A Business Plan? Or a Journey to Plan B?

From Apple to Twitter, some of the most successful businesses are not what their inventors originally envisioned.

Courtesy of Apple Inc.

In March 2006, Biz Stone, Evan Williams and Jack Dorsey were working on a new venture called Odeo, a podcasting service. Odeo was in something of a creative slump, and Dorsey wondered if a short messaging service that would enable everyone in the company to communicate with others in the group might be of some help.

Their solution, which the world now knows as Twitter Inc., was to build a simple Web application that would let the team stay in touch by sending short 140-character messages to the rest of the group. It wasn’t long before they realized that the new application held considerably more promise than the original podcasting idea on which they had been working.

The rest of the story is history. Twitter reached its tipping point at the South by Southwest festival in 2007, where the number of tweets per day jumped to 60,000 and it won the festival’s Web Award. Whether or not Twitter will develop a viable business model remains in question, but the Twitter story is a powerful reminder that an entrepreneur’s main job is not to flawlessly execute the business idea so lovingly articulated in his or her business plan. It’s to embark on a learning journey that may, on occasion, reach the destination that the initial plan had in mind. More commonly, though, for open-minded entrepreneurs and innovators in large companies, the surprises that arise on this journey lead to a very different destination, which we call Plan B.

So, What’s the Problem?

Nearly every aspiring entrepreneur or innovator has a business plan, and virtually all of these individuals believe that their business plan — what we call Plan A — will work. They can probably even imagine how they’ll look on the cover of Fortune or Inc. And they are usually wrong. But what separates the ultimate successes from the rest is what they do when their first plan sputters. Do they lick their wounds, get back on their feet and morph their new insights into great businesses, or do they stick to their original plan? If the founders of Google, Starbucks or PayPal had stuck to their original business plans, we’d likely never have heard of them. Instead, they made radical changes to their initial models, became household names and delivered huge returns for themselves and their investors. How did they get from their Plan A to a business model that worked? Why did they succeed when most new ventures crash and burn?

First, an uncomfortable fact: The typical startup process, whether in nascent entrepreneurial ventures or in the innovation units of established businesses, is largely driven by poorly conceived business plans based on untested assumptions. This process is seriously flawed. Most new ventures, even those with venture capital or corporate backing, share one common characteristic: They fail. There is a better way to launch new ideas — without wasting years of time and loads of investors’ money. This better way is about discovering a business model that really works: a Plan B, like those of Google Inc. and Starbucks Corp., which grows out of the original idea, builds on it and once it’s in place, helps the business grow rapidly and prosper.

Most of the time, breaking through to a better business model takes time. And it takes errors, too, errors from which you learn. For Max Levchin, who wanted to build a business based on his cryptography expertise, Plans A though F didn’t work, but Plan G turned out to be PayPal Inc.

Getting to Plan B at Apple

Were Sergey Brin and Larry Page of Google, Howard Schultz of Starbucks or PayPal’s Max Levchin simply lucky? Or is there something rigorous and systematic about their successes that any entrepreneur can learn? Indeed, there is. Let’s let the story of Apple Inc.’s transition from a creative but struggling maker of personal computers to a consumer electronics and music phenomenon show us the way.

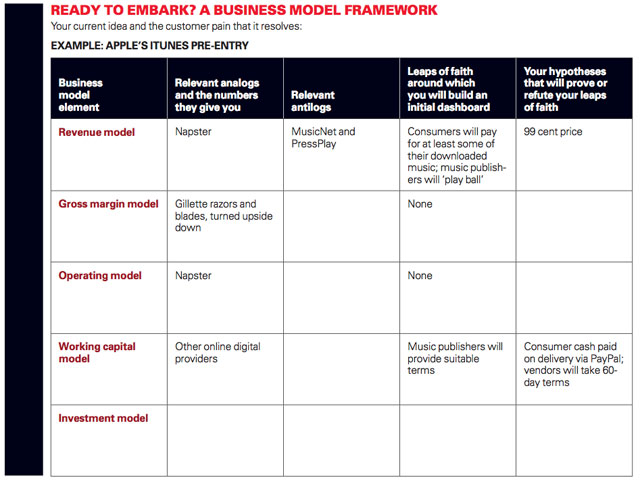

While the iPod and the iTunes store have no doubt revolutionized how people listen to and approach music — not to mention TV and movies — are they really all that new after all? Consider Sony Corp.’s Walkman: It made music personal and portable back in 1979! By 2000 Sony had sold more than 300 million Walkmen. Then there was Napster Inc., another analog, whose 26 million users were downloading music one tune at a time (illegally, as the courts eventually decided). But analogs — predecessor companies that are worth mimicking in some way — are only part of the Apple story. For Apple there were antilogs, too: predecessor companies compared to which you explicitly choose to do things differently, perhaps because some of what they did was unsuccessful. For the iPod and the iTunes store there were several important antilogs. There were MP3 players like the Rio, which sported clunky user interfaces. There were online music stores like MusicNet and Pressplay, whose very limited music selection and limited rights limited their appeal to music lovers.

For Apple, there was one more analog that put all the pieces together, courtesy of The Gillette Co.’s razors and razor blades. Gillette sold razors at low break-even prices and made its money selling the blades. Ingeniously, Apple’s Steve Jobs flipped the model. Jobs’s hypothesis was that people would pay for easy to use, licensed downloadable music and that a business model of high gross margins on the iPod with razor-thin margins in the iTunes store would be profitable while keeping the music industry off his back. Jobs showed how well he understands the value of applying an existing idea to his business: “Picasso had a saying: he said good artists copy, great artists steal … and we have always been shameless about stealing great ideas.”

Apple’s revenue on iPod sales in the first year alone was $143 million. When the iTunes store was launched in April 2003, over 1 million songs (at 99 cents each) were downloaded the first day. In 2007, Apple’s music business passed $10 billion in annual revenue, and by 2008, 6 billion tunes had been sold to 75 million customers through the iTunes store. Paying for downloaded music had become cool.

Getting to Plan B in Your Business

How can you break through to a business model that will work for your business? First, you’ll need an idea to pursue. The best ideas resolve somebody’s pain, some problem you’ve identified for which you think you have a solution. In Apple’s case, the pain of music composers and artists and their publishers was both tangible and real. Consumers were enjoying their music but not paying for it!

Next, you’ll need to identify some analogs, portions of which you can borrow or adapt to help you understand the economics and various other facets of your proposed business and its business model. And you’ll need antilogs, too. As we have seen from the Apple story, analogs and antilogs don’t have to be only from your own industry. Sometimes the most valuable insights come from rather unusual sources.

Having identified both analogs and antilogs, you can quickly reach conclusions about some things that are, with at least a modicum of certainty, known about your venture. But it is not what you know that will likely scupper your Plan A, of course. It’s what you don’t know. The questions you cannot answer from historical precedent lead to your leaps of faith — beliefs you hold about the answers to your questions despite having no real evidence that those beliefs are actually true.

Taking the Leap

To address your leaps of faith, you’ll have to leap. Identify your key leaps of faith and then test your hypotheses that you believe hold the answers. That may mean opening a smaller shop than you aspire to operate, just to see how customers respond. It may mean trying different prices for your newly developed gadget to see which price makes sales pop. By identifying your leaps of faith early and devising ways to test hypotheses that will prove or refute them, you are in a position to learn whether or not your Plan A will work before you waste too much time, and money, too!

But what do you actually need to consider when developing your business model? What is it that you hope your analogs, antilogs and some judiciously chosen hypothesis tests will tell you? Every business model needs to quantitatively address five key elements.

- Your revenue model: Who will buy? How often? How soon? At what acquisition cost? How much money will you receive each time a customer buys? How often will they send you another check?

- Your gross margin model: How much of your revenue will be left after you have paid the direct costs of what you have sold?

- Your operating model: Other than the cost of the goods or services you have sold, what else must you spend money on to keep the lights on?

- Your working capital model: How early can you encourage your customers to pay? Do you have to tie up money in lots of inventory waiting for customers to buy? Can you pay your suppliers later, after the customer has paid?

- Your investment model: How much cash must you spend up front before enough customers give you enough business to cover your costs?

Uncovering useful analogs and antilogs, identifying your most important leaps of faith and testing a series of hypotheses to inform all five elements of your business model will give you much of the data you need to craft a possibly compelling business model, at least for Plan A. But a truly viable business model is unlikely to arise in a single “eureka” moment. Getting from Plan A to a viable Plan B, as PayPal’s Max Levchin discovered, is a journey that can take months, even years.

Guiding Your Journey

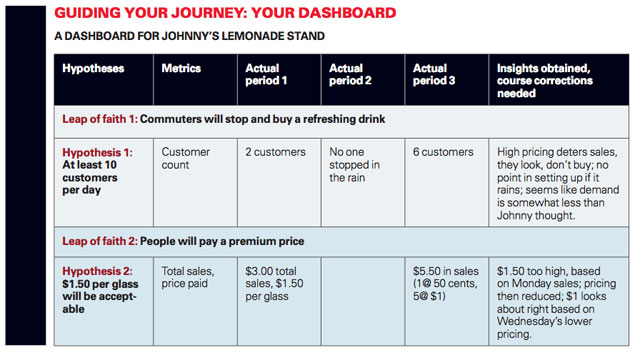

Like any journey that wants to get somewhere, this journey needs a tool to point the way and track your progress, something we call a dashboard. A dashboard drives an evidence-based process to plan, guide and track the results of what you learn from your hypothesis testing. In part, it highlights key indicators of your progress, much as the dashboard in your car tracks key information about your holiday trip to Grandma’s house. But dashboards as entrepreneurs use them are much more than the dashboard in the family car. A dashboard in this sense is also a trip planner to help you determine the best route. It provides a detailed map of the hypothesis-testing journey you will take, as well as making clear the need for any necessary midcourse corrections as your journey unfolds.

Your dashboard serves four key roles:

- It forces you to think strategically about the most crucial issues presently on the table that can — quickly and inexpensively — answer the all-important question, “Why won’t this work?”

- It forces you to think rigorously about how you can examine your leaps of faith by testing hypotheses whose results can be measured quantitatively, most of the time. Numbers are more persuasive than naïve hopes or dreams.

- If one or more of your leaps of faith are refuted by the evidence you collect, the results displayed on your dashboard are visible and dramatic indicators of the need to alter your Plan A and move toward Plan B.

- A dashboard is a powerful tool for convincing others — whether members of your management team, investors or others, even yourself — of the need to move from Plan A to Plan B. If your tenacity or perseverance is questioned, you can point to the evidence to support the move toward Plan B. You are not being erratic or flighty. You are systematically testing hypotheses to prove or refute your leaps of faith, and you are listening to what the data tell you.

A dashboard is a flexible tool for addressing your leaps of faith. It forces you to keep track of the most crucial questions you have about your venture, while keeping your assumptions (often guesses, really) in mind. It focuses your attention and more efficiently deploys your precious time and resources to remove the critical risks. And it provides a way to respond to the real-life data you generate. Moving into the dashboarding stage in developing your business model means moving from spectator — observing others as you gathered analogs and antilogs — to doer.

One Element Can Hold the Key

While all successful business models address each of the five elements, for many great companies, just a single element holds the key. The key element for Google was its eventual revenue model, but initially there wasn’t a revenue model — just a free search engine. Plan B, to license its engine to other portals, wasn’t much better. In order to bring money in, Google’s Plan C — as anyone with an Internet connection knows — provided paid search listings alongside the “objective” ones. Google’s even more successful Plan D built on its proprietary search algorithms to deliver targeted ads to other Web sites, which has generated more than half of Google’s revenue since 2004.

For Ryanair Holdings Inc., the low-cost European airline based in Dublin, the key was its operating model. The Ryanair operating model utilized only one type of aircraft, no free in-flight meals, direct-to-consumer online ticket booking to cut out travel agent commissions and even getting rid of window shades and seat back pockets to decrease the time on the ground between flights. This incredibly efficient operating model has allowed Ryanair to soar past all other European airlines and become Europe’s largest in passenger traffic.

There are many more examples of businesses around the world that have revolutionized their industries by hanging their hat on one key element of their business model. Some of these companies include:

- China’s Shanda Interactive Entertainment Limited: Revenue model

- Japan’s Toyota Motor Corp. and the United States’ eBay Inc.: Gross margin models

- India’s Oberoi Hotels & Resorts: Operating model

- The United States’ Costco Wholesale Corp. and Dow Jones & Co. Inc.: Working capital models

- Luxembourg’s Skype Technologies S.A.: Investment model

For others, such as Spain’s Zara International Inc., combining two or more elements has made their business models particularly difficult to imitate, creating sustainable competitive advantage and an ability to grow rapidly even in challenging industries like retailing. Zara’s is a story of how a carefully crafted combination of sourcing, merchandising and distribution strategies created a unique new pattern of revenue, gross margin and working capital models that enabled Zara to grow like wildfire and take its young fashion-forward customers by storm.

The Zara model revolves around four processes, all tailored for speed — design, production, distribution and sales — resulting in so-called “fast fashion,” where an article of clothing can go from design sketch to the store in less than two weeks.

- Revenue model: Small production runs create scarcity and encourage shoppers to visit Zara often and purchase quickly, before its fast-moving styles disappear.

- Gross margin model: The number of unpopular items is minimized, so markdowns are rare, providing one of the highest gross margins among apparel retailers.

- Working capital model: In return for predictable high-volume business with Zara, its suppliers gave it favorable 60-day terms. With customers buying their clothes with cash or credit cards, Zara has its customers’ cash in hand in less than a week. Fast-turning inventory paired with quick customer cash and slow payment for its merchandise produces an attractive working capital model indeed!

The Cold, Hard Facts

Most business plans assume that almost everything is already known up front — but that is not the case, as our examples have now shown. As the famed American general in World War II, Douglas MacArthur, is reputed to have said, “No plan ever survives its first encounter with the enemy.”

The process articulated here is a healthy alternative to the straightjacket of today’s business planning practices — enabling you to anticipate and move beyond a failing or suboptimal Plan A. It is a process designed for learning and discovering, rather than pitching and selling. It’s a process that may enable you to discover the next Twitter. Most importantly, it’s a process that recognizes and embraces the cold, hard facts: Most often, what ultimately works is not the Plan A that was so persuasively articulated in the original plan. Instead, it’s the unexpected surprise that we call Plan B.

Comments (3)

Fred Noham

Tristan Kromer

kennedy mwinamo