The Risk of Not Investing in a Recession

Two very different ways of thinking about investment and risk are headed for a showdown. One emphasizes the financial risk of investing; the other concerns the competitive risk of not investing. In normal times, the bearishness of the former tends to (or is supposed to) complement the bullishness of the latter. But the balance between the two seems to break down at business cycle extremes. Specifically, at the bottom of the business cycle, companies seem to overemphasize the financial risk of investing at the expense of the competitive risk of not investing. Once-in-a-cycle errors of this sort can create a lasting competitive disadvantage, which is reason enough to write (and read) an article on the risk of not investing while the economy is still weak.

Risk — Financial and Competitive

By risk, I mean what managers mean: failure to achieve satisfactory performance along some dimension. The financial risk of investing is the failure to achieve satisfactory financial returns from an investment. And the competitive risk of not investing is the failure to retain a satisfactory competitive position for lack of investment. Of course, it doesn’t make sense to stamp out either type of risk, even though financial risk could be eliminated by investing not at all and competitive risk could be eliminated by investing indiscriminately. Instead, a balance must be struck between the types of errors implicit in these two types of risk: the error of pursuing too many unprofitable investment opportunities as opposed to the error of passing up too many potentially profitable ones.

As one might expect, companies have devised arrangements for dealing with both financial and competitive risks. These arrangements can be associated, respectively, with their capital budgeting and strategic planning processes. Capital budgeting tends to be a bottom-up process in which investment proposals are filtered through screens that are intended to limit financial risk. A decade has passed since Hayes and Garvin pointed out in their landmark article, “Managing as if Tomorrow Mattered,” that the capital budgeting processes at U.S. companies discounted competitive risk as well as cash flows.1 That bias persists and seems likely to do so well into the next century (see the sidebar, “Capital Budgeting and Competitive Risk”).

To address competitive risk, managers have turned, instead, to strategic planning. Strategic planning is more of a top-down process than capital budgeting: it influences how investment proposals are (or aren’t) defined, evaluated, and implemented. The focus of strategic planning has shifted since the late 1970s from basic forecasting to an external orientation that is more responsive to competitive pressures and that is intended, in part, to countervail the financial emphasis of capital budgeting.

How effectively do companies use capital budgeting, strategic planning, and the other processes at their disposal to trade off financial and competitive risk? This question is particularly controversial in the United States, where a debate rages about whether national competitiveness has declined and, if so, whether the decline is due, in part, to investment rates that have been persistently lower in the United States than in Japan or (West) Germany.

In this article, I will not attempt to answer the question of whether U.S. companies are investing enough in the future. Instead, I will emphasize the importance of maintaining a balance between financial and competitive risk. I will do so by discussing business cycle downturns, when the balance is especially likely to break down.

Investment during Downturns

Some insight into the balance that is actually struck between financial and competitive risk can be obtained by tracking investment over time. Investment turns out to be very volatile over the business cycle. For the sake of concreteness, I will illustrate this point using U.S. investment in physical capital during the last few decades, although other countries and other forms of investment (training, research and development, advertising, and other marketing communications) could also be used. During general business downturns, such investment has tended to decline two to four times as fast as output.

Business economics suggests several explanations for the macroeconomic volatility of investment. Lags in adjusting capital stocks to desired levels create an incentive to stretch out investment projects during slow periods. The heightened ambiguity about future economic prospects that often accompanies downturns may reinforce that incentive by increasing the (flexibility) value of the option of waiting to see where the economy is headed. And downturns may combine with debt service and other obligations to create liquidity crunches that rule out even desired investments.

Although such effects contribute to the volatility of investment over the business cycle, quite a few economists think that that volatility is excessive rather than efficient and, to a significant extent, self-imposed. John Maynard Keynes emphasized as much in his original discussion of the investment process and managers’ “animal spirits.” Keynes fell back on a general drop in business confidence as the major reason managers might voluntarily cut investment too much during business downturns. Several less arbitrary sets of reasons have since been identified. They can be classified as operating on the individual, group, or organizational levels.

At an individual level, financial risk, which involves out-of-pocket costs and the prospect of red ink, may loom larger than competitive risk, which involves “only” opportunity costs. Any such perceptual mismatch is likely to loom largest at business cycle downturns, assuming that is when managers are most likely to see red.

At the group level, there are several additional reasons for underinvestment during downturns, all involving herd behavior. A herd mentality is a plausible psychological affliction. Herd behavior can also be a rational response to the receipt of common information (such as a credible forecast that the economy is headed downward). Economic theory indicates, in addition, that herd behavior can be induced by information asymmetries among competitors or between managers and their employers. Whatever its sources, herd behavior implies boom-and-bust investment cycles, with the busts tending to coincide with business cycle downturns.

Finally, at the organizational level, research by Donaldson and Lorsch, among others, indicates that at least through the last downturn, many U.S. companies chose to finance investment from internal cash flow even when funds were available to them from external sources.2 Such a self-imposed constraint has the awkward effect of choking off or delaying investment during downturns as internal cash flow falls off or even moves into the red.

All of these reasons for underinvestment during downturns manifest themselves as an excessive concern with the financial risk of investing at the expense of careful consideration of the competitive risk of not investing. A case study will illustrate that this emphasis is misplaced — that although the financial risk of investing during a downturn may be high, the competitive risk of not investing can be even higher because failure to invest can permanently erode competitive position.

Competitive Risk during Downturns: A Case Study

Consider the loss of leadership by the United States in semiconductors. This case is important because sales of semiconductors may expand to several hundred billion dollars by the turn of the century; because semiconductors play a vital role in many other industries (e.g., computers, robotics, telecommunications, and consumer electronics); and because the U.S. loss of leadership to Japan in this sector mirrors patterns in a large and growing number of high-tech industries.

The semiconductor industry was dominated from its inception through the mid-1970s by U.S. competitors. The U.S. semiconductor industry benefited from access to leading-edge research at universities, Bell Labs, and other institutions; governmental support (from the Department of Defense and the National Aeronautics and Space Agency); the largest and most sophisticated home market in the world; a strong supporting cast of industries (particularly semiconductor manufacturing equipment); and vigorous rivalry, funded by venture capitalists. As a result, U.S. merchant suppliers outsold their Japanese rivals more than two-to-one through the early 1970s.

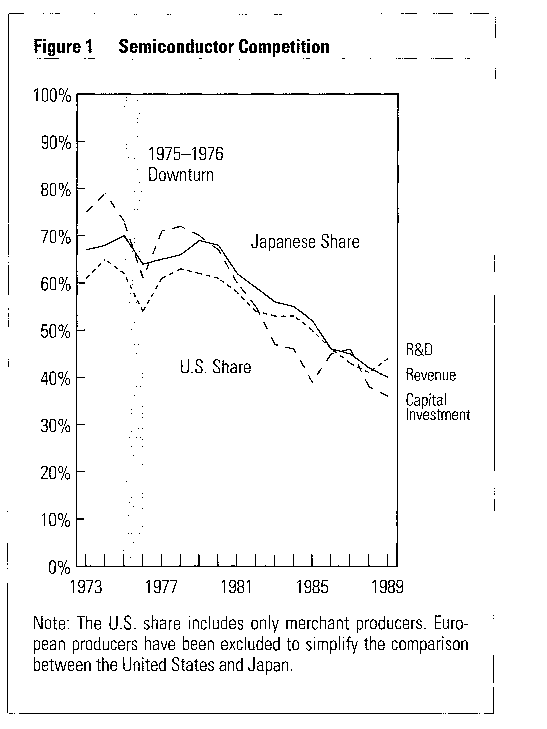

But by the end of the 1980s, U.S. merchant suppliers’ revenues had dwindled to two-thirds of the Japanese level. Although many overlapping elements caused this decline, the one I wish to focus on is the one that leaps out from a comparison of revenue shares and investment shares of Japanese and U.S. merchant suppliers from 1973 to 1989. These data, which are plotted in Figure 1, suggest that in the aftermath of the 1974–1975 recession, U.S. competitors in semiconductors took their collective foot off the investment pedal while Japanese competitors didn’t, and that the U.S. competitors have never been able to recover the ground that they lost. So striking is the pattern that it has led some to stereotype Japanese semiconductor competitors’ (relative) steadiness in investing during downturns as the archetypal Japanese competitive strategy.

{kind=link}

The data in Figure 1 are, of course, highly aggregated. Does the pattern make sense in more specific terms? Consider dynamic random access memories (DRAMs), the discrete memory chips that constitute the single largest segment of the overall market for semiconductors and that most often make the headlines. Texas Instruments and other U.S. companies introduced DRAMs with 64-component memories in the mid-1960s. They outpaced non-U.S. competitors over the next decade, introducing a new product generation (with components half the size of the previous one and with four times as much memory) every three years. By the mid-1970s, 4K (4,096 bit) DRAMs were beginning to replace IK (1,024 bit) DRAMs, and 16K DRAMs were being designed.

When the downturn hit, U.S. competitors mostly deferred their investment in capacity to produce 16K chips, but their Japanese rivals didn’t. When the upturn came, IBM and other U.S. customers, unable to source 16K DRAMs from domestic suppliers, began to turn to Japanese suppliers for the first time. This shifted the balance of trade in semiconductors to favor the Japanese, who, by 1979, had captured 43 percent of the U.S. market for 16K DRAMs. They have never looked back, with the result that there is virtually no U.S. merchant supply of DRAMs today. Failure to invest in time proved fatal in this segment for three related reasons: its very fast growth, the opportunities that it afforded for rapid yet relatively cumulative technological progress, and customers’ willingness to switch vendors if that was necessary to secure improved (next generation) chips. Note, by the way, that the critical failure occurred after the economy had bottomed out, that is, during a general recovery.

What would have happened if U.S. manufacturers had invested more aggressively in 16K DRAMs in 1975 and 1976? Although we can never be certain, one industry expert (the only one I have been able to draw out on this point) guesses that U.S. DRAM manufacturers would have managed to hang on to 95 percent of their customer base if they had invested in time. Even a 95 percent customer retention rate probably wouldn’t have let them hang on to 95 percent of their initial market share: the demand for memory chips was growing more quickly in Japan than in the United States. But such a rate might well have sustained U.S. leadership in the single most important industry segment.

Why did events take the turn they did? U.S. producers seemed, for the most part, to have adopted “balanced” capacity expansion strategies that limited investment during downturns in order to staunch losses (and push profits up during upturns). Although most U.S. producers could have invested during the 1975–1976 downturn, they stuck to those “balanced” strategies, even though they realized that their Japanese competitors were maintaining or increasing investment levels. Sadly, concern about the financial risk of investing had crowded out consideration of the competitive risk of not investing.

Recommendations

The lessons from the semiconductor story have, to some extent, been learned, at least by industry participants. Analog Devices, a competitor in nondigital semiconductor niches, has long prided itself on investing steadily over the business cycle and has apparently profited from doing so. And Intel, which dropped out of DRAMs in 1985 but maintains a strong position in other memory chips and microprocessors, recently announced that it would spend $800 million to $1 billion on plant and equipment in 1991, up from $670 million in 1990 and $450 million in 1989. According to Andy Grove, president and chief executive officer, Intel wants to move “not when the competition becomes palpable, but well before it does…. For us to have the opportunities that we have today and not bet on them, I don’t want to lose that way.”

Underlying this view is the assumption that a competitor that does not invest in the future is unlikely to have much of one. Of course, that is also likely to be the fate of a competitor that invests indiscriminately: no company can afford to make a major investment without considering its pros and cons. What managers need, in good times as well as bad ones, are not exhortations to invest or not invest but ways to separate good investment opportunities from bad ones. The rest of this section discusses how investments ought to be analyzed at cyclical extremes.3

Think Long Term

It is important to retain a long-term perspective on investment because of the lags in implementing major investment programs. Consider some cross-industry averages. As a rule of thumb, two years are required to build the average plant. Casual evidence suggests that building a new distribution system or reforming an existing one may take even longer. The mean lag in returns for R&D expenditures tends to be four to six years.4 Major changes in human resource practices (as opposed to policies) may, it has been suggested, require as many as seven years.5 And the restructuring of a corporate port-folio may take a decade or longer to implement.6

Adding the economic lives of assets to these investment implementation lags often pushes the appropriate investment planning horizon ten or more years into the future. However, the typical business cycle lasts well under a decade; the U.S. average since 1920 has been about four years. The typical macroeconomic model’s effective forecasting horizon is shorter still. These figures strongly suggest the importance of maintaining a long-term perspective on investment, one not dominated by short-term conditions.

I should emphasize that this long-term perspective is not meant to exclude consideration of cyclical fluctuations. The more cyclical the industry, the more important it is to distinguish booms from busts instead of aggregating them into an “average year.” That is why Delta Air Lines, which operates closer to the macroeconomic edge than most manufacturing companies, builds two sharp recessions into its ten-year plan. The purpose of this planning exercise is apparently to keep debt low enough to allow expansion during a general downturn.

Nor does the long-term perspective imply that temporary bargains (and other short-term phenomena) should be ignored. It may sometimes be possible to acquire assets for less than their true value during downturns. The paper industry is a case in point. Of the bargain hunters that have scored spectacular coups during slumps, Stone Container is perhaps the most notable. Stone became the world’s biggest manufacturer of brown paper bags and corrugated boxes by spending $1.7 billion between 1983 and 1987 to purchase assets from companies that were disenchanted with the brown paper business, strapped for cash, or poorly managed. Stone thereby quintupled its capacity for perhaps one-fifth of what it would have cost to build new plants. Investors were delighted: the market-to-book value ratio of the company’s stock exceeded two, and even three, through much of 1987 and 1988.

Stone’s subsequent fall from grace is a reminder, though, that one can easily overestimate one’s own bargain-hunting ability. In 1989, Stone borrowed $2.7 billion to buy Consolidated Bathurst, a leading Canadian competitor in European pulp and paper markets. Stone’s strategic intent of establishing a solid position in Europe before 1992 led it to purchase these assets toward the peak of the pulp and paper cycles and to pay more than twice as much for them (relative to replacement cost) as it had in previous acquisitions. Stone’s stock has since slumped — its market-to-book ratio has recently ranged between one-half and one — and the company has had problems servicing its debt. According to one of Stone’s (recently retired) outside directors, “Clearly we were overconfident.” While it is important not to overlook temporary bargains, it is also important not to be carried away by the prospect.

Focus on Competitive Position

Stone’s problems serve as a reminder of the pitfalls of presuming superior long-term forecasting ability. How then should the long-term profitability of investment be assessed? It is useful, in this regard, to focus on (long-term) competitive position, for three reasons. First, comparisons with competitors will foster an external orientation by forcing the organization to keep its eyes on its environment instead of on its navel. Second, even apparently minor operating differentials relative to competitors can have major effects on financial performance. In discount retailing, for example, Wal-Mart’s three percentage point operating margin advantage over K mart has, in conjunction with Wal-Mart’s faster growth, ensured that the market-to-book value ratio of its stock is seven times as high as K mart’s. Third, competitive benchmarking facilitates the long-term analysis of investment opportunities because the margin available to the organization will equal the margin of the benchmark competitor plus the organization’s competitive advantage (or minus its disadvantage).

I will draw on my own consulting experience to illustrate the logic of competitive benchmarking at cyclical extremes. In the spring of 1988, I was retained as a consultant by a chemical company that was considering spending several hundred million dollars on a new plant for making ethylene, a commodity chemical that serves as the building block for many other organic chemicals. The market for ethylene had been depressed through much of the 1970s and the 1980s, but its price had more than doubled in the previous twelve months as the supply-demand balance had tightened. One early mover had already parlayed this tightening into a billion dollar gain by buying seven ethylene plants for $1.1 billion (most of it borrowed) in 1987 and reselling them less than a year later for $2.2 billion. But by 1988, it was clear that new U.S. capacity was needed to meet the forecast market opportunity. It was unclear, though, who would actually add capacity and how much.

It would take four years to bring a new ethylene plant on stream. Given this lead time and the extreme volatility of ethylene prices, the study group agreed that we would not try to make a case for or against the new plant on the basis of particular assumptions about its timing with respect to market cycles, even though they would significantly affect its ultimate financial performance. We decided, instead, to look at whether the long-term margin expected from new capacity would allow an adequate return on the capital sunk into the project. To facilitate the analysis, we split long-term margin into three components: the average industry margin, the cost advantage of new plants relative to old plants, and the cost advantage of the client’s new plant relative to the average new plant (see Table 1).

{kind=link}

Assessment of the first component, the average long-term margin on ethylene, involved assessing the industry’s structural attractiveness in the 1990s. Would the industry go through booms and busts as it had in the 1970s and 1980s, or would it track the more stable 1960s, during which industry profitability had been quite healthy? The structural changes since the 1960s –the tripling of efficient plant scale, the maturation of the market, and the entry by oil companies and others –all appeared to increase the probability and penalties of excess capacity. This was strike one against the new plant.

The second component of the long-term analysis involved comparing the cost positions of new ethylene plants and old ones. The low operating costs of new plants would place them fairly far down the industry cost curve. But when we took account of their capital costs (which for old plants were already sunk), the total costs of new plants substantially exceeded the (operating) costs of old plants. In other words, existing plants had to operate at capacity if new ones were to make money because the improvement in ethylene process economics over time had been relatively limited. This was strike two against the new plant.

The final component of the long-term analysis involved comparing the relative costs of the new plant the client was contemplating and the capacity competitors might add. The competitors who were judged most likely to expand to meet the market opportunity were expected to add full-scale plants, each capable of producing up to 1.5 billion pounds of ethylene per year. Because this scale was incompatible with the client’s resources and other plans, the company was contemplating a smaller addition. Subscale design significantly increased the investment required per pound of ethylene capacity, to an extent that more than offset the client’s other advantages. This was the third strike against the option of adding a plant as soon as possible. The client decided not to expand in ethylene, at least until it could do so at full scale. Today, it is glad that it did not do so.

Recognize the Moving Baseline

The analysis of long-term competitive position provides a useful benchmark for deciding whether to invest. It is an incomplete basis for choice, however, because reactions by competitors, buyers, and suppliers typically shrink the returns. This threat to strategies that focus purely on positioning deserves to be stressed because managers seem to slight issues regarding the (un)sustainability of superior positions.

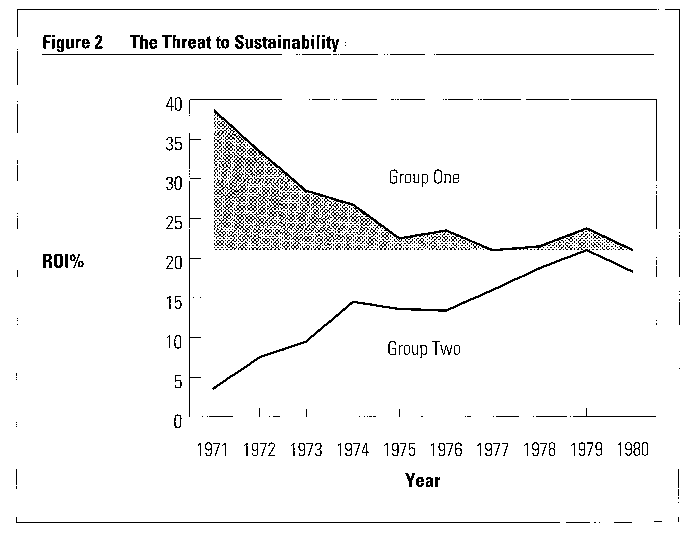

Consider the returns on investment (ROI) reported over the 1971 to 1980 period by the 692 business units in the Profit Impact of Market Strategy (PIMS) database for which such data were available. I split this sample into two equal-sized groups based on their ROI in year one and, keeping businesses in the groups in which they started out, tracked the group averages through year ten. In year one, the top groups ROI was 39 percent and the bottom groups was 3 percent. It is safe to say that the businesses in the top group started out with generally superior positions and those in the bottom group with generally inferior ones. What do you think happened to that thirty-six-point spread between year one and year ten?

Managers that I have asked have tended to guess that the initial ROI spread between the two groups shrank by one-third to one-half over the ten-year period. Figure 2 indicates that the correct answer is greater than nine-tenths! It is the basis of my claim that managers should think harder about the (un)sustainability of the superior positions to which they aspire.

{kind=link}

Although sustainability is a topic of general strategic significance, it is particularly important in the context of investment because investment can help a company achieve a sustainable advantage or avoid a sustained disadvantage. The simplest way of thinking through these benefits of investment is to compare the competitive implications of investing and not investing. In a previous article, I described the sustainable competitive advantages that might be created through investment.7 Now I want to take a complementary perspective: the risk of a permanent erosion of competitive position as a consequence of not investing.

The importance of thinking through sustainability from this perspective is illustrated by De Beers, the orchestrator of the most successful cartel of modern times. De Beers’s share of world diamond production has slipped steadily with the discovery of diamond mines outside South Africa: from 95 percent at the end of the nineteenth century to 10 percent today. De Beers nevertheless dominates the industry through its distribution arm, the Central Selling Organization (CSO), which markets 80 percent to 85 percent of the worlds rough (uncut) diamond supply on the basis of multi-year contracts with independent producers and its own captive production. The CSO functions, in effect, as a valve that regulates the flow of rough diamonds into the market.

This function was sorely tested by the short, sharp rescession of the early 1980s, which reduced final demand for polished diamonds by 5 percent. Destocking by jewelry retailers and manufacturers and by diamond dealers and cutters compounded this change as it traveled back up the pipeline: the demand for CSO s rough diamonds collapsed by about ten times as much as final demand. On the supply side, a large new mine in Australia and significant expansion of an existing one in Botswana threatened to double the production of natural diamonds within five years. De Beers was forced, as a result, to reconsider the CSO’s traditional strategy of mopping up rough diamonds from suppliers, propping up their prices to buyers, and, by implication, stockpiling them during downturns.

Continued commitment to the traditional strategy would require the CSO to stockpile between $1 billion and $2 billion worth of diamonds while the recession ran its course and then to try to draw the stockpile down over a five- to ten-year term. It might seem unwise to tie up the bulk of the company’s net worth in diamond inventories, which afford no interest, at a time when interest rates were high and inventory reduction was starting to become a craze. But De Beers did invest in the billion-dollar-plus unsure thing. Ten years later, it still controls the market for diamonds, although the current recession is once again raising questions about its future.

De Beers decided to invest in stockpiling in the early 1980s because it understood that that investment was absolutely critical to long-run sustainability. Gemquality diamonds, whether purchased for adornment or investment, have no intrinsic value. Purchasers are nevertheless willing to pay high prices for them that bear little relation to their cost because they perceive that such diamonds are and will remain scarce. De Beers has cultivated that perception over several decades by advertising heavily (“A Diamond Is Forever”) and otherwise developing demand; by building up a downstream infrastructure capable of handling rapidly expanding supply; and, perhaps most remarkably, by publicizing and persisting with a pledge never to cut the list prices charged by the CSO. Allowing independent producers to flood the market — the only real alternative to stock-piling output at the CSO — would have shattered the perception that diamonds are safe stores of value and probably destroyed the diamond cartel. De Beers therefore had to weigh the risk of investing in a stockpile it might not be able to work off against the risk that not investing would wipe out most of the scarcity value of its own (and affiliated) diamond mines — scarcity value that might be sustainable with investment. It came to the conclusion that the risk of not investing outweighed the risk of investing.

Of course, not all companies can dominate their markets to the extent that De Beers does. But the importance of investment’s effect on sustainability is, if anything, even greater when a company faces capable competitors than when it doesn’t. Capable competition, as in the semiconductor industry, places a company on a treadmill where it may have to run very hard (invest) just to maintain its relative position. To assume, as seems common, that the alternative to investment is perpetuation of the competitive status quo is to fail to grasp this point.

Conclusion

Following the recommendations listed above will help you reduce the probability of error but probably wont rule it out. It is important, therefore, to maintain a margin for error. More specifically, a balance should be maintained between errors of omission and of commission. Ideally, concern about financial risk shouldn’t force you to incur a serious risk of competitive collapse by accepting too few investment opportunities. Nor should concern about competitive risk force you to incur a serious risk of financial bankruptcy by accepting too many investment opportunities.

Having said this, I should acknowledge that companies’ abilities to live up to these risk-management ideals depend in important ways on their initial positions. Reconsider that Intel spent $800 million to $1 billion on plant and equipment in 1991. The company has announced its intention to sustain this level of expenditure for several years. None of Intel’s competitors appears to be investing nearly as aggressively. Some of this difference may have to do with differences in foresight, but much of it is surely due to Intel’s sustained competitive advantage in microprocessors, which allows it more room to maneuver than many of its competitors.

More generally, investing to create and sustain a competitive advantage is still the single best recipe for dealing with downturns and other challenges if an advantage can be achieved cost effectively. The framework for investment analysis that underlies this article will help prudent managers with the hard part of the recipe: judging whether investment is cost-effective in a sense that encompasses competitive and financial considerations rather than just the one or the other. ♦

References

1. R.H. Hayes and D.A. Garvin, “Managing as if Tomorrow Mattered,” Harvard Business Review, May–June 1982, pp. 71–79.

2. G. Donaldson and J.W. Lorsch, Decision Making at the Top (New York: Basic Books, 1983).

3. For additional specifics on how the analysis ought to be conducted, see:

P. Ghemawat, Commitment: The Dynamic of Strategy (New York: Free Press, 1991), especially chapters 4 and 5.

4. W.M. Cohen and R.A. Levin, “Empirical Studies of Innovation and Market Structure,” in Handbook of Industrial Organization, eds. R. Schmalensee and R.D. Willig (Amsterdam: North-Holland, 1989).

5. W. Skinner, “Big Hat, No Cattle: Managing Human Resources,” Harvard Business Review, September–October 1981, pp. 106–114.

6. See, for example, G. Donaldson, “Voluntary Restructuring: The Case of General Mills,” Journal of Financial Economics ’27 (1990): 117–141.

7. P. Ghemawat, “Sustainable Advantage,” Harvard Business Review, September–October 1986, pp. 53–58.