Beyond Business Process Redesign: Redefining Baxter’s Business Network

In the rush to dramatically compress product development cycle times, improve market responsiveness, and redefine customer-focused operations and service quality, many companies have turned increasingly to redesigning — “reengineering” — operational business processes. Yet the majority of these efforts focus almost exclusively on redesigning internal operations in areas such as invoicing (Ford), insurance application processing (Mutual Benefit Life), and marketing and distribution (Rank Xerox U.K.).1 Although many business process redesign initiatives start out amid great fanfare and bold projections of state-of-the-art performance improvements, lurking beneath the glare are often quite modest attempts to reduce operational costs in a single functional area, to improve product quality in a single product line, or to downsize the business to reduce the firm’s cost structure. A few initiatives involve total quality programs, cycle time compression, or outsourcing. Yet many, if not most, business process redesign initiatives invariably turn inward. From the perspective of customers, the external supplier network, and key trading partners, the danger is simply that business process redesign may have little or no measurable impact on the firm’s external market performance. Worse, in some cases, internally focused redesigns may actually allocate scarce resources away from company initiatives that could directly affect external customers.

Information technology (IT) has not dramatically affected this picture. In and of itself: IT has been shown to have little or no impact on overall firm performance.2 Indeed, the usual methods for boosting internal performance — process simplification (usually through process rationalization but now increasingly through outsourcing of selected functions) and process automation — have not produced the required impact on performance. To the extent that many companies still tend to use IT to automate existing processes rather than to redesign them, investments in IT have yielded disappointing results. Of course, most of our job designs, work flows, control mechanisms, and organizational structures came about before the advent of the computer. It is not surprising, therefore, that using information technology to redesign internal business processes has been difficult.3

Ultimately, what distinguishes improvements in the efficiency and effectiveness of internal operations from a broader rethinking of the firm’s external relationships with different markets, trading partners, customers, and suppliers is what Hamel and Prahalad have succinctly labeled “strategic intent.” They point out that strategic intent is more about outpacing competitors in building new advantages than seeking competitive advantages that are inherently stable: “Whereas the traditional view of strategy focuses on the degree of fit between existing resources and current opportunities, strategic intent creates an extreme misfit between resources and ambitions. . . . It challenges the organization to close the gap by systematically building new advantages.”4

Although it is fashionable to refer to electronic data interchange or interorganizational systems as attractive sources of strategic advantage, astute managers recognize that IT offers the capability to redefine market boundaries, alter the fundamental rules and basis of competition, redefine business scope, and provide a new set of competitive weapons. Gaining strategic advantage through the use of IT, however, implies a “sizable stretch” for the organization.5 A number of experts have argued recently that interorganizational systems, in and of themselves, do not provide any sustainable competitive advantage.6 Common examples include automated teller machines in banking, travel reservation systems in the airline industry, and pharmacy distribution systems in health care. Attention, therefore, has shifted away from the technology itself to the interrelationships between the technology and the firm’s ability to manage concordant changes in internal structure and work processes.7 It is with this emphasis — the interrelationships between interorganizational systems and internal innovation and redesign — that we turn to the case developed here.

Baxter Healthcare: From Automated Order-Entry to Value-Added Partnerships

American Hospital Supply Corporation’s Analytic Systems Automatic Purchasing (ASAP), a computerized system for ordering, tracking, and managing hospital supplies, is one of the best-known, most often cited strategic information systems. ASAP, which traces back to 1957 but only became widely written about in the mid-1980s, is credited with helping propel American Hospital Supply Corporation (AHSC—now Baxter Healthcare) from its early, 1960s market position as a medium-sized, regional supplier of generic hospital supplies (such as gloves, gowns, sutures, bandages, etc.) to Baxter’s current position as market leader in this health care segment.

We have studied ASAP and a current service offering, the ValueLink program, over the last several years in order to analyze the interrelationship between business process redesign — the company’s actions to restructure internal operations to improve product distribution and delivery performance to the customer (hospitals) — and what we term business network redesign — the corresponding reconfiguration of the products and services provided by the major players constituting the larger business network. We advance two key conclusions, based on a longitudinal case study of ASAP’s full, thirty-year-plus history. First, a distinctive characteristic of this case, as we will illustrate below, was AHSC-Baxter’s ability to proactively make the literally hundreds of small, incremental redesigns of internal work processes and information technology necessary to improve its overall service level and business relationship with customers. A second distinctive characteristic was Baxter’s ability to reconceptualize its primary business relationship with hospitals — as the market began to move away from purely product/price-based exchange (a traditional supplier role) — to one of a value-added partner with changed business scope in the late 1980s. Our analysis is based on numerous interviews with Baxter and former AHSC personnel over the last several years, archival studies of corporate reports and other secondary sources, and interviews with selected hospitals and other health care suppliers. The appendix summarizes our methodology. See Sidebar.

Evolution of the ASAP System

Below we describe the evolution of ASAP in two phases. The first phase includes localized experimentation — AHSC’s initial, experimental attempts to respond to market needs for efficient distribution through the use of a computerized order-entry system and communication capabilities; organizational assimilation — AHSC’s business strategy to leverage ASAP through aggressive penetration and diffusion into its hospital customer base; and competitive jockeying — the actions by AHSC-Baxter, as well as its competitors, to control the electronic channels of distribution and the contrasting pressures from hospital customers to evolve toward a multivendor, universal distribution system. The second phase, termed strategic transformation, is distinguished by a redefined relationship between Baxter and its customers. A critical question at this phase is: Will the business relationships established with proprietary systems like ASAP move toward a common electronic distribution network? Figure 1 summarizes these shifts in emphasis over time.

Localized Experimentation

The Trigger.

In the 1950s and early 1960s, AHSC, located in McGaw Park, Illinois, was one of several medium-sized regional hospital supply and distribution companies. Like its local and regional competitors, AHSC built its business around efficient purchasing, warehousing, and distribution of generic hospital supplies to customers. The firm manufactured only a small proportion of its distributed product line (ranging from 20 percent to 30 percent depending on product category). AHSC purchased product from a network of large and small manufacturers and then labeled and warehoused its products in one of several large distribution centers for ultimate sale and delivery to customers.

The typical ordering process between a hospital purchasing agent and the supply firm at this time was the responsibility of the salesperson. This individual either mailed in or phoned in a given order to the supply firm’s distribution center. For both customers and AHSC, this amounted to a time-consuming, paper-intensive, and ultimately expensive process. In 1957, AHSC’s automation initiatives focused on reducing the costs of order entry at the distribution centers through the deployment of IBM tab-card machines. These initiatives followed a then-emerging management practice of targeting and reducing costs through selective automation. From a business transformation point of view, however, the critical turning point was the shifting of order entry out of AHSC’s distribution center and into the customer’s purchasing department. Note that while AHSC management did not refer to “redesigning the order-entry process” in these initiatives, the focus and intent of these early moves were clear precursors to today’s emphasis.

Servicing Stanford Medical Center.

In 1963, one of AHSC’s west coast offices was experiencing difficulties in servicing Stanford Medical Center. Stanford had adopted a unique numbering system for all of its hospital product categories in order to create common internal product numbers. The difficulty was that these unique product numbers made telephone orders with different suppliers inefficient because Stanford had to match its own numbering scheme with that of each supplier. Frank Wolfe, a manager in the AHSC west coast office, arrived at a simple solution to improve efficiency: prepunched cards at each Stanford purchasing department with the punched holes corresponding to AHSC’s numbering scheme and handwritten numbers corresponding to Stanford’s numbering scheme. The ordering clerks could then thumb through their set of cards, select the cards they wanted based on the hand-written numbers, and process these cards through an IBM 1001 Dataphone at Stanford attached to an IBM 026 card punch at AHSC.

The availability of prepunched cards from AHSC not only increased order efficiency by decreasing errors, it also ensured that the clerks ordered only from AHSC, as the prepunched cards had only the AHSC numbering scheme. The new system was called Tel-American. As Carl Steiner, then with AHSC and later vice president of Baxter corporate information resources, noted, “This first step was not the result of any top-down strategic directive to leverage information technology; it was simply the result of a manager at AHSC doing his job — assuring the timely and accurate delivery of our products to our customer.”

Organizational Assimilation

Recognition and Response.

AHSC’s successful exploitation of the early Tel-American system rested on two key factors: (1) the recognition of the automated order-entry process’s potential to support its business strategy and (2) the corresponding organizational responses necessary to build the business processes and technology to allow AHSC to capitalize on the opportunities afforded by greater customer integration. Many executives with AHSC at the time believe that the critical turning point came during a 1966 corporate strategic planning meeting. Steiner recalled, “We were reviewing an outside recommendation to invest additional resources to improve what amounted to our back-office accounting systems. As we moved to decide the issue, we all realized that AHSC’s chairman, Karl Bays, had been pressing us to allocate the information systems [IS] resources to our core marketing and distribution functions rather than to accounting. We did.” The executives recognized that IT was central to driving these functions, and thus they committed IT resources as investments rather than as administrative expenses. The decision was supported by centralized coordination and senior management commitment. Further, AHSC’s corporate IS division was given responsibility for the design, development, and modification of the Tel-American system as well as make-versus-buy decisions in key technologies.8

The commitment shown by Bays and senior business managers to leverage IT capabilities played an important role in this phase. Although local experimentation could be carried out with minimal resources, the continuation of the Tel-American system required not only financial resources but also senior management support. CEO involvement was key: Bays, who in 1985 was quoted as saying “The computer is at the heart of our success,” himself participated in two-hour monthly meetings with his information systems and Tel-American staff: These meetings encouraged staff and informed Bays and his senior management team about the program’s progress.

Continuing System Enhancements.

Another key element was the dynamic alignment between customer needs and the adaptation of technological and business process functionalities. The experimental Tel-American system evolved into an order-entry system using a touch-tone phone — known as ASAP I. The customer would simply call an AHSC distribution center and “key in” the order. Although this simple system revolutionized order processing, a major limitation was the system’s inability to directly interconnect AHSC, its sales representatives, and hospital customers, and its inability to provide printed pies for order verification. Customer requirements led to the next major enhancement. ASAP 2 supported order entry through teletype machines at customer sites (clerks typed in the order and received a printed copy of the order directly from the teletype machine). Customers paid for the teletype machines, and AHSC incurred the telephone charges.

In contrast to ASAP 2, ASAP 3 focused on customizing the system to the requirements of different hospitals. For example, ASAP 3 allowed hospitals to order supplies using their own internal stock numbers and to create standing order files for regular ordering. In this way, economic order quantities for different items could be incorporated into each hospital’s system, facilitating quicker ordering. Similarly, from the output perspective, customers could specify their purchase order formats and avoid a multiplicity of formats. These capabilities proved to be major differentiators. Most hospitals had not automated their materials management and supply functions by the early 1970s and could not have designed and developed such a system without incurring significant costs. Thus, ASAP 3 capitalized on hospitals’ steadily increasing needs to improve their own internal supply management.

Furthermore, a significant aspect of AHSC’s service-level strategy was to work with hospitals to define, measure, and improve the nonproduct-related costs of materials management.9 This was a new emphasis in the industry, and by the mid-1970s it had led AHSC to provide to select hospitals “customer purchase analysis” reports — essentially reports showing historical ordering patterns but also including information that could be used later to determine economic order quantities and other materials management-like functions. For a few larger customers, AHSC went a step further and put together small teams of sales, marketing, distribution, and IS personnel to analyze a hospital’s paper flow around materials ordering and receiving. These types of services were later incorporated into the company’s broader value-added services approach.10

The point here is that AHSC responded to the needs of a few leading-edge customers in the beginning, but this service-level requirement rapidly diffused throughout the industry and became a necessary service for all customers by the early 1980s. As Michael Heschel, former CIO at AHSC and Baxter International, noted, “These early reports and services back to the hospitals were part of a larger overall strategy to work with the customer in advancing the purchasing function within the hospital (it had been a very clerical-like function in most cases). We felt it should be a materials management function. We knew that working with them in this way would bring good value to the hospital and create within the hospital someone who would appreciate our services.”

In 1983, ASAP 4 was introduced to respond to requests from hospitals to provide direct computer-to-computer links. This version of ASAP simplified the hospital’s purchasing process by eliminating all the manual steps required except purchase approval. Table 1 provides a summary of the continuing enhancements from Tel-American to ASAP 4.

Preemptive Penetration of Hospitals.

AHSC’s major initiative in the marketplace was to aggressively penetrate hospitals with ASAP in order to gain relative competitive edge over other suppliers. Several industry forces helped. By the late 1960s and early- to mid-1970s, hospitals were shifting from a focus on service-level quality to a focus on cost. The period was marked by major increases in the demand for hospital services, largely owing to the passage of Medicaid and Medicare I legislation (in 1965 and 1966, respectively). By 1971, hospital care was the fastest growing component of health spending, largely owing to “greater government funding” and “sales of medical supplies and equipment that were growing at 10 percent annually.”11 Indeed, during the period 1970 to 1987, health industry sales grew at over 16 percent compound average nominal rate, with total sales moving from $2.14 billion in 1970 to $22.5 billion in 1986.

Early Tel-American and ASAP system capabilities proved to be strong inducements for hospitals to sign up. Just over two hundred hospitals authorized AHSC to install ASAP 1 systems within the first few years of its introduction. By the mid-1970s, over 500 hospitals were ASAP or Tel-American customers. Figure 2 profiles the pattern of aggressive ASAP penetration into the marketplace (figures include terminals provided to AHSC sales teams for customer support). By the late 1980s, of the roughly 6,900 hospitals nationwide, 5,500 were using ASAP Interestingly, almost 3,500 hospitals accessed the system from teletypes or other (dumb) terminals.

Attainment of “Prime Vendor” Status.

Our final point about these early days relates to AHSC’s strategy of achieving “prime vendor of choice” status with the hospitals. The concept of “prime vendor” involves the contractual basis by which the customer negotiates volume purchase agreements, generally (but not exclusively) on a fixed price basis, with its principal supplier of hospital goods. The advantage of the prime vendor concept is straightforward: the key purchasing decision shifts from price (the prime vendor contractually agrees to be market competitive) to service, and the customer agrees to volume purchases. Although AHSC managers believed that successive enhancements of ASAP would provide first-mover advantages, it was also clear that the technology itself was a relatively small part of differentiating the company from other suppliers and not an end in itself Indeed, several regional competitors had introduced small, Tel-American-like systems in a few hospitals (e.g., Owens & Minor and Durr-Fillauer. Inc.). These companies, however, failed to aggressively install these systems across a wide base of customers.12 Although ASAP customers benefited from materials management and order-processing cost reductions, the feeling among AHSC managers was that the technology could be imitated by competitors (“It was only a matter of time,” Heschel recalled). It was the “one-stop shopping” approach, supported by AHSC’s broad product line, that could not be imitated. As Steiner noted, “Our whole approach at the time, pushed by Gary Nei [AHSC product manager for systems marketing] and supported by marketing up to and including AHSC’s chairman, Karl Bays, was that we had a broad enough product line to become the hospitals’ prime vendor of choice. The systems were really thought of as the way to show this to the customer and, even better, to provide improved service (lower error rates, reduced processing costs) on top of that.” Steiner also emphasized the importance of AHSC’s broad product line rather than the technology linkage: “It always amazes me that even today we still hear talk about locking customers in with technology. In fact, the customer requirements we were dealing with at the time were for us to help provide them with a very simple device, one very easy to understand and implement (in what was still largely a clerical function), and above all, very inexpensive. We certainly did not view this kind of device as anything more than an opportunity to show the customer we had the product line to simplify their ordering process.”

Thus, AHSC’s two-pronged strategy rested on its ability to leverage its extensive product scope and the ASAP platform to market the concept of “prime vendor” to the hospitals. From the hospital’s point of view, while most of AHSC’s unit prices were no better than those of other suppliers, by consolidating and reducing the number of orders placed, the hospital could reduce administrative overhead. Hence, hospitals preferred a prime vendor. Moreover, hospitals viewed the firm’s business scope as primarily distribution oriented, given that AHSC manufactured less than 30 percent of its products.

Competitive Jockeying

Delayed Competitive Response: Regional Fragmentation or Inertia Barriers?

What were AHSC’s competitors doing as the firm consolidated its penetration of the hospital supplies marketplace? The answer lies in two major factors:

- Fragmented, regional competition — the smaller players could not effectively provide similar systems, service levels, and product support: and

- Inertia barriers — competitor-specific characteristics (such as other priorities; organizational/structural idiosyncrasies, including the possibility that no one business group or area had the direct responsibility to respond; and administrative procedures and bureaucratic policies) slowed competitors’ abilities to respond effectively.

The hospital supply market was highly fragmented in the 1970s and early 1980s. In 1972, Standard & Poor’s reported that over 70 percent of producers had fewer than fifty employees per plant.13 Table 2 summarizes the relative market positions, highlighting the degree of fragmentation.

It was into this market, therefore, that Durr-Fillauer, a regional hospital supply company in the southeastern United States and a direct AHSC competitor, introduced a Tel-American/ASAP I -like system in the mid-1970s. At about the same time, Van Waters & Rogers, a local competitor in the specialty products segment on the west coast, introduced another, similar order-entry system. Both systems, however, never constituted much of a threat. AHSC had already established its service level and product position in these regional markets, and ASAP offered equal (if not better) system functionality. Thus, even when Whittaker General Medical, AHSC’s largest competitor, introduced ADAMM, an electronic order-entry system similar to ASM in the late 1970s, AHSC’s position in the marketplace was not fundamentally weakened.14

It is interesting to note that at the same time, an unfair trade practices suit was filed in the Western District Federal Court (Michigan) by White & White, Inc., a regional competitor, in party with several other distributors. In essence, the suit charged AHSC with unfairly restricting trade by “biasing” hospital purchasing agents to order supplies over the proprietary electronic link (this suit was similar in concept to the complaint filed in late 1982 by Frontier Airlines against United over the latter’s use of its APOLLO travel reservation system). Initially, the court found in favor of the plaintiffs. AHSC appealed, and the appeals court ultimately found for the defendant in December 1983.15

Fragmented competition was one factor in delaying competitive responses; a second was simply inertia. Here, the dominant pattern of interrelationships between manufacturer and distributor was the key driver. AHSC’s largest supplier in the 1970s and 1980s was Johnson & Johnson (J&J), itself a major manufacturer and distributor of hospital supplies. J&J viewed AHSC’s early initiatives as efforts by one of its leading distributors to better service its ultimate customer, the hospital. Similarly, Abbott Laboratories competed with AHSC only in the relatively narrow market segment of intravenous solutions and otherwise bought most of its glassware for R&D and other supplies from AHSC. Thus, initially J&J and Abbott had little reason to directly counter AHSC’s moves regarding computer-based distribution channels.

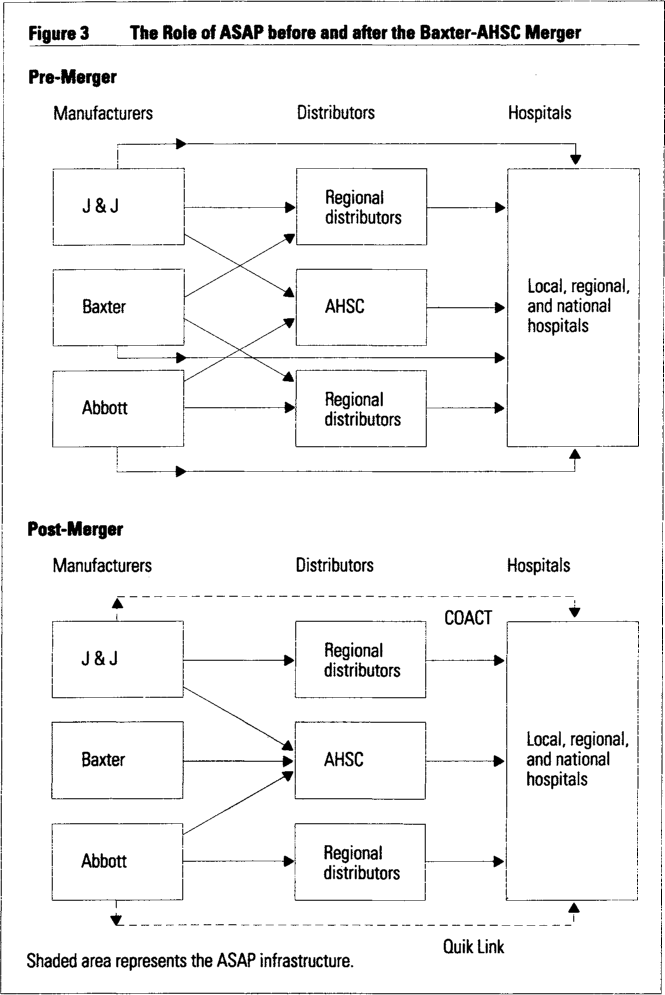

In 1985, however, the competitive dynamics of the market changed dramatically when Baxter Travenol Laboratories acquired AHSC. J&J and Abbott (as well as other, smaller hospital supply companies) saw a key competitor, Baxter Travenol, acquire one of their major distribution channels (see Figure 3). Prior to the AHSC-Baxter merger, J&J and AHSC were complementary in the overall value-creation system. However, Baxter’s acquisition left competing firms with few choices: quickly develop (or augment) their own electronic order-entry systems, continue to use ASAP as a major distribution c channel, or push for a universal, open distribution network. From 1984 to 1986, a major shakeout saw several big suppliers (Bard, 3M, Monojet, and J&J’s patient care and orthopedic divisions) pull their products from Baxter’s ASAP distribution network.16

AHSC-Baxter Merger: Acquiring Distinctive Competencies

Although we do not intend to analyze the pros and cons of the AHSC-Baxter merger here, we do point out that the merger signified a strategic move by a manufacturing firm seeking to control the dominant electronic distribution channel with the hospitals.17 Since the market-place had accepted the “prime vendor” concept, Baxter Travenol’s success before the merger critically depended on its available product scope and its access to AHSC’s electronic distribution channel. Moreover, given the penetration levels ASAP achieved over the 1965 to 1985 period, it would have been difficult, if not impossible, to create a competing electronic channel. Thus, Baxter seized on an aggressive strategy of acquiring control of AHSC and the ASAP channel.

In discussing the acquisition, Bays remarked, “Both companies have similar customer bases. AHSC over the years had invested in a distribution system and remote order-entry system that clearly will be of help to Baxter.18 The importance of ASAP was further highlighted when AHSC’s senior IS executive group was put in charge of Baxter’s new IS organization, and ASAP served as the electronic pipeline anchoring the new company’s post-merger business strategy.19 Table 3 summarizes the merged company’s dominant market share positions in several key product lines.

Continuing System Enhancements

Subsequent to the acquisition, Baxter continued to emphasize system enhancements (see Table 1, especially the additional features included in ASAP 5 to ASAP Express PowerBase).

Toward an Electronic Distribution Network

A critical question at this stage is: Will the business relationships established with proprietary systems move toward a common electronic distribution network? By one account, by 1988, there were over fifty different order-entry/materials management systems in the marketplace.20 From the hospitals’ point of view, order-processing efficiency decreases with multiple, incompatible systems, and they have increasingly demanded the establishment of a common order-entry platform. More than a decade after the introduction of ASAP 1 and several years after smaller, regional competitors imitated ASAP with their own versions of proprietary order-entry systems, both J&J and Abbott introduced their own versions of proprietary, multivendor systems: J&J’s Cooperative Action Plus (COACT) and Abbott’s Quik Link.

COACT, first introduced in July 1985, is a sophisticated computer-based logistics system. It combines features such as on-line order inquiry and consolidated reporting. More specifically, COACT brings together fifteen J&J companies, hitherto distributing their products separately, onto one system. COACT PLUS, introduced shortly thereafter, offered a centralized gateway to J&J products as well as to products from other selected vendors. Additional system-related features include the ability for the hospital to use a few custom codes to generate purchase orders, rather than manually entering full orders, a database manager that tracks all the products purchased by the hospital, and telecommunications services with selected other vendors.

Quik Link, developed jointly by 3M and Abbott Laboratories, was announced in October 1987. This system has the following key capabilities: multivendor remote order-entry capability, consolidated product deliveries, and centralized customer service. The alliance between 3M and Abbott ensures economies of scale in pricing, product line availability, and technology — essential requirements for competing in this marketplace.

These moves to provide common gateways reflect competitor attempts to match Baxter’s broad product I scope and high penetration rate for terminals in the hospitals (as noted in Figure 2, Baxter had installed ASAP l in approximately 80 percent of all major — over 200-a bed — hospitals). Earlier, relatively weak proprietary systems offered by smaller competitors (Durr-Fillauer, Van Waters & Rogers) failed because of AHSC’s extensive product scope, the high levels of ASAP penetration, and the continual modifications and upgrading of ASAP to improve ease of use, functionality, and cost. By April 1988, however, both Abbott and J&J offered over thirty vendors on each of their systems, significantly broadening their product scope and thus attempting to compete head on against Baxter. Pressure was also building on the customer side — many hospitals faced the option of converting over to COACT or Quik Link or, worse, running all the systems in parallel.

In June 1988, Baxter responded with ASAP Express — its own version of a multivendor system (initially eight vendors were on the system). ASAP Express extended Baxter’s proprietary network to include other network providers, including GE Information Systems Company (GEISCO) and McDonnell Douglas, which provided global telecommunications services and an electronic clearinghouse for the other eight firms. ANSI X.12 standard formats were adopted for all communications. As Baxter’s director of ASAP systems noted, “Baxter now is more globally defining ASAP as automated communications rather than just automated order entry. We realize that the life of vendor-discrete systems — at least those in health care — is limited. We are purposely following the successful example of American Airlines’ moving into the all-vendor arena. Moreover, our customers continue to shape our ASAP future. Their needs involve all areas of their management responsibilities, not just order entry.”

Synthesis

It is clear that the focus of ASAP evolved from an operational emphasis on order entry and service-level reporting to one focused on service quality, cost management, and value-added materials management. The ASAP technology platform has continued to shift away from a dedicated system with proprietary protocols toward a common electronic data interchange platform, with gateways to third-party network providers (GEISCO, McDonnell Douglas, IBM, and other value-added networks).

However, like all proprietary systems, even if multi-vendor, ASAP Express carries price and product availability only for Baxter’s and covendors’ product lines. True price comparisons between competing product lines and vendors are not possible on-line (unlike the airline reservation systems, which display such information). Following Williamson and Malone et al., we note that there is a movement away from electronic hierarchies in this industry (i.e., proprietary ASAP 1 to ASAP 4 systems) and toward a “biased” electronic market (i.e., a few relatively large multivendor systems).21 Simultaneously, on the customer side, hospitals themselves are investing in their own materials management systems.Consequently, there are strong pressures to reduce the “bias” in multivendor systems for purely product-based exchanges and move instead toward a common network infrastructure. However, because this market depends crucially on value-added, materials management services as well as product sales, it is still unclear how or when this market will evolve into an electronic marketplace with largely price-based exchange.

Strategic Transformation

The critical business strategy and technology challenges facing Baxter and its competitors in the 1990s are substantially different from those of the evolutionary perspective just outlined. We discuss this second phase, termed strategic transformation, in terms of (1) shifts in business competences and (2) shifts in business network roles.

Shifts in Business Competences

The distinctive business competence has shifted from efficiently distributing products through automated order entry to delivering an integrated materials management service guaranteeing product availability and information-based logistics services. Whereas success in the first phase depended on a firm’s ability to carry a wide product range to support the prime vendor concept, success in the second phase will depend on a firm’s ability to control and exploit key attributes of information flows underlying product exchanges with the hospitals. This is because the electronic order-entry system has shifted away from dedicated systems to a system that has the capability to access multiple competing suppliers on a near-equal basis. This implies that a firm with the capability to provide a broad product line from multiple vendors, just-in-time (JIT) delivery, and logistics management to the hospitals will succeed relative to those competitors without such competences.

The beginning of the second phase is marked by the deployment of Baxter’s ValueLink program in 1990. ValueLink is defined by Baxter as “a logistics capability, based on integrated information management, that delivers products on a just-in-time basis in a ready-to-use package for specified-user departments.”22 In simplest terms, it is an integrated logistics system synchronizing the flow of products and information between the customer and Baxter via consolidated purchases (e.g., prime vendor) and multiple deliveries to point-of-use in the hospital seven days a week. This business program has the potential to reshape traditional conceptualizations of control and coordination in customer-supplier relationships in areas such as initiating purchases, inventory control, monthly invoicing, and payment. The underlying business rationale for ValueLink is that the overall efficiency within the manufacturing-distribution-customer chain increases as the distributor assumes inventory and distribution functions, in exchange for customer purchase commitments. As Baxter and hospitals become more interdependent via ValueLink, greater trust and understanding between them will be required to sustain and manage the “strategic partnership.”

The success of the partnership requires that each hospital commit to a long-term contract (minimum multi-year) for purchase volume as well as a high share of product flow with fees for value-based services. Baxter, for its part, commits to providing a 100 percent fill rate, lowering inventory levels (and associated operating and fixed costs), in addition to developing customized procedures to ensure delivery to multiple, distributed user departments (e.g., operating rooms, laboratories, X-ray units, etc.). Since this requires Baxter to distribute a broad product line, including its competitors’ products, it is particularly significant that Baxter has obtained limited rights to distribute products from over four hundred manufacturers that traditionally have not distributed through Baxter’s hospital supply division.23 It is also interesting to note, however, that Abbott, 3M, and certain J&J companies have to date refused to sell their products through the ValueLink program, thus highlighting the importance of product breadth, rather than order entry, as the critical business competence in the changed marketplace.

Table 4 summarizes the details of six major ValueLink contracts. These contracts highlight the partnership nature of the relationship between the hospitals and Baxter. Our assessment is that Baxter is seen as shifting away from a focus on economies of scale (i.e., efficient, standardized, low-cost distribution) and toward economies of scope (i.e., customized, materials management services provided through a combination of product scope and information scope).

Shifting Business Network Roles

Beyond Baxter’s ValueLink program and several competing programs offered by regional competitors, this phase is marked by fundamental shifts in the business roles of the marketplace’s key players.24 Specifically, the roles of manufacturer, distributor, purchaser, information systems provider, and materials manager are blurring. In the first phase, the primary role of AHSC was one of a full-line distributor of products, whose suppliers included J&J, Abbott, and other hospital supply manufacturers. Thus, AHSC’s attempts to leverage ASAP to increase its competitive position vis-à-vis other distributors was not a major concern to the manufacturers. From the hospital point of view, ordering via the ASAP system saved administrative costs and inventory carrying costs and provided valuable service-level reports back to hospital management. These could not have been duplicated as efficiently within the hospitals.

Moreover, with the introduction of ASAP Express and, later, ASAP Express PowerBase in early 1990, Baxter is steadily assuming the role of an information gateway. With the launch of the ValueLink program later in 1990, Baxter is assuming a still greater role as a JIT-materials manager for the hospital. To illustrate the point, consider the case of the ValueLink contract with Vanderbilt University Hospital (see Table 4). Here, Baxter is in the midst of moving its own staff into the hospital to manage the flow and restocking of supplies. Vanderbilt has sold or leased its stock of supply carts to Baxter, and Baxter is reconfiguring part of its Nashville warehouse to accommodate the hospital’s goal of delivering to each category of end user the required units for use. Such an arrangement redefines the traditional role of a distributor, requiring greatly increased levels of trust and mutual interdependence.25

Summary

We summarize our conclusions in terms of two critical activities undertaken by AHSC-Baxter during ASAP’s thirty-odd-year evolution: the need to (1) proactively shift strategic emphasis over time and (2) reconceptualize the firm’s primary business relationship with hospital customers.

Proactive Shifts in Strategic Emphasis.

A key theme emerging from this case is the proactive way in which AHSC-Baxter s strategies for electronic integration shifted over time. The early years were marked by a “business-led IT response” — namely, the design of the dedicated, proprietary ASAP system to support an overarching business strategy of being an efficient, national-scale, full-line distributor of hospital supplies. However, as the marketplace shifted under increasing pressure from hospitals and competitors for a common electronic infrastructure, Baxter shifted its emphasis away from dedicated systems to a multivendor platform that leveraged its installed technology base. Simultaneously, Baxter offered the ValueLink program. Certainly materials management as a value-added service is not new to the industry, but Baxter’s offering is distinguished by its ability to leverage the firm’s product scope and information technology base. AHSC-Baxter’s proactive strategy to continually change the rules of the game in this marketplace is particularly characteristic in this case setting.

Reconceptualizing the Business Network.

A second, distinctive characteristic of this case is Baxter’s (and formerly AHSC’s) ability to reconceptualize its primary business relationship with hospitals as the marketplace shifts away from purely product/price-based exchange to one of “value-added partner.” This characteristic again underscores the need to view interorganizational systems in terms broader than simple electronic data interchange. Baxter’s core business strategy has been to continually redefine the nature of the business relationship between itself and the hospital (efficient distributor to prime vendor to electronic distribution channel to value-added partner). This business strategy viewed ASAP as a means, not an end in itself.

From Business Process Redesign to Business Network Redesign

Business process redesign — with the traditional focus on streamlining the processes within a given firm — addresses only a part of the larger issue of business transformation through information technology. We argue that too much attention has been placed on business process redesign that either implicitly or explicitly assumes that the boundaries of the different firms in the marketplace are fixed. Our argument is that there are real opportunities for restructuring when the business processes are defined across different organizations that serve to deliver value to the customers. In other words, it is important to first articulate the larger business network that contains the critical business processes and then adopt a more holistic approach to redesign.

More specifically, this case highlights the fact that although the initial benefits from IT came from the redesign of business processes internal to AHSC and Baxter (namely, order entry, delivery turnaround, etc.) the current emphasis is on assuming the materials management activities of customers (hospitals), thereby redefining the business roles (who does what in the marketplace) of the firm as well as the business scope (the domain of business activities of the different players in the marketplace). Had Baxter restricted its view of the business process as being contained within its company boundaries, it would have realized efficiency benefits but not the potential to restructure the basis of competition in the marketplace. Our call is for greater management attention to the redesign of the business network with business processes being defined across organizational boundaries rather than restricted to any one organization.

We entered the 1990s with significant attention to business process redesign (or reengineering) with a particular focus on eliminating inefficiency and streamlining operations. As one manager involved in our research commented, “We had to take out the fat that we had built up, and reengineering is a means to do it, but we should realize that it is not an end in itself After we have all cleaned house, we need to find new and different avenues to compete.” To conclude, business process redesign creates the necessary organizational capability to compete, whereas business network redesign identifies the avenues to obtain new sources of competitive advantages in the marketplace.

Appendix

We describe our case methodology in terms of the eight steps outlined in Eisenhardt for building theories from case study research.26 The philosophy of case research underlying these steps is consistent with the current thinking on scientific research, and this set of steps best helps us to describe our approach.

Getting Started.

This step involved defining the re search question and possible prior constructs. Specifically we framed the research question in terms of understanding the evolution of Baxter’s ASAP system in its broader context of environmental, organizational, technological, and competitive characteristics.

Selecting the Case.

As it is one of the “popular” cases of strategic benefits from IT (especially as two others have been previously subjected to detailed assessments), we selected the hospital services market.

Crafting Protocols and 4. Entering the Field.

Our approach was to adopt multiple data collection methods involving both qualitative and quantitative data. Two different investigators collected data from several sources: customers, company, archival records, secondary data on market trends, and so on. The use of diverse sources helped us strengthen our conviction in the conclusions.

Analyzing the Data.

Our approach was essentially to carry out “within-case” analysis to ensure internal consistency and validity of our interpretations and conclusions. We had constant feedback discussions with multiple managers at Baxter to validate our interpretations. The arguments presented in this paper reflect our analysis of the data that have been discussed (but not always necessarily endorsed) by the internal managers.

Shaping Hypothesis and 7. Enfolding Literature.

Although inductive, our arguments in the paper are congruent with relevant bodies of theory such as Williamson’s modes of governance.27

Reaching Closure.

We believe that we have been able to offer adequate insights in relation to the first phase (evolution) and have raised interesting issues for the second phase, which is just unfolding. It is a rich setting to continue further research assessing Baxter’s capability to compete effectively in the changing marketplace.

References (36)

1. T. Davenport and J. Short, “The New Industrial Engineering: Information Technology and Business Process Redesign,” Sloan Management Review, Summer 1990, pp. 11–28.

2. G.W. Loveman, “An Assessment of the Productivity Impact of Information Technologies” (Cambridge, Massachusetts: MIT Sloan School of Management, Management in the 1990s Program, Working Paper No. 88-054, July 1988). See also:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}