Managing Foreign Exchange for Competitive Advantage

GENERALS PLANNING military action and CEOs plotting corporate strategy often start from the same point: they identify the key strengths and weaknesses of their position vis-à-vis their rivals and develop a strategy to exploit the strengths and protect the weaknesses. In the corporate world many factors come into play, including quality of product, service, and availability, but two factors stand out because of their direct effect on the bottom line: pricing and cost of production. Senior managers across a wide spectrum of industries devote considerable thought to optimizing these two factors, but often ignore or underestimate a powerful force that influences them: the relative value of the currencies in which revenues and costs are denominated.

In the Bretton Woods world of stable exchange rates, currency values were less significant.1 At that time, pricing and volume determined revenues and relative labor and material costs determined production decisions. Today the world is different. Many U.S. corporations with large international businesses have seen their stock prices drop because investors have feared that a strong dollar would reduce the contribution of overseas operations to sales and earnings growth. Exporters in the United States are worried that a stronger dollar will cut into their profit margins.

Despite these developments, corporate management has been slow to grasp the full importance of foreign exchange movements. While most multinational firms are quite active in the foreign exchange market, they expend most of their effort protecting their near-term reported results, and they allow relatively low-level managers to make decisions about their foreign exchange activities. This is unlikely to continue. The increasingly global structure of the world economy and the increased volatility of exchange rates will make it imperative that firms use foreign exchange as a strategic tool in the battle for worldwide market share and profits.

The Evolving Global Market

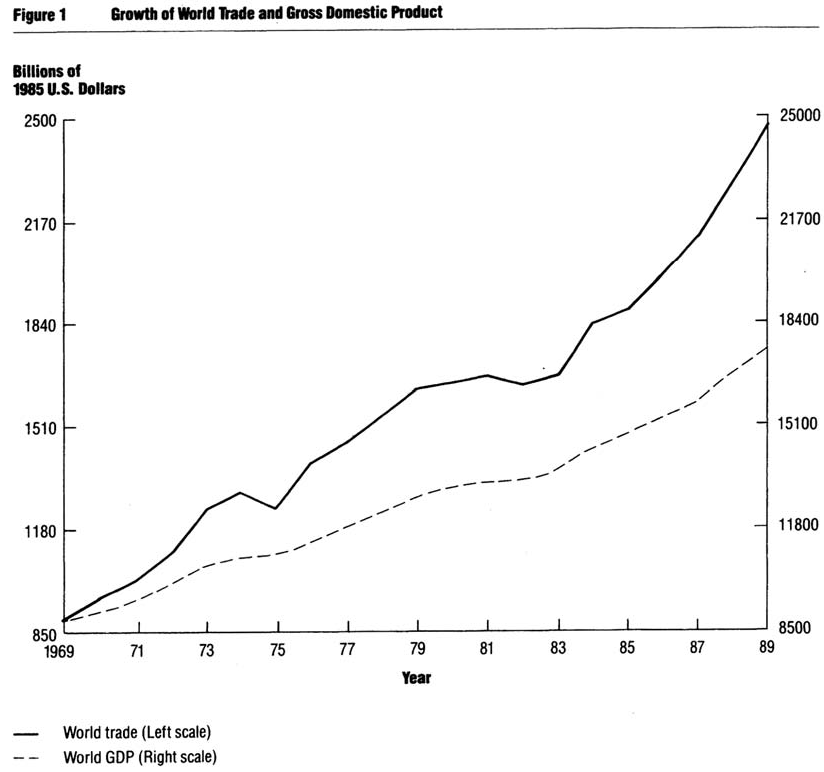

Although globalization means different things to different businesses, there is no debate that it is happening. Figure 1 compares the growth of world trade with that of world gross domestic product (GDP) over the last twenty years, assuming parity in 1968. Worldwide reductions in trade barriers, the effects of the General Agreement on Tariffs and Trade (GATT), and increasingly specialized manufacturing have increased the value of goods travelling across borders faster than the actual production of those goods has increased.

{kind=link}

References

1. Representatives of forty-four nations met in Bretton Woods, New Hampshire, in 1944 to forge the Bretton Woods Agreement that established the International Monetary Fund and the International Bank for Reconstruction and Development.

2. The Economist, 4 April 1987, p. 81.

3. J. Madura, International Financial Management, 2d ed. (St. Paul, Minnesota: West Publishing, 1986), p. 249.

4. Egon Zehnder International, Inc., “1989 Directors Survey,” Corporate Issue Monitor 4 (1989): 3.

5. With the recent adoption of SFAS 105, which deals with the disclosure of information about financial instruments with off balance sheet risk, outside analysts should be better able to identify the financial actions taken by individual compa-