Beefing Up Operations in Service Firms

A national preoccupation with U.S. international industrial competitiveness, driven by our continuing enormous balance of payments deficit, has tended to focus media and political attention during the 1980s on manufacturing. A torrent of books and articles has inundated business managers, offering guidance on how to improve manufacturing performance. Terms like “world class manufacturing” and “dynamic manufacturing” sprinkle discussions in college classrooms, corporate boardrooms, and the halls of Congress. The concept of “manufacturing strategy,” considered somewhat esoteric only a few years ago, gets increasing attention from both top managers and academics.

There is, however, another battlefield of economic competitiveness where operations effectiveness is just as crucial to success as it is on the factory floor. This less visible battlefield is that huge, ill-structured arena called the “service sector,” which employs 76 percent of our workforce and accounts for 68 percent of our real GNP. It is also, unfortunately, a sector––comprising activities such as banking, engineering, transportation, communication, and myriad others––whose trade surplus went negative for the first time in mid-1989 and is now barely in the black.

We have no quarrel with the assertion that the United States needs a strong manufacturing base in order to maintain and improve its standard of living. But we have to get serious about service competitiveness as well. Just as our machine tool and semiconductor industries should have studied the successful attacks of foreign steel, auto, and consumer electronics producers on our domestic market-and prepared themselves for similar onslaughts–so should our service industries study and learn from our manufacturing sector’s decline. Those manufacturing firms that have remade themselves or sustained their leadership position have shared a common approach: they have focused attention on their most important markets and then mobilized their operations organization, through a well-planned strategy, to squarely meet those markets’ needs.

In this article we will discuss how to make operations in service organizations more competitive. We will examine ideas that have emerged from successful manufacturers and outstanding service firms. Our key conclusions are that service firms, like manufacturing firms, can structure their operations according to a four-stage model of competitiveness and that they can apply the manufacturing strategy concepts of ocus and integration as they move from lower to higher stages.

Before developing this perspective, however, it is useful to first review some basic concepts.

Service Firm Management: The Basics

Service firm management, especially of operations, is best understood within the context of three key constructs.

The Strategic Service Vision.

The strategic service vision is “the logically organized plan for implementing new businesses and ideas.”1 It consists of four elements: a target market (Who is our intended customer?), a service concept (What are the most important elements of our service from the customer’s perspective?), a competitive strategy (How will we differentiate ourselves from our competitors?), and a service delivery system (How will we provide this differentiated service?).2

The vision focuses on the customer’s perceived value of the service. To remain competitive, a service firm must consistently meet or exceed customers’ expectations of value—the price they pay relative to the quality and convenience of the service they receive.

Levels of Service.

The core service is the essential set of services that the firm must provide just to participate in its market. Peripheral services facilitate the core service or are expected features of the service bundle. Amenities are add-ons that are not essential to the core service but that might sway a customer’s buying decision.

An airline’s core service, for example, is getting someone from one place to another. Its peripheral services include its reservation and baggage handling systems, while amenities consist of such things as cabin food service and in-flight entertainment. As a general principle, the firm must provide basic competency in core and peripheral services to survive. No amount of add-ons can save a firm that is clearly deficient in these dimensions. Put another way, the core and primary peripheral services define the lower limit of customer expectations about performance.

The Operations Function.

In service firms, operations consists of two quite different spheres of activity. One sphere is the service encounter or cycle of encounters between the customer and the organization. The medium by which these encounters are carried out (i.e., face-to-face, by phone, or by electromechanical device) constitutes the firm’s service delivery system. The other sphere encompasses those activities that take place behind the scenes and constitute the “back office” support system. These involve such tasks as processing paperwork, cooking a restaurant meal, or taking baggage off of a plane. These latter activities are analogous to the production processes in the factory— working on things rather than people. The existence of these two spheres of activity and, more important, the emphasis on the encounter as the core output function in most service organizations are what differentiate services from manufacturing.3 The extent to which value is added in the front office rather than the back office often distinguishes one service business from another and determines structure and staffing of the operations organization itself.

An Operations Framework

Regardless of a firm’s particular competitive strategy, senior management needs some framework for relating operations’ activities to the firm’s overall service performance. This is so for several reasons. One is to help pinpoint the key elements that must be addressed in the strategy development process itself Another is to help position the firm’s operations relative to competitors. The final and most compelling reason, in our opinion, is to provide a current perspective and future vision that can be communicated to the organization’s members. The questions “where are we now?” and “where do we want to be?” are more easily answered if they can be related to even a rough performance classification.

The classification we propose for addressing these issues is the four-stage scheme depicted in Table 1. This scheme distinguishes among service firms according to their general effectiveness in service delivery at different stages of their development. Accompanying each stage are the management practices and attitudes that, based upon our experience, generally indicate how service firms at each stage deal with key operations issues. (An analogous framework, developed by Wheelwright and Hayes, is widely used to analyze the role of operations in strategy development for manufacturing firms.4)

Before discussing the stages, we must consider two issues. First, the stage attained by a firm at any given time is a composite. Every service delivery system embodies a unique set of choices about such factors asservice quality, role of the back office, workforce policies, and the like. A company may fall at a different point along the continuum for each category or have some organizational units that are further or less advanced than others. What determines the firm’s stage is the overall balance among these different positions —where, in a sense, the firm’s center of gravity lies.5 In defining this center of gravity, the model assumes a weighing of each dimension’s relative importance. Thus a firm can achieve Stage 3 or possibly Stage 4 status, even if it is not outstanding on all dimensions, providing that it is clearly superior on the critical success factors for its industry. An example here is UPS, whose mastery of its core service, through its technology and back office capabilities, enables it to “go global” and compete effectively on price. It does not, however, do a particularly good job at tracking overseas shipments, nor does it excel in its service quality practices. Thus, in our view, it averages out to a Stage 3 company.

Second, it is difficult, if not impossible, for a company to skip a stage in its quest for world class status. A company obviously must achieve journeyman performance levels before it achieves distinctive competence, and distinctive competence is a necessary foundation for becoming world class. This does not mean that a company can’t pass through a stage in a relatively short time, however. Scandinavian Airlines Systems (SAS) moved from Stage 1 to Stage 3 in about a year and a half After Suffering a huge operating loss in fiscal year 1979–1980, its CEO, Jan Carlzon, instituted a program involving some 120 service improvements designed to help it become the airline of choice for its selected target market, the full-fare business passenger. The improvements focused on achieving exceptional on-time performance and excellent service by all personnel. By January 1982, SAS had the best on-time record in Europe, and in August 1983, Fortune named it the best airline for business travelers in the world.6

At the same time, companies can very easily slide back a stage. This can come about gradually, typically from losing touch with the market, or overnight as the result of a widely publicized service failure. An example of a gradual decline is that of Sears, whose complacency and bureaucratization have made them play catch-up in everything from pricing to customer service. An example of an overnight downfall is the case of the Los Angeles Police Department, which was nationally recognized as a leader in policing practices prior to the Rodney King incident in the spring of 1991.7

Also, while it is appealing in theory for a service firm to move as a single entity through these stages, the sheer size of major companies precludes immediate across-the-board shifts. Even when a company has developed a clearly defined new service delivery system and debugged it on a pilot basis, getting it operational can involve months of retraining, extensive systems work, and so forth. Woolworth takes a couple of years to test its new store concepts; Burger King runs extensive experiments in its R&D lab.

Often, people assume that new technology will put them on the fast track through the four stages. However, we know of no firms that have leapfrogged a stage solely by relying on a new technology. A new fleet of planes, a new telecommunications system, or a new point-of-sale scanning system may be necessary for “upstaging,” but innovation can’t do the job overnight—or alone. For example, while American Airlines and the American Automobile Association have achieved their dominant industry positions through aggressive use of information technologies, effective integration required major managerial and procedural refinements over the course of many years. Likewise, implementation of Fidelity Investment’s Investors Express package, which allows active traders to initiate security trades from their personal computers, and Mrs. Field’s Cookies’ computerized point-of-sale inventory tracking system worked because appropriate infrastructures were already in place.8

With these points in mind, we now consider the stages themselves.

Stage 1: Available for Service

Service firms that fall into this category tend to consider their operations organizations “necessary evils.” They often see operations’ mission as almost totally reactive: to deliver the service that some other person or group in the company has defined and to deliver it in the manner specified. Thus management pays little attention to how other firms, whether direct competitors or not, design and manage similar service delivery systems. It assumes that if operations can do what it is supposed to do, without major disruptions, the firm will be able to make a profit. The major guidance given operations, therefore, is “don’t screw up.”

In order to keep costs down, operations receives minimal back office support. The company makes little investment in specialized equipment, and it staffs operations with people who have marginal skills—and who are therefore willing to work for relatively low wages. Constantly looking at the bottom line, management designs operations jobs that require little skill or creativity, and it provides almost no training. Few people advance out of operations into another function or into general management, so operations tends to be regarded as a dead end. Thus supervisors must continually monitor and direct frontline staff, and there is a high rate of turnover. Moreover, because operations employees acquire only limited skills in their jobs, they seldom can achieve major advancement by transferring to other companies. Ironically, as in the case of the banking industry, efforts to cut labor costs frequently result in higher total costs because of the need to fix quality problems.

The companies that fit this mold tend to be either relatively young firms that offer a new or unique service or those that serve a niche market (often one based on minimum service at a minimum price).

Stage 2: Journeyman

The problem with niches is that one usually outgrows them, or they grow to the point where other companies decide to move in. Therefore, after maintaining a sheltered existence for some time, Stage 1 firms often find themselves coming into direct competition with other companies that offer similar services in the approximate geographic area. No longer can they simply ask operations to get the job done; they must seek feedback from their customers on the relative cost and perceived quality of their service, and ensure that they are not penalizing themselves unduly through idiosyncratic approaches, such as odd business hours or complicated credit procedures.

The goal becomes: “Don’t let our competitors gain too much of an advantage over us.” And the firm begins to adopt industry practice in its operations. Instead of reacting to internal directives, operations reacts to external practices, particularly in its back office (which usually is trying to minimize cost no matter what service priorities the front office identifies).

Over time, such companies’ operations organizations tend to look more and more like those of their competitors. They build similar facilities, use similar equipment and systems (often purchased from the same equipment or software suppliers), purchase materials or ancillary services from the same suppliers, adopt similar management practices, and routinely even hire workers and managers from competing firms. Such people blend into their new environment almost immediately because it is so much like their previous one, and even use many of the same procedures. Line management’s role is to ensure that workers faithfully follow the procedures established by top management; improvisation is not encouraged. (Stage 2 companies, like Stage 1 companies, are not big on worker empowerment.)

In effect, companies that have adopted a Stage 2 approach have agreed not to compete against each other in terms of operations effectiveness; they all operate essentially the same way. (Quickly, can you name any difference in service between, say, J.C. Penney and Montgomery Ward?) Instead, they compete, often quite vigorously, along other dimensions: breadth of product line, advertising, and financial incentives. Management still regards operations employees as specialists, and therefore they have limited upward mobility. They do have more mobility between firms, however, and as a result begin to acquire an industry orientation. In fact, their allegiance to their industry profession, often quite narrowly defined, usually surpasses their allegiance to the particular company they happen to work for at any given time.

In summary, the challenge confronting Stage 2 firms is keeping pace with competitors that do just as good a job in the core service and that raise the ante by excelling on service quality or by providing peripheral services that have real value to the customer. This problem faces upscale retail department stores such as Bullocks, Saks, and Robinson’s, in the wake of Nordstrom’s legendary customer service. An equally effective service system may take months or years to duplicate. It is a fragile structure in which the competitive edge is often the invisible internal capabilities and organizational culture rather than the visible Steinway Grand on the mezzanine.

Stage 3: Distinctive Competence

In a Stage 3 firm, senior management has a clear vision of what creates value in the customer’s eyes, and it designs operations carefully to deliver that value. Richard Rosenberg, CEO of Bank of America, saw value as providing one-stop shopping, in this case, one account that bundled checking, savings, and safe deposit privileges at a price that was cheaper than getting them individually. The burden fell on virtually every part of the operations organization to convert this vision into reality, which it did with great success.9

The operations organization in a Stage 3 firm also reflects a coherent operations strategy, that is, making consistent choices for each element in Table 1 relative to price, quality, flexibility, and convenience objectives. Operations also provides the tactics and leadership to implement the strategy. Relative to service quality, for example, operations is the typical advocate of a Total Quality Management philosophy, and it assumes the lead role in implementing service guarantees and service enhancing technologies, and fostering worker empowerment. Federal Express is probably the classic example of a company that relies on its operations personnel to push, as well as execute, actions in these three areas.

These innovations are especially practicable because Stage 3 firms have, by definition, mastered their core service. They understand the essential strengths and limitations of their operations and are well aware of the careful analysis that must precede change. First Interstate Bank of California, for example, spent three years shaping up its back office operations and its branch operations before it launched its five-point service guarantee.

The achievement of distinctive competence, however, can bring certain personnel problems. Workers whose responsibilities in Stage 2 companies were limited to following set procedures are now encouraged to take initiative and make choices among alternative procedures. Delta Airlines goes even further. It encourages all of its employees to learn multiple jobs in order to prepare themselves for advancement and to appreciate the problems and jobs of the other guy.

The challenge for operations, and for the whole firm at this stage, is to assure that the operations strategy remains supportive of the rest of the company, particularly marketing. At the same time, sales, marketing, and product development must be open to new service initiatives that operations personnel propose.

Stage 4: World Class Service Delivery

The ultimate stage represents an apparently natural extension of Stage 3, but a traditionally managed company will probably find this the hardest transition of all. The company must develop the capabilities and credibility of its operations organization to the point where operations becomes proactive, forcing higher performance standards on the whole company, identifying new business opportunities, and helping redefine the firm’s competitive strategy. Rather than simply investigating customer needs and attempting to fulfill them, Stage 4 companies (e.g., Disney, Four Seasons Hotels, and Singapore Airlines) seek to create needs, establish expectations, and continually expand those expectations. They define the quality standards by which their competitors are judged.

Customers, in fact, become consultants, sources of ideas as well as revenue, as in the case of CIGNA’s Customer Advisory Board. Competitors provide stimulation as well as pressure. The company bases its performance standards not on its own historical achievements, but on the performance achieved by its best competitors around the world, that is, it does competitive benchmarking. It designs controls and rewards to motivate continuous improvements upon those standards, and it gives employees the tools and training to achieve them. NYNEX, for example, offers its employees the Chairman’s Award for World Class Service and provides extensive training in process management to help them attain it.

The company’s view of technology undergoes a similar transformation. Rather than being simply a means for cutting costs and removing people, it becomes a potential means for developing competitive advantage, making it possible for the organization to do things its competitors can’t do. The company worries less about technological risk than about losing the first mover advantage. For example, some leading firms have adopted an “informate and automate” strategy to let the customer know vital information and to facilitate the server’s job. Hertz has established business centers at some airports that are equipped with flight monitors providing the latest information on airline schedules and departure gates, and handouts that provide driving directions in five languages. Faster service is facilitated by personnel using hand-held computers to print receipts in the parking lot so that customers don’t have to go to the counter when returning cars.

Workers in Stage 4 companies become “company men and women” in the best sense. They are “Marriott people,” “Southwest Airlines types,” and “Home Depot folks.” Their identity with the company they work for often matches or even exceeds that with their alma mater or hometown team. Like production employees of world class manufacturers (the Millikens, Xeroxes, and Motorolas), operations employees of world class service firms, no matter what their job, know they are working someplace special and doing something valued by the company. Indeed, just as the Honda janitor sweeping the floor is “building cars,” the Disney Maintenance Host sweeping the lot is “helping the guests enjoy their day at the Park.”

Of course, managers of such companies also have tremendous pride in the organization’s service and appreciate the centrality of operations in providing it. Often such firms regard an outstanding service delivery system as so important that operations experience is considered essential to one’s upward mobility. In a similar vein, it is common for senior executives who run Stage 4 firms, in order to maintain their feel for operations as well as staying close to the customer, to spend time “in the trenches.” Bill Marriott, Sr., often took a turn at the registration desk, and the CEO of Columbus’ Riverside Methodist Hospital, a leader in health care service quality, occasionally works as an orderly. The president of Swissair has been seen dispensing boarding passes and has instructed all managers of the airline, regardless of function, to spend one day a month dealing directly with customers.

A world class operations function has two major challenges. One challenge is sustaining superior performance at every point in its service delivery system and throughout its service network, as service firms often are judged more by the performance of their weakest links than by the things they do especially well. To be world class, therefore, all organizational units must meet impeccable standards of service and productivity.

The other major challenge, especially for multisite services, is managing the increasing complexity of personnel recruitment, training and motivation, technological innovation, and communication as the firm grows. Operations’ ability to reproduce and manage its proven system in highly diverse cultural settings— McDonald’s in Moscow—ultimately determines the firm’s permanence, literally, as a world class competitor.

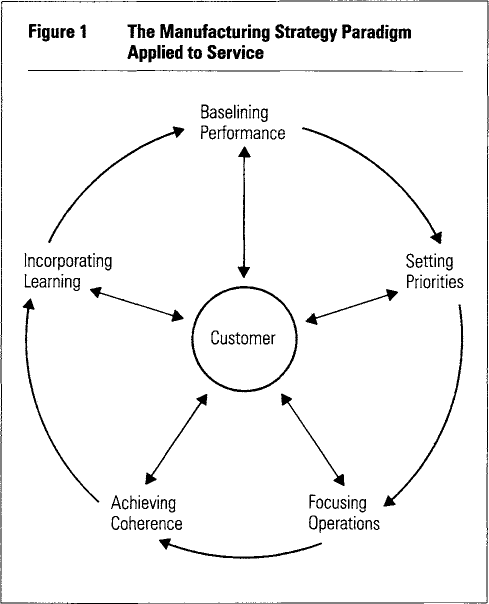

The Manufacturing Strategy Paradigm Applied to Service

The concept of manufacturing strategy has been around for over twenty years, but only in the last decade has it received serious consideration from academics and practitioners. The strategy is based on the widely observed rule that general purpose systems, like general purpose tools, are seldom as effective as those that are designed and managed for a specific purpose.10 Therefore, a company must begin designing a manufacturing system with a careful, and broadly shared, assessment of how the firm will compete in a particular industry—in what respects will its products and services be distinctive? Once the company establishes its competitive priorities, the paradigm provides an orderly approach for examining the organization’s structure (facilities and equipment) and infrastructure (policies and systems) to determine if they are consistent with those priorities. If inconsistencies are detected, the paradigm also provides guidelines for making appropriate alterations. The term “manufacturing strategy” encompasses the whole process: setting competitive priorities, making structural and infrastructural decisions, and establishing a discipline (such as the notion of focused factories and plant charters) for ensuring that the structure and infrastructure remain consistent with the priorities.

We can easily adapt the same framework to service companies, although we must make a few modifications to accommodate the differences between services and manufactured products. For our purposes, the key difference is that, for the service firm, the customer encounter with the system is the focal point of all operations activities.

Planning the Transition

Assuming that the service company is a going concern and knows how it will compete in its industry, management may move around the wheel in Figure 1— baselining operations’ performance, setting priorities, focusing operations, achieving coherence, and incorporating learning—with each step linked to customer requirements.

- Baselining performance is determining the operating system’s success on those things that are important to the customer, both by itself and in comparison with its competitors.

A useful tool for this purpose is performance-importance mapping. This involves gathering information, typically via customer surveys, on each aspect of service delivery and placing it on a grid (see Figure 2).

In this example, we have plotted factors of importance to bank customers. The map shows that customers value short lines and think this bank’s lines are too long. Customers do not value extended hours, and the bank apparently does not provide them. Customers believe statement accuracy is very important, and they think the bank performs very well in this area.

The second part of baselining is comparing oneself with the competition. One could plot a similar grid showing on one axis selected competitors’ performance relative to the bank and, on the other, importance to customers. When a company performs about the same as the rest of the industry on important elements, strategists call this “qualifying to compete.” When it performs better on important elements, strategists call this “order winning.” When it performs better than competitors on an unimportant element, we refer to it as an “air ball”—essentially a waste of effort and resources. Performance that is worse than that of the industry on important elements is generally termed “order losing,” and obviously requires urgent action.

- Setting priorities for manufacturing operations boils down to choosing on which specific delivery attributes to excel: cost-price, flexibility, quality, or dependability. Services have to make similar choices, each of which has direct implications for the service delivery elements shown in Table 1. Here we encounter the notion of trade-offs. The company must choose not only a limited set of things to do well, but it must choose the right set. And it must be precise. As manufacturing strategy pioneer Wickam Skinner observed in 1969, “The variables of cost, time, quality, technological constraints, and customer satisfaction place limits on what management can do, force compromises, and demand an explicit recognition of a multitude of trade-offs and choices. Yet everywhere I find plants that have inadvertently emphasized one yardstick at the expense of another, more important one.”11 This is a key lesson for service executives as well. The priority-setting process must stem from the findings of the performance-importance baseline analyses just described. If short lines have a higher priority to the bank’s target customer than extended hours, then labor use must be adjusted accordingly. The trade-off is between flexibility (of access to the service) and speed.

- Focusing operations requires aligning the operating system, operations personnel, and facilities with the performance priorities. Lens Crafters’ priority is speed, so it targets all of its equipment and procedures toward fast turnaround; H & R Block’s priority is low cost, so its operating system is geared to volume; First Wachovia Bank and Trust of North Carolina emphasizes relationship banking, so its operating system excels at database management; and Andersen Consulting, which prides itself on being able to provide consulting anywhere in the world at the drop of a hat, focuses its operating organization on getting its consulting staff quickly into the field.

In manufacturing, focus calls for organizing factories according to the product’s specific processing requirements. The essential issue is whether to design for high volume, standardized products using dedicated machines and specialized workers, or low volume, customized products using flexible equipment and broadly skilled workers. Matching the right equipment to the product is critical for services as well. Kentucky Fried Chicken got into trouble a few years ago by not recognizing this when it introduced spareribs. The problem was that its technology and operating system were designed around frying and pressure cooking, not barbecuing. The result: soggy ribs served by frustrated workers.

Designing focused operating units for service companies presents some unique problems. One problem is that customers don’t like to be treated as high-volume products, even when the cost is low. Another is that the typical direct service worker is often ill prepared in skills and policy knowledge to effectively customize a service.

Service companies that lose focus, like their brethren in manufacturing, fail due to one or more of the following reasons:

- Corporate management has not clearly spelled out the operations task; it’s excessively general. This results in trying to do everything “a little bit well.”

- Overly ambitious marketing programs have made promises that operations can’t keep. For example, an airline billboard ad several years ago showed flight attendants lavishing personal service on passengers flying coach in a 747.

- The priorities are inconsistent. For example, a company tries to provide highly personalized service and high volume, low-priced service in the same facility.

- Service products have proliferated out of control. Too many items on the fast food menu, too many services sold by the consultant, and too many products, rates, and terms offered by banks lead to unfocused operations.

- Achieving coherence in the operating system means that the individual components are mutually reinforcing, all contributing to the organization’s goals. The Benihana Restaurant operating system is a classic example. Everything from the chef pacing the meal by serving directly from the teppenyaki, the hard seats, sherbet desserts that melt quickly (they’re placed on the table next to the grill), to communal dining at tables of eight, contributes to the system’s throughput objectives. While few service firms can achieve this level of coherence—or to use a manufacturing term, system integration—it is nevertheless a good ideal to strive for. A quick test is to focus on one element of a system and see if changing it adds to or subtracts from the operation’s overall performance.

- Incorporating learning requires both gathering and disseminating new ideas obtained from analyzing operations. We can distinguish between two types of service organizations, relative to the way they do this: street smart services and systematically smart services. Street smart services learn on an ad hoc basis. Managers and workers pick up ideas through their interactions with customers and general awareness of industry developments. Managing by wandering around, suggestion systems, and some low-key competitive benchmarking constitute the usual approaches. While these may work effectively for smaller service firms, large multisite service organizations must, in our opinion, employ more efficient and scientific ways of finding and implementing operational improvements. We advocate the use of carefully designed experiments at representative branches and development of an information infrastructure to routinely share successful, and unsuccessful, results. Manufacturing product design is generally way ahead of service design in this area. Perhaps the primary reason for this is that factory product designers are accustomed to experimenting with the functioning of each component of a product in minute detail, both individually and as part of the end product.

By way of example, if an HMO chain seeks to improve the atmosphere of its waiting rooms, it can selectively change magazines, provide fresh coffee, or manage other forms of visible “evidence” of service quality. It could administer customer surveys to ferret out the attitudinal effects of these seemingly minor modifications. Similar things could be done in the process side, such as changing greeting “scripts” at reception. Findings from such experiments, both good and bad, could then be conveyed systematically to its other HMO clinics. Some service firms are working along these lines, of course. Banc One has a formalized process for providing the results of operations experiments to its member banks, a practice that CEO John McCoy credits for rapid implementation of its operating improvements. Likewise, Cal Fed Savings uses every other Monday conference calls among its regional managers to share sales and operating techniques that worked and didn’t work. The regional managers then share this information with their branch managers.

Another approach is to use home office “pilot plants” to evaluate the layout and appearance of a field unit. The Limited has full-size store interiors next to the president’s office in its hangar-like home office, enabling executives to tinker with the design until they get it right.

Making the Transition

Unlike manufacturing, which has often pushed operations to the background, the service sector challenges operations executives to use their inherently central position more effectively. We believe these executives should take the lead in changing their area’s relationship to customers, employees, and processes. We propose three broad categories of change.

From Closed System to Open System.

In a 1978 article, one of us advocated that many service activities should be shifted to a remote back office in order to maximize efficiency.12 This, after all, seemed to work well for manufacturers because it kept outside influences, that is, customers, from disturbing the production process. If a technician is assembling a widget, you don’t want the customer asking him what he’s doing.Or if a clerk is processing forms, talking to the customer on the phone takes her away from her job. In retrospect, this closed system philosophy overlooked the fact that there are positive benefits to both the customer and the organization by having the customer closely linked to the server, even though the job is traditionally performed in the customer’s absence. From an information exchange perspective, the greater the links between consumer and producer, the easier it is to understand and respond to the customer’s needs. In manufacturing, the ability to link the producer with the consumer through direct computer linkups driving CAD/CAM systems has provided the technological wherewithal to go “forward to the past” to a craftsman-type organization. That is, it has reintegrated design, production, and even sales into the manufacturing firm’s “back office”—its factory.

That this open systems philosophy can be applied to services can be seen in the following practices:

- Desk sharing between customer service representatives and operations clerks at the London suburb administrative offices of Citibank. (In the Letter of Credit department, a customer service rep told the customer on the phone that a special request couldn’t be processed by operations. The operations clerk, overhearing the conversation, said, “Oh yes, we can.”)13

- Assignment of back office production workers in insurance companies and banks to specific customers so that they can give personalized service.

- Production worker outreach programs. For example, Chestnut Hill (Philadelphia) Toyota’s mechanics are required to call recent customers to find out how the car they repaired is working.

- Bringing traditionally behind-the-scenes production workers on stage to “do their stuff” in front of the customer. Stu Leonard’s Norwalk, Connecticut, Dairy Store (of Tom Peters fame) has several such show-off jobs. One involves a meat cutter and a packer slicing rolls of beef into steaks and packaging them in styrofoam. The team works in the center of the store in a glass booth. The cutter puts on a show, performing artistic flourishes with his cleaver, while his helper smoothly flips and wraps the steaks.

From Procedures Focus to Customer Focus.

Every service firm executive will aver that his or her organization is customer oriented and service driven. However, if you scratch the surface of the organization, you will encounter an armadillo-like armor of procedures and rules that quickly indicates otherwise. “Bureaucracy, thy name is service firm.”

To break out of the procedures trap, ask how you can make the encounter more “user friendly”; each rule you eliminate is value added from the customer’s perspective. It is here, by the way, that systems and procedures groups should direct more of their attention, rather than to back office work simplification. In fact, we would go even further and advocate a new position—customer task analyst—to look for ways to simplify the customer’s role in the service encounter. Admittedly, many services find ways of easing the customer’s job, but rarely do they approach it with the same degree of analysis that they apply to their employees’ jobs.

From Islands of Activity to Total Enterprise Integration.

Manufacturing and service firms face a common problem—coordination of activities around a common purpose. Although both have made extensive use of information technology—CAD/CAM and materials management in manufacturing and database management and transaction processing in services—both are still wrestling with the age old problem of getting departments to work together. The common contemporary solution is to cast each operating unit as a service supplier to the next downstream operation unit, that is, establishing an internal “supplier-customer” relationship. American Express, Xerox, and Hewlett-Packard are primary exponents of this philosophy. For many firms, however, this approach is only marginally successful, for the simple reason that many important supplier duties are not explicitly measured, monitored, and most of all, rewarded in performance reviews. Let’s face it, no matter how company oriented the manager, helping the other guy will always be a secondary priority, unless it is an important and rewarded priority on the management by objectives sheet. We are not advocating that the downstream customer philosophy be dropped. Far from it. What we do advocate is that internal supplier service duties and actions be clearly acknowledged in the organization’s performance measurement and reward system.

Conclusion

A company’s stage of operations effectiveness reflects directly on its vulnerability to competition. A Stage 1 company, for example, will generally operate successfully as long as it remains protected by location or personal relationships, or if all its competitors are also in Stage 1. Corner groceries, dry cleaners, and hamburger joints are examples. Such companies become vulnerable, however, as soon as their niche is invaded by a company that is more representative of the industry as a whole and has elevated its operating capabilities to Stage 2 status. The corner grocery becomes threatened by a new 7-11 Store, and the hamburger joint by a new Burger King. They must then either differentiate themselves from these new competitors, elevate their operations to Stage 2 status, or retreat to a new niche.

Almost by definition, Stage 2 companies can compete with reasonable success within their domestic industry. But if one or more of their competitors elevates its operations capabilities to Stage 3, and can thereby offer superior cost, quality, flexibility-responsiveness, or convenience, they find themselves in trouble. This happens most dramatically after an industry restructuring. A bank, for example, that was able to offer one-stop banking services profitably under regulation may find itself unable to compete against other banks or financial service firms that focus on providing superior service of a more restricted product line. Like those airlines that found themselves after deregulation suddenly vulnerable to competitors that had consciously focused and upgraded their operating capabilities, such companies often end up seeking salvation through merger.

Stage 3 companies are like elephants and whales; they are the kings of their respective environments and have no natural predators, except one. But that one, humanity, is decimating both species. So it is that the only competitor that a Stage 3 company has to fear is a world class Stage 4 company—one that has developed its capabilities and honed its operations to the point that it can compete anywhere in the world. Once it has attained Stage 4, a company can successfully enter a number of national markets, and it often does so with surprising speed and effectiveness. Witness the speed with which Citicorp’s $8 billion consumer banking division entered and came to dominate many of its forty foreign markets.

The danger for a Stage 3 company is that, despite its evident success and the lack of visible challengers, one or more Stage 4 companies may be gestating out of sight in some foreign environment. When such competitors enter a new country, they usually force a rapid escalation in competitive intensity. This can be seen in the case of airline competition, where seven of the top ten international airlines are foreign competitors, with only American Airlines ranking in the top five (fifth), in a 1989 poll.14 And there is evidence that additional Stage 4 companies are incubating in many other service industries: DHL (express mail), Japan’s Yaohan Department Stores, Hong Kong’s Chuo Trust & Banking, and Thailand’s Oriental Hotel. Clearly, the time to prepare one’s operations strategy for the eventual battle is now, while those emerging world class service organizations, be they foreign or domestic, are still preparing themselves for the attack.

References (17)

1. J. Heskett, Managing in the Service Economy (Boston: Harvard Business School Press, 1986), p. 1.

2. Heskett (1986), p. 2.

{kind=link}

{kind=link}

{kind=link}