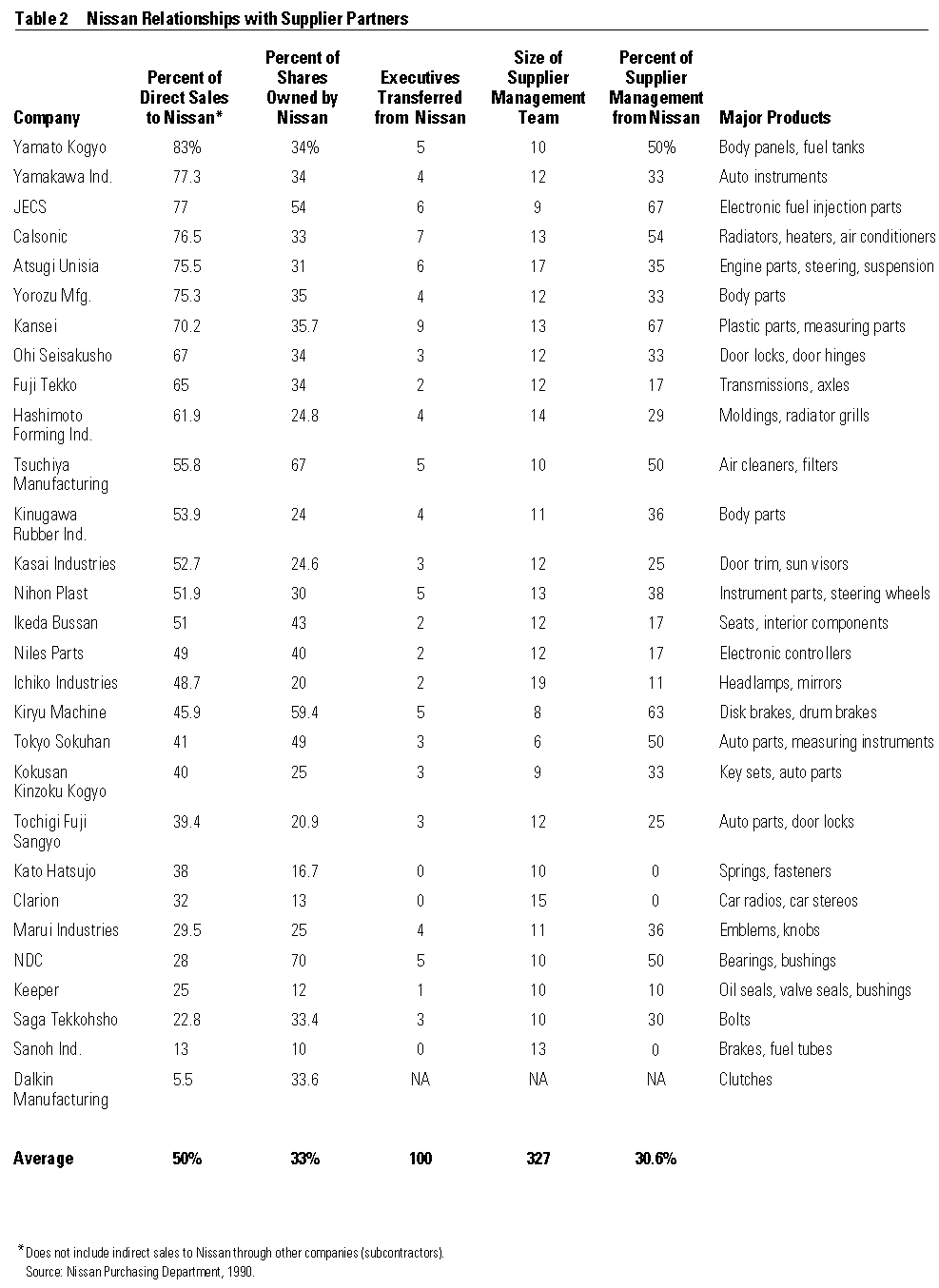

Another way that Japanese firms build trust is by requiring career paths in which employees transfer from firm to firm (or simply work at partner firm facilities). Employee transfers, both temporary (usually two years) and permanent, are common among business partners, particularly between large manufacturers and their subcontractors.31 Cusumano describes how executive transfers were particularly important in the auto industry because they “usually preceded technical assistance, loans, or exclusive procurement contracts.”32 He found that employee transfers preceded additional partner-specific investments by the automakers. Toyota is more likely to make investments in partners when it trusts the individuals it is dealing with — and who better to trust than former employees or people you’ve worked with for years? Our own study indicates that almost 30 percent of the top management teams at Nissan’s kankei-gaisha are former Nissan employees (see Table 2). Clearly, this innovative practice helps Nissan and its suppliers work cooperatively.

{kind=link}

In addition to permanent and temporary employee swaps, suppliers often send guest engineers to work at their customer technical centers on an ongoing basis. For example, Toyota currently has almost 350 guest engineers (mostly from supplier partners) at its main technical center in Japan. These engineers become a part of the design team and are given desks next to the Toyota engineers. Thus, supplier and automaker engineers jointly design the component for a new car model. Supplier engineers may work at Toyota’s facility for as long as two to three years.

This practice is not unusual in Japan. A U.S. manager working for Mitsubishi told us that, while working in Japan, each day he greeted a coworker who worked at the same facility. Six months later he discovered that the coworker didn’t work for Mitsubishi but for one of its suppliers. The manager said he “was astonished to find a supplier’s employee working at our facility every day just as though he worked for Mitsubishi. I’ve never seen anything like that in the United States.”33

Not only do these career-path practices help build trust between firms, but also transferred and guest employees are better able to understand how to optimize the efficiency of the value chain because they know both customer and supplier operations.

Face-to-Face Contact

Direct contact is much more important than other forms of contact in developing ways for employees to know and trust each other. Kankei-gaisha and automakers encourage a tremendous amount of face-to-face contact between supplier salespeople and engineers and between automaker purchasing agents and engineers. The kankei-gaisha in our sample had an average of 7,235 days per year of direct contact with automakers (including guest engineers). Conversely, the U.S. suppliers averaged 1,129 days of face-to-face contact with automakers. Thus, kankei-gaisha have almost seven times the direct contact with automakers, even when one does not include employee transfers.

Minority Ownership

Companies need credible commitments if they are going to be willing to make customized investments. Stock ownership in Japanese trading relationships represents commitments that firms have made to each other, and in many ways, it is an arrangement that is akin to an exchange of hostages. If I own a portion of a partner company, then I am less willing to try to take advantage of it because I am only hurting myself. Moreover, I benefit financially when the partner is successful. In Japan, “Equity shareholdings take on symbolic meaning in signifying relationships with other firms, rather than as straightforward investments for capital gain.”34 Japanese firms like Nissan, instead of vertically integrating, will either swap stock or take significant minority ownership positions in many key suppliers. Nissan owns 33 percent (on average) of the shares of its major supplier partners (see Table 2). This ownership stake builds trust and goal congruence between Nissan and its supplier partners. Interlocking stock ownership represents a commitment to the supplier that needs an incentive to make the customized investments Nissan requires.

Specialized Investments

As previously mentioned, Japanese auto suppliers develop more unique parts for their customers and make greater investments in specialized assets than do U.S. suppliers. A kankei-gaisha does not receive a separate payment for the investment in tools, dies, molds, and jigs that are highly customized (because they “touch the part”) and would need to be scrapped if the automaker cut off orders to the supplier. (In contrast, U.S. suppliers require that U.S. automakers buy the customized tools, dies, and molds that the supplier uses to make the product.)

Executives at twenty-eight kankei-gaisha indicated that, on average, 31 percent of their total investment in capital equipment could not be redeployed to products for other customers if they were prohibited from selling to their primary customer. Executives at thirty-one U.S. suppliers indicated that only 15 percent of their capital equipment investment could not be redeployed. Thus, kankei-gaisha are much more dependent on their primary automaker.

Moreover, as previously mentioned, kankei-gaisha manufacturing plants are built close to the customer and are largely dedicated to a specific customer. The average distance between a kankei-gaisha plant and an auto-maker plant is forty-one miles in Japan (eighty-seven miles in the United States), and an average of 61 percent of output is dedicated to a specific customer. (In comparison, U.S. supplier plants are an average distance of 521 miles from their primary automaker plants.) Clearly, the suppliers’ specialized capital investments make them highly dependent on the automakers, with the real possibility of opportunistic exploitation.

However, automakers are also significantly dependent on kankei-gaisha. Most kankei-gaisha parts are “black box,” meaning that the automaker provides only very general specifications while the supplier does all of the detailed functional specifications and blueprints. Consequently, suppliers have significantly more knowledge about the design and manufacture of the part than does the automaker. Because kankei-gaisha black-box parts are customized to a specific model, the automaker is highly dependent on the supplier. If the supplier did not perform as desired, the automaker would have difficulty simply shifting business to another supplier, given the product’s customized nature. Some kankei-gaisha claim that they do not provide the carmakers with all of the specific functional details when they submit their design drawings for approval (although they admitted they would if the automaker insisted), but intentionally leave out certain important details such as tolerances. Because the automaker does not know the part’s exact design specifications, it is difficult to change suppliers, resulting in the automaker’s dependence on the supplier. One kankei-gaisha executive states, “They can’t really move business away from us very easily. They need us for our skills, just as we need them.”35

Under these conditions, each party makes substantial specialized investments, which creates a composite profit stream only if the transactors continue working together. If the relationship is terminated, each party loses some portion of the rent. Thus these specialized investments create interdependence, which in turn creates incentives to cooperate.

What Are the Implications for U.S. Businesses?

What does all this mean for U.S. managers? U.S. companies need to develop a capability for partnering or be at a competitive disadvantage. The question is whether the Japanese partnership approach is adaptable to U.S. companies or is uniquely “Japanese.” The answer is that we can adapt the partnership approach to our environment in the same way that we are learning Japanese production practices. For example, Toyota has worked successfully as a partner with Flex-N-Gate, a bumper maker, and Johnson Controls Inc. (JCI), a seat maker. Both U.S. companies have allowed Toyota consultants to spend weeks with their organizations teaching them how to improve their operations and work closely with Toyota. Both have made significant changes in their production systems. Both have incorporated Toyota’s just-in-time system. And both claim that the Toyota model of working with suppliers is far superior.

The results speak for themselves: Flex-N-Gate has reduced die-change time from forty-seven minutes to twenty-two minutes, and a bumper that used to take three days to produce now takes only forty-two minutes. Overall, Flex-N-Gate has more than doubled productivity while cutting lead times 94 percent, inventories 98 percent, and defects 91 percent.36 JCI’s Georgetown plant (just down the road from Toyota’s Georgetown assembly plant) operates at almost one-half hour of inventory. The entire process of ordering, seat assembly, shipping, and installation into the Camry takes a little over three hours. JCI makes complete seats only for Toyota. According to JCI general manager Don Buchenberger, “Toyota took a close look at our metals operation, and we began making changes. At one time, we had a thirty-two-day inventory in metals. Now it’s seven days. . . . The Toyota supplier technical support group taught us about quick die change. The savings over the old way are immeasurable.37

Perhaps most important is the trust and cooperation building between Toyota and these suppliers. According to Jeffrey Smith, JCI’s Toyota account executive, this kind of cooperation has built a depth of trust he has not seen anywhere else: “We’ve spent $10 million preparing for the 1992 Camry model change, without a single purchase order. I don’t know that we’d do that with any other customer.”38

Other U.S. firms are making progress. Xerox has lowered costs and increased quality by reducing its suppliers from 4,000 to 500, while imitating many features of the Japanese approach. Chrysler, Ford, Boeing, and other U.S. companies are starting to do the same. However, to effectively utilize partnerships, U.S. managers must learn the following lessons:

- Don’t overintegrate. In cases where all things appear equal, you should probably show a preference for outside production. Extensive vertical integration often leads to less innovation and world-class underperformance. In short, U.S. managers must recognize their dependence on those individuals and companies outside their organization who have the ability to supply key inputs and perform key tasks more efficiently and effectively than they do.

- Reduce the number of direct suppliers to reduce costs and increase quality through greater economies of scale and less variation in inputs.

- Make customized investments to optimize the value chain and tailor the system to meet customer and supplier needs. Investments in customized assets can create significant economic value when information is openly shared, problems are continuously identified and solved, and a see-through value chain is created.

- Force suppliers to compete and reward superior performance. Moreover, help your weaker suppliers improve so that they will continue to provide competition to your stronger suppliers. Work with partners as a consultant to solve problems jointly and improve productivity.

- Protect investments by building trust. Whether it be through stock swaps, interfirm employee transfers, flexible contracts, or other mechanisms, find ways to trust each other while making customized investments to reduce costs and improve quality.

Of course, many will argue that these practices simply won’t work in the United States because we’re “different.” But much of what has made Japanese corporations successful is transferable to U.S. companies. Indeed, Japanese firms operating outside Japan have been able to achieve roughly equivalent productivity in their U.S. plants. Toyota’s relationships with Flex-N-Gate and JCI suggest that JSPs can work in the United States. The challenge for U.S. firms is to learn from the Japanese in order to gain the advantages of Japanese-style partnerships. But we must adapt them — as the Japanese have adapted our best practices — to fit the requirements of our environment. If we fail to learn from Japan’s subcontracting structure, we may continue to give Japanese companies the competitive edge they need to win in the global marketplace.

Appendix

The data and insights for this paper come from two Japanese and two U.S. automakers and a sample of 143 of their suppliers. Each automaker’s purchasing department selected fifty suppliers for study, twenty-five of which were identified as “partnerships” or “most like a ‘keiretsu’ relationship.” (In the Japanese automakers’ case, these twenty-five companies were “kankei-gaisha” or “affiliated companies,” as in Nippondenso’s relationship with Toyota.) The other twenty-five suppliers were identified as those suppliers with whom the automaker had “traditional arm’s-length relationships.” (In the Japanese automakers’ case, these were “dokuritsu-gaisha” or “independent companies” like Bridgestone or Yazaki.)

We then interviewed sales and engineering vice presidents at fifty of the suppliers (twenty Japanese and thirty U.S. suppliers) and developed a survey. The survey was then sent to the sales vice president or president (the person the automaker identified as most responsible for managing the day-to-day relationship) of the entire sample of 200 suppliers (100 Japanese and 100 U.S. suppliers). Usable responses were received from seventy-six Japanese suppliers (a 74 percent response rate) and sixty-seven U.S. suppliers (a 67 percent response rate).

In addition, we also asked the automaker’s purchasing agent most responsible for the supplier relationship to complete a survey to give the automaker’s perspective. Purchasing agents for 194 of the 200 suppliers provided usable surveys.

References

1. Ministry of International Trade and Industry, White Paper on Small and Medium Enterprises in Japan (Tokyo: MITI, 1987), pp. 36–37.

2. World Motor Vehicle Data (Detroit, Michigan: Motor Vehicle Manufacturers Association of the U.S., Inc., 1991), p. 14.

3. Bain & Company, unpublished automotive study, January 1985.

4. A.B. Fisher, “Behind the Hype at GM’s Saturn,” Fortune, 11 November 1985, pp. 34–46.

5. “Shaking up Detroit,” Business Week, 14 August 1989, pp. 74–79.

6. K.B. Clark and T. Fujimoto, Product Development Performance (Boston: Harvard Business School Press, 1991), p. 40.

7. K.B. Clark, “Project Scope and Project Performance: The Effect of Parts Strategy and Supplier Involvement on Product Development,” Management Science 35 (1989): 1247–1263.

8. Bain & Company, unpublished automotive study, January 1985.

9. J. McMillan, “Managing Suppliers: Incentive Systems in the Japanese and U.S. Industry,” California Management Review, Summer 1990, p. 51.

10. Author interview with GM executive, 23 March 1991.

11. P. Ghemawat, “Sustainable Advantage,” Harvard Business Review, September–October 1986, p. 53.

12. Author interview with the sales vice president of a Toyota supplier, 9 September 1992.

13. S. Helper, “Automotive Supplier Relations: Results of 1989 Survey,” IMVP International Policy Forum, May 1989.

14. M. Walton, The Deming Management Method (New York: Perigee Publishing Group, 1986), p. 62. From Dr. Deming’s diary, “Travel Logs, Around the World by Air,” 1946–1947, p. 88.

15. J.P. Womack, D.T. Jones, and D. Roos, The Machine That Changed the World (New York: Harper Perennial, 1990), p. 160.

16. Ibid.

17. Walton (1986), p. 64.

18. J.P. Walsh, “Top Management Turnover Following Mergers and Acquisitions,” Strategic Management Journal 9 (1988): 173–183.

Walsh finds that “turnover rates in acquired top management teams are significantly higher than ‘normal’ turnover rates, and that visible, very senior executives are likely to turn over sooner than their less visible colleagues.” [p. 173]

19. T. Nishiguchi, “Strategic Dualism: An Alternative in Industrial Societies” (Oxford, England: Oxford University, Neffeld College, Ph.D. Diss., 1989), pp. 154–227; and

McMillan (1990), pp. 46–47.

20. From the 1990 IMVP World Assembly Plant Survey, reported in Womack et al. (1990), p. 157.

21. Author interview with NEC supplier manager, 23 July 1991.

McMillan (1990, p. 50) notes that a small number of bidders does not necessarily create a bargaining/contracting problem. “The fierceness of bidding does not depend on just the number of bidders. There is a more subtle determinant of bidding competition. If each of the bidders is roughly equally efficient at doing the job, the bidding competition is aggressive even if only two bidders compete.” McMillan claims that this is why it is in the large Japanese manufacturers’ interest to provide technical assistance to its potential suppliers to keep them on roughly equal footing and ensure that each of them is using efficient techniques.

22. Author interview with Nissan purchasing manager, 22 October 1992.

23. McMillan (1990), p. 47.

24. D.L. Birch, Job Creation in America: How Our Smallest Companies Put the Most People to Work (New York: Free Press, 1987), pp. 6–22; and

J. Jewkes, D. Sawers, and R. Stillerman, The Sources of Invention (New York: St. Martin’s Press, 1959).

25. T.J. Pempel, Policy and Politics in Japan — Creative Conservatism (Philadelphia: Temple University Press, 1982), p. 20; and

M.J. Smitka, Competitive Ties: Subcontracting in the Japanese Automotive Industry (New York: Columbia University Press, 1991), p. 206.

26. D. Friedman, The Misunderstood Miracle: Industrial Development and Political Change in Japan (Ithaca, New York: Cornell University Press, 1988), p. 35.

27. Nishiguchi (1989), pp. 84–151.

28. R. Dore, “Goodwill and the Spirit of Market Capitalism,” British Journal of Sociology 34 (1983): 459–482; and

McMillan (1990), p. 40.

29. B. Asanuma, “The Contractual Framework for Parts Supply in the Japanese Automotive Industry” and “The Organization of Parts Supply in the Japanese Automotive Industry,” Japanese Economic Studies 15 (1985a&b): 32–78; and

S. Kawasaki and J. McMillan, “The Design of Contracts: Evidence from Japanese Subcontracting,” Journal of the Japanese and International Economies 1 (1987): 327–349.

30. W.G. Ouchi, “Markets, Bureaucracies, and Clans,” Administrative Science Quarterly 25 (1980): 124–141.

31. M. Gerlach, “Business Alliances and the Strategy of the Japanese Firm,” Organizational Approaches to Strategy, ed. G. Carroll and D. Vogel (Berkeley: University of California, 1987), pp. 127–143.

32. M. Cusumano, The Japanese Automobile Industry: Technology and Management at Nissan and Toyota (Cambridge, Massachusetts: Harvard University — Council on East Asian Studies, 1985), p. 242.

33. Author interview with Mitsubishi manager, 14 October 1990.

34. Gerlach (1987), pp. 127–143.

35. Author interview with Mitsubishi manager, 14 October 1990.

36. J.B. Treece, “The Lessons GM Could Learn for Its Supplier Shakeup,” Business Week, 31 August 1992, p. 29; and

M. Blake, “The Evolution of an American Business,” Synergy, a publication of Toyota Motor Sales, 1991, pp. 4–7.

37. “Sitting Pretty,” Synergy, 1991, p. 13.

38. Ibid.