Reassessing the Japanese Distribution System

Critics describe the Japanese distribution system in such unflattering terms as mysterious, archaic, outmoded, old-fashioned, inefficient, and one of the most complicated jigsaw puzzles ever contrived.1 Industrialists and trade negotiators argue that the complex channels represent a major nontariff barrier to entry in Japan and are a key contributor to the U.S. trade deficit.2 Distribution, therefore, remains a key issue in the continuing trade negotiations between the two countries.

But do these claims bear up under close scrutiny? Are they valid in the 1990s? Recently, we have seen some fundamental shifts in the Japanese economy, Japanese management, and consumer life-styles since the collapse of the “bubble economy.” Recent socioeconomic trends in Japan have filtered through its distribution system, resulting in a number of changes.3

In this paper, we examine the unique features of the Japanese distribution system to highlight some of its merits and demerits. Second, we provide an overview of various drivers that are gradually altering the channels for many consumer products and identify five important trends in Japanese distribution.

Features of Japan’s Distribution System

There are four major features of Japanese distribution systems for consumer products: (1) the size and number of retailers, (2) the length of distribution channels, (3) manufacturers’ domination of many channels, and (4) symbiotic relationships.4 We review each to demonstrate that the claimed differences between Japanese and Western systems may not be as significant as they first appear. Furthermore, rather than being sources of inefficiency, these features may indeed reflect some important strengths.

Size and Number of Retailers

The comparatively high number of retailers in the Japanese system has frequently been used as evidence of inefficiency. However, in many cases, the only country used for comparison was the United States. Thus, for example, using figures for 1982, Goodnow and Kosenko showed that Japan had 1,721,000 retail outlets, or one for every 69 people, compared with the United States, which had 1,923,000 outlets, or one for every 126 people.5 This simple comparison suggests that Japan has more retailers than necessary. By extending and updating the analysis, however, we can see that Japan currently has a greater number of retail outlets per 1,000 people than other industrialized countries like Britain, France, and Germany, as well as the United States. In Europe, the number of retail outlets per 1,000 people is 13.8 in Ireland, 15.2 in Italy, and 23.2 in Spain. These figures indicate that Japan is by no means the only industrialized country with a relatively low level of retail concentration.

The overall figures belie strong sectoral similarities. Japan has a larger proportion of small food retail outlets compared with countries like the United States, but, in the case of nonfood stores, it compares quite favorably. For example, while 56 percent of Japan’s nonfood stores employed two people or fewer in 1985, some 50.6 percent of U.S. nonfood stores were the same size.6 Furthermore, the high proportion of small food outlets can be explained to some degree by social and economic circumstances in Japan. Food retailing establishments in Japan were traditionally not located in spacious suburban areas, as in Western countries, but near railway stations in cities and large towns. High real estate prices meant that these outlets were generally small and cramped. Independent “mom and pop” stores were very popular, easily accessible to the customer, with a high level of service and an easy return policy for defective products.

Shopping habits are quite different from those in Europe and the United States. The Japanese emphasize the freshness and quality of produce; for example, Lawson, a leading convenience store, has food delivered three times daily — at midnight, before noon, and in the evening —and discards day-old food. The space constraints in Japanese households mean that shoppers visit stores frequently for small quantities rather than buying in bulk. A food shopper in the United States is likely to visit a retail store approximately 1.8 times per week; in Japan, 5 times.7 Despite apparent numerical inefficiency, Japan’s food distribution systems are very effective in service quality and responsiveness.

Length of Distribution Channels

Japanese distribution channels are generally longer and involve more participants than those in the West. A Ministry of International Trade and Industry (MITI) survey in 1989 found that, in the 1980s, Japan had on average 2.21 wholesale steps between producer and retailer. This compares with 1.0 in the United States, .73 in France, and .90 in the former West Germany. Japanese wholesalers sold their goods twice as frequently to other wholesalers than their counterparts overseas did, and each player’s addition of margins contributed to the high consumer prices in Japan.8

The wholesalers’ role is rooted in the ecological development of the distribution system. We can trace the source of their strength from the Tokugawa era in the seventeenth century, when commercial activities began to flourish as the Tokugawa regime achieved a degree of political stability and integration previously unknown. However, the production sector consisted of numerous small-scale establishments with limited lines, output, financial strength, and, most important, marketing capability. A large number of small retailers had limited financial capacity, knowledge of the market, and management know-how. The merchant class sought security in a hostile environment by developing a highly monopolistic system with complex trade practices and institutional arrangements, the relics of which remain today.9

The just-in-time or kanban system is another feature of Japanese distribution; it has been essential because of the space constraints in Japanese retail stores. Frequent, on-time delivery and minimum inventories have become a source of competitive advantage for small retailers. Average weekly deliveries to retail outlets increased sharply, providing business opportunities for secondary and tertiary wholesalers. The escalating cost of real estate during the boom years meant that established wholesalers obtained warehouse space at low cost, while new retailers paid high prices for space, including rent, administrative charges, security deposits, and even a construction contribution fund. In addition, the wholesalers were an invaluable source of market information for manufacturers, which meant they held the balance of power in many product channels.

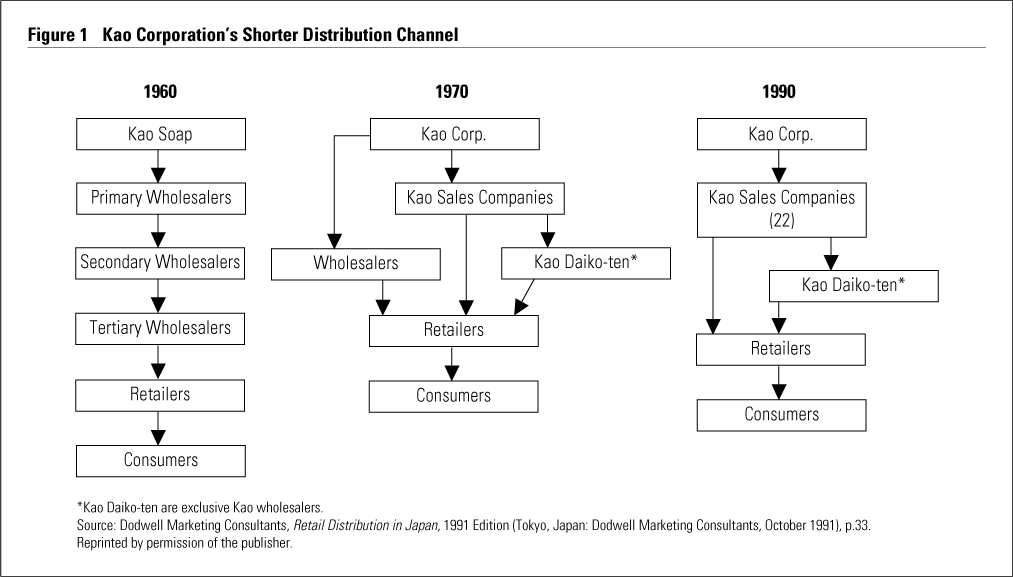

However, once again, the overall figures belie important sectoral differences. While some products such as fresh food still pass through long, complex channels, many newer products such as electronic goods take a much shorter route. Furthermore, many channels are getting progressively shorter (see Figure 1 for an example).

{kind=link}

Manufacturer Domination

In a variety of industries, the dominant player in the distribution channel is the manufacturer. In the past, manufacturers enjoyed higher prestige than merchants, and their position strengthened during Japan’s so-called “economic miracle.”10

Manufacturers use a variety of ingenious techniques to ensure channel control, such as company-affiliated stores, returns policies and financing, and recommended resale prices and rebates. Company-affiliated stores prevailed after World War II when, in many cases, there was no adequate distribution alternative. These exclusive distributors are found mostly in consumer electronics, household appliances, and pharmaceuticals. In the late 1950s, when the home appliance market was booming, Matsushita had 30,000 affiliated stores throughout Japan, while Toshiba had 13,000, and Hitachi, 11,000. Manufacturers sometimes have financial stakes in their affiliates or have helped them develop by offering sales commissions, advertising help, and occasionally staff. The manufacturers can dictate product range, pricing, and other marketing issues to affiliates. Exclusive dealerships are now also prevalent in motorcycle and automobile distribution, although there are some cracks in this system. Recently, Nissan affiliates began handling Ford vehicles, and Toyota announced that it may market Ford cars.

Japanese manufacturers have very liberal product-return policies that extend not only to damaged goods but also to products that are not selling well. Known as hen-pin, the system allows retailers to return goods through wholesalers to manufacturers, a practice particularly popular in apparel, books, and pharmaceuticals. Small retailers find it advantageous because, despite their limited display and storage space, they can still offer a wide product range without the risk of large, unsold stocks. For them, it is an important competitive weapon, given the well-documented Japanese consumer’s penchant for new, different products. However, it has proved to be a real stumbling block for foreign firms that are not accustomed to handling high levels of returns and cannot replenish stocks frequently. Similarly, the common use of tegata, or promissory notes, also presents problems for foreign companies. Tegata are a form of financing that offer buyers credit, for up to 120 days, which enables the buyer to avoid cash flow problems if products sell slowly. The notes reflect the high level of trust, built during years of business, between channel members.

Particularly in the case of company-affiliated stores, manufacturers have been able to press for maintaining recommended resale prices. These prices, or tatane, incorporate given profit margins for each intermediary, which for many in Japanese management, lend stability to the system. Tatane are also tied to market share leadership, the Japanese manufacturers’ preferred strategy. Research in the area of price setting shows that market share leaders set prices using the cost-plus or market-based approaches, while smaller companies use competitive pricing methods.11

A controversial technique that manufacturers use to control the distribution channel is the rebate system. Rebates encourage wholesalers and retailers to attain particular sales targets, pay on time, follow manufacturer’s pricing policies, adopt marketing techniques, or simply compensate for loyalty to the manufacturer. However, manufacturers do not base rebates on objective criteria, as Western companies do, but negotiate privately with each intermediary, reflecting the personal relationships among channel members and contributing to the manufacturers’ power. (Such practices in the United States would be an obvious violation of the Robinson-Patman Act.) More recently, manufacturers have used rebates to compensate channel members for losses sustained from reduced margins, which further increases the channel members’ dependence on the manufacturer.

Manufacturers’ control of the channel is not unique to Japan. For example, companies like Benetton have developed a tightly controlled, global system of franchise retail outlets that carry only Benetton products and use standardized marketing strategies.

Symbiotic Relationships

In Japanese business, there is a high level of horizontal interaction between companies in the gurupu system and vertical interaction in the keiretsu system. Company-affiliated distribution networks, known as ryutsu keiretsuka, bear all the hallmarks of a vertical system. Financial ties are not unusual among members, whether in the form of full ownership of retail outlets or cross-shareholding among manufacturers, wholesalers, and retailers. Interlocking directorates and the temporary sharing of management personnel are common. In some cases, these systems provide “helpers,” particularly in the apparel, cosmetics, and electrical retail sectors, who work in the store (often wearing store uniforms) but are on the manufacturer’s or wholesaler’s payroll.

Close personal relationships develop among channel members. Their long-term dealings with well-known partners lead to stability and consistency, which characterizes much of Japanese management. Relationships are nurtured by frequent visits, gifts, and support in difficult times; the maintenance of the relationship is generally considered more important than sales levels. This closeness represents a particularly difficult barrier for a new or foreign supplier to overcome.12 But several advantages accrue from this kind of working arrangement. The closeness of the players has resulted in a rapid transfer of innovations, which benefits all “family” members. Regular market feedback from channel partners greatly facilitates new product introductions. But, perhaps most important, these relationships represent major savings in the transaction costs that characterize many other channel systems. Dealing with well-known channel members reduces the cost of information gathering, monitoring, and negotiation. These are similar to the advantages Japanese companies have achieved on the supply side of the equation, where they have also developed strong relationships with subsuppliers.13

Forces of Change

It is important to recognize that the Japanese distribution system is undergoing a fundamental transition. In 1982, the number of retailers declined for the first time and a variety of new forces that emerged from the collapse of the “bubble economy” in April 1991 have accelerated change. Deregulation, new manufacturing imperatives, changing consumer behavior patterns, and economic drivers are all interacting to significantly reshape Japanese distribution.

Regulatory Forces

Japanese business practice is generally characterized by its high level of regulations, many built up over years of deals involving the “iron triangle” of big business, bureaucrats, and politicians. The main beneficiaries are established firms; the main losers are new competitors, both domestic and foreign.

In the distribution sector, there is a startling array of regulations to govern all aspects of business. For example, paint retailers cannot expand their business because paint products, defined as inflammable, can be stocked only in small quantities. Retailers seeking to expand their product range face even greater difficulties. A variety of products, even basic stocks such as meat, fish, snacks, ice cream, milk, and frozen foods, require separate trading licenses. Opening a supermarket can require up to forty licenses to comply with nineteen different laws. Daiei Inc. recently estimated that the cost of complying with all the necessary regulations to open a new store was as high as ¥160 million or about U.S. $1.12 million.14 However, some recent regulatory changes are beginning to alter the picture.

· The Large-Scale Retail Store Law

(LSRSL). While this law, enacted in 1973, says that restrictions of large stores were necessary to protect consumers’ rights, its purpose clearly has been the protection of small to medium-sized retailers by regulating large stores’ business hours, holidays, and sales space. The law identifies two categories of large stores: (1) stores over 16,145 square feet (32,292 in Tokyo and eleven other cities with populations of over one million people); and (2) stores over 5,382 square feet (16,145 in Tokyo and other designated cities). Before a retailer can open a store in the first category, it had to submit a business plan to its local Sho-Cho-Kyo (Council for Coordinating Commercial Activities). Since the local chambers of commerce operated the councils, decisions sometimes took up to eight years and frequently favored small retailers. Applicants often had to contend with restrictions on store hours and sales space.

An important amendment to the law, approved in May 1991, was enforced in January 1992. A Large-Scale Retail Store Council has replaced the Sho-Cho-Kyo. It must make decisions on new store applications within twelve months. The sales space for the first category of stores has been extended to 32,292 square feet and over, or 64,583 square feet in designated cities. Approval of store hours is necessary only for stores wishing to remain open after 7 p.m. The minimum number of store holidays has been reduced from forty-eight to forty-four. In addition, a special law concerning floor space for imported products has been added; any store or store expansion devoted exclusively to the sale of imported goods is exempt from the coordination procedures of the law, such as having to gain approval from other retailers in the area.15 The latest amendments to the law, effective from May 1994, are that any store under 10,764 square feet is now allowed to operate outside the restrictions of the law and that the mandatory closing time for large stores has been extended to 8 p.m.

· The Antimonopoly Law.

As noted earlier, manufacturers have tried to lock retailers into a system of recommended resale prices, often facilitated by providing “helpers.” In cosmetics distribution in particular, this practice is widespread; prices are exactly the same in a department store, a neighborhood pharmacy, or in many of the emerging discount stores.

However, a landmark ruling against Shiseido, one of Japan’s leading cosmetics companies, will change an industry once considered the last bastion against the discount stores’ onslaught. Under Japan’s Antimonopoly Law, enacted in 1947, producers are barred from dictating retail prices or engaging in restrictive marketing practices, although a resale price maintenance system, introduced in 1953, exempts some products. Shiseido has almost 30 percent of the Japanese market and, along with Kanebo Ltd. and Kao Corp., accounts for over half of all cosmetics sales in Japan. In May 1990, its sales arm, Shiseido-Tokyohanbai, suspended shipments to a Tokyo-based retailer, Fujikihonten, for failing to follow Shiseido’s marketing plan, which prohibited retailers from using methods other than “face-to-face sales” by Shiseido employees. A ruling in Tokyo District Court in September 1993 considered this practice a violation of the Antimonopoly Law; Shiseido was ordered to deliver approximately ¥500 million in products that had been on order for three years.

In another conflict between the administration and Shiseido, the Fair Trade Commission (FTC) raided the offices of two Shiseido sales companies in July 1993, after a discount company, Kawachiya Ltd., filed a complaint that Shiseido, Kanebo Ltd., and Kao Corp. were trying to prevent its sale of products at 25 percent to 30 percent below recommended retail prices. In September 1993, Kawachiya Ltd. was forced to push its prices up again after manufacturers’ rebates shrank, so clearly the battle is not over yet. An appeals court has upheld Shiseido’s decision to suspend shipments to Fujikihonten.

· The Liquor Tax Law.

Each product sector invariably has a range of regulations regarding distribution. The Liquor Tax Law illustrates many of the regulatory anomalies. The law, enacted in 1938, governs liquor-licensing regulations and accruing tax revenues. The National Tax Administration Agency operates it under the auspices of the powerful Ministry of Finance. Over the years, liquor licenses became increasingly hard to obtain as existing liquor stores sought to prevent erosion of their business by new retailers. Although department stores were able to obtain licenses based on their wide range of merchandise, supermarkets were not. Under claims that the system was discriminatory, the law was amended in 1988; as a result, supermarkets with at least 107,639 square feet of floor space are unconditionally able to obtain a license. The required distance of a new store from an existing store fell from 110 yards to 55 yards, and mail-order companies are now allowed to market alcohol, with some restrictions.

This law is once again a center of controversy, with traditional liquor stores currently under pressure from discount stores. The Tax Administration Agency has imposed several adjustments to the granting of licenses, including (1) if a liquor store goes out of business, it cannot sell its liquor license to new management and (2) when new management has acquired the liquor rights, the new owners are not allowed to increase the store area to more than 3,229 square feet. While this may be a deliberate ploy to prevent the growth of large discount operations, the authorities say the restrictions are aimed at preventing alcohol sales to minors, despite the fact that alcohol is widely available through vending machines.

· The Fair Trade Commission.

Japan’s watchdog of regulatory violation, the FTC (traditionally known as the toothless paper tiger or the never-barking watchdog) has achieved a much higher profile. By the end of its fiscal year in March 1993, the FTC had taken legal measures in thirty-four cases, compared to seven in 1990, reduced the number of cartels exempted from the Antimonopoly Act from 261 in 1989 to 160, and planned to halve the fifty items still exempt from the resale price maintenance system by December 1994.16 Its plans to ensure that importers pass the benefits of the strong yen on to consumers represent a boost for foreign companies. However, the FTC has been notably unsuccessful when facing industries like construction that have strong political and bureaucratic connections. Japan’s construction industry is widely known for its dango or bid-rigging system. The FTC’s attempts to raise fines for such clear violations of the Antimonopoly Law have been, it claims, persistently blocked by members of Japan’s Liberal Democratic Party (LDP), known for its close connections to the construction sector.

Manufacturing Forces

In the three years since the bubble economy burst, growth in consumer expenditure has slowed, domestic competition has increased, and the strengthening yen has slowed the export trade. The business precepts that served Japanese companies so well during the boom years, such as strong relationships, lifetime employment, consensus decision making, and promotion by seniority are increasingly under threat. Unemployment levels reached a new high of 2.9 percent in January 1994, although many experts argue that the real rate is closer to 6 percent, and recruitment of new graduates has fallen drastically. There are indications that the recession is likely to continue.

Throughout years of growth, most Japanese companies followed a policy of capacity expansion in the pursuit of market share leadership. In the 1990s, this has, in many cases, led to overproduction and surplus stock levels. Intense competition in the marketplace has meant that sales of surplus stock are increasingly going to discounters, either directly from manufacturers or from wholesalers.

Product-line breadth was another strategy Japanese manufacturing companies pursued during the 1980s. Continuous innovation and modifications raised barriers to entry and displayed a product commitment essential to intermediaries. For example, during the late 1980s, of the estimated 700 new soft drinks launched each year, 90 percent disappeared within twelve months. The broad product line also met voracious consumer demand for new consumable and durable products. However, manufacturers are increasingly rationalizing product lines and reducing variety in consumer products in response to retailers’ demands for strong selling products. Ajinomoto, Japan’s top food processor, has reduced its launches of frozen food brands from thirty-one annually in the late 1980s to nineteen in 1993. Matsushita, which cut its 5,000 audio products to 1,000, has reduced consumer choice, intermediaries’ sales levels, and, in many cases, the need for secondary and tertiary wholesalers.17

Consumer Forces

In autumn 1993, the significant contraction in consumer spending led to a series of government packages to stimulate consumer demand and pull Japan out of its recession. Several factors combined to reduce personal consumption, including distaste for the conspicuous consumption of the late 1980s, fears about job security among salaried workers, lack of new products, and the declining birth rate.18

Japanese consumers have altered their shopping habits to become much more cost conscious, a major change from the late 1980s, when they purchased mainly high-priced, brand-name products. They are increasingly asserting their independence, being guided less by manufacturers and retailers. In the past, a consumer who bought inexpensive products lost face, whereas now a consumer who buys high-quality products at low prices is admired, a trend emphasized by discount stores’ significant gains in the past two years.

Workdays have gotten shorter, so many fathers can now spend increasing time at home. The result is a sharp rise in sales of home cooking appliances and a shift in shopping patterns. Families now travel by car to shop in suburban areas rather than the traditional stores located near train stations.19

Women are the hardest hit by the current employment downturn. Part-time female workers have generally been the first laid off, followed by full-time female workers, who many managers believe will leave anyway to start families. Women seeking another career have become employees for direct marketing cosmetic companies, like the successful U.S. firms, Nu Skin, Amway, and Avon.20

Economic Forces

The current economic recession is affecting distribution in other ways as well. Real estate prices have collapsed from the dizzy, speculative heights of the late 1980s, when the value of the Imperial Palace grounds in Central Tokyo was estimated at more than the state of California. Land prices dropped by more than 60 percent between 1988 and 1989 and have increased only marginally since. Warehouse and storage space has become cheaper, with the result that many retail chains are now constructing large suburban distribution centers to reduce the need for wholesale services and enable frequent product delivery. And lower land prices have enabled suburban roadside retailers to open outlets in central city areas, a symbol of their challenge to traditional department stores.

The yen has been appreciating steadily against other currencies since the late 1980s, reaching a high of almost ¥95 against the U.S. dollar. Along with reducing the cost of foreign products, the strong yen has created gray markets in a variety of brand-name products with parallel imports, particularly common in high margin items like cosmetics. However, the regulatory agencies are creating difficulties for parallel importers. For example, imported cosmetics must carry a label with the importer’s name and the product’s contents. Jonan Denki, a discount store, removed the labels for fear that the manufacturer would pressure the parallel importers. The company was forbidden to sell its discounted cosmetics, although it defiantly left the goods on its shelves with a notice to customers that they should contact the Health and Welfare Ministry if they wanted to buy them.

Overall, imports to Japan rose by 3.2 percent in 1993, and some products, such as men’s suits, increased by 60 percent. Prices of many products like whiskey and personal computers have dropped by more than 20 percent.21 General merchandise stores (GMSs) and discount stores have led the way with strong sales.

New Trends

The regulatory, consumer, manufacturing, and economic forces have interacted to generate some fundamental changes in Japanese distribution. We can identify five main developments: an increased concentration of retailers, growth of discounters and corresponding decline of department stores, growth of nonstore retailing, increasing pressure on wholesalers, and new sources of competitive advantage.

Retail Concentration

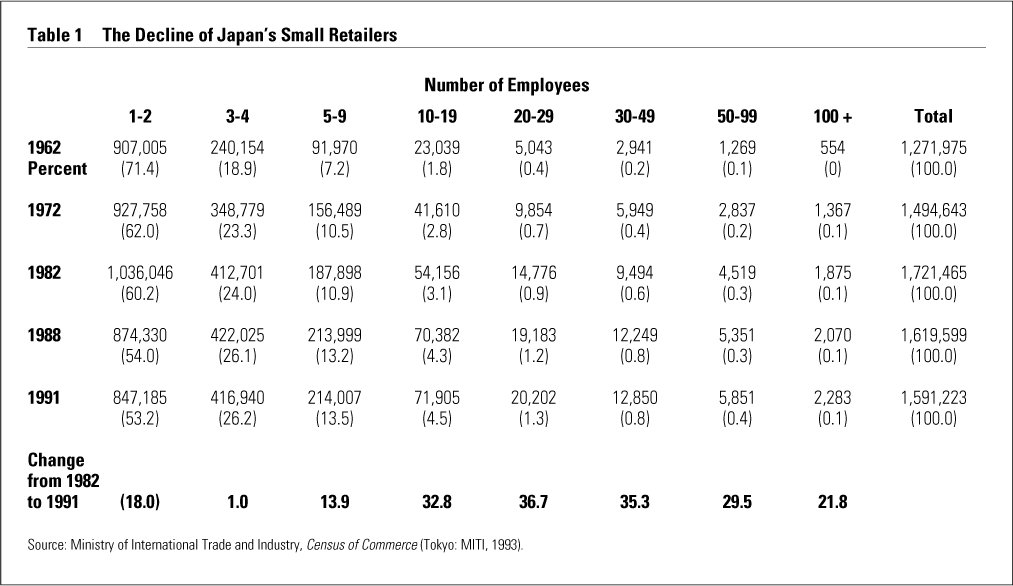

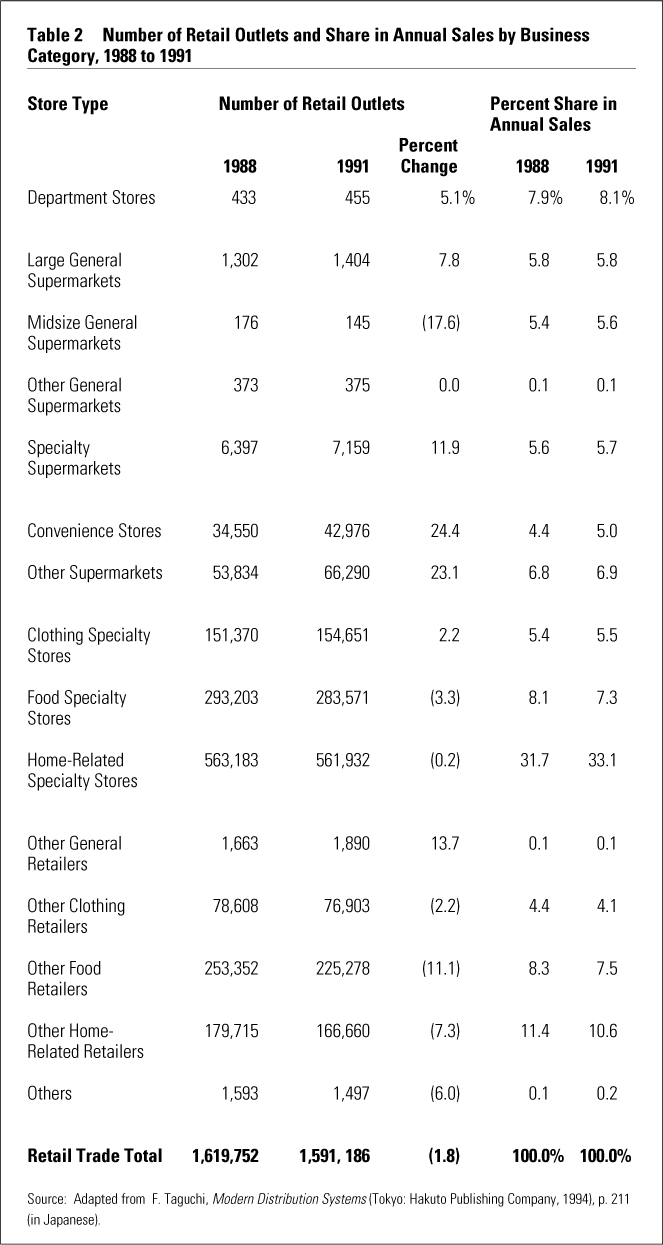

The ongoing recession, the falling real estate prices, and the amendments to the Large-Scale Retail Store Law have been key factors in the decline of the number of retail stores. In 1982, Japan had 1.7 million retail stores; by 1991, this number had fallen to 1.59 million. MITI forecasts a continued decline of 20 percent to 1.2 million units by the year 2000 (see Tables 1 and 2). In particular, medium-size general supermarkets (not part of national chains) and small stores centering on food items registered notable declines.

{kind=link}

{kind=link}

There are already several different categories of large stores in Japan, including general merchandise stores, food supermarkets, and department stores. The GMSs have been growing fastest; the top four retailers in Japan are in this category — Daiei Inc., Ito-Yokado Co. Ltd., Seiyu Ltd., and Jusco Co. Ltd. — but sales in this sector suffered in 1993 due to the recession. The top 200 retailers in Japan now account for over 25 percent of all retail sales. Large-scale suburban, leisure, and shopping centers have grown rapidly, offering consumers a wide range of entertainment and shopping with parking. Further growth of this type is forecast for the 1990s, due to changing consumer behavior patterns. The Jusco complex in Sagamihara, outside Tokyo, features swimming, karaoke, a gymnasium, and a culture center (for modern dance, flower arranging, foreign languages, etc.), as well as shopping, spread over 700,418 square feet of floor space. Japan’s largest shopping mall at Tokyo’s LaLaport even contains an indoor ski slope. And its first super-supermarket chain was completed in spring 1994, when Daiei Inc. formally took control of three affiliated, general merchandise stores, Chujitsuya Co., Uneed Daiei Co., and Dainaha Inc. This move will make Daiei Inc. the undisputed heavyweight; its sales are already 70 percent greater than its nearest rival, Ito-Yokado.

Chains of convenience stores have been even more successful, with a 10.7 percent growth rate in 1992 that outpaced all other retail formats. Seven-Eleven (Japan) Co., the foremost operator in the sector, opened some 430 new outlets between fiscal 1991 and fiscal 1992. GMSs own all major convenience store chains in Japan; Ito-Yokado recently purchased Seven-Eleven, Daiei Inc. runs Lawson, and the Saison Group, which includes Seiyu Ltd., owns Family Mart. Convenience stores can therefore pioneer technological advances and retail innovations. Convenience stores can differentiate themselves from the large stores by providing a variety of supplementary services such as parcel delivery, photo processing, photocopying and faxing, and bill settlement services. They are planning to offer travel agency services and mail-order services. Seven-Eleven recently installed an automatic teller machine at one of its outlets.

These changes reflect the shift in power from manufacturers to retailers.22 Retailers increasingly control the most vital resource, information, through their extensive use of technology. This enables them to identify which products sell best, to whom, and when, removing wholesalers’ information-gathering role and increasing their importance to manufacturers. Retailers’ increasing size means that traditional tegata financing is no longer attractive. They also perceive the potential of discounted products and bypass traditional channels to import directly. In the years ahead, large retailers will dominate the distribution channel, similar to those in Europe and the United States. We see this shift as a primary factor in modernizing Japan’s distribution system.

Growth of Discounting and Department Stores’ Decline

The strongest trend in Japanese distribution is, arguably, the growth of discounting. The success of specialty discount stores, earning themselves the label of “category killers,” has been most significant. These stores gained in the clothing and home electronics sectors and are forecast to gain in sporting goods, jewelry, used cars, pharmaceuticals, and cosmetics as well.23 Discount stores’ sales have significantly outpaced those of department stores and supermarkets. While the latter have been stagnant or falling, sales at 149 major discount stores increased an average of 8.5 percent in fiscal 1992; 79 specialty discounters reported sales increases of 10.9 percent during the year.

Aoyama Trading Co., one of Japan’s leading men’s suits retailers, illustrates the strength of specialty discounters. The company buys its products directly from the manufacturer, which enables it to offer prices about 50 percent less than its competitors. It pioneered roadside retailing, which capitalized on Japanese consumers’ exodus to the suburbs. Roadside retailers gain advantage from lower land costs, inventory, and parking space, and since sales in these stores typically occur during the weekends, companies can employ a greater number of part-time personnel. Aoyama, which has 464 stores in Japan, has the fastest growth record of any retailer in recent years. It recently formed an alliance with the U.S. retailer, J.C. Penney, to expand Aoyama’s product range with a line of casual clothing.

The large, general merchandise stores and supermarkets, in response to declining sales in 1993, are increasingly exploring discounting options. Daiei Inc. has its own “savings” label, undercutting private brands by almost 50 percent. It is experimenting with one outlet to see how far it can cut costs; Hypermart Sakaide is in a one-story building with more than 161,459 square feet of floor space and contains unprecedented features like bare floors and no heating during the winter. Customers must pay for deliveries and put a deposit on shopping carts.24 Daiei’s future plans are to convert money-losing supermarkets near railway stations into urban condominiums by using expertise from its diversification into real estate.

In contrast to the discounters’ growth, department stores are facing increased difficulty, mirroring trends in Europe and the United States. Department stores traditionally competed on the basis of a wide range of branded products sold in a luxurious atmosphere. They spare no expense in providing top-quality service, including gift wrapping, delivery, and a liberal return policy. The stores have a large number of customer service staff, “greeters,” and, in many cases, elevator operators. Department store sales registered a drop of 5.6 percent from December 1993 to January 1994, for the twenty-second consecutive month of decline. Interestingly, the biggest declines have been in the clothing and home electronics divisions, two sectors experiencing stiff competition from discounters.

Gift giving is an important aspect of Japanese life, particularly on two major occasions, chugen (mid-year) and seibo (end-year). Previously, most companies and individuals bought gifts at prestigious department stores; such gifts accounted for almost 40 percent of some outlets’ total sales. During the recession, this crucial market shrank, with sales of gift certificates alone falling by 7.5 percent from December 1993 to January 1994.

Related to the department store decline is the emergence of factory outlets, particularly in clothes retailing. These outlets have two sources of supply, brand-name products direct from the factory and unsold stocks from department and specialty stores with manufacturers’ labels removed. Previously, department stores returned unsold stocks to the wholesalers and manufacturers, which readily accepted them because they had already been factored into the selling price. Many department stores are now buying supplies outright, rather than on consignment, to take advantage of lower prices, so factory outlets are an important way to reduce unsold stock. One successful outlet is Garden Pier, in Nagoya, where 80 percent of the 50,000 clothing items comprise the previous year’s stocks from department stores and sell at 20 percent to 50 percent below the regular list price. Sales have been running at an annual rate of ¥1.5 billion, exceeding original projections of ¥1.1 billion.25

Nonstore Retailing

The pressure for space and the Japanese consumer’s desire for high levels of service increased the popularity of nonstore retailing. Combined with a very low crime rate, this means that Japan has the largest number of vending machines per capita in the world, some 5.4 million, or one machine for every twenty-three people. Vending machines are used mostly to sell hot and cold drinks, or beer and cigarettes, but they also carry other items like batteries, umbrellas, compact discs, and even underwear. The vending machine market is saturated and competition is intense, resulting in innovations to improve their convenience. A new type of machine with an elevator has been developed that lifts the product to waist level, so the consumer can buy a soft drink without bending over to take it out of the machine.26

The mail-order industry has had a long tradition in Japan, despite the commonly held view that Japanese customers resisted buying products sight unseen. Mail-order companies have differentiated themselves by offering novel products not available in department stores. Annual sales growth from 1982 to 1991 averaged 11.9 percent, compared with 4.6 percent for the retail sector overall.27 The increased number of Japanese women working outside the home has contributed to this growth, not only because they have less time for shopping but also because some 90 percent of mail-order customers are female. The most popular products sold by mail-order include ladies’ clothing, fashion accessories, jewelry, electronic equipment, and furniture and interior goods, but everything from airline tickets to gravestones is available.

However, a number of factors could hamper the continued growth of the mail-order business. As we stated earlier, women have been hardest hit by the current recession, so some of the most important segments of the business could contract. Also, postal rates jumped 24 percent from December 1993 to January 1994. Rates were already four or five times higher than those in the United States or Europe. Companies are responding by taking orders by telephone (70 percent of all orders are by postcards) and are considering postcards rather than envelopes for billing. In addition, database development has been slow, with many mailing lists still on cards rather than on computer. Some 1,500 mail-order firms compete in the industry, resulting in a number of small mailing lists; trading of mailing lists is limited.

In Japan, home delivery and selling are important distribution media. Direct selling grew at a double-digit pace during the early part of the 1980s, and sales have continued to grow at an annual rate of about 6 percent since the collapse of the “bubble.” The market in 1992 was worth U.S. $34 billion, making it the largest in the world. All of the major direct marketing cosmetics companies in the United States, such as Amway, Avon, and Nu Skin International are now operating in Japan, and, with the likely addition of Mary Kay Cosmetics, this sector will become increasingly competitive. In contrast with the fairly stagnant sales levels in the United States and Europe, Japan’s cosmetics companies are achieving annual profit increases of between 5 percent and 10 percent. The Japanese market is particularly suited to this form of distribution, due to the collective nature of the society in which clubs and groups for everything from flower arranging to tea ceremonies provide an audience for group marketing.

Pressure on Wholesalers

Wholesalers are increasingly being caught in the middle of the power struggle between manufacturers and retailers. Many of the competitive advantages they developed are eroding. Japanese distributors are renowned for technological innovations. Manufacturers can obtain accurate market information directly from retailers, reducing the data-gathering role of wholesalers, while convenience stores can become an important test market for new products. Most convenience stores and supermarkets now use point-of-sale (POS) systems. Lawson, for example, divides its customers into five age groups — primary school children and younger, middle and high school children, and adults aged eighteen to twenty-nine, thirty to fifty, and over fifty. Along with recording purchases by product and time, a Lawson cashier inputs age and gender information on each customer. Thus, while Lawson carries around 3,000 items in each store, more than half, which have proved unpopular, are phased out within one year.28 With this technology, stores can track inventory requirements, reducing the need for the cushion that wholesalers provided.

Wholesalers’ warehousing and delivery functions are also becoming less important. Manufacturers’ and retailers’ development of distribution centers has increased, due to falling land prices and the difficulty of making frequent deliveries because of increased traffic congestion. The newly formed distribution centers contain warehouses, display space, office buildings, and parking, resulting again in the replacement of wholesalers’ activities. For example, Daiei Inc. started a wholesale club, the first in Japan, in 1992.

To provide lower prices, many retailers are simply bypassing wholesalers. Large GMSs and supermarkets are increasing their share of private label brands, sourced directly from the manufacturer or from importers. Toys “R” Us is probably the best known example of a company that has insisted on buying directly from suppliers in order to keep prices down. While it has been very successful, it has met a great deal of reluctance from Japanese suppliers. Some toy makers overcame this resistance by absorbing wholesale affiliates. Aoki International, a leading roadside clothing discounter has gone even further, integrating back through the wholesale function to manufacturing. It recruited designers, pattern planners, and stylists and developed a system in which products are manufactured under contract for exclusive sale at its outlets. This enables the company to offer high-quality products at 40 percent to 50 percent below department store prices. Aoki now has the largest sales per outlet and the highest sales per employee of any of the menswear chains.29

Perhaps the biggest threat to the wholesaler is the increasing number of alliances between big manufacturers and big retailers. Daiei Inc., in particular, has formed a variety of alliances with leading manufacturers. It has a cooperative agreement with Ajinomoto, one of Japan’s biggest food processors, to develop low-priced retailer brands. It has a product development link with Kanebo Ltd., a major spinning firm, to produce a range of low-cost women’s wear. Daiei provides information on consumer demand collected through its stores, while Kanebo manufactures the garments from wool imported from its processing factory in Australia, which will be woven and dyed in Japan and finished in China. The garments retail at about 30 percent below current prices at Daiei stores. Other companies are developing technological linkages. In 1993, Jusco Co. and Kao introduced a paperless, electronic data interchange system for Kao products. The system is used to place orders, track deliveries, settle bills, and exchange product information, removing the need for the 360,000 slipsheets that annually passed between the companies.

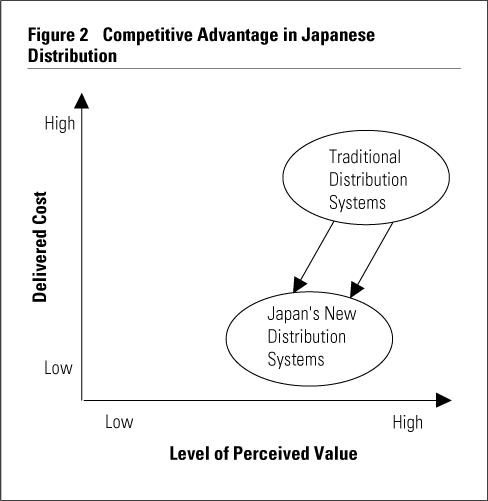

New Sources of Competitive Advantage

The parameters of competitive advantage have changed in distribution (see Figure 2). In Porter’s terms, retailers have traditionally sought a position of market differentiation on the basis of high quality and top-class service.30 Department stores competing on the basis of their wide range of quality brands, luxurious atmosphere, and additional services such as consultation and delivery most clearly illustrate this positioning. In the 1990s, successful Japanese retailers are adopting the dual position of high perceived quality and low delivered cost.31 Several new sources of competitive advantage are leveraged to achieve this position. Information technology plays a critical role. Point of sale, electronic ordering systems, and electronic data interchange systems allow the channel to operate much more efficiently by providing accurate market information, reducing stock levels, and reducing workers’ tasks. Quality foreign products are increasingly available at competitive prices due to the strength of the yen. GMSs in particular are increasing their proportion of private-label brands through overseas sourcing or links with major manufacturers.

{kind=link}

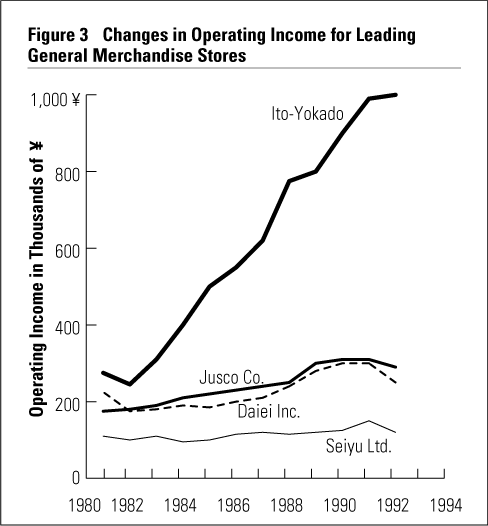

Ito-Yokado is a prime example of a distribution company that has prospered by applying information technology. In the fastest-growing industrialized economy in the past twenty years, it has grown faster than any other company to become the second largest GMS in Japan and by far the most profitable (see Figure 3). When Ito-Yokado bought out Seven-Eleven’s parent, Southland Corporation of Dallas, it implemented such POS operational efficiencies in test stores, starting in Austin, Texas. Ito-Yokado also uses TOSS (Tenpo or store operation support system) to send orders directly to the supplier or distribution center via the headquarters’ host computer. Thus Ito-Yokado can provide delivery schedules for suppliers, reducing the frequency of visits and cutting costs. Products are then delivered in specified quantities on a specified date or suppliers will be penalized by having to pay Ito-Yokado the lost opportunity costs of the undelivered products. The benefits of its technological innovations and purchasing practices are seen in major drops in inventory levels and loss rates accompanied by rising profitability.32

{kind=link}

The scope of competition has also changed. Department stores have to compete with discount stores and mail-order companies, as well as each other. General merchandise stores and discount stores are integrating back into design, manufacturing, and warehousing. Small family restaurant chains must review their pricing strategies because of competition with the successful bento (lunch box) food that leading convenience stores offer.

Conclusion

Some see the pace of change in Japan as slow. The country has ingrained business practices, integration of the private and public sectors, and societal values that ensure that traditional systems will persist, at least in the short term. But there is little doubt that Japanese distribution, so long the target of Western criticism, is undergoing fundamental change. Signals are everywhere. Matsushita is weeding out inefficient family-owned stores, realizing that it must sell instead to the big retailers. Akihabara, the once thriving electronics “bazaar” in central Tokyo has seen average sales fall by 10 percent and big-name retailers like Shinkoku KK cease operations. Sales at discount stores like Aoyama Trading continue to grow, while cheap imports become attractive options for intermediaries responding to consumer demands for lower prices. These changes are collectively driven by economic and political forces.

Major structural shifts in distribution, such as the growing power of retailers and the decline of department stores, have already occurred in the United States and Europe. Innovative competitors in Japan are increasingly monitoring developments and adopting practices that have proved successful in other industrialized countries. This does not mean that Japan is suddenly an easy market to enter. But distribution is becoming less of a barrier, and recent commentaries have focused not on the difficulties of doing business in Japan but on the successes achieved there, particularly by U.S. companies.33 Manufacturers and retailers may want to take a second look at Japan to determine if the current signals of change present an area of opportunity.

References

1. C.D. Shepard, M.M. Helms, and R.C. Tillotson, “Japanese Marketing: A Review,” Marketing Intelligence & Planning 10 (1992): 35–40;

J.D. Goodnow and R. Kosenko, “Strategies for Successful Penetration of the Japanese Market or How to Beat Japan at Its Own Game,” Journal of Consumer Marketing, Fall 1990, p. 16; and

W. Lazar, S. Murata, and H. Kosaka, “Japanese Marketing: Towards a Better Understanding,” Journal of Marketing 49 (1985): 79; and

M. Zimmerman, Dealing with the Japanese (London: Allen & Unwin, 1985), p. 134.

For an excellent review, see:

A. Goldman, “Evaluating the Performance of the Japanese Distribution System,” Journal of Retailing 68 (1992): 11–39.

2. R. Kosenko and D. Rathz, “The Japanese Channels of Distribution: Difficult But Not Insurmountable,” in G. Frazier et al., Efficiency and Effectiveness in Marketing (Chicago: American Marketing Association, 1988), pp. 233–236; and

M.R. Czinkota, “Distribution in Japan: Problems and Changes,” Columbia Journal of World Business 20 (1985): 65–71.

3. Goldman terms this approach the institutional-ecological approach, which contrasts with the positivistic-modernization approach in which the U.S.-Western distribution system is used as a yardstick and other systems are evaluated in terms of their closeness to this ideal. Using the institutional-ecological approach, Goldman concludes that Japan’s distribution systems score well on effectiveness dimensions such as service quality, flexibility, and responsiveness to new developments, and equity dimensions such as fairness, but score poorly on performance dimensions such as labor productivity and prices to consumers. See: Goldman (1992): 11–39.

4. See, for example:

M. Shimaguchi and L. Rosenberg, “Demystifying Japanese Distribution,” Columbia Journal of World Business 14 (1979): 32–41;

Czinkota (1985): 65–71; and

M.R. Czinkota and J. Woronoff, Japan’s Market: The Distribution System (New York: Praeger, 1986).

5. Goodnow and Kosenko (1990).

6. A. Goldman, “Japan’s Distribution System: Institutional Structure, Internal Political Economy and Modernization,” Journal of Retailing 67 (1991): 156.

7. M. Ariga, “Mass Retailing to the Japanese Consumer,” Japan 1992: Marketing and Advertising Yearbook (Tokyo: Dentsu Inc., 1992), p. 66.

8. Sales for the wholesale sector include that of the general trading companies, which gives something of an inflated view of the size of the sector in international terms.

9. M.Y. Yoshino, The Japanese Marketing System: Adaptations and Innovations (Cambridge, Massachusetts: MIT Press, 1971), pp. 2–6 and pp. 183–185.

10. Goldman (1991), p. 167.

11. Market-based pricing is the practice of setting prices based on an assessment of likely market reaction. Competitive pricing is the practice of setting prices in line with those of competitors. See:

Y. Tajima, ed., Manufacturer’s Price Policy and Competition (Tokyo: Fair Trade Foundation, 1988), p. 331 (in Japanese).

12. Goldman describes these relations as the “internal economy” of the channel, suggesting that the modern segment of Japanese distribution has remained traditional due to these practices, thus constraining its development. See:

Goldman (1991).

13. J.H. Dyer and W.G. Ouchi, “Japanese-Style Partnerships: Giving Companies a Competitive Edge,” Sloan Management Review, Fall 1993, pp. 51–63.

14. “Tangled Up in Regulation,” Tokyo Business Today 61 (1993): 9.

15. Dodwell Marketing Consultants, Retail Distribution in Japan (Tokyo: Dodwell Marketing Consultants, 1991), pp. 51–54.

16. “Pussycat: Japan’s Fair Trade Commission,” The Economist, 23 October 1993, pp. 75–76.

17. “Marketing in Japan: Taking Aim,” The Economist, 24 April 1993, p. 70.

18. “Recession Gives Rise to New Attitudes,” Nikkei Weekly, 13 December 1993, p. 6.

19. Ariga (1992): 64.

20. “They’ve Got Their Feet in the Door,” Business Week, 31 May 1993, p. 20.

21. “Can’t Get Enough of that Super Yen,” Business Week, 4 October 1993, p. 26–27.

22. A. Toffler, Powershift: Knowledge, Wealth and Violence at the Edge of the 21st Century (New York: Bantam Books, 1990), pp. 95–105.

23. H. Ishii, “Retailing in Japan: the Price Revolution, Category Killers and Survival Strategies,” NRI Quarterly 2 (1993): 20–33.

24. “Daiei Supermarket an Exercise in Austerity,” Nikkei Weekly, 3 January 1994, p. 10.

25. Japan External Trade Organization, “A Wealth of Opportunity: Japan’s Distribution Channels” (Tokyo: JETRO, 1993), p. 40.

26. Ariga (1992): 69.

27. “Post Haste: Japan’s Mail Order Firms Thrive While Retailers Sink,” Far Eastern Economic Review, 20 May 1993, p. 64–65.

28. “At Your Convenience: 24-Hour Services Take Root in Urban Areas,” Daily Yomuri, 9 September 1993, p. 10.

29. JETRO (1993): 35.

30. M.E. Porter, Competitive Strategy: Techniques for Analyzing Industries and Competitors (New York: Free Press, 1980), pp. 34–46.

31. The importance of adopting this dual position has been noted by some writers looking at manufacturing firms. See, for example:

W. Hall, “Survival Strategies in a Hostile Environment,” Harvard Business Review, September–October 1980, pp. 75–85; and

X. Gilbert and P. Strebel, “Developing Competitive Advantage,” in H. Mintzberg and J.B. Quinn, eds., The Strategy Process (London: Prentice-Hall, 1991), pp. 82–93.

32. “Ito-Yokado Tops List of High Growth Companies,” Nikkei Weekly, 26 April 1993, p. 9.

33. See: V.R. Alden, “Who Says You Can’t Crack Japanese Markets,” Harvard Business Review, January–February 1987, pp. 52–56;

J.G. Kaikati, “Don’t Crack the Japanese Distribution System — Just Circumvent It,” Columbia Journal of World Business 28 (1993): 34–45; and

V. Kouyoumdjian, “Foreign Firms Overcome Obstacles,” Journal of Japanese Trade & Industry 5 (1993): 18–20.