When Do Private Labels Succeed?

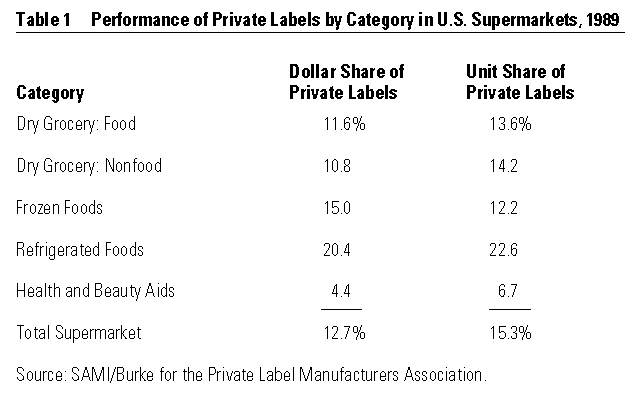

In 1989, private labels or store brands accounted for 65 percent of sales of frozen green and wax beans and for 25 percent of sales of liquid bleach but for only 1.1 percent of sales of personal deodorants. As shown in Table 1, private label market share (in terms of both dollar sales and units sold) varies significantly across supermarket merchandise groups. What factors account for this variation? Private labels traditionally have been merchandised on the basis of price. The conventional wisdom has been that store brands should offer acceptable quality relative to national brands, but they should emphasize price. Recently, however, some retailers have been emphasizing quality over price; they have received a great deal of attention in the trade press and caused alarm among national brand manufacturers. For example, A&P is aggressively introducing a high-end line of private label products under the Master Choice label, reportedly under the influence of its German parent, Tengelmann.1 In this paper, we propose and test a framework to explain variation across categories in private label dollar share. We try to isolate the determinants of success and examine the roles of relative price and quality. Such understanding appears particularly timely in light of recent highly publicized price rollbacks by national brands such as Marlboro and Pampers. These moves are apparently responses to the threat manufacturers perceive from lower price alternatives, including private labels. This research attempts to understand the nature of that threat.

{kind=link}

Private labels represent a sizable fraction of general merchandise retailing.2 Our focus is on store brands in the food retailing industry, where they accounted for 13 percent of U.S. supermarket sales in the year ending 30 June 1991.3 In that period, sales in all U.S. grocery stores amounted to $368.5 billion, implying private label sales of $48 billion. Private labels have a greater share of unit sales because they are priced 21 percent below the national brands on average. When we refer to “share” in this paper, we mean dollar share unless otherwise noted.

Private labels can be exclusive retailer programs (such as the Dominick’s brand at Dominick’s Finer Foods or A&P’s Ann Page) or they can be developed by a third party (such as Topco or Loblaw). The category also includes generic products with black-and-white labels.

References

1. E. Shapiro, “Grocers’ Fancy Brands on the Rise,” New York Times, 14 January 1992, C1, 5.

2. B.P. Pashigian and B. Bowen, “The Rising Cost of Time of Females, the Growth of National Brands, and the Supply of Retail Services,” Working Paper No. 70 (Chicago, Illinois: Center for the Study of the Economy and the State, University of Chicago Graduate School of Business, 1991).

3. Shapiro (1992).

4. Until recently, SAMI was a major supplier of audit data collected by monitoring warehouse withdrawals in most major U.S. markets. SAMI’s product became less valuable as Nielsen and Information Resources, Inc. began offering more timely and accurate point-of-sale electronic data. See:

“The Rebirth of Private Label,” Advertising Supplement, Progressive Grocer, January 1990, pp. 75–82.

5. “National Brands, Private Labels, and How They Compete,” Progressive Grocer, October 1976, pp. 47–56; and

“Brand Power 1982,” Progressive Grocer, October 1982, pp. 49–104.

6. L.W. Stern and A.I. El-Ansary, Marketing Channels, 4th ed., (Englewood Cliffs, New Jersey: Prentice-Hall, 1992), pp. 67–73.

7. P.B. Fitzell, Private Labels: Store Brands and Generic Products (Westport, Connecticut: Avi Publishing Company, 1982).

8. The regression results, with t-statistics in parentheses, were (see here) where PLMS = private label market share and I = disposable income. The R2 for the regression is .57 and the Durbin-Watson statistic is 1.89, indicating the absence of autocorrelation.

{kind=link}

9. “They Have Names Too,” The Economist, 24 December 1988, pp. 98–99.

10. P.K. Kotler, Marketing Management: Analysis, Planning, Implementation, and Control, 7th ed. (Englewood Cliffs, New Jersey: Prentice-Hall, 1991), pp. 581–582.

11. B. Klein and K. Leffler, “The Role of Market Forces in Assuring Contractual Performance,” Journal of Political Economy 94 (1981): 796–821;

P. Milgrom and J. Roberts, “Price and Advertising Signals of New Product Quality,” Journal of Political Economy 94 (1986): 615–641; and

B. Wernerfelt, “Umbrella Branding as a Signal of New Product Quality: An Example of Signalling by Posting a Bond,” Rand Journal of Economics 19 (1988): 458–466.

12. C.A. Montgomery and B. Wernerfelt, “Risk Reduction and Umbrella Branding,” Journal of Business 65 (1992): 31–50.

13. For more on PIMS, see:

R.D. Buzzell and B.T. Gale, The PIMS Principles: Linking Strategy to Performance (New York: Free Press, 1987);

M.E. Porter, Competitive Strategy (New York: Free Press, 1980); and

R. Jacobson and D.A. Aaker, “The Strategic Role of Product Quality,” Journal of Marketing 51 (1987): 31–14

14. “Private Label: Poised for Performance,” Advertising Supplement, Progressive Grocer, April 1991, pp. 85–98.

15. Ibid.

16. Montgomery and Wernerfelt (1992).

17. J.S. Raju, R. Sethuraman, and S. Dhar, “Cross-Category Differences in Store Brand Market Share” (Philadelphia: University of Pennsylvania, Wharton School of Business, Working Paper, 1992).

18. R. Sethuraman, “The Effect of Marketplace Factors on Private Label Penetration in Grocery Products” (Cambridge, Massachusetts: Marketing Science Institute, Report No. 92–128, 1992).

19. “Private Label’s Shortcomings,” Food and Beverage Marketing, 25 December 1989.

20. “Repositioning Private Label — It’s Part of a Broad New Strategy at Star,” Progressive Grocer, February 1977, pp. 107–108.

21. K.J. Lancaster, Consumer Demand: A New Approach (New York: Columbia University Press, 1979); and

R. Schmalensee, “Entry Deterrence in the Ready-to-Eat Breakfast Cereals Industry,” Bell Journal of Economics 9 (1978): 305–327.

22. P.W. Farris and M.S. Albion, “The Impact of Advertising on the Price of Consumer Products,” Journal of Marketing 44 (1980): 17–35.

23. Klein and Leffler (1981);

Milgrom and Roberts (1986); and

P. Nelson, “Advertising as Information,” Journal of Political Economy 82 (July-August 1974), pp. 729–754.

24. R. Lal, “Manufacturer Trade Deals and Retail Price Promotions,” Journal of Marketing Research 27 (1990): 428–444.

25. “41st Annual Consumer Expenditures Study,” Supermarket Business 43 (1988): 63–218.

26. The correlations were as follows: manufacturers with brands r = .77, manufacturers with UPCs r = .60, and brands with UPCs r = .64.

27. BAR/LNA Multi-Media Service (New York: Leading National Advertisers, 1988).

28. Thomas Food Industry Register (New York: Thomas Publishing Company, 1990).

29. The dependent variable in all the analyses was a logit transformation of each product category i’s private label market share (PLMSi),

where

logit(PLMSi) = ln{(PLMSi)/(100 - PLMSi)}.

A logit transformation is standard when the dependent variable is bounded as in the case of the market share variable (0 percent to 100 percent). The logit transformation also corrects for heteroskedasticity.

30. The food category serves as the base group with an implied coefficient of zero.

31. It is possible that an observed positive relation between margin and private label share is driven by the systematically higher margins offered by private labels. To assess the seriousness of this problem, we obtained private label margins from a large supermarket chain in Chicago for a subset of 138 of the categories and then backed them out of the aggregate category numbers. The estimated coefficient for the margin variable is actually slightly larger (.14 versus .11) when private labels are not included, suggesting that endogeneity is not a serious problem in this case.

32. The correlation between the number of manufacturers and the share of the private label is strongly negative (–.61) compared to the same correlations with shares of national brands: the top national brand (–.21), the second national brand (–.03), the third national brand (+.06), and the fourth national brand (+.17). Market share data for the top four brands in each category comes from:

Product Summary Report (New York: Mediamark Research, 1988).

33. The overall fit of this model decreases very little when the product class terms are dropped (R2 drops from .72 to .71). The decrease is not significant using the Chow models comparison test (F(3,166) = 2.29, p>.05).

34. We randomly selected two-thirds of the categories, estimated Model 3, and then used the model to predict the shares of the remaining categories in the hold-out sample. We did this procedure ten times to ensure stable results. The estimates are remarkably consistent. Also the overall fit in the hold-out samples is close to that obtained on the complete data set (.69 versus .71).

35. M.J. McCarthy, “What’s in a Name? Increasingly, Little, Research Suggests,” Wall Street Journal, 12 October 1990, p. B1; and

M.J. McCarthy, “Soft-Drink Giants Sit Up and Take Notice As Sales of Store Brands Show More Fizz,” Wall Street Journal, 6 March 1992, pp. B1–3.

Comment (1)

marc normandeau