Making Global Strategies Work

It is hardly a novel insight that global competitive forces compel multinationals to fully leverage the distinctive resources, knowledge, and expertise residing in their subsidiary operations. Questions of what are “winning” global strategic moves for the modern multinational have increasingly intoxicated international executives.1 Yet for all the fanfare about global strategies and their increasingly undeniable link to multinational success, little has been said or written about how to make global strategies work. The key question we address here is just that: What does it take for multinationals to successfully execute global strategies?

Our research results paint a striking picture of the importance of the strategy-making process itself for effective global strategy execution. Over the last four years, we have done extensive research to understand how multinationals can successfully implement global strategies. Because subsidiary top managers are the key catalysts for, or obstacles preventing, global strategy execution, we asked them directly just what it was that motivated them to execute or to defy their companies’ global strategic decisions.

Subsidiary top managers were quick to rattle off a series of well-established implementation mechanisms: incentive compensation, monitoring systems, and rewards and punishments. They were equally quick to add that they did not believe these control mechanisms alone to be either sufficient or that effective. The general consensus was that these mechanisms were not particularly motivating and were easy to dodge and cheat. Even more recurrent in our discussions, however, were the dynamics of the global strategic decision-making process itself. When deciding whether or to what extent to carry out global strategies, subsidiary top managers accorded great importance to the way in which those strategies were generated. Their overriding concern involved a deceptively simple though evidently profound principle: due process should be exercised in the global strategic decision-making process.

In practical terms, due process means: (1) that the head office is familiar with subsidiaries’ local situations; (2) that two-way communication exists in the global strategy-making process; (3) that the head office is relatively consistent in making decisions across subsidiary units; (4) that subsidiary units can legitimately challenge the head office’s strategic views and decisions; and (5) that subsidiary units receive an explanation for final strategic decisions.

In short, we observed that, in the absence of these factors, subsidiary top managers were often upset and negatively disposed toward resulting strategic decisions. However, in the presence of these factors, the reaction was just the reverse. Subsidiary top managers were favorably disposed toward resulting decisions, thought them wise, and were motivated to implement them even if, and here is the biggest benefit of all, these decisions were not in line with their individual subsidiary units’ interests.

We begin this paper by probing in depth just what subsidiary top managers mean by due process and why they judge its exercise important in the global strategy-making process. Next we examine what leads subsidiary top managers to view traditional implementation mechanisms as increasingly insufficient for global strategies. Finally, we trace the real effects of due process in global strategy making on global strategy execution and explore why they are so profound.

The Meaning of Due Process

To get to the heart of how multinationals can make global strategies work, we held extensive interviews with sixty-three subsidiary presidents.2 Our initial objective was to get subsidiary presidents’ honest evaluation of the factors that drove them to carry out or resist their organizations’ global strategic decisions. As the interviews progressed, the one tendency that stood out was the subsidiary presidents’ natural inclination to discuss how global strategies were generated. Time and again, the dynamics of the global strategy-making process itself were the centerpiece of their discussions. Their principal concern was whether due process was exercised. That is, was the strategy-making process fair from the subsidiary unit perspective?

Through these interviews, we identified the five characteristics above that, taken together, defined due process in global strategic decision making (see Figure 1).3 What is interesting is that these five characteristics were important regardless of the industry or the subsidiary’s strategic importance. Appendix A profiles our sixty-three subsidiary presidents and discusses how they were selected. Here we discuss each of the characteristics and examine through the eyes of subsidiary top managers what makes each of them vital.

{kind=link}

Head Office’s Familiarity with Local Conditions

The head office does not know a damn thing about what’s going on down here. They tell me to further push their global “core” products even at the expense of our existing product lines. And you know what I tell them? I tell them they’re crazy. They don’t realize that not only don’t these “core” products sell in our local market but that we are already losing sales on our existing product lines from tough local competitors due to our lack of push on them.

This statement indicates subsidiary top managers’ attitudes when the head office lacks knowledge of the local market. One manager explains why local familiarity is important:

The head office needs to invest in understanding the local market. How can I respect their decisions and follow them if I don’t believe that they are made with an understanding of the local market?

When subsidiary managers believe the head office has a reasonable grasp of the local situation, they are apt to make statements like this one:

I have tremendous faith and trust in the head office’s strategic decisions. They know the local market. When they make a decision, they understand the ramifications of that decision, be those ramifications good or bad. Whether I like their decisions or not, there’s at least a method to their madness.

What it comes down to is that in the absence of local familiarity, subsidiary top managers do not judge the head office to be competent and sincere. They tend to think of the head office instead as incapable and apathetic toward their foreign operation. As a consequence, these managers have little respect for the decisions coming down. They quickly become skeptical of the soundness and quality of the resulting global strategies. This provides an excellent excuse for not only why they do not implement global strategies but why they should not. As one executive put it, “To not follow the global strategic decisions handed down to a subsidiary unit is not a curse but a blessing in disguise. Those decisions aren’t based on reality; they are based on air.” At the most, local familiarity gives confidence that global strategies are based on thoughtful analyses; at the least, it prevents subsidiary managers from using this seemingly reasonable justification for not executing global strategic decisions.

Two-Way Communication

When global strategic decisions are being made that affect a subsidiary unit, subsidiary top managers value the ability to voice their opinion and work back and forth with the head office in decision formulation. This communication symbolizes the respect the head office has for subsidiary units as well as the confidence it places in subsidiary managers’ opinions and insights.

Our observation is that this respect and confidence is quickly reciprocated by subsidiary top managers as well. Although two-way communication often results in heated debates, it also builds a profound spirit of comradeship, unity, and mutual trust among the head office and subsidiary top management teams. Moreover, when subsidiary managers participate in global strategic decision making, they come to view the decisions as their own. As a result, they often defend and uphold these decisions. As one executive commented:

The open exchange of information and ideas is critical in global strategy making. It opens the ears of managers in both the head office and subsidiary units and typically results in better value judgments. When we [subsidiary managers] feel that our views are given sufficient attention, we are less likely to be dissatisfied with global strategic decisions or to feel antagonistic toward the head office and are better motivated to act rigorously to carry out the agreed-upon plan of action.

Consistent Decision-Making Practices

Consider two opposing comments made by different executives. One says:

Our global strategic decision making is a very political process. If you are on the “inside track,” the head office treats you as a relatively important element of global strategic decision making. But if not, you and your unit are likely to be completely overlooked and just slapped with a set of strategic decisions that are supposed to be implemented. At times, I think the whole process is just a scam, a politicians’ arena where strategic decisions reflect not competitive and economic dynamics but the dynamics of political interplay.

The other says:

Admittedly subsidiary units don’t walk away with symmetric decision outcomes — one subsidiary unit may get what seems to be a windfall allocation of resources while another may take a cut. But all subsidiary units are treated relatively consistently when it comes to how these decisions are reached. It’s a fair process. There doesn’t seem to be much favoritism or political jockeying in this decision-making process.

These two comments shed light on why consistent decision-making practices across subsidiary units are a prized aspect of due process. Basically, they are thought to minimize the degree of politics and favoritism in the strategy generation process. Subsidiary managers are confident that there is a level playing field across subsidiary units. And this is important. Subsidiary managers do not expect the strategic decisions made across subsidiary units to be identical, as they understand that units are not equally important for the organization. But they do view the consistent application of decision-making rules as an essential element of due process.

In the absence of consistency, subsidiary managers are quick to judge the decision-making process as arbitrary, politically rigged, and hence not to be trusted. They find the confusion and uncertainty extremely frustrating, and they are inclined to attribute unfavorable strategic decisions to unfair decision rules as opposed to competitive and economic dynamics. Consequently, they become bitter and resentful and more apt to want to undermine resulting decisions.

Ability to Refute Decisions

Having the ability to refute the head office’s strategic views and decisions also makes subsidiary managers feel that due process is being exercised. Admittedly this can be traced in part to managers’ perceived increase in influence over strategic decisions, but our discussions suggest another reason why the ability to refute is important. It makes managers feel that the process is fair simply because they can clearly point out possible mis-perceptions or wrong assumptions made by head office managers concerning local conditions or subsidiary operations. But more than this, the ability to challenge head office decisions inspires subsidiary managers to more willingly follow these decisions because they know that if the decisions should prove unreasonable or wrongheaded, the possibility always exists to correct them. As one executive explained:

When I know I have the right to openly challenge the head office’s decisions, that automatically tells me that the head office is confident in their decisions, that they have faith that their underlying logic and analyses can stand the test of open scrutiny. But it also tells me that, despite the head office’s confidence, they also recognize that being removed from the local market opens up the possibility that they will judge the local situation incorrectly. Not only do I respect the head office for this, but it in turn gives me confidence that the intentions and global strategic decisions of the head office are truly made in the interests of the overall organization and not based on politics.

An Explanation for Final Decisions

Subsidiary top managers think it only fair that the head office give them an explanation for final global strategic decisions. And they consider it an important aspect of due process. In short, subsidiary managers need an intellectual understanding of the rationale driving ultimate decisions. They want to know why they should carry out the decisions. This is especially true if those decisions override their expressed views or seem unfavorable to their own unit. To quote one executive:

When the head office provides an explanation for why decisions are made as they are, they provide evidence that they acted in a fair and impartial manner. This signals to me that the head office has at least considered the subsidiary point of view before they may have rejected it. When I understand why final strategic decisions are made as they are, I’m more inclined to implement those decisions even if I don’t particularly view them as favorable.

What Makes Due Process Important for Global Strategy Execution

As our interviews with subsidiary presidents progressed and the meaning of due process became clear, a second equally important trend became visible: those managers who believed that due process was exercised in their firms’ global strategy-making process were the same executives who trusted their head offices significantly, who were highly committed to their organizations, who felt a sense of comradeship or unity with the corporate center, and who were motivated to execute not only the letter but also the spirit of the decisions. That is, not only did subsidiary presidents articulate the importance of due process in global strategy making, but their attitudes and behavior were significantly affected by its perceived presence or absence. And not just any attitudes or behavior, but attitudes and behavior that determine the success or failure of global strategy execution.

A review of some of the most popular global strategic prescriptions makes this point clear. They are as follows: locate each value-added activity in the country that has the least cost for the factor that activity uses most intensely;4 dexterously shift capital and resources across national markets, cross-subsidizing global units, to knock out global competitors;5 institutionalize fully standardized product offerings, marketing approaches, and commonly used distribution systems worldwide to allow for maximum global efficiencies;6 and, as argued recently, consciously consolidate worldwide knowledge, technology, marketing, and production skills to build reservoirs of distinctive core competencies that can act as engines for continuous new business development, innovation, and enhanced customer value.7

Each of these global strategic prescriptions is different. There is no one formula for success. Different global competitive and economic dynamics will always dictate different and multiple routes to success. Yet a fundamental thread runs through and unites each of these prescriptions, and that is the underlying condition necessary for the effective execution of each strategy.

Ask about any of these purported global strategies: What does it take to successfully execute it? Time and again the answer involves three underlying requirements: (1) the increasing sacrifice of subsystem for system priorities and considerations; (2) swift actions in a globally coordinated manner; and (3) effective and efficient exchange relations among the nodes of the multinational’s global network. Which is to say that to implement global strategies, multinationals need subsidiary managers with a sense of commitment, trust, and social harmony. Organizational commitment inspires these managers to identify with the multinational’s global objectives and to exert effort, accept responsibility, and exercise initiative on behalf of the overall organization —despite potential “costs” at the subsidiary unit level. Trust is essential to work out mutual wills in the multinational. It inspires subsidiary managers to more readily accept in good faith the intentions, actions, and decisions of the head office instead of second guessing, procrastinating, and opportunistically haggling over each directive. Which is to say that trust is necessary for quick and coordinated global actions. Lastly, social harmony is essential to strengthen the social fabric among members of global units. It encourages efficient and effective exchange relations, which have fast become indispensable to effective global strategy execution.

These salutary attitudes, however, are not in and of themselves sufficient to make global strategies work. Beyond this, multinationals need to ensure that subsidiary managers actually engage in not only compulsory but also voluntary execution of strategic decisions. By compulsory execution, we mean carrying out the directives of global strategic decisions in accordance with the multinational’s formally required standards — satisfying, to the letter, the stipulated responsibilities. In contrast, by voluntary execution, we mean exerting effort beyond that which is formally required to execute decisions to the best of one’s abilities. Put differently, it is the effort subsidiary top managers exert beyond the call of duty to implement global strategic decisions.8

What all this suggests is that the exercise of due process in global strategic decision making represents a potentially powerful though unexplored route to the implementation of global strategies. Not only do subsidiary top managers emphasize the importance of fairness and impartiality in global strategic decision making, they are so obsessed by the existence or nonexistence of due process that it profoundly affects their attitudes and behavior — attitudes and behavior that are virtually indispensable to making global strategies work. We are talking about commitment, trust, social harmony, and the motivation to execute not only the letter but also the spirit of decisions — that is, to engage in compulsory and voluntary execution of strategic decisions.

But what about other implementation mechanisms? Are traditional implementation mechanisms alone not sufficient for the effective execution of global strategies? If not, how does due process support these traditional mechanisms to make global strategies work?

Traditional Implementation Mechanisms

As mentioned earlier, when we asked subsidiary presidents what motivated them to implement or to defy global strategic decisions, they typically began with a list of well-established administrative mechanisms. Most of them mentioned incentive compensation, monitoring systems, the fist of the head office, and the magnitude and precision of rewards and punishments. But as our discussions progressed, we found subsidiary presidents eager to add that they did not believe these implementation tools alone to be either sufficient or effective. For one thing, they were not particularly motivating. For another, the tools were increasingly easy to dodge and cheat.

Not Motivating?

I am not saying that rewards and punishments and auditing systems are useless in the implementation process. They certainly are useful. If the head office could assess exactly to what extent I followed global strategic decisions and rewarded me based precisely on that behavior, it would be a lie to say that this would not act as an incentive to execute global strategies. It would. It’s just that this would not motivate me to do more than is absolutely necessary to satisfy the minimum requirements of global strategic decisions. It wouldn’t inspire me to exert energy, exercise initiative, or to take on tasks that I am not directly compensated for in the execution of global strategies.

This comment, made by one executive, is representative of the general opinion of most of the subsidiary presidents we interviewed. Save for a few specific cases, we discovered that a reliance on instrumental approaches produced a utilitarian, contractual attitude toward compliance.9 Stated succinctly: to the extent that subsidiary top managers judge that the head office can carefully monitor their behavior and will accurately allocate rewards and punishments, managers have an incentive to satisfy the minimum requirements of global strategic decisions. No more, no less. Instrumental approaches have the power to encourage only compulsory execution —execution to the letter, not to the spirit, of the decisions. The trouble, as we have already argued, is that to make global strategies work, subsidiary managers cannot simply “execute this” or “undertake that” in some highly prescribed manner. Their actions must be secured less by rational calculations of individual gain than by kinship obligations. What we are talking about is voluntary execution. An example will bring this to life.

The Case of Global Learning

Global learning — the ability of a multinational to transfer the knowledge and expertise developed in each part of its global network to all other parts worldwide — has fast become an essential strategic asset.10 For global learning to be actualized, we argue that nothing less than an affirmative attitude toward cooperation will suffice — that is, voluntary execution. One reason for this is that knowledge and expertise are often viewed as power and as such are not easily shared. Another reason is that the major benefits of internal diffusion of knowhow accrue to recipients, not transmitters. Of course, were it possible for subsidiary units to “sell” their knowledge and expertise to other subsidiary units, these problems might be overcome. However, this is often and perhaps usually infeasible. As know-how is largely an intangible asset, its value to a “purchasing” unit cannot be known until the purchaser has it, but once the knowledge is disclosed, the purchaser has acquired it without cost.11 In the absence of economic incentives and with the presence of perceived power disincentives to diffuse knowledge and expertise, it follows that full-blown global learning will not transpire as long as quid pro quo attitudes toward strategy execution prevail. Rather, the hoarding and withholding of knowledge and expertise are far more likely.

Easy to Dodge and Cheat?

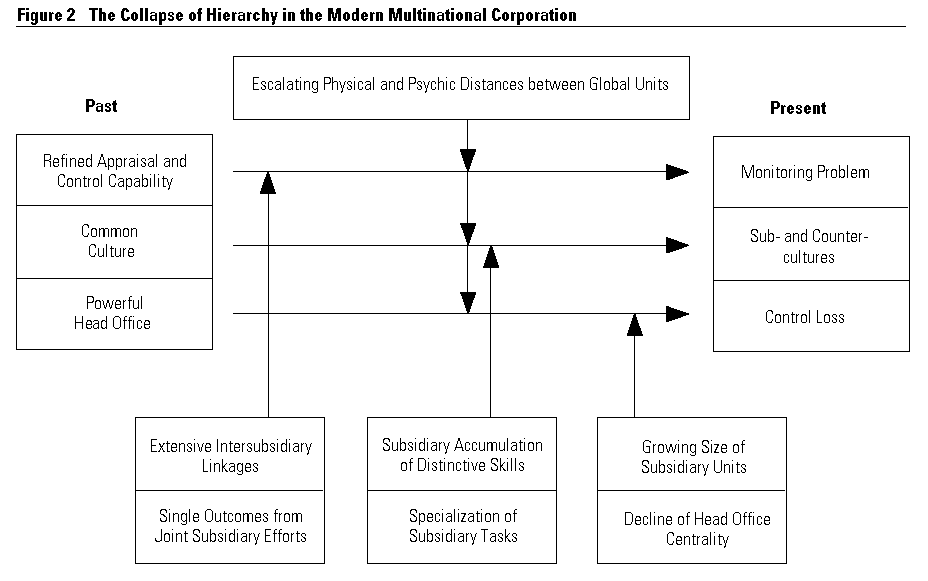

Beyond the fact that subsidiary managers do not consider these instrumental approaches to be that motivating is the reality that managers increasingly find these tools easy to dodge and cheat. And if they are easy to dodge and cheat, they are truly ineffective. Basically, the decline in their effectiveness can be explained by the collapse of the three distinctive features of hierarchy in the modern multinational. These three features are: (1) appraisal and control capability; (2) the power of the head office; and (3) common values and expectations.12 Traditional implementation tools are increasingly easy to dodge as these hierarchical features collapse.13 Let us take a quick look at the forces leading to the demise of these features.

Collapse of Appraisal and Control Capability.

International executives are witnessing a collapse in the multinationals’ appraisal and control capability. Although, in theory, information systems can be designed to meet the complexity of any organization or situation, in reality, they are having a tough time meeting the modern multinational’s demands. The predominant reason for this is the rapid increase in horizontal linkages and interdependencies across subsidiary units. As subsidiary units increasingly share resources and work together on single projects to realize global economies of scale and scope, the unique performance and contribution of each subsidiary unit is increasingly difficult to decipher.14 Distinctions between faulty and meritorious performance are becoming tenuous. Confusion opens the door for shirking, opportunistic behavior and conflict. Moreover, this problem is made even more severe by the escalating size of most multinationals. The corporate center is limited in its ability to make accurate evaluations of each subsidiary unit.

Eroding Power of the Head Office.

No longer do centrally directed orders elicit easy obedience from subsidiary units. One reason for the erosion in the head office’s hierarchical power is subsidiary units’ increasing size and resource parity. Subsidiaries are less reliant on the head office, and the head office is more dependent on subsidiary units. To the extent that dependence decreases power, the corporate center and overseas units are converging in power.15 This situation is aggravated further by the mounting intensity of direct subsidiary-to-subsidiary linkages, which lessens the head office’s centrality.16

Decline in Common Values and Expectations.

As subsidiary units have increasingly accumulated distinct resources and capabilities in response to their different task environments, they have developed values and behavioral norms distinct from those in the home office.17 On top of this, the nontrivial physical and psychic distances increasingly separating overseas units from corporate centers fuel even further the emergence of subcultures and countercultures within the modern multinational. The result is more antagonistic relations between head office and subsidiary top management teams and a natural inclination on the part of subsidiary managers to pursue subsidiary-level objectives.18

The upshot of all this is that the distinctive features of hierarchy in the multinational used to support traditional implementation mechanisms are increasingly collapsing. As shown in Figure 2, the emergence of a monitoring problem, the intensification of sub- and countercultures, and mounting control loss increasingly plague the multinational, making its traditional implementation tools less and less effective.

{kind=link}

How Does Due Process Support Traditional Implementation Mechanisms?

Although traditional implementation tools have become on the whole less effective, the extent to which this is true appears to be contingent in part on whether due process is exercised. Recall for a moment the due process characteristics. Two-way communication, the ability to refute the head office’s viewpoints, and an accounting for final strategic decisions all foster open interaction and intensive information exchange between head office and subsidiary top managers. This open interaction almost forces the head office to keep rewards, punishments, and appraisal and control systems aligned with strategic decisions. An example will make this point clear.

One subsidiary president we interviewed had been requested to institute an aggressive price-reductions policy in his local market. The strategic aim was to counter an assertive price attack launched by a global competitor in his company’s home market. The subsidiary president understood that the execution of such a policy would benefit the overall organization — it would drain the resources of the global competitor’s profit sanctuary, its home market. He also knew, however, that the policy would likely result in negative financial performance by his local operation.

The open interaction between him and the head office allowed him to address his concern directly. He stated that he understood why it was necessary for his unit to institute such a policy and that he would accept such a global strategic mission. But he argued that the execution of this mission would invalidate a sole reliance on “stand-alone” financial criteria for assessing his subsidiary unit’s performance. He proposed having his unit’s performance evaluated also by the strategic contribution it made to the overall organization. The head office managers and subsidiary president were able to develop a mutually acceptable set of performance evaluation criteria for his unit. In this way, the exercise of due process spurs the head office to keep traditional implementation tools aligned with strategic decisions.

Lessons from Our Field Observations

We can draw two overriding lessons from our field observations. The first is that the multinational increasingly faces a dilemma in executing its global strategies. On the one hand, the effective implementation of global strategies requires a sense of community and cooperation among all the nodes of the multinational’s global network. On the other hand, multinationals are experiencing a loss in hierarchical control and an increasing independence of subsidiary units, which creates an environment of calculative, utilitarian, and frictional in-terunit relations. This is not particularly conducive to efficient and effective exchange. In the face of this multinational dilemma, we need more than traditional implementation mechanisms to make global strategies work.

The second lesson is that the exercise of due process in global strategy making seems to be a powerful, yet unexplored, way to overcome the multinational dilemma and make global strategies work. This is traceable to two sources. The first is that due process helps to overcome the exchange difficulties in the multinational by inspiring a sense of commitment, trust, and social harmony among subsidiary top managers. The second is that, beyond these salutary attitudes, the exercise of due process inspires subsidiary top managers to more readily execute strategic decisions to not only the letter but also the spirit with which they were set forth.

The Tangible Effect of Due Process

At the end of our interviews, we presented our findings to the subsidiary presidents’ head office managers. These head office managers found our results fascinating and provocative. They were intrigued by our proposition that instrumental calculations of gains and losses were not the dominant driver behind subsidiary managers’ actions and found it particularly interesting that subsidiary managers had placed so much emphasis on the importance of due process in global strategy making. According to these executives, it was a challenging proposition that the presence or absence of due process had the power to influence not only the important attitudes of commitment, trust, and social harmony but also subsidiary managers’ actual execution of resulting decisions.

Nonetheless, despite the executives’ overall excitement with our findings, underneath this ran a current of hesitation. To quote one executive:

Your findings are provocative. But to institute due process in global strategy making is a time-consuming, difficult task. Before I start to embark on such an attempt, I would like to have more evidence of the tangible benefits of due process than just the observations made and insights gained from your field research.

This hesitation was valid. It challenged us to go beyond our field work and empirically test our propositions. This meant conducting an extensive mail survey to develop a bigger database that could test the validity of our field observations. In short, we set out to examine whether due process exercised a positive overall effect not only on the commitment, trust, and social harmony of subsidiary top managers but also on compulsory and voluntary execution. We also set out to test whether these effects were significantly stronger or particularly potent in those subsidiary managers who received unfavorable strategic decision outcomes vis-à-vis those who received favorable outcomes. Appendix B presents a profile of our sample population, the measurements used to estimate each variable, and the type of analyses we employed.

The Results

The results of our regression analyses confirmed our observation that due process in global strategy making is indeed positively related to subsidiary managers’ sense of organizational commitment, trust in head office management, and social harmony between them and the head office. All slope coefficients proved to be statistically significant (p<.01),19 which is to say that the more subsidiary managers believe that due process is exercised in the global strategy-making process, the more positive attitudes they have toward head office management and the organization as a whole.

Beyond this, we also found a positive relationship between due process and compulsory and voluntary execution. All slope coefficients again proved to be statistically significant (p<.01). This provides evidence that the exercise of due process does more than inspire positive attitudes. It also triggers subsidiary managers to “go the extra mile” and carry out the spirit of global strategic decisions.

More interesting from an implementation perspective, however, are the results of another analysis. We wanted to see the effect of due process when subsidiary managers judged strategic decisions to be favorable or unfavorable for their unit. By strategic decisions we mean the strategic roles, resources, and responsibilities received by subsidiary units as a result of the last annual global strategy-making process.

During the course of our interviews, one of the most fascinating things we observed was that the effect of due process on subsidiary managers’ attitudes and behavior was particularly strong precisely in those individuals who received decision outcomes viewed as unfavorable. Put differently, due process provided an especially strong “cushion of support” that mitigated the negative ramifications of unfavorable decisions by significantly inflating positive attitudes and behavior within recipients of unfavorable outcomes.20 Figures 3a through 3c show the average commitment, trust, and social harmony scores for subsidiary top managers receiving favorable versus unfavorable strategic decision outcomes. As the figures consistently reveal, when decision outcomes were viewed as unfavorable, the exercise of due process did much to check discontent and to give “loser” subsidiary managers powerful reasons to stay committed to their organization (in Figure 3a, the mean commitment score increases from 3.2 to 5.9; p<.01), to have trust in head office management (in Figure 3b, the mean trust score increases from 2.0 to 5.3; p<.01), and to cultivate an atmosphere of social harmony between them and the head office (in Figure 3c, the mean social harmony score increases from 2.3 to 4.7; p<.01). On the other hand, when outcomes were viewed as favorable, the due process effect, although undeniably present, was not as potent as with unfavorable outcomes. In particular, as due process heightened, the mean score for commitment increased from 4.5 to 6.0 (p<.01), that for trust from 4.4 to 5.6 (p<.05), and that for social harmony from 3.5 to 4.8 (p<.05). For all three salutary attitudes, the slope coefficient differential between the favorable outcome and the unfavorable outcome group also proved to be statistically significant (p<.01).21

{kind=link}

{kind=link}

Figures 4a and 4b present the average compulsory and voluntary execution scores for subsidiary top managers receiving favorable versus unfavorable strategic decision outcomes. As Figure 4a reveals, the use of due process in global strategic decision making indeed appears to boost compulsory execution in managers who receive unfavorable decision outcomes to a greater extent than in those who received favorable outcomes. Specifically, when decision outcomes were judged unfavorable, the exercise of due process did much to motivate subsidiary managers to perform the strategic roles and responsibilities assigned to their unit in accordance with the organization’s formal requirements (mean compulsory execution score increased from 3.8 to 5.7; p<.01). On the other hand, when outcomes were viewed as favorable, the due process effect on compulsory execution, although undeniably present, was not as potent (mean score increased from 5.2 to 6.2; p<.05). The slope coefficient differential between the favorable outcome and the unfavorable outcome group proved to be statistically significant (p<.05).22

{kind=link}

The same cannot be said, however, for voluntary execution. On the one hand, the voluntary execution of all subsidiary top managers significantly escalates as due process increases (in Figure 4b, mean voluntary execution score increases from 2.4 to 5.2 for recipients of unfavorable outcomes and from 2.9 to 5.5 for recipients of favorable outcomes; both significant at p<.01). On the other hand, the effect of due process on voluntary execution does not vary whether the decision outcomes are favorable or not. For voluntary execution, the slope coefficient differential between the favorable outcome and the unfavorable outcome group proved to be statistically not significant (p>.10).23 These findings indicate that although decision outcomes do not seem to affect subsidiary managers’ voluntary execution, the exercise of due process does inspire these managers to go beyond the call of duty to implement strategic decisions. This is further supported by our regression result that decision outcomes had no relationship with voluntary execution; the regression coefficient for this relationship was not statistically significant (p>.10).

In summary, except in the case of voluntary execution, with a low level of due process, there is a big gap between the attitudes and behavior of subsidiary top managers with favorable and unfavorable decision outcomes.24 As expected, with a low level of due process,subsidiary managers with unfavorable decision outcomes were generally dissatisfied with the head office and the overall organization and consequently felt a low level of commitment, trust, and social harmony. Not surprisingly, these same managers were not highly motivated to execute global strategic decisions to the letter or spirit with which they were set forth.

However, with a high level of due process, the picture was different. There was little gap between those managers who had received favorable and unfavorable decision outcomes in their reported scores of commitment, trust, and social harmony and compulsory and voluntary execution; all these gaps proved to be statistically not significant (p>.10). Hence, the gap was significantly reduced as due process heightened. Which is to say that the power of due process is strong enough to overcome the negative ramifications of unfavorable outcomes and even inspires in those subsidiary top managers the positive disposition necessary for global strategy execution. Moreover, whether managers received favorable or unfavorable outcomes, their degree of commitment, trust, and social harmony and compulsory and voluntary execution was much higher when due process was exercised in global strategy making than when it was not. Hence, our empirical tests strongly support our field observations.

Conclusion

How can multinationals make global strategies work? The results of this research suggest that the answer resides in the quality of the global strategy-making process itself. When deciding whether or not or to what extent to carry out global strategic decisions, subsidiary top managers accord great importance to the way in which global strategies are generated. Their overriding concern: Is due process exercised in the global strategy-making process?

In the presence of due process, subsidiary managers are motivated to implement global strategies. They feel a strong sense of organizational commitment, trust in head office management, and social harmony with their head office counterparts. These attitudes are not only important, they are the fundamental requirements for making global strategies work. Further, the exercise of due process translates directly into a high level of compulsory and voluntary execution, which is to say that due process motivates managers not only to fulfill corporate standards but also to exert voluntary effort to implement strategic decisions to the best of their ability. The power of due process in this regard is more remarkable when we consider our finding that voluntary execution was induced only by due process and not by the instrumental value of decision outcomes. In the absence of due process, the effect is just the reverse. Subsidiary top managers are frustrated with the head office, the overall organization, and the resulting global strategic decisions. This diminishes fast their willingness to execute global strategies.

But beyond this, what makes due process particularly significant for global strategy execution is that its effect on salutary attitudes and implementation behavior is especially strong in managers who receive unfavorable decision outcomes. This is one of the most critical tasks for global strategy execution. After all, it is precisely those managers who are inclined to subvert, undermine, and even sabotage global strategic decisions. This is a significant issue because the intensity of global competition and the requirements of winning global strategies require an increasing number of decisions that are perceived as unfavorable.

Examples Abound

There are many examples of unfavorable decisions. In one multinational we studied, subsidiary units were recently asked to forgo their national products in favor of global core products that many units considered to be either overstandardized or overpriced for their national markets. In another multinational, the U.S. subsidiary was required to transfer a large portion of its export sales to its sister European subsidiaries. Although this substitution substantially increased capacity utilization rates in Europe and decreased the losses suffered from over-capacity there, as one U.S. executive put it, “The transfer was nothing but a loss for us.” And so the list goes, endlessly on. To cite one executive:

Our modern enterprises live in a world of global competition. The key to win here is to think globally and fully leverage our globally dispersed resources, skills, and knowledge. It is important to maximize our efficiency at the global level. To achieve this, it is unavoidable that an increasing number of subsidiaries will end up receiving unfavorable decision outcomes from their individual standpoints. No doubt, these subsidiary units will be more inclined to foot-drag and exert counterefforts than to execute global strategies. The question is then, how can we turn around these negative attitudes and inspire subsidiary units to follow and implement a global approach?

To make global strategies work, head office executives need to pay greater attention to the way they generate global strategic decisions. Although the exercise of due process by itself does not make difficult head office – subsidiary issues vanish, it does motivate subsidiary managers to accept and implement global strategies. The image of the subsidiary manager that emerges here stands in marked contrast with that of the organization man who is driven overridingly by concerns of instrumental and economic maximization. It seems that subsidiary managers are both sensitive and responsive to issues of fairness in decision-making processes. Given that both our field observations and our empirical study consistently support the importance of due process, maybe it is time that companies seriously reflect on just what they have been doing to motivate their subsidiary top managers to implement global strategies. They need to pay more heed to the importance of due process in global strategy making.

Appendix A

How did we conduct our field research? We solicited the participation of twenty-five multinationals by means of direct and indirect personal contacts with head office senior executives. Nineteen of these multinationals agreed to support this research, and they gave us the names of the subsidiary presidents heading their ten largest subsidiary operations in terms of annual sales. The dominant industries of these nineteen multinationals were: computers (five firms), packaged foods (four), electrical products (four), pharmaceuticals (three), automobiles (one), paper and wood products (one), and textiles (one).

We were able to successfully contact, via telephone, 141 of the subsidiary presidents. We guaranteed that all comments would be held strictly confidential and used solely for scientific research and that their head office managers would not be informed as to which subsidiary presidents ultimately participated in our study. Sixty-three of these subsidiary presidents were willing to participate. The remaining subsidiary presidents declined, most frequently because of a lack of time. We then held extensive interviews.

Appendix B

Sample Population

We distributed the mail questionnaire to 195 subsidiary top managers. This pool comprised the 63 subsidiary presidents who participated in our field research and 132 other subsidiary top managers who directly participated in the last annual global strategic decision-making process between the head office and their national unit. The latter were also members of our nineteen original participating multinationals; their names were supplied by the 63 subsidiary presidents.25 The titles of the subsidiary top managers ranged from president to executive vice president to director. These executives were considered to represent the key catalysts for global strategy execution in their national units.

We distributed the questionnaire within six weeks of the completion of the last annual global strategic decision-making process of our nineteen participating multinationals. Of the 195 questionnaires distributed, 142 were returned to the researchers. The questionnaire assessed the extent of due process in the last strategy-making process, subsidiary top managers’ attitudes of organizational commitment, trust, and social harmony, and the perceived favorability of strategic decision outcomes.

Ten months later, just before the start of another annual global strategic decision-making process, we distributed a second questionnaire to the 142 managers who responded to our first-round questionnaire. In this one, we assessed subsidiary top managers’ compulsory and voluntary execution of the global strategic decisions resulting from the preceding annual strategy-making process. Of these, 119 questionnaires were returned to the researchers and used in our analysis of the relationship between due process and compulsory and voluntary execution.26

Measurements

Due Process.

To assess whether or to what extent due process was exercised in global strategic decision making, we used a five-item measure in our survey questionnaire.27 This involved having subsidiary top managers evaluate on a seven-point Likert-type scale each of the five identified aspects of due process, in short: (1) the extent to which the head office is knowledgeable of the subsidiary unit’s local situation; (2) the extent to which two-way communication exists in the process; (3) the extent to which the head office is fairly consistent in making global strategic decisions across subsidiary units; (4) the extent to which subsidiary top managers can legitimately challenge the strategic views and decisions of the head office; and (5) the extent to which subsidiary top managers receive a full explanation for global strategic decisions.28 The Cronbach’s coefficient alpha for this five-item scale was .86.29

Organizational Commitment.

Nine items were used to assess the top managers’ organizational commitment.30 Sample items include, “I am willing to put in a great deal of effort beyond that normally expected in order to help this organization be successful,” and “This organization really inspires the very best in me in the way of job performance.” All items were assessed on a seven-point scale with anchors labeled (1) strongly disagree and (7) strongly agree. The Cronbach’s coefficient alpha for this nine-item scale was .91.

Trust in Head Office Management.

To measure the trust subsidiary top managers have in the head office, we used four questions.31 These are:

- How much confidence and trust do you have in head office management?

- Head office management at times must make decisions that seem to be against the interests of your unit. When this happens, how much trust do you have that your unit’s current sacrifice will be justified by the head office’s future support for your unit?

- How willing are you to accept and follow those strategic decisions made by head office management?

- How free do you feel to discuss with head office management the problems and difficulties faced by your unit without fear of jeopardizing your position or having your comment “held against” you later on?

Again, all four items were measured on seven-point scales. The Cronbach’s coefficient alpha for this four-item scale was .94.

Social Harmony.

A four-item measure assessed the perceived social harmony between head office and subsidiary top managers.32 The managers were asked to think of their relations with head office management when answering the following items: (1) how well they help each other out; (2) how well they get along with one another; (3) how well they stick together; and (4) the extent to which conflict characterizes their relations. These items were measured on seven-point scales with the fourth item reversely scored. The Cronbach’s coefficient alpha for this four-item scale was .87.

Strategic Decision Outcome Favorability.

Four items assessed the perceived favorability of global strategic decisions received by subsidiary units as a result of the last annual global strategic decision-making process.33 Subsidiary top managers were asked to assess the extent to which the global strategic roles, responsibilities, and resources allocated to their unit: (1) reflected their unit’s individual performance achieved; (2) mirrored their unit’s relative contribution to the overall organization; (3) exceeded their unit’s expectations; and (4) were absolutely favorable. All four items were measured on seven-point scales. The Cronbach’s coefficient alpha for this four-item scale was .83.

Compulsory Execution.

To assess the extent to which each subsidiary top manager carried out global strategic decisions in accordance with their formally required corporate standards, two questions were posed. First, for each of eight major activities (marketing and sales, research and development, manufacturing, purchasing, cost-reduction programs, general cash-flow utilization, human resource management, and other administrative activities), subsidiary top managers were asked to respond on a seven-point (1=not at all, 7=completely) scale to the following question: “Please try to recall as accurately as possible your overall behavior and actions taken since the preceding annual global strategic decision process between the head office and your national unit. Then for each of the eight outlined activities indicate the extent to which you executed these decisions in accordance with your organization’s required standards. Note that you should not include in this assessment any efforts that may have been extended beyond your organization’s required standards in order to achieve optimum performance in these activities.” Organization was defined here as the multinational.

For each of these eight activities, we then had subsidiary top management rate on a five-point scale, ranging from “1=not important” to “5=extremely important,” the degree of importance of each of these activities to the successful fulfillment of their overall job requirements. This assessment is important because although each of our respondents was a top manager with overarching responsibilities for and involvement in overall subsidiary unit operations across these activities, many reported having full responsibility for some activities but having only limited responsibility in the sense of giving final approval in other activities. Accordingly, to assess the extent of each manager’s compulsory execution, these importance ratings were used as weights to reflect each activity’s relative contribution or importance to the fulfillment of each manager’s overall job requirements. Using these weights, we then obtained each manager’s weighted-average compulsory execution score. Specifically, for each manager, we first multiplied the manager’s compulsory execution score on each of the eight activities by his or her corresponding importance ratings and then added these weighted execution scores. Finally, we divided this added figure back by the sum of these importance ratings to arrive at each manager’s weighted-average compulsory execution score.34

Voluntary Execution.

To assess the extent to which subsidiary top managers exerted voluntary effort to carry out global strategic decisions to the best of their abilities, we used a similar approach to that used in our assessment of compulsory execution. First, for each of the eight major activities, the managers were asked to respond on a seven-point scale (1=not at all, 7=greatly) to the following question: “Please try to recall as accurately as possible your overall behavior and actions taken since the preceding annual global strategic decision process between the head office and your national unit. Then for each of the eight outlined activities indicate the extent to which you voluntarily exerted effort beyond the formally required standards of your organization to execute global strategic decisions to the best of your abilities. Rephrased, to what extent did you willingly exert energy, exercise initiative, and devote your effort beyond that which is formally required to achieve optimum performance in your execution of global strategic decisions in each of these activities?”

Using the same question on dimensional importance described above for compulsory execution to obtain weights, we derived a weighted-average measure of each manager’s voluntary execution of global strategic decisions. The process used to derive this weighted-average measure of voluntary execution mirrors that used to arrive at our weighted-average measure of compulsory execution.35

Analyses

We used two tests to establish the effect of due process on the managers’ attitudes and behavior. First, we performed regression analyses to see whether due process positively correlated with the managers’ attitudes of organizational commitment, trust in head office management, and social harmony between them and head office management and whether due process was also related to the managers’ compulsory and voluntary execution of the resulting decisions.

Second, we tested whether due process produces a “cushion of support” that enhances salutary attitudes and execution to a greater extent in those managers who received unfavorable decision outcomes than those who received favorable outcomes. To perform this test, we first divided respondents into two groups based on the perceived favorability or unfavorability of strategic decision outcomes received in the last annual strategy-making process. Those managers with outcome favorability scores above the sample mean were classified as recipients of favorable strategic decision outcomes; those below the sample mean were classified as recipients of unfavorable outcomes. We then further split our respondents based on the perceived degree of due process exercised. Respondents with due process scores above the sample mean were treated as experiencing a high level of due process, whereas those having due process scores below the sample mean were treated as experiencing a low level of due process. Finally, we calculated and compared the mean levels of reported organizational commitment, trust in head office management, social harmony, and compulsory and voluntary execution for each of our four groups: the high outcome favorability – high due process group; the high outcome favorability – low due process group; the low outcome favorability – high due process group; and the low outcome favorability – low due process group. As is described in the article, we used variance analysis and the slope coefficient differential test to test differences between these four groups. We observed no evidence for systematic differences in contextual variables such as industry type and subsidiary size across these four groups.

References

1. For an excellent review of the literature on global strategy, see:

S. Ghoshal, “Global Strategy: An Organizing Framework,” Strategic Management Journal 8 (1987): 425–440.

2. For an extensive discussion on our field study, see:

W.C. Kim and R.A. Mauborgne, “Implementing Global Strategies: The Role of Procedural Justice,” Strategic Management Journal 12 (1991): 125–143; and

W.C. Kim and R.A. Mauborgne, “Procedural Justice Theory and the Multinational Organization,” in Organization Theory and the Multinational Corporation, eds. S. Ghoshal and E. Westney (London: MacMillan, 1993a).

3. The Q-sort technique was used to define the meaning of due process in global strategic decision making. For a detailed explanation of this process, see:

Kim and Mauborgne (1991 and 1993a).

4. B. Kogut, “Designing Global Strategies: Comparative and Competitive Value-Added Chains,” Sloan Management Review, Summer 1985, pp. 15–28; and

M.E. Porter, “Competition in Global Industries: A Conceptual Framework,” in Competition in Global Industries, ed. M.E. Porter (Boston: Harvard Business School Press, 1986).

5. G. Hamel and C.K. Prahalad, “Do You Really Have a Global Strategy?” Harvard Business Review, July–August 1985, pp. 139–148; and

W.C. Kim and R.A. Mauborgne, “Becoming an Effective Global Competitor,” The Journal of Business Strategy, January–February 1988, pp. 33–37.

6. T. Levitt, “The Globalization of Markets,” Harvard Business Review, May–June 1983, pp. 92–102; and

G.S. Yip, “Global Strategy...In a World of Nations?” Sloan Management Review, Fall 1989, pp. 29–41.

7. C.K. Prahalad and G. Hamel, “The Core Competence of the Corporation,” Harvard Business Review, May–June 1990, pp. 79–91.

8. For an extensive discussion of these two forms of compliance, both the conceptual distinction between them and their theoretical root, see:

C. O’Reilly and J. Chatman, “Organizational Commitment andPsychological Attachment: The Effects of Compliance, Identification, and Internalization on Prosocial Behavior,” Journal of Applied Psychology 71 (1986): 492–499; and

P.M. Blau and W.R. Scott, Formal Organizations (San Francisco, California: Chandler Publishing Company, 1962), pp. 140–141.

9. That a reliance on instrumental approaches to compliance leads to utilitarian contractual attitude toward involvement relations finds strong support in the award-winning article:

J. Kerr and J.W. Slocum, “Managing Corporate Culture through Reward Systems,” Academy of Management Executive 1 (1987): 99–108.

10. C.A. Bartlett and S. Ghoshal, “Managing across Borders: New Strategic Requirements,” Sloan Management Review, Summer 1987, pp. 7–16; and

S. Ghoshal and C.A. Bartlett, “Creation, Adoption, and Diffusion of Innovations by Subsidiaries of Multinational Corporations,” Journal of International Business Studies, Fall 1988, pp. 365–388.

11. K.J. Arrow, “The Organization of Economic Activity,” The Analysis and Evaluation of Public Expenditure: The PPB System (Joint Economic Committee, Ninety-first Congress, First Session, 1969), pp. 59–73.

12. For a brilliant discussion on the distinctive powers of hierarchy and internal organization, see:

O.E. Williamson, Markets and Hierarchies: Analysis and Antitrust Implications (New York: Free Press, 1975).

13. See the perspicacious article by Hedlund for further support for this argument:

G. Hedlund, “The Hypermodern MNC-A Heterarchy?” Human Resource Management 25 (1986): pp. 9–25.

14. For an extensive discussion on the ways in which interdependencies and joint efforts confound accountability and create monitoring difficulties, see:

G.R. Jones and C.W.L. Hill, “Transaction Cost Analysis of Strategy-Structure Choice,” Strategic Management Journal 9 (1988): 159–172.

15. For an excellent discussion on the inverse relationship between power and dependence, see, for example:

R.M. Emerson, “Power-Dependence Relations,” American Sociological Review 27 (1962): 31–41.

16. For a discussion on the ways in which centrality affects power relations, see:

L.C. Freeman, “Centrality in Social Networks: Conceptual Clarification,” Social Networks 2 (1979): 215–239.

17. That business units’ or divisions’ accumulation of distinct capabilities and tasks reinforces distinct values and behavioral norms was empirically validated. See:

P.R. Lawrence and J.W. Lorsch, Organization and Environment (Boston: Harvard University Press, 1967).

18. See Hedlund (1986) for further elaboration of this point.

19. That the exercise of due process or, as it is often referred to, procedural justice, has the power to effectuate the higher-order attitudes of commitment, trust, and social harmony finds theoretical and empirical support in other settings. See, for example:

S. Alexander and M. Ruderman, “The Role of Procedural and Distributive Justice in Organizational Behavior,” Social Psychology Research 1 (1987): 177–198; and

R. Folger and M. Konovsky, “Effects of Procedural and Distributive Justice on Reactions to Pay Raise Decisions,” Academy of Management Journal 32 (1989): 115–130; and

E.A. Lind and T.R. Tyler, The Psychology of Procedural Justice (New York: Plenum, 1988).

20. This “cushion of support” effect not only finds support in the existing procedural justice literature but is recognized to be one of the most important effects of procedural justice or due process. See, for example:

Lind and Tyler (1988); and

T.R. Tyler, Why People Obey the Law: Procedural Justice, Legitimacy, and Compliance (New Haven, Connecticut: Yale University Press, 1990).

21. We examined and confirmed the statistical difference in the due process effect between the favorable outcome and the unfavorable outcome group for organizational commitment, trust in head office management, and social harmony. This was done using what econometricians call the Chow test, which is able to examine the statistical significance in slope differentials between the groups. In our case, test statistics of F values for all three salutary attitudes were significant at the 1 percent level and hence indicated to reject the null hypotheses that no slope coefficient difference exists between the favorable outcome and the unfavorable outcome group. For a detailed discussion on the Chow test, see:

G.C. Chow, “Tests of Equality between Subsets of Coefficients in Two Linear Regression,” Econometrica (1960): 591–605.

22. The F value for compulsory execution was significant at the 5 percent level and hence indicated to reject the null hypothesis that no slope coefficient difference exists between the favorable outcome and the unfavorable outcome group. Ibid.

23. The F value for voluntary execution was not significant (p>.10) and hence indicated not to reject the null hypothesis that no slope coefficient difference exists between the favorable outcome and the unfavorable outcome group. Ibid.

24. Variance analysis was employed to assess the statistical significance in the mean difference between the groups.

25. For an extensive discussion on the design and administration of our mail questionnaire, see:

Kim and Mauborgne (1991 and 1993a).

26. For an extensive discussion on the design and administration of the second-wave questionnaire of our longitudinal study on subsidiary top managers’ strategy execution, see:

W.C. Kim and R.A. Mauborgne, “Procedural Justice, Attitudes, and Subsidiary Top Management Compliance with Multinationals’ Corporate Strategic Decisions,” Academy of Management Journal, forthcoming, June 1993b.

27. Kim and Mauborgne (1991 and 1993a).

28. We averaged the scores for these multiple items to estimate our due process measure. The same procedure was used for all of our other multi-item measures: organizational commitment, trust, social harmony, and strategic decision outcome favorability. For a detailed discussion on why this simple averaging approach yields an unbiased estimate, see:

H.M. Blalock, “Multiple Indicators and the Causal Approach to Measurement Error,” American Journal of Sociology 75 (1969): 264–272.

29. The Cronbach’s coefficient alpha indicates the internal consistency reliability of a scale. Generally, a multi-item scale can be judged to be reliable when the value of its Cronbach alpha exceeds 0.70. Notice here that besides our due process measure, all of our other multi-item scales can be said to be reliable. For a detailed discussion on a measure’s reliability, see:

J. Nunnally, Psychometric Methods (New York: McGraw-Hill, 1978).

30. The nine-item measure used to assess organizational commitment was developed by:

R.T. Mowday, R.M. Steers, and L.W. Porter, “The Measurement of Organizational Commitment,” Journal of Vocational Behavior 14 (1979): 224–247.

31. The items used to measure trust were drawn from the interpersonal trust measures of:

W.H. Read, “Upward Communication in Industrial Hierarchies,” Human Relations 15 (1962): 3–15; and

R. Likert, The Human Organization (New York: McGraw-Hill, 1967).

32. The indicators used to measure social harmony were drawn from the cohesiveness index developed by:

S.E. Seashore, Group Cohesiveness in the Industrial Work Group (Ann Arbor: University of Michigan Press, 1954); and

C. Cammann, M. Fichman, G. Douglas, and J.R. Klesh, “Assessing Attitudes and Perceptions of Organizational Members,” in Assessing Organizational Change, eds. S.E. Seashore, E.E. Lawler, P.H. Mirvis, and C. Cammann (New York: John Wiley & Sons, 1983).

33. The four-item measure used to assess strategic decision outcome favorability was originally developed by:

Kim and Mauborgne (1991).

34. The use of a multidimensional approach with criterion weights to measure both compulsory and voluntary execution is in line with Steer’s advice and seemed particularly appropriate for taking into account subsidiary top managers’ different levels of involvement in carrying out these activities and hence their different levels of contribution to the execution of these activities in accordance with their formal job requirements. See:

R.M. Steers, “Problems in the Measurement of Organizational Effectiveness,” Administrative Science Quarterly 20 (1975): 546–558.

35. Ibid.