Beyond Outsourcing: Managing IT Resources as a Value Center

Topics

How to best extract value from information technology (IT) resources is a major challenge facing both business and IT managers, particularly as they turn their focus from searching for the competitive benefits of strategic information systems and striving for benefits beyond process reengineering. At the same time, managers are beginning to synthesize lessons from nearly a decade of IT outsourcing. Now astute managers are asking: How can we move beyond leveraging IT for redesigning current business processes to create new business capabilities? What is the best design for organizing our IT activities as a business driver? How can we best exploit the potential benefits of the Inter-net and the World Wide Web for delivering superior value to customers? How should we allocate and manage IT investments? How can we develop a strategic approach to IT sourcing that balances the risks and benefits of insourcing and outsourcing?1 What types of sourcing options should we explore? What truly distinguishes our ability to exploit IT functionality differently from our competitors? How can we continually achieve and sustain the required strategic alignment between business and IT operations? What are the driving principles for organizing IT resources in the twenty-first century?

During the past decade, I have observed and analyzed how companies respond to such questions and challenges. In this article, I synthesize my observations and analyses into a framework for managing IT resources as a value center. I introduce the value center concept, describe its essential features, and highlight its use in reframing the dialogue between business managers and their information systems counterparts on IT’s role in shaping and supporting business strategies. In doing so, I position the value and risks of IT outsourcing as part of the larger challenge of crafting an effective IT strategy.

The Compelling Case for Change

Most managers are painfully aware of the limitations of their legacy technological infrastructure and plan to migrate from their centralized, mainframe technology toward a more decentralized, distributed, multimedia platform. In this arena, they seem preoccupied with the year 2000 conversion problem. Few recognize the potential weaknesses of their legacy administrative architectures. Outmoded IS organizational design and processes, misdirected IS resource allocation criteria, inappropriate IT planning systems, parochial views on outsourcing, and mismatched IT skills with business needs are as critical as obsolete technological platforms. Managers can benchmark, quantify, and analyze the impact of a legacy technology infrastructure, but the implications of an obsolete administrative logic are less obvious until it reaches a critical point — often, without any warning signals.

Three major shifts make a compelling case for rethinking the administrative logic of managing IT resources:

- In the technical arena, there is a rapid migration toward a hybrid (centralized and distributed) multi-media platform to link business processes with suppliers and buyers. At the same time, the fundamental characteristics of the technical infrastructure are shifting from hardware to software standards, for example, Windows-Intel (Wintel) versus Network Computer (NC). A manager half-jokingly remarked: “We used to define our technical standards in terms of being IBM-compatible; now we refer to it as being Bill Gates-compatible!” More seriously, there is increased reliance on standardizing business processes with software packages such as SAP R/3, Oracle database, or Net-scape Navigator, thereby anchoring the infrastructure on software choices. The developments and evolution pertaining to the Internet and intranets also have significant implications for the design and rapid adaptation of the technical infrastructure.

- In terms of business shifts, managers have renewed expectations of business value from IT investments. Somewhat sobered by the unrealized (and unrealistic) expectations of the 1980s, managers are cautiously optimistic about the role of IT in driving new business capabilities. Leading retailers such as Wal-Mart, Sears, the Gap, Macy’s, and others are focusing beyond efficiency benefits in their supply chains toward leveraging their unique knowledge and expertise to fine-tune their marketing strategies. Financial institutions such as Citibank, American Express, BayBank, Fidelity Investments, and Charles Schwab are evolving from their traditional focus on back-office efficiency to exploring new ways to deliver service through the Internet. Logistics companies like Federal Express and UPS are leveraging their IT capabilities to derive new sources of revenues and margins. Indeed, in nearly every market, there is a range of IT-enabled business capabilities beyond efficiency improvements.2

- Finally, there are fundamental changes occurring in the external market for IT products and services. No longer can leading IT organizations be passive buyers of standard offerings in the market in the wake of the exploding number and type of business arrangements. These include multiyear outsourcing relationships with one primary vendor (for example, Kodak and IBM, Xerox and EDS, General Dynamics and CSC), strategic sourcing involving multiple vendors to simulate competitive pressures and continuous benchmarking (British Petroleum Exploration-BPX and three vendors, Sema Group, SAIC, and Syncordia; J.P. Morgan and the Pinnacle Alliance), joint development (Wal-Mart and Microsoft), cross-equity investments (Swiss Bank and Perot Systems), and joint ventures (Eastman Kodak and IBM joining to create Technology Services Solutions for multivendor PC maintenance and support; CSC and CNA Financial to create an entity that delivers IT services in the life insurance market).

The Concept of a Value Center

The value center is an organizing concept that recognizes four interdependent sources of value from IT resources (see Figure 1). It allows companies to differentiate the management approaches needed to realize these distinct sources of value. The cost center has an operational focus that minimizes risks with an emphasis on operational efficiency. The service center, while still minimizing risk, aims to create an IT-enabled business capability to support current strategies. The investment center, on the other hand, has a long-term focus and aims to create new IT-based business capabilities. Finally, the profit center is designed to deliver IT services to the external marketplace for incremental revenue and for gaining valuable experience in becoming a world-class IT organization. Thus cost and service centers seek to minimize risk by focusing on current business strategies, while investment and profit centers focus on maximizing opportunities from IT resources and shaping future business strategies. Collectively, the four components balance the role of IT in today’s operations with the requirements in tomorrow’s business context.

{kind=link}

Cost Center

Companies have historically managed most IS activities as a cost center: they allocated resources on the basis of rigid, quantitative payback criteria (reduction in operating costs or increased margins); they operated the infrastructure, like the data center and telecommunications network, as a utility independent of business strategy; they designed the IS organization as a support unit with a reporting relationship to the finance function; and they assessed IS performance using cost-based indices.

The cost center is the first building block of the value center and is valid when the following three conditions hold. One, the value the firm expects from IT resources is independent of its business strategy (for example, the operational infrastructure involving most data centers, telecommunications network, and routine maintenance). Two, the firm well understands the nature of the relationship between input and output (for example, the impact of increasing the operating budget by a factor of two on output metrics). Three, the firm has external comparison standards on relevant performance metrics — like cost per million instructions per second (MIPS), maintenance cost per workstation, or training cost per employee on a new operating system — that are available and meaningful.

However, companies have applied cost center logic even when the above three conditions did not hold. In general, companies have been disappointed with their ability to manage the cost center activities — which have become the cornerstone of IT operations in most organizations. Hence, it is not surprising that they have enthusiastically embraced the possibilities of outsourcing. Indeed, most outsourcing discussions and decisions reflect a cost center perspective. In 1989, East-man Kodak Company pioneered the current dominant model of outsourcing when it transferred a significant part of its IT infrastructure and human assets to three different vendors. Subsequently, several major corporations3 have outsourced at least some parts of their IT operations. More than sixty contracts, each valued at $200 million, have been awarded since Kodak’s pioneering move.4

Should cost center activities always be outsourced? The answer is clearly no. But managers should evaluate every cost center activity for possible outsourcing by asking:

- How large is the cost parity gap? What is the impact of this gap on business performance? Benchmarking the cost levels with major competitors and leading vendors provides a useful external frame of reference. The ultimate purpose of benchmarking is to assess the impact of the cost parity gap on business performance.

- Is it worthwhile investing to close the cost parity gap? What are the risks and rewards of investing incremental resources to close the projected gap? Often, looking at cost center activities in isolation leads to a different decision than looking from a broader portfolio viewpoint. Can we reassign our internal resources from cost center activities to higher value activities? When Xerox announced its outsourcing, CIO Pat Wallington said, “We want to focus our internal staff on moving us to the environment that will support us tomorrow.” John Cross, CIO of BPX, said it best: “We have to step out of the kitchen and let someone else do the cooking,” implying that IT management should focus on new business capabilities through IT rather than on operating and owning the technology.5

Obviously, decisions on investment levels and sourcing options require a more complete understanding of the value from IT resources beyond cost. Next I develop the other building blocks of the value center that complement the more well-understood cost center.

Service Center

The service center is the second building block, with a focus on IT-enabled business capabilities that drive current business strategy. These capabilities are created not with a focus on lowest possible cost but as drivers of competitive advantage.

Consider Frito-Lay’s business relationship with McCormick & Co. In the early 1990s, Frito-Lay managers could use Lotus Notes® internally, but not with their trading partners, because interorganizational transactions were based on structured data standards, not Lotus Notes. Frito-Lay’s internal IS organization created a specific Notes application to support business exchange with McCormick. This application allowed Frito-Lay and McCormick to exchange images and memos in addition to structured data, and McCormick managers could analyze Frito-Lay’s inventory information from multiple perspectives. Both achieved lower inventory levels and could be more confident of the interpretability of data being exchanged. The company could not have justified such a capability with cost center logic because it reflects the specific business objective of reduced operating costs through a redefined partnership with a key supplier.

More recently, Lufthansa Airlines deployed a new version of its maintenance system that allows its maintenance engineers at geographically dispersed airports to work simultaneously on aircraft malfunctions over ISDN and ATM network links. The multimedia platform allows many users to jointly view and edit documents, video, and still images, while transmitting video images of faulty aircraft components for problem analyses to specific experts. This capability was not driven by cost center considerations but as a means to minimize downtime and improve its punctuality and reliability. Another example is Bank of America’s development of its customer targeting system to give its sales and service managers better predictive models on likely customer response behavior than its competitors had.

Sears Products Services — the nation’s largest consumer repair and service organization — has equipped its 14,000 service technicians with mobile computing devices to vastly increase customer service by automating routine tasks and providing a wide range of information.6 Similarly, Hale & Dorr, a Boston-based law firm, deployed a multifaceted business platform — a home page on the Internet, ISDN links, high-speed servers, voice-recognition systems, and laser disk-driven multimedia presentations — so its attorneys could have access to information and leverage their internal expertise to their advantage in the courtroom.7 Such a business capability was motivated by the need to deliver superior legal service and could not have been justified solely on a strict cost center basis.

What differentiates a service center from a cost center? First, there is no a priori classification of activities into cost or service centers. For instance, help desks can be considered a cost center initiative if the expected benefit is not directly related to business strategy (like responses to queries on company policies or standard software problems) or as a service center if the expected benefit is directly related to the business strategy (such as a consulting or a legal organization’s need to tap into a knowledge and expertise base). Similarly, the development of a Web site can be seen as a cost center (establishing a presence on the Internet) in one setting, while it is clearly a service center in companies that view the Web as a platform for delivering superior value to customers (creating market differentiation through electronic commerce).

Second are the performance criteria for allocating resources. A service center compels the use of specific business-unit objectives, not generic indices, to allocate key resources and assess performance. Thus a company can assess a help desk not in terms of operating costs but in terms of the degree of perceived contribution to specific business processes. It can assess intranet applications in terms of business results rather than administrative cost savings. Companies such as Federal Express, Charles Schwab, and American Express assess IT-enabled customer service capabilities using relevant business indices (end-customer satisfaction, customer loyalty, and repeat purchases) rather than cost indices (cost displacement through labor substitution or cost-per-service call) alone.

Third is the IT organization’s degree of service orientation in understanding IT’s role in the business processes. If IT managers proactively bring their skills, knowledge, and experience to suggest, demonstrate, and create IT-enabled business capabilities (customer service, logistics, or new product development), they have a service center orientation. For example, at Astra-Merck, “IT people . . . live and work in the process areas that make up [the] business. They are not isolated in a support department.”8 Similarly, when IT managers are catalysts for redesigning business processes and have performance and compensation stakes in the creation of new business capabilities, they indeed have a service center orientation.

Investment Center

The investment center is the third component of the value center. In contrast to the first two, the investment center has a markedly strategic focus and seeks to maximize business opportunity from IT resources. A forward-looking R&D component is particularly advantageous when the business is undergoing a discontinuous change, and the new business model is likely to be grounded in IT functionality.

Several companies have formed advanced technology groups charged with the task of scanning, selecting, evaluating, and transferring the knowledge about emerging technologies to the business. For instance, the advanced technology group at SmithKline Beecham, a global pharmaceutical company, created a multi-media training system in the early stages of the technology’s evolution with demonstrable gains in learning efficiency and job effectiveness. USAA, a leading player in the insurance and financial services market delivering services to military families, has a unit that scans for emerging technologies that could significantly enhance its customer service capability. More recently, CIGNA, a leading insurance company, created a forty-person IS R&D organization with a focus on “looking at technologies that are ripe for development.”9 There are similar units in leading companies such as Federal Express, American Express, Wal-Mart, Johnson & Johnson, Citibank, Merck, and others.

Management’s challenge is to ensure that such groups do not become aggressive champions of specific technologies but focus on specific business capabilities that leverage leading-edge technologies. The CEO in a global financial institution charged a joint business-IT team to evaluate options for serving retail customers using a “nontraditional” channel. He did not want the team driven by any specific technology such as the Internet but focused on delivering enhanced customer value. His challenge to the team was: “Create a new business model, even if it destroys our current capabilities. I want us to know very clearly how our business model could be made marginal (or at worst, obsolete) by someone.” The team is now in the midst of constructing and assessing a wide range of business models based on alternative scenarios reflecting different technological capabilities.

Another practice within the investment center is technology licensing — often seen in the form of beta testing of emerging technologies. It is expensive and time-consuming but could provide an edge over competitors if the technologies create new business capabilities. Beta testing of early versions of scanning technologies has helped insurance and credit card companies. Similarly, early experimentation with electronic data interchange helped Wal-Mart explore the potential for enhancing operational efficiency in the supply chain. Now several companies are experimenting with Sun’s Java applets on the Internet. Beta testing of technologies is most useful as a form of advanced intelligence to signal the potential obsolescence of current business capabilities or the creation of new capabilities.

It is possible for companies to go beyond passive participation in beta tests of standard technologies and actively participate in creating differential capabilities. Companies must make a much more aggressive investment commitment and participate in a range of activities such as technology licensing, joint development, equity investments, and joint ventures (see Figure 2). During the first half of the 1990s, several companies entered into technology alliances. American Express delivers its electronic interactive services to members, like downloading monthly statements into personal finance programs (such as Quicken), through its unique relationship with America Online. Wal-Mart is moving from physical stores into on-line retailing through its special relationship with Microsoft. McGraw-Hill launched its custom publishing initiative, Primis® through alliances involving Kodak scanning technology and R.R. Donnelley’s flexible binding capability. Indeed, equity investments and joint development are popular ways to access critical technology functionality.

{kind=link}

Some leading companies are beginning to charter their investment centers with an eye toward creating new, future-oriented business capabilities rather than investing in isolated technologies per se. Robert Martin, ex-CIO of Wal-Mart and president and CEO of Wal-Mart International, noted: “When I’m presented with a proposal to invest in new technology, I look beyond the financial commitment I’m asked to make today and try to understand what my follow-on commitments will be. . . . We have to know how we will get from the investment we make in today’s generation of technology to the next generation.”10 Companies should base resource allocation to the investment center on a multistage creation of business capabilities under uncertainty and market shifts rather than a single “go-no go” investment in technology.11 Thus the investment center has a two-pronged role: early identification of the likely obsolescence of the current business model and the proactive creation of the new business platform. Long-term business performance in the fast-changing marketplace is dependent on the successful operations of the investment center.

Profit Center

The profit center is the fourth building block of the value center, with a focus on delivering IT products and services in the external marketplace. Long advocated, previously abandoned, and scorned by many when focused only on financial benefits, its importance can be appreciated when nonfinancial benefits are also considered. When properly conceived and implemented, an IT organization can have an external focus on opportunities for market-based benchmarking, rapid learning, confidence building, and incremental revenue and margins.

During the past five years, several companies such as USX Corp., Humana, Mellon Bank, Sears Roebuck, Kimberly-Clark, Boeing, and others have attempted to compete in the IT marketplace, with limited success. So, why renew the call for a profit center? The main impetus is the opportunity to pool complementary skills and resources through a wide range of mechanisms to pursue profit center opportunities (see Figure 3).

{kind=link}

Consider a case in which a company has either the best-of-industry or best-of-breed technological proficiency but does not have a major commercial intent to leverage its world-class proficiency across industry and geographical boundaries. This occurs when a firm realizes its proficiency in areas that are tangential to its primary business purpose; nevertheless, it seeks to realize its full value. In such a setting, the company would find it advantageous to consider licensing its proficiency to a commercial entity, without distracting the internal IT operations. Wal-Mart’s licensing arrangement with IBM to market its best-of-industry supply chain processes is a case in point.

Now, consider a case in which a company with the best-of-industry proficiency has a commercial intent to leverage its IT proficiency to create new lines of business operations. An attractive option is to go beyond licensing its expertise to create a distinct market-facing unit either on its own or through alliances. In 1995, Liberty National Bank and Trust created a subsidiary, Liberty Payment Services, to provide an overnight check-clearing service for banks. Liberty’s check-processing capability is combined with the logistics capability of UPS Worldwide Logistics to achieve lower cost and faster speed than offered by the Federal Reserve System. Similarly, Holiday Inn created its hotel reservation business as a separate entity based on its relationship with IBM’s ISSC to serve the entire hotel and hospitality marketplace.

The investment banking division of Swiss Bank Corporation (SBC), SBC Warburg, has formed a unit to market IT products and services to the global financial marketplace as part of a complex cross-equity deal with Perot Systems. SBC has a 24.9 percent equity stake in Perot Systems, while Perot Systems took a 40 percent stake in an IT-oriented subsidiary of SBC, Systor AG, which handles the back-office functions.

In November 1996, Computer Sciences Corporation (CSC) and CNA Financial agreed to establish a subsidiary to handle information processing requirements in such areas as claims, new policy issuance, accounting and record keeping, and tax and related administrative processes. The new entity is expected to function as a subsidiary of CNA, delivering services in the marketplace; CSC has no equity stake but has the rights to share in profits based on the entity’s performance.

There are many examples of companies that have a best-in-class IT proficiency and a commercial intent to create new products and services — often, unrelated to the companies’ traditional business intent. Popular examples are AMR Corporation’s Sabre unit, which has recently been spun off as a separate business to become a full-fledged competitor in the travel information services marketplace; General Motors’ spin-off of EDS; and the unleashing of Allegiance Corporation, the distribution and materials management arm of Baxter Healthcare Corporation. In all these cases, the parents realized that the best-in-class technical proficiencies within their respective units could not be fully nurtured and exploited within the traditional corporate structure. The newly formed entities are now free to fully exploit their profit center intentions; initial indications are that the firms are performing well.

Whenever I suggest the role of profit center as a key component of the value center, I get two objections. The first is that it diffuses the business purpose — especially given the renewed emphasis on core competencies.12 Referring to Figure 3, I discuss options for realizing the potential value without necessarily diverting valuable internal resources. Thus licensing arrangements are more attractive when the commercial intent from organizing IT as a profit center is peripheral to the business purposes. Delineation of separate units, as in the case of CNA Financial and SBC Warburg-Perot Systems, clarifies the specific roles and responsibilities. The second objection pertains to the difficulty of ensuring that companies do not inadvertently give away important IT competencies (the so-called crown jewels) to competitors in the open market. I overcome this valid objection by judiciously delineating those few IT-enabled business capabilities that truly provide unique value in the marketplace from those that are, at best, a competitive necessity. A disciplined view about the scope and relative emphasis of the profit center within the overall value center is absolutely necessary.

Ultimately, a profit center is not attractive when viewed only as a source of incremental revenue. The president of a major chemicals distribution company remarked: “The sales from the profit center is a roundoff error on my sales numbers. I don’t want to be bothered by it.” He is right. It is important to view profit in broader terms such as the valuable experience and market knowledge gained by the IT managers. In the case of Barclays Bank in the United Kingdom, the IT organization’s track record in competing successfully in the external market significantly enhanced its internal standing with the business managers. CEOs are more favorably disposed to the profit center in the value center equation when the spillover nonfinancial benefits are included than otherwise.

For a summary of the four components of the value center with important characteristics, see Table 1, which shows that the value from each component is distinct, requiring different management approaches.

{kind=link}

Realizing Value: Reframing the CEO-CIO Dialogue

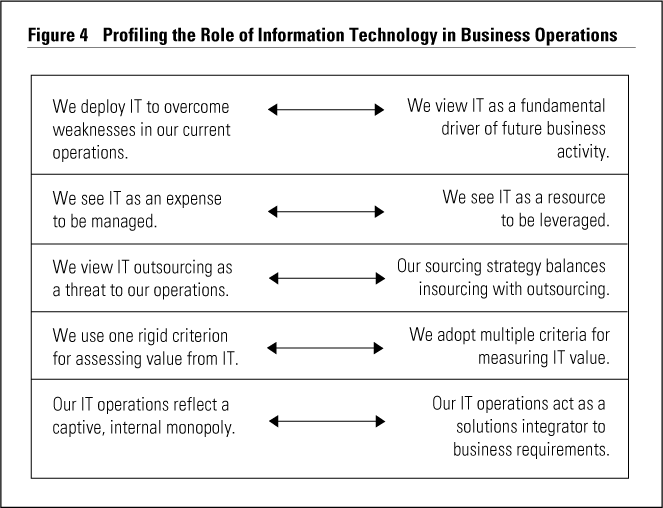

After profiling your company’s current positions on the role of information technology, profile the desired positions (see Figure 4). If your desired profile is noticeably to the right of the current profile, you need to manage IT operations from a value center perspective. This is the case in many organizations that are in the midst of reorienting their business strategies and aligning their business and IT strategies. The characteristics on the left of the table reflect the traditional cost-center logic, while those on the right reflect the emerging value-center perspective. The following questions help reframe the discussion between business and IT managers on the value center concept and are useful in transforming IT operations.

{kind=link}

The Raison d’être: Create Business Capabilities or Rectify Operational Weaknesses?

Is the fundamental business purpose of the IT organization primarily to deploy IT capabilities to rectify weaknesses in the current operations or is it to create future business capabilities? As part of MIT’s Management in the 1990s research program,13 I developed a model of IT’s role in business operations.14 Using the model, companies can compare and contrast two different purposes of IT operations: rectification of past weaknesses and creation of future capabilities. The former focuses on overcoming weaknesses inherent in the traditional business model through the use of IT. The latter seeks to define the future operating state (in terms of business scope and pattern of alliances and relationships, including out-sourcing) before developing the overall logic for process redesign and the purpose of IT operations.

Companies have paid far more attention to deploying IT for the rectification of past weaknesses rather than for the creation of future capabilities. Thus cost and service centers have been management’s dominant focus. If future operations are merely a linear extrapolation of the past, then overcoming the deficiencies in the current design could create a foundation for the future. On the other hand, if the information revolution destroys traditional sources of advantage while creating new sources, companies need to do more than rectify current weaknesses. This requires a value center profile that goes beyond cost and service centers and includes an investment center — especially for leveraging newly emerging functionality.

So, both business and IT managers need to jointly articulate the raison d’être for IT operations. Some leading companies have recognized the advantages of a broad view of value from IT resources and are articulating their IT mission accordingly. Hallmark Cards Inc. is developing its strategy for the emerging multi-media marketplace, which could render its traditional products and associated business model of printing and distributing greeting cards obsolete. It is selectively exploring a range of activities within the investment center while it manages its traditional supply chain requirements through a mix of cost and service centers. Similarly, as the Encyclopedia Britannica shifts its strategy from selling bound volumes through door-to-door sales toward electronic on-line access and related services, its value center profile should emphasize an investment center. Other examples with marked investment-center emphasis include Levi Strauss’s customized jeans (Levi’s Personal Pair), Boeing Co.’s innovative approach to designing and manufacturing its 777 model, Charles Schwab’s wide variety of gateways for customer transactions, and Federal Express’s attempt to create a niche in on-line services through its integrated electronic commerce and catalog services. Articulating the IT mission in terms of the relative emphasis on the different components of value center is senior management’s first major task.

Allocating Resources: One Rigid Yardstick or Many Distinct Criteria?

A second, thorny question for both business and IT managers is: “How much should we spend (or invest) on IT to support our value center profile?” There are contentious discussions on such issues as: Are we spending enough? Are we best leveraging the IT resources that produce business value? How well are we balancing today’s needs with tomorrow’s requirements?

Unfortunately, most companies seem to look outward (seeking to imitate best practices) rather than focus inward (to better understand IT’s role in its business operations). By benchmarking, companies can take comfort in the fact that their level of input (for example, IT budget) or output (for example, cost per workstation) is approximately on par with peers. Such general benchmarking fails to recognize the differences in the value center profiles across the companies within the benchmarking pool. Indeed, finalizing the funding level for a value center based on general benchmarks that do not recognize the differences in value center profiles is dysfunctional and limiting.

Wal-Mart did not decide its level of IT investment on the basis of the IT spending levels of Sears or Kmart. If it had, Sears and Kmart would probably still be leaders. Wal-Mart’s retailing strategy was to leverage IT functionality not only for increasing the efficiency in its supply chain but also for effectively replicating successful experiments across its network of stores on a continuous basis. Wal-Mart’s spectacular growth in sales and profits during the past decade is based on its ability to rapidly learn from its numerous ongoing experiments. Store managers are connected through a sophisticated, multimedia knowledge network so they can exploit their collective expertise and continually fine-tune marketing strategies. Wal-Mart’s particular choice of how IT could contribute to its business strategy influenced its funding strategy.

Moreover, investments in IT should not be considered in isolation from complementary investments required to create specific IT-enabled business capabilities. As Wayne P. Yetter, the CEO of Astra-Merck, observed: “We do not consider technology investments in isolation. We look at capabilities, such as developing drugs faster or providing customers with service they can shape themselves. If technology is necessary to make a capability work, then technology investments are part of the package.”15 Such an approach reflects a fundamental belief that IT is only a piece — albeit an important one — of business capabilities and is consistent with an options view of investments.

The value center approach behooves using different criteria to allocate IT resources to the different components. Capabilities based on cost center initiatives are allocated resources based on quantitative, financial payback criteria with appropriate external benchmarks. Those capabilities reflecting the service center are justified based on a specific business plan using a mix of financial and strategic considerations. Business managers quantify and justify the link between IT-enabled business capabilities and marketplace performance to their appropriate business review boards and not to technical committees.

An investment center requires a long-term strategic focus on new business capabilities rooted in a wide array of technological developments. Creation of new capabilities might involve various initiatives such as selective participation in beta tests of emerging applications, preemptive licensing of high-potential developments, joint development with vendors, minority equity investment in start-up ventures, and potential acquisitions of companies with key complementary capabilities. Companies base the selection of particular mechanisms for an investment center on strategic considerations and support them with appropriate resource allocation criteria. Funding for the profit center is based on sound business cases like any other new business launch, with the caveat to also recognize possible nonfinancial benefits.

Acquiring Capabilities: Outsourcing as Taboo or a Strategic Sourcing Network?

Outsourcing is no longer a taboo topic among senior managers, including IT professionals. Now the question is not whether to outsource but what to out-source, as companies redirect valuable internal skills and capabilities to high value-added areas.16 The ten-year $3 billion outsourcing relationship between Xerox and EDS is structured so that while EDS manages the operational components of the IT infrastructure, Xerox concentrates on new application developments on the new platform. Xerox’s CIO Pat Wallington remarked, “I view outsourcing as a part of the transformation strategy.” Similarly, Henry Pfendt, former director of IT management at Kodak, noted, “Through outsourcing, it is possible to transform the IT operations from a service deliverer to a broker and facilitator of needed services for business managers.”17

How can companies develop a sourcing strategy to support the value center profile? No one company can — or, indeed, should — source all capabilities for its value center internally. The sourcing strategy is to balance the required skills and competencies from internal and external sources. Outsourcers are able to bring their expertise to improve cost levels of data center operations, systems maintenance, and telecommunications networks as well as to enhance help-desk services and system upgrades. This frees valuable internal resources for higher value-added activities. Owens-Corning contracted with Hewlett-Packard to manage its legacy systems so that it could concentrate its internal efforts on rapidly implementing its chosen SAP R/3 enterprise software and creating a new operating platform for growth.

A balanced approach to sourcing helped one insurance company recognize that its skills best matched the cost and service centers approach, while there was a gap in skills for the investment center approach. Instead of expanding its internal skill set (requiring significant additional resources to match the required quality), the company identified a series of strategic relationships with vendors to support investment center requirements. In contrast, a global financial services company aggressively examined the feasibility of out-sourcing cost and service centers while migrating and transforming its internal operations to support the investment center and even parts of the service center — where external sourcing might not have yielded maximum benefits. Similarly, Xerox outsourced its IT requirements in the cost and service centers to EDS, while forming a different set of relationships with Oracle and others to create new business capabilities reflecting investment and profit centers.

More recently, J.P. Morgan announced that it has developed a consortium, Pinnacle Alliance, with CSC as the primary partner and associated players —AT&T Solutions, Andersen Consulting, and Bell Atlantic — to manage its data centers and voice, data, and software services. Peter Miller, cohead of corporate technology at J.P. Morgan, remarked: “Technology is moving very rapidly, and the constant challenge to get technological skills up to speed is one that any single company will have a difficult time achieving.”18 At the same time, the company will direct internal resources at developing complex computer programs for securities trading and other leading-edge financial services.

Profiling the value center in terms of the relative emphasis on the four components of value allows managers to systematically evaluate different sourcing options. IT managers seem to feel that IT out-sourcing will seriously diminish the scope and power of the IT unit relative to other units. This is true if the overall value expected from IT resources is predominantly cost related and independent of business strategy. It is clearly not the case in the emerging information-age economy. So the issue is not one of insourcing versus outsourcing but of carefully balancing different sourcing options.

The Xerox-EDS relationship is indeed a portfolio of multiple independent agreements reflecting different sources of value. The Xerox-Oracle alliance is focused on the investment and profit centers. SBC Warburg has two different relationships with Perot Systems — a twenty-five year, $250 million annual contract for the data center operations, reflecting the cost and service centers, and a cross-equity agreement for the investment and profit centers. On the other hand, J.P. Morgan decided to direct its internal skills at investment center activities and outsource its cost and service centers to the Pinnacle Alliance. By sourcing cost and service center activities through the alliance, J.P. Morgan has been able to concentrate its internal resources on creating distinctive capabilities so it can outperform its rivals in the financial services marketplace.

In putting such principles into practice, a clear delineation of decision rights among decision makers is the most important requirement. Companies must specify who has what areas of responsibility in making decisions about IT, and under what conditions. For instance, when Xerox entered its multiyear agreement with EDS in 1995, it retained all important decisions pertaining to “information management functions that focus on strategy, architecture, and applications”19 while outsourcing operational decisions to EDS. In contrast, Philips Electronics retained operational decision rights over its IT infrastructure, while transferring decision rights on application development to an external entity.

Clear decision rights are particularly important because the new form for the IT organization is more likely to resemble a network of multiple relationships rather than the traditional command-and-control hierarchy. In some areas, it makes sense to assign joint decision responsibilities, while, in other cases, it is more prudent to specify sole responsibilities. Joint, shared decision responsibilities, while appealing, often require more of managers’ time and should be reserved for only those specific areas needing multiple viewpoints.

Thus the CIO’s role will grow and change from being an owner and controller of predominantly internal IT assets to orchestrating a strategic sourcing network of relationships to deliver required support to the business managers.

Assessment Approach: Single or Multifaceted Criteria?

How to assess value from IT resource deployment is the fourth and perhaps most contentious issue. Companies have abandoned the search for one universal measure of business performance valid under all conditions (such as market share, return on investment, assets, or equity) and recognized the need for multidimensional measures. They include quantitative (e.g., return on equity) and qualitative (e.g., corporate reputation, quality) indices, internal (business growth rate) and external (e.g., growth rate relative to market) measures, and accounting (e.g., cash flow and liquidity) and financial market (e.g., market value added) measures. The use of a balanced performance measurement that is tied to strategic thrusts is gaining popularity.20 Unfortunately, companies are still preoccupied with the search for a unidimensional measure of IT value, because of the historic emphasis on the cost center and the predisposition to deploy IT resources to enhance operational efficiency. Despite obvious limitations, companies have not abandoned using a single, dominant cost-oriented metric of IT value. Indeed, productivity enhancement through IT is still a holy mantra within the IS professional community.

The value center is predicated on the need for multiple, distinctive metrics for the four components. A cost center is assessed using cost metrics such as efficiency enhancements or labor substitution and might be anchored with appropriate external benchmarks (best-in-industry levels and best-of-breed levels — typically found in other industries or among leading outsourcing providers). A service center is assessed through business indices specified by the business managers and, where feasible, compared with peer groups in other industries. An investment center is assessed through a mix of strategic and quantitative indices reflecting the creation of new business functionality. A profit center is assessed in terms of target profit indices and qualitative learning and confidence-building opportunities. In these two centers, given their strategic emphasis, companies can selectively use external benchmarking to gain possible insights into how to enhance these sources of value.

Ultimately, performance criteria should be directly related to the value center profile developed as the first item on the discussion agenda. Otherwise, companies fail to achieve internal consistency between strategy and performance assessment.

Organizational Logic: Internal Captive Monopoly or a Solutions Integrator?

The final question relates to the logic of IT organization. When invoking the value center concept to design the IT organization, companies have several questions: Who has overall responsibility for the value center? Should all four components of the value center be under the CIO? Who is responsible for the integrity of the IT architecture? What are the working organizational relationships among the different components of the value center? Obviously, it is impossible to deal with all organizational design questions in sufficient detail here. I offer some initial ideas for designing the IT organization as a solutions integrator. At a minimum, companies need to clearly shift from the historical dominant view of an internal captive supplier.

The organizing logic of a solutions integrator works best when supported by five guiding principles:

- Companies recognize the ownership of IT as a strategic resource by business managers, who have the primary responsibility for specifying IT’s role as part of the overall business capabilities.

- Companies assign an overall custodian of IT architecture, which is viewed as the underlying engine for the overall business processes. When multisourcing with a wide range of providers, it is important to specify who has supreme authority to resolve conflicts involving specific applications and the overall architecture. The IT organization as custodian works well when it is seen not as a technology czar but as a valued business partner; Johnson & Johnson has assigned the overall enterprisewide responsibility to the corporate office of information technology. When a corporate IT office does not have the required credibility, a joint decision-making body composed of business and IT managers — charged to act in the best interest of the organization — is a good alternative.

- The IT organization is a solutions integrator —distinguished from system integrator or system builder — implying specific emphasis on integrating the various components to deliver business solutions. Ownership of assets and technical focus are not as necessary as the IT organization’s ability to source the various pieces (technology as well as complementary drivers) to deliver business solutions.

- Business managers seek the IT organization as their primary source for IT solutions. However, they have the right to source directly from an external entity when they believe that they are not receiving the required solution from their primary source.

- The design and deployment of processes is continuously aligned with business and IT plans so that, whenever possible, sourcing from external providers is coordinated across different business units.

In the right organizational climate, IT managers can move from having captive demand for their technical services toward earning a right to contribute to business capabilities. Over time, the solutions integrator receives a revenue stream commensurate with its value-added to the business, a far cry from the detached, technically focused, cost center operations with penalty clauses attached to service-level agreements.

Conclusion

Companies are at a critical stage in the management of IT resources. As businesses develop their strategies in the information economy, there is more emphasis on technology-enabled capabilities — not only for operational efficiency but also for strategic effectiveness. There is a need for a different approach to managing IT resources that goes well beyond outsourcing. In this article, I develop a framework for decomposing the components of value from IT resources. I recommend that every organization focus on the four possible sources of value from IT resources. Their relative importance is clearly dependent on the specific business context. Indeed, the relative mix among the four components reflects the strategic role for IT within a particular business and will undoubtedly change over time. The implementation challenges are to ascertain how best to source the required capabilities and to design and manage processes with business and IT managers in order to realize business advantage. Successful companies will leverage their IT resources beyond efficiency enhancements through a cost center and realize a broad range of business benefits through a value center.

References

1. For a recent discussion on the value of selective outsourcing, see:

M. Lacity, L. Wilcocks, and D. Feeny, “The Value of Selective IT Sourcing,” Sloan Management Review, volume 37, Spring 1996, pp. 13–25.

For an overview of the risks of outsourcing, see:

M.J. Earl, “The Risks of Outsourcing IT,” Sloan Management Review, volume 37, Spring 1996, pp. 26–32.

2. See T. Davenport, Process Innovation (Boston: Harvard Business School Press, 1992);

M. Hammer and J. Champy, Reengineering the Corporation (New York: Harper Business, 1993);

N. Venkatraman, “IT-Enabled Business Transformation: From Automation to Business Scope Redefinition,” Sloan Management Review, volume 35, Winter 1994, pp. 73–87; and

D. Tapscott, Digital Economy: Promise and Peril in the Age of Networked Intelligence (New York: McGraw-Hill, 1996).

3. Leading companies include: McDonnell Douglas, Continental Bank, British Petroleum, Philips Electronics, Inland Revenue in the United Kingdom, Xerox, Blue Cross/Blue Shield of Massachusetts, National Car Rental, J.P. Morgan, Salomon Brothers, Campbell Soup, Swiss Bank, and DuPont.

4. Kodak’s move indeed elevated IT outsourcing as an acceptable administrative practice. For a technical discussion on the diffusion of this phenomenon within the United States, see:

L. Loh and N. Venkatraman, “Diffusion of Information Technology Outsourcing: Influence Sources and the Kodak Effect,” Information Systems Research, volume 3, December 1992, pp. 334–358.

For a recent discussion on the state of IT outsourcing, see:

“Outsourcing Megadeals,” Information Week, 6 November 1995, p. 10.

5. CSC Index Foundation, “New Perspectives on IT Outsourcing” (Cambridge, Massachusetts: report #105, December 1995), p. 10.

6. “Sears Hit the Road with Wireless Devices,” Computerworld, 29 May 1995, p. 6.

7. “Law Firm Thrives on Bleeding Edge,” Computerworld, 25 September 1995, p. 73.

8. W.P. Yetter, president and CEO of Astra-Merck, quoted in:

“The End of Delegation? Information Technology and the CEO,” Harvard Business Review, volume 73, September–October 1995, p. 169.

9. “CIGNA Creates Top Technology Post,” Computerworld, 10 July 1995, p. 20.

10. Quoted in:

“The End of Delegation” (1995), p. 162.

11. Some research is underway at Boston University Systems Research Center by Professor Nalin Kulatilaka and his colleagues on applying the options thinking to IT investments. This approach provides valuable insights on the investment management process under conditions of uncertainty.

12. See, especially:

J.B. Quinn, Intelligent Enterprise (New York: Free Press, 1992); and

G. Hamel and C.K. Prahalad, Competing for the Future (Boston: Harvard Business School Press, 1994).

13. M. Scott Morton, The Corporation of the 1990s (New York: Oxford University Press, 1991).

14. Venkatraman (1994).

15. Quoted in:

“The End of Delegation” (1995), p. 169.

16. See, for instance:

Quinn (1992).

17. Personal conversation, June 1992.

18. “J.P. Morgan Allies with Four Firms,” Boston Globe, 14 May 1996, p. 55.

19. News release, 28 March 1994.

20. R. Kaplan and D. Norton, The Balanced Scorecard: Translating Strategy into Action (Boston: Harvard Business School Press, 1996).