A Dearth of Exit Strategies

Fallout from the financial crisis could hinder innovation—by limiting options for technology start-ups.

")

Image courtesy of Flickr user Sergei Golyshev.

While governments deliberate responses to the financial crisis of 2008 and its aftermath, one important question should not be overlooked: What will be the long-term impact of the crisis on technological innovation? As part of the fallout from the financial crisis, funds for many types of economic activity have become far more scarce—and that includes research and development.

As economists know, innovation is a key driver of economic growth. Any significant decline in the rate of invention would have a much bigger impact on growth over the next 10 to 20 years than whatever few percentage points of GDP we may lose during the next couple of years because of recession. Thus, we need to be concerned about the impact of the financial crisis on the system of innovative activity in the United States and elsewhere.

THE DOWNTURN MANIFESTO

A manager’s guide to surviving—and thriving—in recessionary times

The notion that a recession is problematic for the rate of innovation is a controversial one. No less a figure than economist Joseph Schumpeter welcomed downturns because he thought that they weeded out old processes and products in the economy. Schumpeter’s conception of the innovative process held that successful entrepreneurs are the generators of economically productive ideas and that over time they transform their businesses into larger enterprises. Those larger enterprises, Schumpeter argued, become more conservative and seek to protect their hard-won market positions. To the next generation of entrepreneurs, the established companies represent a barrier to competing successfully in the marketplace. By shaking out less efficient established enterprises, recessions create opportunities for entrepreneurs once again, Schumpeter thought. He coined the phrase “creative destruction” to describe the phenomenon and saw the cycle of boom and bust as necessary for economic progress.

Two Pathways for Entrepreneurial Start-Ups

We are, however, no longer in the economy of the early- to mid-20th century, when Schumpeter wrote. The fact that new ideas must in some sense displace old ones remains true—but, in today’s economy, the mechanisms of entrepreneurial innovation are somewhat different. In particular, entrepreneurship in some critical technology sectors is dependent upon the activities of larger enterprise in new ways. What is troubling is that the financial crisis poses a risk to that relationship.

RELATED RESEARCH

- A. Arora, A. Fosfuri and A. Gambardella, “Markets for Technology: The Economics of Innovation and Corporate

Strategy” (Cambridge, Massachusetts: MIT Press, 2001). - J.S. Gans, D. Hsu and S. Stern, “When Does Start-Up Innovation Spur the Gale of Creative Destruction?” RAND Journal of Economics 33, no. 4 (winter 2002): 571-586.

- J.S. Gans and S. Stern, “The Product Market and the ‘Market for Ideas’: Commercialization Strategies for Technology Entrepreneurs,” Research Policy 32, no. 2 (February 2003): 333-350.

- D.J. Teece, “Profiting From Technological Innovation: Implications for Integration, Collaboration, Licensing, and Public Policy,” Research Policy 15 (1986): 285-305.

In a series of papers, Scott Stern, associate professor of management and strategy at Northwestern University’s Kellogg School of Management, David Hsu, associate professor of management at the University of Pennsylvania’s Wharton School, and I investigated the strategic commercialization choices of entrepreneurial start-up companies. (See “Related Research.”) Commercialization of new technologies can be undertaken competitively, with entrepreneurs placing products in markets themselves, or cooperatively, with entrepreneurs pursuing mergers or licensing agreements with established companies. The competitive and cooperative paths differ in two key respects: First, a competitive path requires entrepreneurs to develop or purchase access to the infrastructure needed to bring products to markets. The second difference is that a competitive path, as its name suggests, pits entrepreneurial start-ups in head-to-head, Schumpeterian-style competition with established companies. However, start-ups may instead choose to cooperate with established businesses by striking licensing deals or by being acquired.

Our research found that in industries where getting a product to market was comparatively expensive and challenging an incumbent’s market power was difficult, entrepreneurial companies were more likely to strike some type of deal with established companies than in industries where the competitive environment was more favorable to new entrants. For example, because biotechnology and medical device start-ups have to invest in considerable regulatory and specialized marketing competencies to be successful independently, there were more licensing and acquisition deals among the biotechnology and medical device companies we studied than among, say, the electronics start-ups in our sample.

Cooperative commercialization has an additional impact. When larger corporations can draw on creativity from outside the company and pick the most promising ideas at a later stage, they can cut their most speculative research and development activities and rely on the fruits of smaller start-ups’ research. This allows innovative activity to be better allocated to those organizations most suited to it. Similarly, for start-ups, there is no need to displace large corporations to be entrepreneurial when you can sell your innovation to them. Just as easy international trade allows businesses to allocate production across countries to maximize productivity, a market for ideas can allow fruitful exchanges to take place between different types of companies.

The Current Challenge

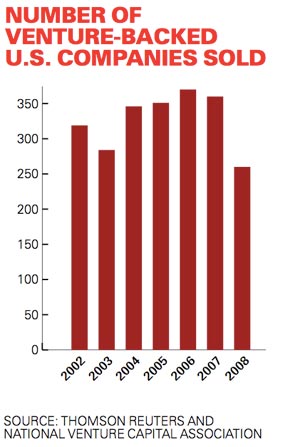

Financial crises mean that capital flows away from risk. In industries where the dynamic of cooperative commercialization is common, that flight from risk is a flight away from entrepreneurship. Even though the financial crisis truly accelerated only in the latter half of 2008, the number of U.S. companies with venture capital backing that were acquired in 2008 decreased almost 28% from the previous year. (See “Number of Venture-Backed U.S. Companies Sold”) On a quarterly basis, the collapse was starker, with more than 70 acquisitions taking place in each of the first three quarters of 2008, yet only 37 in the fourth quarter. At the same time, initial public offerings on U.S. exchanges of companies with backing from U.S. venture capitalists all but disappeared—dropping from 86 such IPOs in 2007 to only 6 in 2008. With fewer viable exit strategies, would-be company founders—and venture capitalists—may find technology start-ups less attractive.

In many circles, governmental attention has been concentrated on large enterprises—banks, auto companies and the like—and the need to ensure their continued survival. However, in technologically dynamic industries, overlooking the role of smaller companies is worrisome. Put simply, the ongoing engine of creativity that technology start-ups supply is what we need to preserve economic growth beyond the next few years.

I do not want to suggest bailouts for entrepreneurs as a policy solution; it is simply too difficult for governments to pick winners among technology start-ups. Instead, this may be a time for a renewed effort in programs that assist entrepreneurial technology companies in general; one example is the Small Business Innovation Research (SBIR) grant program in the United States, which increases such companies’ access to early-stage capital. In the long run, the liquidity of our knowledge capital is just as important an outcome as the liquidity of our financial markets.

Comment (1)

jhemsath